2023 Q3 Web3 Primary Market Review and Track Analysis: Gradual Bull Market, How to Position?

2023 Q3 Web3 Primary Market Review and Track Analysis: Gradual Bull Market, How to Position?

2023 Q3 Web3 Primary Market Review and Track Analysis: Gradual Bull Market, How to Position?Author: Colin

The Activity Level of Supply and Demand in the Primary Market Has Declined for Three Consecutive Quarters

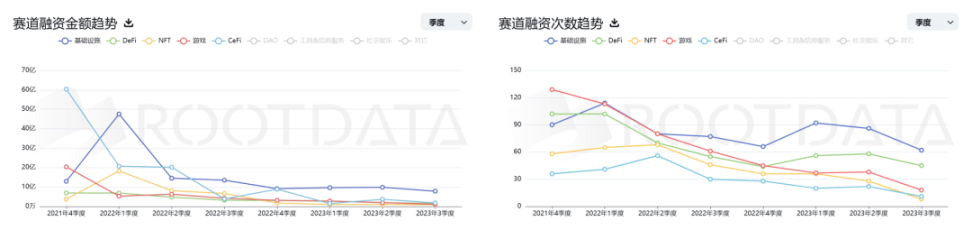

In Q3 2023, the total market financing amount was $1.694 billion, with 170 financing events, and the average financing scale slightly increased (Ramp and BitGo, two fund infrastructures aimed at traditional institutions, completed $400 million in financing). In October 2023, the financing amount was $426 million, marking the lowest monthly financing amount in nearly four years. Both the financing amount and events have been declining, and overall trading in the market is not active. Institutions continue to adopt a conservative strategy, mainly focusing their funds on infrastructure and projects with strong fundamentals, such as Flashbot.

Data Source: RootData

Market Sentiment Is Dull, Expected to Warm Up in the Next Two Quarters

As the investment and financing funds continue to decline, the rate of decline is gradually narrowing. Originally dominant sectors like DeFi, GameFi, and gaming have dropped to a freezing point, and RWA and BTC projects have not brought continuous activity to the altcoin market.

We believe that the current state of the primary market has shown a similar sentiment dullness to that of Q4 2019, where institutions only invest in projects with strong fundamentals. The optimization projects in conventional sectors have completed their basic framework layout over the past year and a half, and are relatively conservative towards sentiment-driven or slightly innovative projects. It is difficult for the market to break the sentiment ice point in the short term with new narratives. The current market state needs to regain confidence after a qualitative change in fundamental growth.

Chart Source: ROOTDATA 2023.09.28

Considering the current on-chain capital volume, the number of wallets, and the continuous growth of basic infrastructure fundamentals, we believe that the primary market is experiencing a bottoming phase and is expected to warm up in the next two quarters:

Projects like Zksync, Starknet, Celestia, Layerzero, Eigenlayer, and Scroll are expected to have significant fundamental updates and testnet iterations, or mainnet launches in the next two quarters, which could drive potential on-chain activity and further ecological layout opportunities. Large Infra projects did not launch in Q3, and on-chain activity and sentiment did not follow the main line;

The Ethereum Cancun upgrade will further enhance the L2 ecosystem, with Q3 L2 ecosystem TVL stabilizing at $10 billion. The asset volume and trading volume have entered a growth bottleneck period. The Cancun upgrade will bring lower gas costs and faster on-chain experiences, effectively boosting secondary market prices and sentiment, potentially providing new layout opportunities for the L2 ecosystem;

The gaming sector is set to see a large-scale launch, with a high probability of driving the market; the current supply of gaming products is complete, with gaming financing exceeding $5 billion in the second half of 2021. After more than a year and a half of preparation, the new generation of blockchain games has significantly improved in production quality, operational maturity, playability, and experience optimization, and will be launched in the next three quarters;

Industry Sector Analysis

Overall, this bear market cycle has lasted for more than six quarters, during which almost all old narratives have evolved and developed to varying degrees, some of which have been fully disproven by the market. New narratives have also emerged one by one to test the waters, generating effective market feedback. In our six-quarter observation and research, we believe that the market has produced sufficient material for inductive reasoning, allowing for more reliable research ideas and observational perspectives.

