Bear Market Advice from Crypto VCs: Don't Blindly Trust Institutions, Retail Investors Can Do Well Too

It is important to: continuously learn, lead the narrative, rather than follow it.

It is important to: continuously learn, lead the narrative, rather than follow it.Original Title: What Do Crypto VCs Know that You Don't?

Original Author: Ignas

Original Compilation: Luffy, Foresight News

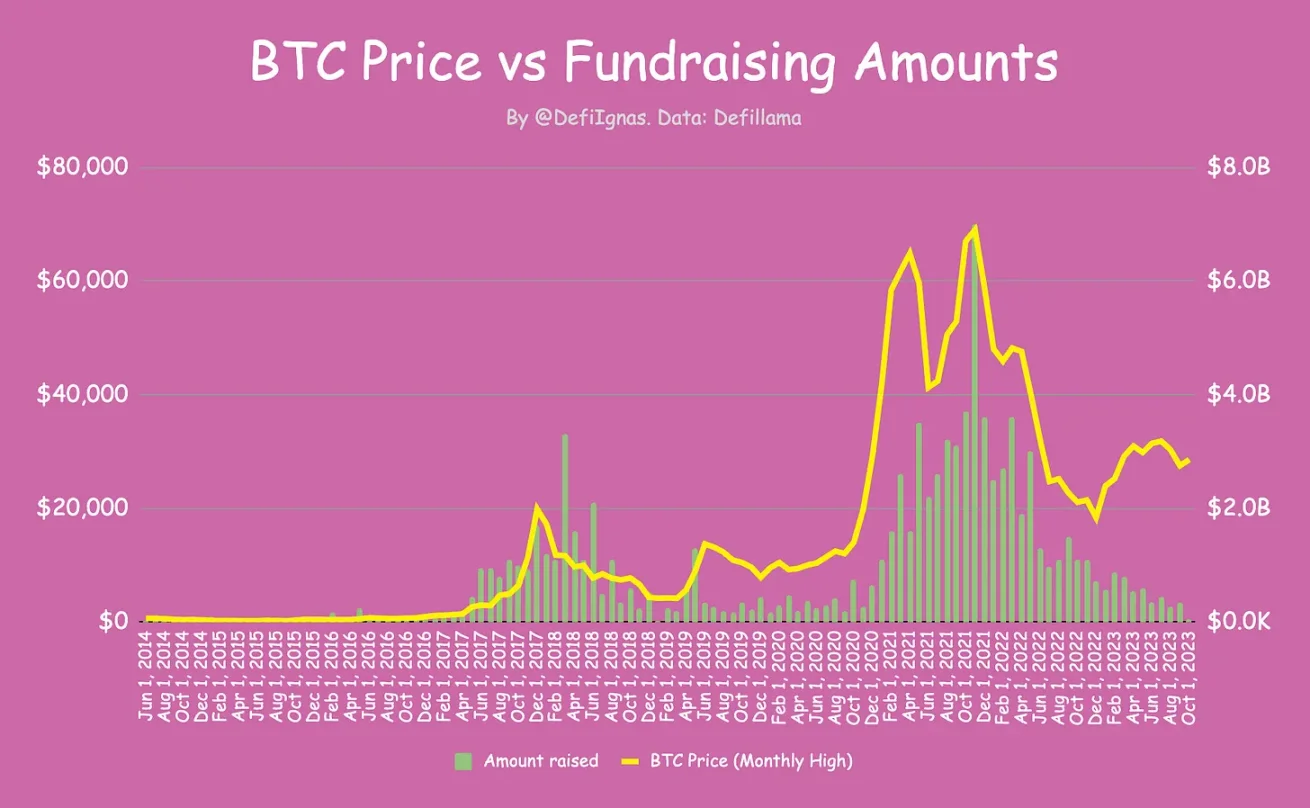

The relationship between Bitcoin prices and project financing amounts in the cryptocurrency market is fascinating. Typically, when Bitcoin prices drop, the amount of fundraising decreases as well.

Interestingly, although Bitcoin and Ethereum prices are higher than during the peak of the 2018 bull market, the scale of financing has returned to levels seen before 2020. Bitcoin has actually rebounded from its lows in 2022, but the amount raised continues to decline.

