Arthur Hayes's Blog: Funds Will Flood into Artificial Intelligence, Optimistic about Decentralized Storage

The massive printing of fiat currency and the lightning-fast adoption of artificial intelligence will jointly create the largest financial bubble in history.

The massive printing of fiat currency and the lightning-fast adoption of artificial intelligence will jointly create the largest financial bubble in history.Original Title: Double Happiness

Original Author: Arthur Hayes

Original Compilation: Kate, Marsbit

Excerpt Compilation: Wu Says Blockchain

Note: This article is an excerpt compilation based on the aforementioned Chinese version, and some details or information may have been omitted. We recommend readers refer to the original text for a more comprehensive understanding. Additionally, this is Arthur Hayes' last article on the intersection of artificial intelligence and cryptocurrency. On September 13, 2023, Arthur Hayes delivered a brief speech titled "Double Happiness" at the Token2049 conference in Singapore, and this article is the text of that speech.

In this article, I will explore a very specific happiness: when this dreary cryptocurrency bear market ends, and we enter an exciting, unprecedented bull market, I hope we all can experience pure nirvana. That is to say, a bull market driven by the surge of fiat liquidity to levels unprecedented in human history, along with the excitement brought about by the commercialization of artificial intelligence (AI). So far, we have experienced cryptocurrency bull markets driven either by increases in fiat liquidity or by appreciation in certain aspects of blockchain technology, but not both at the same time. A bull market of fiat liquidity and technology will bring double happiness to the portfolios of loyal investors.

First, I will gradually introduce why the world's major central banks—the Federal Reserve (Fed), the Bank of Japan (BOJ), and the European Central Bank (ECB)—will jointly print the most fiat currency in a 2-3 year window in human history to "save" their respective government bond markets. Then, I will describe the excitement I expect to see surrounding new AI technologies, which will largely be funded by "toilet paper money." Finally, I will explain why I believe a certain junk coin—Filecoin (FIL)—will regain its historical highs from 2021 in the context of these two trends.

Formula

Cryptocurrency Price = Fiat Liquidity + Technology

Dirty Fiat

Central bank officials face a tough choice: due to inflationary pressures, they must either protect the purchasing power of their national fiat currencies in terms of energy or ensure that the federal government can service its debt—but they cannot have both. As I have repeatedly pointed out, governments never voluntarily go bankrupt, which makes over-indebted governments more likely to give their central banks the green light to sacrifice the purchasing power of fiat currency at all costs to keep bond yields "affordable."

To understand why governments are so willing to cast aside their national currencies to fund their debt habits, one must first understand why they have become so reliant on leveraging debt to grow their economies. Raoul Pal has a simple formula for calculating the drivers of economic growth—Gross Domestic Product (GDP).

GDP Growth = Population Growth + Productivity Growth + Debt Growth

The establishment of stable and liquid credit markets suddenly gave governments the ability to borrow from the future to build things today. They believed that what they built today would make us more efficient in the future and that more people would use it. If our productivity and population growth outpace the growth of debt interest that funds that productivity, societal wealth will increase.

Population Decline

Unfortunately, for politicians hoping to boost GDP, there is a major obstacle in the "population growth" part of Raoul's formula: the birth rate of the "wealthy class" is lower than it used to be.

Since the late 1980s, developed countries have been heading towards extinction. The chart above clearly shows that by the 2010s, the working population of the entire world began to decline. This makes sense—urban populations making a living in offices or factories do not need children. In fact, children are a net drain on family resources. When the global economy was agrarian, children represented free labor and were therefore a net economic positive for family units.

If the formula for GDP growth is GDP Growth = Population Growth + Productivity Growth + Debt Growth, and population growth turns negative, then governments must double down on improving productivity.

Productivity Delayed

So far, the major trends of the past have driven most of our productivity growth, and they are unlikely to be repeated. They are:

The entry of women into the workforce.

The outsourcing of global manufacturing to Eastern countries, where workers are paid low wages and are willing to degrade their own environment.

The widespread adoption of computers and the internet.

The expansion of hydrocarbon production due to the growth of U.S. shale oil and gas drilling.

