The centralization risks of Lido are not as significant as imagined

Some people also believe that concerns about Lido's market share and centralization risks are more of a marketing tactic aimed at slowing down Lido's growth and allowing competitors to catch up.

Some people also believe that concerns about Lido's market share and centralization risks are more of a marketing tactic aimed at slowing down Lido's growth and allowing competitors to catch up.Author: Daniel Li, CoinVoice

With Ethereum's consensus mechanism transitioning from POW to POS, Lido, as one of the biggest beneficiaries, has seen its growing market share raise concerns and questions within the Ethereum community. Particularly, as Lido refuses to "self-limit" and plans to further expand its market scale, the narrative of threats posed by Lido has become a hot topic of discussion in the current Ethereum community. Some community members worry that Lido's rise may undermine Ethereum's decentralized characteristics. They are concerned that Lido's market monopoly could lead to node centralization, posing threats to the overall security and stability of the network. However, others believe that the concerns over Lido's market share and centralization risks are more of a marketing tactic aimed at slowing Lido's growth and allowing competitors to catch up. Regardless of the viewpoint, each has its own rationale. This article will conduct an in-depth analysis of Lido's market share and centralization risks to objectively assess its impact on Ethereum's decentralization and network security.

Lido's Dominance in Ethereum Staking Raises Widespread Concerns

Lido is a project that addresses the issue of insufficient liquidity for staked tokens on PoS blockchains like Ethereum. In traditional staking processes, tokens are locked in staking to protect the blockchain's consensus mechanism, while Lido allows users to receive tokenized versions of their deposited funds through liquid staking, thereby enhancing the liquidity of staking.

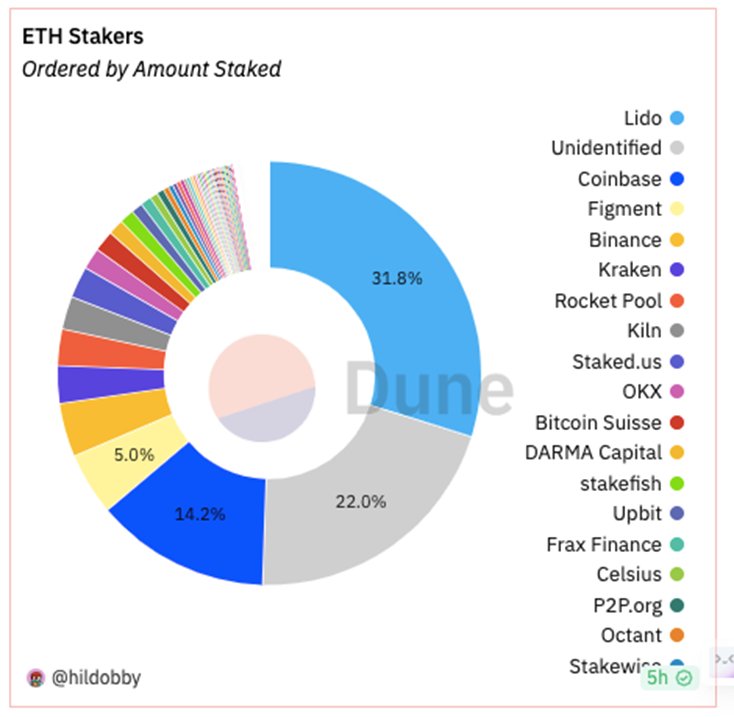

Since its launch in 2020, Lido has become the preferred liquid staking platform for Ethereum 2.0 and other first-layer PoS blockchains such as Solana and Polkadot. Compared to the traditional minimum staking requirement of 32 ETH, Lido allows users to stake any amount, lowering financial barriers. However, with Lido's rapid growth, concerns about its potential threat to Ethereum's decentralization have begun to surface. As of now, Lido has staked 8,813,670 ETH, accounting for 31.8% of the Ethereum staking market.

Lido's excessive market share has also caught the attention of Ethereum founder Vitalik. He recognizes the potential risks posed by Lido. Long ago, Vitalik suggested that all staking service providers limit their market share to below 15%, while Lido's current data far exceeds this limit.

