34 million dollars of blood and tears: RWA is not that easy to do

Real estate, corporate loans... each one is worse than the last.

Real estate, corporate loans... each one is worse than the last.*Author: Azuma, * Odaily Planet Daily

RWA (Real World Assets) is undoubtedly one of the hottest concepts in the crypto industry today.

As a pioneer, Maker has capitalized on the high-interest cycle by opening up a revenue window for U.S. Treasury bonds, thereby amplifying the market demand for DAI and ultimately boosting its market value in a declining market. Subsequently, projects like Canto and Frax Finance have also achieved some success through similar strategies, with the former doubling its token price within the month and the latter's newly launched sFRAX in V3 showing impressive growth.

So, is the RWA concept really as "simple and useful" as it seems, allowing for stable and rapid improvements in project fundamentals? Recent lessons from the market suggest that the situation may not be so straightforward.

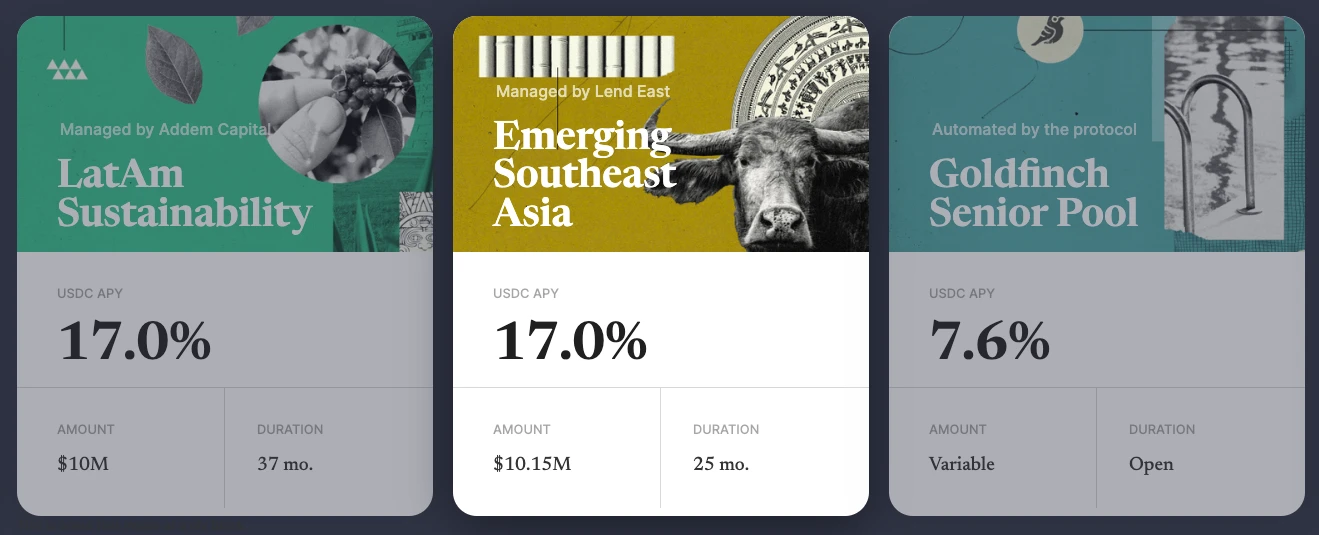

Goldfinch Bad Debt Incident

The first lesson is the bad debt incident involving Goldfinch.

Goldfinch is positioned as a decentralized lending protocol. Since 2021, Goldfinch has completed three rounds of financing totaling up to $37 million ($1 million, $11 million, and $25 million), with the latter two rounds led by a16z.

Unlike traditional lending protocols like Aave and Compound, Goldfinch primarily serves the commercial credit needs of the real world. Its operational model can be roughly divided into three layers.

- "Users" as fund providers can inject funds (usually USDC) into different themed liquidity pools managed by various "borrowers," earning interest income (returns come from real business profits, generally higher than conventional DeFi levels);

- "Borrowers" are typically professional financial institutions from around the world, which can allocate the funds in their managed liquidity pools to real-world "enterprises" that have demand based on their business experience;

- "Enterprises" will invest the funds to develop their own businesses and regularly use a portion of the profits to repay interest to "users."

Throughout the process, Goldfinch conducts due diligence on the qualifications of "borrowers" and constrains all lending terms to "ensure" (which now seems somewhat ironic) the safety of funds.

However, an unexpected event occurred. On October 7, Goldfinch disclosed through its governance forum that the liquidity pool managed by "borrower" Stratos encountered unexpected issues, with a total pool size of $20 million and estimated losses as high as $7 million.

Stratos is a financial institution with over a decade of credit business experience and is also one of Goldfinch's investors, appearing to be quite "reliable" in terms of qualifications, but evidently, Goldfinch still underestimated the associated risks.

According to the disclosure, Stratos allocated $5 million of the $20 million to a U.S. real estate rental company called REZI and another $2 million to a company named POKT (whose business is unclear; Goldfinch stated it did not know what this money was used for…), both of which have ceased interest payments, leading Goldfinch to write down these two deposits to zero.

In fact, this is not the first time Goldfinch has faced bad debt issues. In August this year, Goldfinch disclosed that the $5 million lent to the African motorcycle rental company Tugenden might not be recoverable due to Tugenden concealing the flow of funds between its internal subsidiaries and blindly expanding its business, resulting in significant losses.