These are one-time phenomena, and we have already realized all the gains that can be obtained from each of them. Therefore, productivity must stagnate until some new, unforeseen trend emerges. Artificial intelligence and robotics have the potential to be one of the trends leading a new wave of productivity growth, but even if this proves to be true, it will take decades for these gains to be fully reflected in the global economy.

The Illusion of Infinite Growth

The entire global economy is built on the fallacy that growth must continue indefinitely. The problem is that we have not recognized that the factors that led to global economic prosperity over the past 100 years are one-time events that have long since expired.

My predictions, along with others, regarding the increasing global debt burden are not new. However, earlier in this article, I made a very bold prediction that in the next 2-3 years, all major economic blocs will print more money than ever in history. This requires the U.S., Japan, and Europe to do the same thing at the same time. I hope they all act in unison because their economies are interconnected, and their actions are constrained by the post-World War II order led by the United States.

But before I delve deeper, I need to first take you through the architecture of global trade after World War II and explain how the current trade/capital imbalances make it necessary to print more money to prevent a flawed arrangement from failing.

The End of an Era

This chart is key to understanding the economic structure created by the U.S. after World War II. Countries like Japan and Germany were allowed to achieve post-war recovery through exports. These countries exported goods to the U.S., which paid with dollars borrowed from savers in those countries. This system required certain conditions to be met, including that wage growth in exporting countries be less than productivity growth, and that the U.S. allowed exporters to sell goods and invest in U.S. financial assets tax-free.

The operation of this system was aimed at balance and did not involve moral judgments. Exporting countries needed savings, while the U.S. needed consumption. However, over time, this system faced challenges as foreign markets became saturated, and capital returns on infrastructure investments became difficult to achieve.

Exporting country governments took measures to continue providing cheap credit to industrial enterprises to maintain capacity and avoid bankruptcies and soaring unemployment rates. In contrast, the U.S. financial sector was reluctant to invest domestically and allocated funds to risky foreign companies and countries.

When these foreign borrowers could not repay their loans, it could trigger a financial crisis, requiring intervention from the Fed and the U.S. Treasury to prevent the financial system from collapsing.

The only way for the U.S. and exporting countries is to print money, but this is merely a way to delay the adjustment of the global trade and financial system architecture, not a long-term solution.

The Con Artist Never Wins

As the amount of debt in circulation grows exponentially, U.S. Treasuries have already lost value in terms of energy. If I were a major holder of this junk, I would be very angry. Japan and Germany clearly saw the writing on the wall, which is why they stopped reinvesting export revenues into these bonds. This is also a con.

As U.S. unpaid debt skyrockets, two major trading partners, China and Japan, have begun a buyer's strike. As the last buyers, U.S. banks (which have to buy this junk) and the Fed (which will soon also have to buy this junk) have stepped in.

Everyone is conning each other, and there are valid reasons for it. It is clear that, whether the elites like it or not, a new global economic system will eventually be created. The imbalance cannot continue. But as long as those in power refuse to acknowledge reality, money will be printed in the hope that "growth" is just around the corner—so we can make America, China, Japan, and Germany great again!

I do not know what the new global economic arrangement will look like, but I can be certain that this will be the last credit cycle experienced by the current system. It will be the last time because no one wants to voluntarily hold any government bonds. The private sector does not need them because, due to inflation, they must hoard capital, and if they are businesses, they must purchase increasingly expensive inputs. If they are individuals, they must buy food/fuel. The banking sector does not want them because they are already underwater from buying government bonds during the post-COVID boom. Central banks do not need them because they must combat inflation by shrinking their balance sheets.

Governments will attempt—forcing central banks, the banking sector, and subsequently the private sector to buy bonds with printed money, depositor money, or savings—with varying degrees of success.

Bond Bubble

Here is my estimate of the total amount of government debt that the U.S., China, Japan, and the EU must roll over and issue to cover deficits from 2023 to 2026.

Just because the government is borrowing does not mean that the money supply will increase, leading to inflation. Without natural buyers, the debt burden will only increase the money supply. At sufficiently high yields, the government can easily crowd out other financial assets and absorb all private sector capital. Clearly, this is not an ideal outcome, as the stock market would crash, and no businesses would receive any funding. Imagine if you could get a 20% yield from a one-year government bond. It would be hard to justify investing in anything else.