ETH will undergo the Cancun upgrade within the next six months, and BTC will have its next halving in seven months; we believe that as of Q3 2023, the potential core sectors for the next bull market cycle have basically emerged in the market.

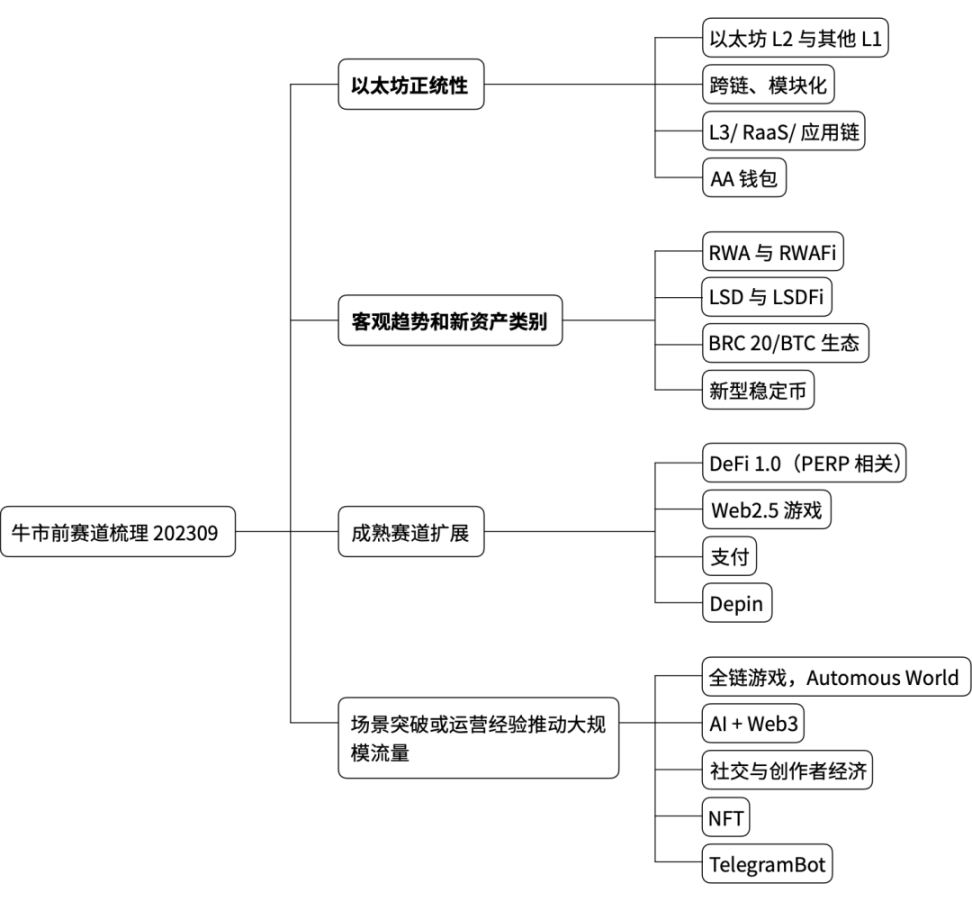

Based on past market experiences and summaries, we categorize the existing main sectors into four categories based on the order of occurrence, reasons for explosive growth, and overall supply scale:

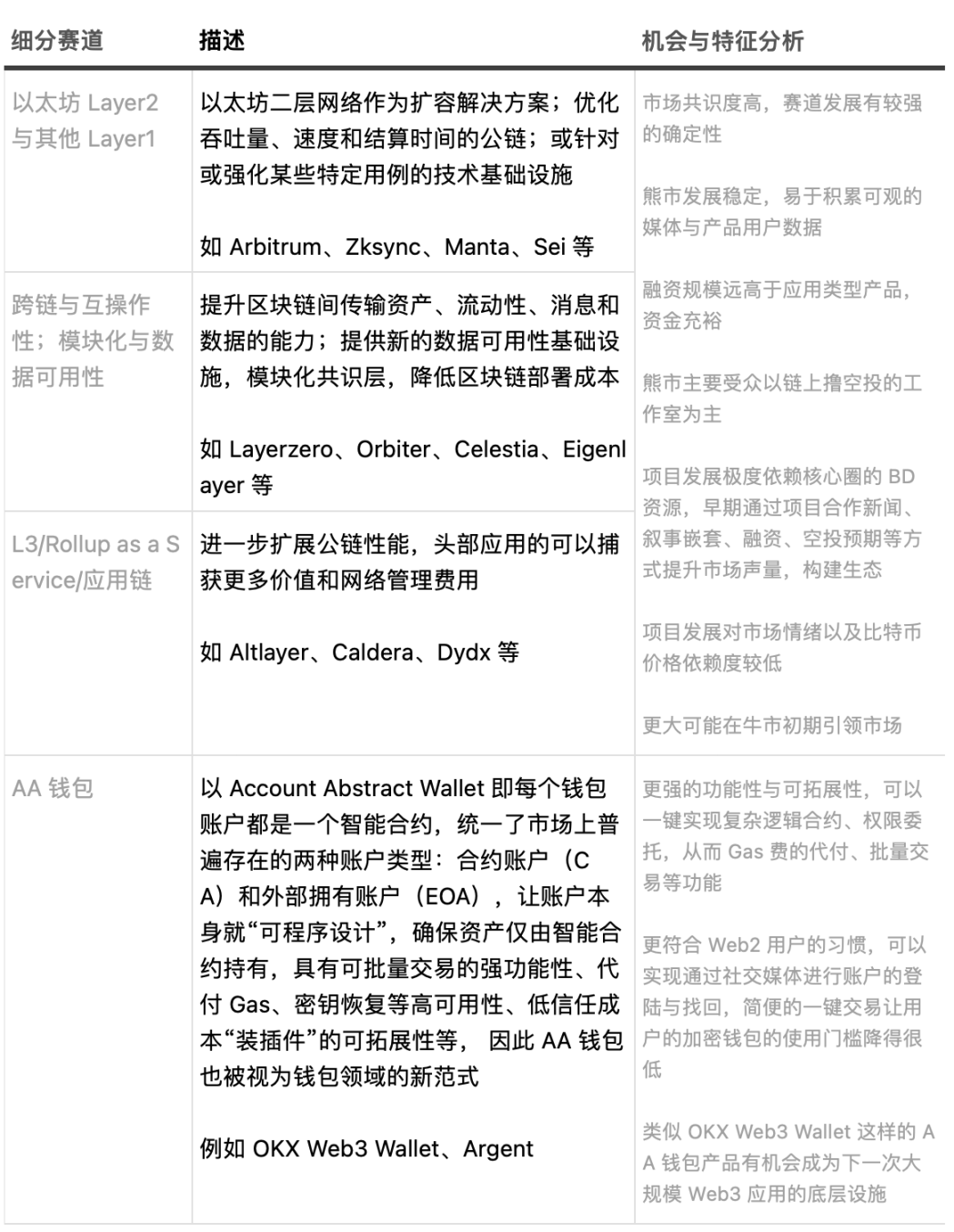

Ethereum Orthodoxy Drive (Important)

Ethereum orthodoxy mainly describes the core technological path of blockchain development. This category has raised over $10 billion in total funding during the six quarters of the bear market, accounting for about 40% of the entire market's fundraising scale.

As large project airdrops have become one of the few effective asset issuance paths and market hotspots during the bear market, these projects have continuously accumulated high user data and ecological resources. At the same time, projects in the "Ethereum orthodoxy" category primarily rely on ecological business development (BD) in the early stages, enhancing brand presence and ecological attention through collaborations with leading projects, narrative embedding, airdrop expectations, and strong capital endorsements. The fundamental development of such projects mainly focuses on building technical ecosystems and narratives, which are less affected by market sentiment and Bitcoin prices. Coupled with good capital strength and airdrop effects, we believe they are more likely to become the main leading sectors in the early stages of the bull market.

Objective Trends May Reach a Turning Point or Create New Asset Categories (Important)

The rapid growth of primary market sectors and their ability to lead the market usually need to meet one of the following standards:

- The original sector or technological environment is stably developing and generating new narrative ideas or operational strategies, such as GameFi and DeFi;

- Objective trends and user or asset volumes are steadily growing, reaching a qualitative change that produces entirely new product categories, such as derivatives trading;

- New narratives create new asset categories, with large new asset distribution channels unrestricted, such as NFTs;

Thus, we have identified which categories of sectors in the current market meet one of the above standards and believe that some subfields of the market are gradually approaching a turning point, with a high likelihood of becoming the engines of the next bull market.