The consecutive bad debt issues have severely impacted the confidence of the Goldfinch community, with many community members questioning the protocol's transparency and auditing capabilities in the comments section below the disclosure page regarding the Stratos incident.

USDR Depegging Incident

On October 11, the stablecoin USDR, backed by physical real estate (emmm, this is a double whammy…), began to experience severe depegging, currently trading at $0.515. Based on its circulating supply of $45 million, the total loss for holders is close to $22 million.

USDR is developed by Tangible on the Polygon chain, and can be minted by collateralizing DAI and Tangible's native token TNGBL, with a 1:1 collateralization ratio for DAI, while for risk considerations, the collateralization scale for TNGBL is limited to no more than 10%.

The emphasis on "backed by physical real estate" is because Tangible uses a significant portion of the collateralized assets (50%-80%) to invest in physical properties in the UK (after purchase, corresponding ERC-721 certificates are minted) and provides additional income to USDR holders through property rentals, thereby increasing the market demand for USDR and connecting the vast real estate market to the crypto world.

Considering the potential redemption needs of users, Tangible also reserves a certain amount of DAI and TNGBL in the collateralized assets, with DAI reserves set at 10%-50% and TNGBL reserves at 10%. However, Tangible clearly underestimated the scale of redemption demand during a bank run.

On the morning of October 11, there were still 11.87 million DAI reserved in the USDR treasury, but within 24 hours, users redeemed tens of millions of USDR and exchanged them for more liquid assets like DAI and TNGBL for sale, which also caused the price of TNGBL to plummet, indirectly leading to a shrinkage of that portion of collateralized assets and further exacerbating the depegging situation.

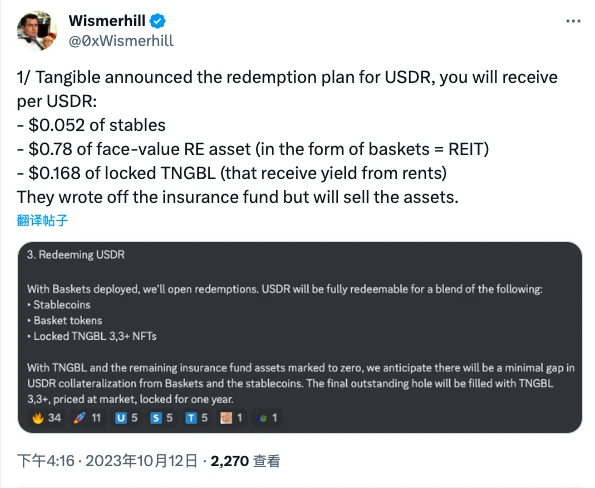

In response, Tangible has announced a three-step resolution plan:

First, emphasizing that USDR still has an 84% collateralization rate;

Second, tokenizing the properties it owns (if there is no demand, it will consider directly liquidating the properties);

Third, redeeming USDR through a combination of "stablecoin + property tokens + locked TNGBL."

According to estimates by overseas KOL Wismerhill, USDR holders are expected to receive:

Stablecoins worth $0.052;

Property tokens worth $0.78;

Locked TNGBL worth $0.168.

In summary, compensation may help holders "recover some losses," but USDR is destined to become a thing of the past, and this attempt at RWA centered on real estate ultimately ended in failure.

Experiences and Lessons

From the successes of protocols like Maker and the failures of Goldfinch and USDR, we can roughly draw the following lessons.

First, regarding the choice of off-chain asset classes. Considering factors such as risk level, pricing clarity, and liquidity status, U.S. Treasury bonds remain the only fully validated asset class at present, while the various relative disadvantages of non-standard assets like real estate and corporate loans can introduce additional friction into the entire business process, hindering large-scale adoption.

Second, regarding the disconnection of liquidity between off-chain assets and on-chain tokens. Analyst Tom Wan noted that in discussing the reasons for USDR's depegging, Tangible could have minted on-chain certificates representing real estate in ERC-20 form but chose the relatively "fixed" ERC-721 form, which meant that once the DAI reserves were exhausted, the protocol had collateralized properties but could not continue to redeem. While real estate has poor liquidity, Tangible could have designed additional mechanisms to improve this situation on-chain.

Third, regarding the auditing and supervision of off-chain assets. The consecutive bad debt incidents at Goldfinch have exposed its management incapacity regarding the real execution status off-chain. Even with the initiation of a dedicated auditing role within the protocol and choosing relatively trustworthy in-house investors for "borrower" management, it still failed to prevent the misuse of funds.

Fourth, regarding the collection of off-chain bad debts. The borderless nature of crypto gives on-chain protocols the freedom to operate regardless of geography (excluding regulatory factors), but when problems arise, it also means that protocols find it challenging to enforce localized bad debt collection, especially in regions where laws and regulations are not well-established, making practical operations increasingly difficult. For example, in Goldfinch's earliest bad debt incident, can you imagine a few New York office workers going to Uganda to collect money from those renting motorcycles…?

In conclusion, RWA has brought an imaginative space for incremental markets in crypto, but as of now, it seems that the only viable path is the "reckless all-in" on U.S. Treasury bonds. However, the attractiveness of U.S. Treasury bonds is closely related to macro monetary policy; if the yields of the former begin to decline with the latter's shift, whether this path can remain open will also be called into question.

At that time, expectations surrounding RWA may shift to other asset classes, which will require practitioners to face challenges head-on and carve out new paths.