According to Justin Galan, co-founder of Asymmetry Finance, Lido operates over 38% of validators, which is more than double what any single entity should control. This centralization phenomenon has raised concerns about Ethereum's centralization. Danny Ryan, chief researcher at the Ethereum Foundation, also emphasized the issue of Lido's centralized staking of Ether on Twitter. He pointed out that Lido controls a large amount of staked Ether and occupies over 90% of the liquid staking market, potentially facing risks from validator slashing, governance attacks, and smart contract vulnerabilities. Addressing Lido's excessive market share has become crucial to ensure Ethereum's decentralization and security.

The Centralization Threat of Lido May Not Be As Severe As Imagined

Currently, Lido is approaching the first security line of 33% of total staked volume. In the past, when the fish pool reached one-third of the hash power, it directly maintained network security by stopping registrations. Last month, four LSD projects—RocketPool, StakeWise, Stader Labs, and Diva—announced commitments to self-limit to below 22%, but Lido, as the industry leader, refused to self-limit. This has raised doubts within the community, while some KOLs have exaggerated the dangers of Lido's high market share online.

However, they overlook a key issue: how much of the market share information is truly public, and how much is based on others' reports? Since Lido is an on-chain protocol and the DAO operates entirely on-chain, it is completely open and transparent, making its data authentic. In contrast, major staking platforms like Coinbase and Binance, which rank after Lido, are centralized exchanges. The staking data of centralized exchanges depends on specific exchange policies and transparency requirements, and they can choose not to disclose unfavorable data. Therefore, Lido's approach to the total staked volume of 33% may still have some discrepancies.

If all parties' data is accurate, then Lido's 33% market share does pose some risks, but it is not as significant as KOLs claim.

To understand this from two perspectives: first, people concentrate their funds in Lido's pool and register as stakers in units of 32 ETH. Then, Lido allocates these funds to 29 designated operators to perform the actual staking operations. So, it can be roughly understood that each operator bears a portion of the risk, meaning the concentration of risk is not that high.

Secondly, node operators do not have the incentive to act maliciously. For Lido to alter Ethereum's finality, it would require the 29 node operators to engage in actions that are very detrimental to the protocol itself, and the node operators would face slashing if they affect finality [slashing is a penalty for validators; in staking, if they behave improperly in any way, the staked Ether will be "slashed" or removed]. When they are slashed, they lose Ether from validators, which means node operators are losing their source of income. So why would anyone want to attempt this? It makes no economic sense.

Aside from the aforementioned potential risks, the current biggest risk, and the area where the public questions Lido the most, is that the node operators are all designated by Lido, and others cannot enter. In this case, if the node operators chosen by Lido can reach a consensus on interests, they may form a cartel or collusion among large stakeholders in pursuit of higher profits. These validators could collude to manipulate the network, leading to adverse outcomes.

However, the probability of such occurrences is also not very high, as Lido has a set of publicly rigorous standards for selecting node operators, ensuring diversity in server types, geographical distribution, client diversity, and other characteristics to avoid centralization. Furthermore, even if Lido's 29 node operators collude to harm their own business, the social layer can intervene to remove malicious Lido node operators and shift business to a new chain.

Lido is a Manifestation of Ethereum's Centralization Problem

Lido's emergence can be seen as a manifestation of Ethereum's centralization problem, and its currently high market share is merely an opportunity. In fact, Lido's situation may recur in other projects. In a community-governed environment, community members are the owners of project interests, and their choices may lean more towards what benefits themselves rather than what benefits the entire ecosystem.

When community governance personnel at Lido agreed to set limits, users holding LIDO tokens were able to cast 99.81% of opposing votes. For a long time, achieving project autonomy through community voting has been regarded as a manifestation of decentralization. However, Lido DAO rejected restrictions on its centralization through decentralized community voting, which to some extent indicates that complete decentralization is uncontrollable.

In fact, since Ethereum transitioned to the POS consensus mechanism, concerns about its centralization trend have emerged, as validators with large stakes have extensive influence over the network, and these large stakeholders may dominate transaction validation, leading to power consolidation.