Theoretically, there is a "win-win" approach where the government funds itself without crowding out the private sector. However, with the global debt-to-GDP ratio reaching 360%, the amount of debt that must be rolled over and issued to cover future deficits will certainly crowd out the private sector from the market. Central banks must be required to print money to directly finance the government by purchasing bonds that the private sector is avoiding.

Let’s reconsider the amount of debt issued and subsequently purchased by major central banks during the period from 2023 to 2026, viewing it as a multiple of the total growth of major central bank balance sheets during the COVID pandemic.

As the private sector was forced to purchase government bonds at the lowest yields in 5000 years during the COVID pandemic, their portfolios solidified unrealized losses worth trillions of dollars. In this round of bond issuance, the private sector will not be able to participate in so much of this round of debt issuance. Therefore, my base assumption is that central banks will purchase at least 50% of the issued bonds. The result will be that from now until 2026, the growth of the global fiat money supply will exceed the growth during COVID.

Where the Money Goes

Now that we have some understanding of the extent of the growth of the global fiat money supply from now until 2026, the next question is, where will this money flow?

The printed money will flow into emerging tech companies that promise crazy returns once they mature. Every fiat liquidity bubble has a new form of technology that attracts investors and draws in massive capital. When the major central banks printed money to "solve" the 2008 global financial crisis, this free money flowed into Web 2.0 advertising, social media, and sharing economy startups. In the 2020s, it was the commercialization of technologies developed during World War I, such as radio. This time, I believe it will all be technology related to artificial intelligence.

The capital influx into AI has already begun, and with the exponential growth of the global money supply, this situation will only intensify.

Don't Be a Fool

The influx of capital into AI companies does not mean that investors will easily make money. In fact, quite the opposite; the vast majority of this money will be wasted on companies that cannot produce products with paying customers. The problem with AI is that, among the business models we can imagine today, few offer protective moats.

During the Korea Blockchain Week, I rode with a tech brother who works at a well-known Silicon Valley venture capital firm. He talked about how difficult it is to make money in the AI space. He recounted a funny incident that happened in a recent class at Y Combinator (YC). The entire class was filled with startups building plugins using OpenAI's large language model (LLM). Then, overnight, OpenAI decided to launch its own suite of plugins, and the valuations of the entire YC class dropped to zero.

Most of the companies that venture capitalists will invest in are just providing software support services on top of projects like OpenAI. Software is easier to replicate than ever. Try writing some code with ChatGPT—it's so damn easy. The vast majority of these "AI" tech companies are built on zero. If your business is based on OpenAI or similar companies allowing you access to their models, then why wouldn't OpenAI perfectly replicate your plugin or tool and ban you from using their platform?

I believe that venture capital heads are not that foolish (the limited partners are the foolish ones), so they will try to invest in companies that build defensible businesses around different types of AI models. This sounds good in theory, but where exactly is this startup spending its money?

AI "eats" computing power and data storage. This means startups will raise funds, immediately purchase processing time powered by GPUs (computer processing chips), and pay for cloud data storage. Most startups will run out of funds before they develop anything truly unique because the scale of computing power and data storage required to create truly novel AI is staggering. I guess that by 2030, less than 1% of the currently funded startups will survive. By the average rule, you as an investor will almost certainly lose all your money in the process of investing in AI.

Instead of searching for needles in a haystack, it would be better to directly acquire NVIDIA (the world's leading GPU chip manufacturer) and Amazon (the parent company of Amazon Web Services, the largest cloud data provider). Both of these companies are publicly traded with highly liquid stocks.

Venture capital can never charge management fees and performance fees by putting your money into two stocks. Unfortunately, for investment capital, they try to act "smart" and shoot at the less than 1% of startups that truly survive (which may still not outperform a simple weighted basket of NVIDIA and Amazon stocks). Let's revisit this prediction in 2030 and see if the venture capital funds from 2022-2024 performed well. I predict a total wipeout!

This concept is very similar to how, during the construction of Web 2.0, startups raised funds and handed them over to Google and Facebook in the form of advertising revenue. I challenge readers to compile the average performance of venture capital funds from 2010 to 2015 and compare the compound internal rate of return after fees to a purchase of equally weighted Google and Facebook stocks. I bet that only the top 5% of venture capital funds (or fewer) could outperform this simple stock portfolio.