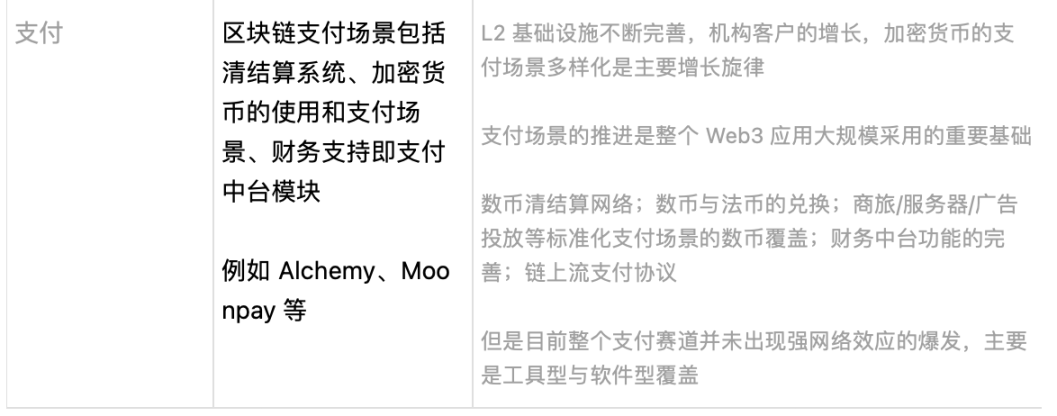

Scale Expansion of Mature Sectors

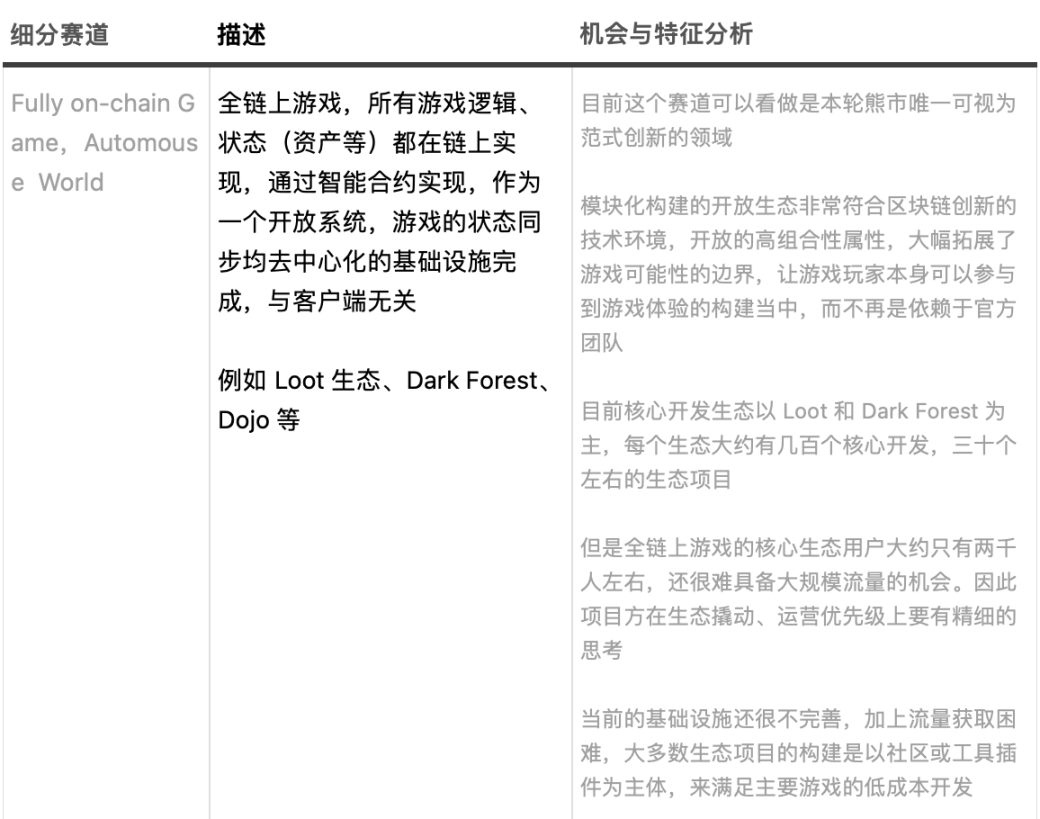