In this regard, Lido is clearly not the most severe case. Because Lido is not a single entity but an intermediary protocol, or simply understood as a "coalition," currently consisting of 29 node operators, who are the real entities staking ETH, similar to current POW mining pools. Node operators are managed by the Lido DAO, which screens operators' values to ensure diversity, thereby avoiding centralization risks. The Lido DAO is managed by holders of LIDO tokens. Therefore, to some extent, Lido is a decentralized organization.

Beyond Lido, the most concerning entities should be centralized staking platforms like Coinbase and Binance. Without Lido, centralized exchanges would quickly dominate most of the staking market, posing a greater threat to Ethereum's push for decentralization. Centralized exchanges can act as a single entity, and once their market share exceeds 50%, it could attract government attention, which may pressure exchanges through policies to manipulate the Ethereum staking market, leading to disastrous consequences for Ethereum's decentralization efforts.

The transition of Ethereum to PoS has brought significant advantages such as environmental sustainability, higher participation, and enhanced security, but it has also introduced centralization issues, such as the concentration of Ethereum network staking, which could pose systemic risks to the Ethereum network. The issues surrounding Lido may serve as an opportunity to spark discussions about Ethereum's centralization problem across various sectors, working together to strike a balance between the benefits of PoS and the centralization risks it brings.

How to Address Lido's Issues

The issues surrounding Lido have also attracted the attention of Ethereum's top designers. From the perspective of the overall ecosystem's robustness, Lido's excessive market scale brings significant single-point risks. Any internal failure within Lido could further impact the entire Ethereum ecosystem and the entire industry that relies on it. Therefore, limiting Lido's excessively high market share has become a desire among Ethereum's top designers. Recently, Ethereum co-founder Vitalik mentioned during a Discord discussion about Reflexer Finance (RAI) that RAI could support non-mainstream liquid staking tokens (other LSD tokens besides stETH) as collateral. This initiative could help address the issue of Lido's high market share. Although RAI's supply is currently limited, if its scale expands in the future, or if more new upper-layer applications begin to avoid stETH, Lido's market share will inevitably face a reduction as demand decreases.

In addition to the upper-layer awareness of Ethereum beginning to introduce policies to limit Lido's market share, Lido can also take a series of measures to improve its impact on Ethereum's decentralization and alleviate community concerns about its excessive market share.

First, Lido could consider self-limiting its market share within a fixed timeframe to promote the overall health and neutrality of the liquid staking market. By setting an upper limit, Lido can avoid excessive concentration, thereby reducing systemic risks.

Second, Lido can work to improve its internal decentralization, ensuring that each staking party has sufficient fault tolerance and response measures. This means Lido needs to take steps to address bad actors or vulnerabilities to ensure the stability and security of the system.

Additionally, Lido can take measures to fairly prevent system price manipulation to maintain market fairness and transparency. This can be achieved by establishing effective regulatory and risk management mechanisms.

Moreover, Lido can continue to increase the number of node operators in its network to diversify staking capacity and reduce centralization risks. By increasing the number and diversity of nodes, Lido can enhance the system's resilience and robustness.

Furthermore, Lido can work to build appropriate system safeguards to ensure that it fulfills its responsibilities as a market leader in this critical area. This includes establishing reasonable regulatory mechanisms and risk management frameworks to ensure the system's security and stability.

Finally, Lido could consider Vitalik's proposed method for upgrading the Lido system, which would automatically increase end-user fees when market share exceeds a target. Such a mechanism could guide Lido's market share to remain within a reasonable range, avoiding excessive concentration and single-point risks.

By taking these measures, Lido can mitigate its impact on Ethereum's decentralization while alleviating concerns about its excessive market share. This will help protect the stability and security of the entire Ethereum ecosystem.

Conclusion

Recently, the market controversies triggered by Lido have led some individuals within the Lido community to respond to the matter. One particularly interesting response raised the question of whether, when discussing limiting Lido's market share, we have considered that without decentralized liquidity protocols like Lido, the staking market could be monopolized by centralized exchanges. At that point, how should we limit these centralized exchanges? This perspective reminds us to consider multiple aspects of the market comprehensively, ensuring both the long-term development of the ecosystem and the maintenance of fair competition in the market.

Risk warning Risk warning

Risk warning Risk warning

Popular articles