For example, investing in NVIDIA is good because it has liquidity. You can get in and out at any time. However, it carries valuation risk. NVIDIA's price-to-earnings (P/E) ratio is as high as 101 times, which is absurdly high.

Due to strong earnings growth, NVIDIA's stock price rose from $14 to $101, with a P/E ratio of 14 times. This deal was a bargain, and your capital appreciated by 621%. Investing during euphoric periods can lead to an 86% loss because sentiment can quickly shift from joy to sorrow. NVIDIA has always been a super company, but the market is beginning to believe that NVIDIA, like other large semiconductor companies, should have a corresponding valuation.

Price is the most important variable. When it comes to my portfolio, I want to participate in the AI frenzy bubble, but I have some rules.

I can only buy things that are liquid and can be traded on exchanges. This allows me to trade at any time. If my investment consists of funds held by venture capital funds investing in pre-IPO or pre-token companies or projects, this is not possible. Venture capital funds typically take 7 years to return capital.

I can only buy stocks that have significantly declined from their historical highs (ATH). I want the multiple I pay for the earnings of another key metric to be significantly lower than the trading price when the stock or project became "The It Thang."

I am very knowledgeable about the crypto capital markets. Therefore, I want to invest in something that connects crypto and AI.

No Ozempic for AI

Because I do not know which AI business model will succeed, I want to invest in what I know AI will rely on—namely, its food groups. I either need to invest in computing power in some way, or I need to invest in cloud data storage. For both of these food groups, AI craves decentralization. If a centralized company controlled by humans decides to restrict access to its services (for example, due to government mandates), AI will face existential risks.

Cryptocurrency-driven blockchains enable people to come together and share excess computing power, which will be interesting, but I have yet to find a coin or token with a sufficient network to indicate that it will survive and thrive in the next two to three years. So, as far as I know, I do not have a decentralized way to invest in computing power.

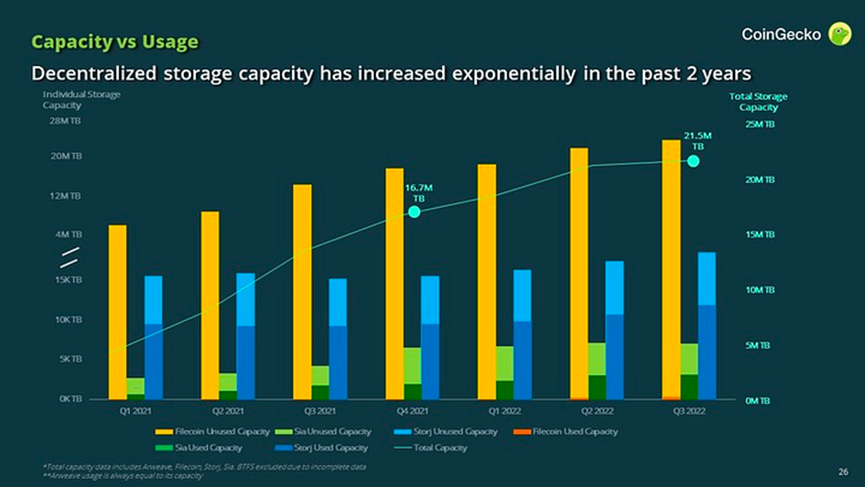

This forces me to invest in data storage. By storage capacity and total bytes of stored data, the largest decentralized data storage project is Filecoin (FIL). Filecoin is particularly appealing because it has been around for several years and has already stored a significant amount of data.

Without data, AI cannot learn. If data is compromised due to a single point of failure, or if a central data storage entity changes access permissions or its pricing, the AI relying on that storage entity will cease to exist. This is an existential risk, which is why I believe AI must utilize decentralized storage solutions.

This is why I do not want to own stocks in large cloud data service providers like Amazon. I fundamentally believe that Amazon is a large centralized company governed by human laws, which is incompatible with the needs of AI for its data hosting providers. Amazon can unilaterally shut off access to data at the government's request. This is impossible in a decentralized network that resists censorship. I know that due to the consensus mechanism and economic incentives of blockchain, it can help create coordinated "sharing." This is why a FIL-driven decentralized data storage network is essential for a thriving AI economy.