Venture capitalists (VCs) are often seen as market leaders capable of making informed and forward-looking decisions. So why do they seem to be following the overall market trend rather than setting it?

Despite a slight market recovery, VC fundraising amounts have dropped to levels seen in 2018-2019. Do they know something that we retail investors do not? Shouldn't they be "buying the dip" when valuations are lower? Especially since post-investment lockups prevent immediate selling, they may ultimately have to sell during a bear market.

To find answers, I interviewed several cryptocurrency venture capitalists and founders of recently funded DeFi projects. I am pleased to share that Sachi Kamiya from Polygon Ventures, Etiënne from TRGC, and an anonymous angel investor (referred to here as Anon) shared their insights.

Jaimin, the founder of Caddi, also provided valuable perspectives from the viewpoint of a DeFi builder. Caddi is a browser extension that helps you save money on DeFi transactions and protects you from scams. He recently raised $650,000 from venture capital firms such as Outlier Ventures, OrangeDAO, and Psalion VC, as well as angel investors Bryan Pellegrino, Alex Svanevik, and Pentoshi.

How Bad Is the Situation?

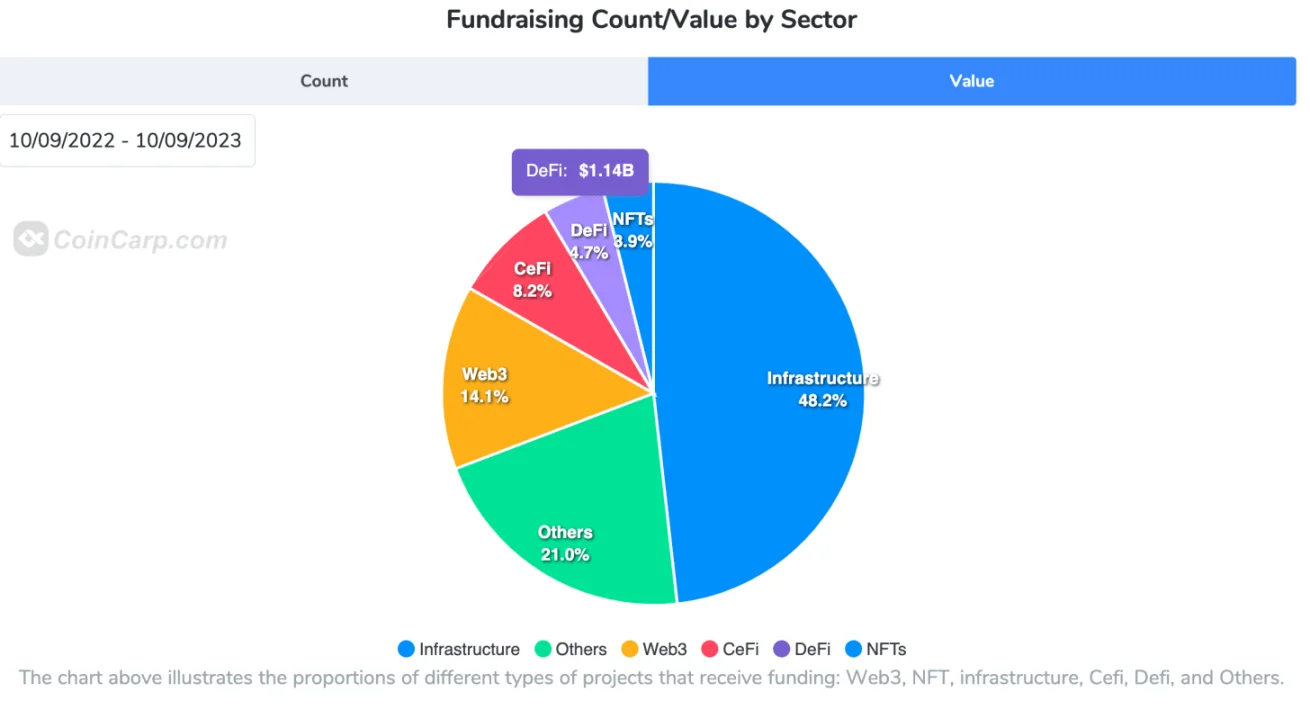

CoinCarp's chart provides a different perspective. The total fundraising amount in the crypto market for 2023 is $18.6 billion, with a total of 1,053 deals, looking much better than in 2020.