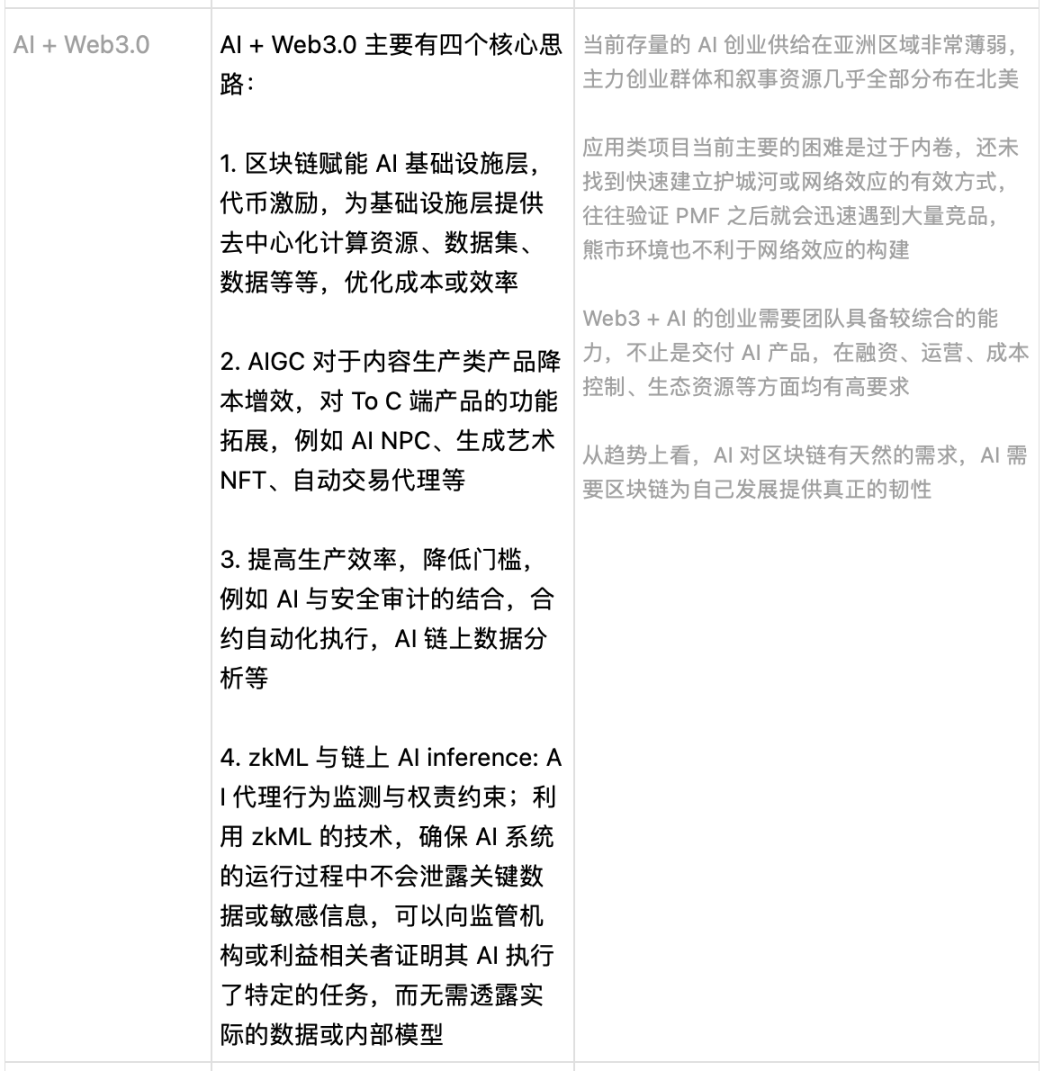

Breakthroughs Dependent on User Scenarios or Operational Experience Leading to Large-Scale Traffic