Let’s look at my checklist to see if FIL is a good fit.

Can it be traded on exchanges?

Yes. FIL started trading in 2020 and is available on all major exchanges worldwide.

Is its trading price significantly lower than its ATH?

Yes. FIL has dropped nearly 99% from its ATH in April 2021. More importantly, both the price/storage capacity and price/storage utilization have contracted by 99%.

Historical Data:

- FIL ATH: $237.24

- Filecoin Storage Capacity (2021): ~4 EiB

- Storage Utilization (2021): ~0.2%

Current Data as of Q2 2023 (Messari Report):

- FIL Price: $3.31

- Filecoin Storage Capacity: 12.2 EiB (exbibyte)

- Storage Utilization: 7.6%

Ratios

- April 2021 ATH Price/Capacity = $19.45/EiB

- April 2021 ATH Price/Storage Utilization = $1186.7 per percentage point

- Current Price/Capacity = $0.27/EiB

- Current Price/Storage Utilization = $0.44 per percentage point

Investing after a drop in the price-to-earnings ratio is always the best practice. Imagine if the price/capacity ratio merely rebounds to 25% of the April 2021 level, reaching $4.86 per EiB, then the price would rise to $59.29, nearly 17 times the current level.

Is it a cryptocurrency whose network can help AI develop?

Yes. FIL is a blockchain based on proof of space-time. FIL is the native cryptocurrency of the Filecoin network.

Trading Related

Many readers have commented on social media that I have been saying the same thing since the last bull market ended, and that I am completely wrong. This is true, but I do not engage in short-term trading for even a minute or an hour. I trade in cycles, and I focus on the cycle from 2023 to 2026. Therefore, as long as I am right later, it does not matter that I am wrong now.

Today, I am able to buy something at a "cheap" price that I believe will make a lot of money. FIL to MOON! The market may not react. In fact, its trading price may even be lower than my average entry price, but the math tells me I am on the right side of the probability distribution.

My portfolio is about to experience double happiness.

Whether now or in ancient times, governments have only known one way to solve the tricky problem of excessive debt and insufficient productivity: print money. The demise of every major empire or civilization can be partially attributed to the devaluation of its currency. Our current "modern" situation is no exception.

I have a gut feeling about these numbers, but even I am surprised by their scale. What comforts me is that others I respect are emphasizing that it is impossible to escape the massive debt accumulated by the world. The question is when the public, composed of banks, corporations, and individuals holding bonds, will refuse to invest excess cash into government bonds that yield negative real returns. I do not know when this will happen, but the world is entering a "hockey stick moment," where the growth rate of debt balances exceeds our lizard brains' ability to comprehend. In the face of these catastrophic charts, the speed at which debt balances rise and turn right will be rapid, and the public will flee, while central banks must step in with their trusted, absolutely rust-free money printing machines.

The boom of fiat liquidity is about to arrive, and I can wait patiently.

Artificial intelligence is experiencing its hockey stick moment of adoption growth. Since the invention of computers in the mid-20th century, people have been discussing and researching AI. It is only now, nearly 70 years later, that AI applications are beginning to be useful to hundreds of millions of people. The things that thinking machines will do will change our lives, and this will be an astonishing growth and speed.

With trillions of free funds, everyone from politicians to hedge fund masters to venture capital technologists will do everything they can to pour money into anything related to AI. Some commentators scoff that NVIDIA's ATH has corrected nearly 10%. They say, "I told you, it's a bubble." But their unimaginative minds have not read enough history or studied the evolution of bubbles. The AI boom has not even begun. Just wait for the major central banks to make a big shift and start printing money to save their governments from bankruptcy. The massive influx of funds and attention towards this "new" technology will be unprecedented in human history.

The massive printing of fiat currency and the lightning-fast adoption of AI will jointly create the largest financial bubble in history!

While the current market bores me, as the numbers decline, my hands will tirelessly collect those bulbs that will grow into powerful tulips. But make no mistake—I will not be foolish enough to believe all the hype. I respect gravity. Therefore, when I buy in, I look to the future, knowing when I must sell.

Let’s celebrate like it’s 2019!