However, this chart includes Web2 cases, such as the $6.5 billion raised by Stripe.

Speaking of my beloved DeFi, there have been a total of 175 funding rounds this year, amounting to $779 million, with an average of $4.45 million per round. This is a significant decline compared to last year, which saw 341 funding rounds totaling $3.56 billion, with an average of $10 million per round.

Thus, funding is tighter this year, with the average amount raised per round decreasing by over 55%.

Unfortunately, the DeFi sector is actually the second worst-performing area, only above NFTs. Over the past year, DeFi protocols have raised only $1.14 billion, while CeFi startups raised $2 billion.

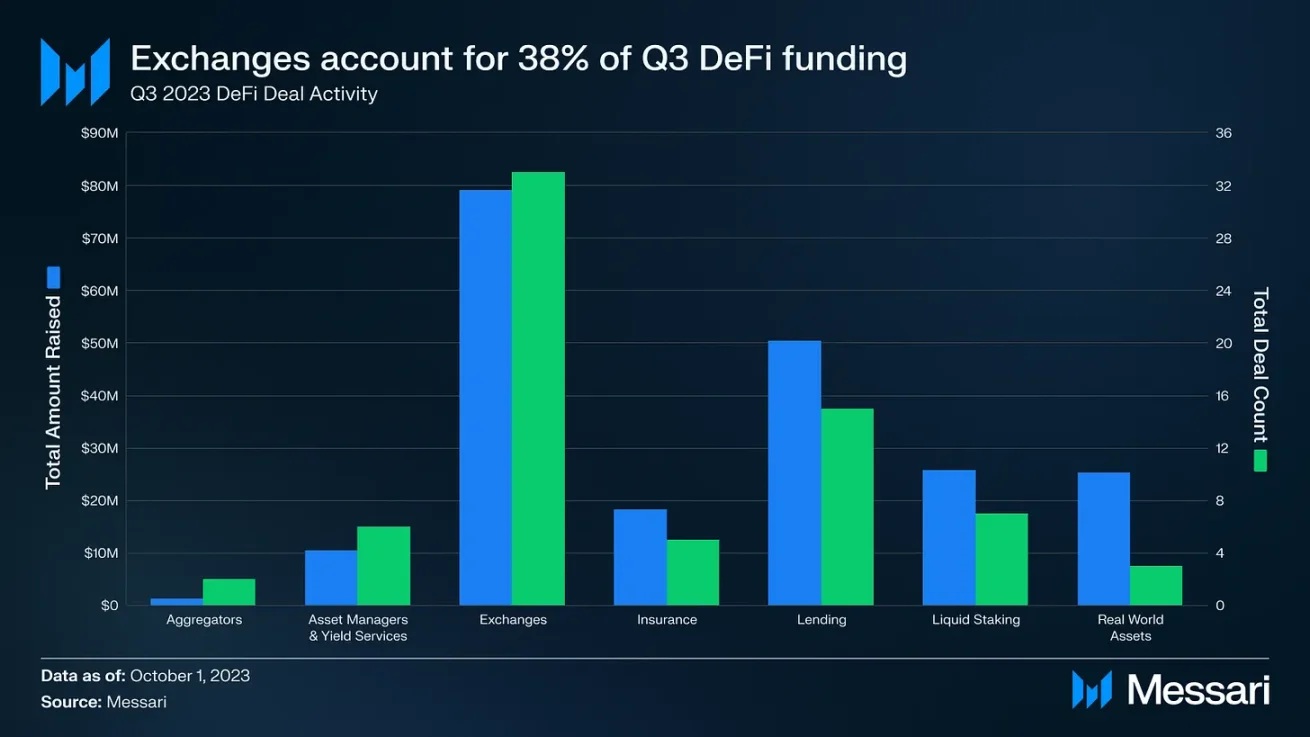

A closer look shows that DEXs dominate DeFi financing. In the third quarter of 2023, DEX financing accounted for 38% of all DeFi financing.

Source: Messari Q3 Financing Report

Due to the tight funding environment, several cryptocurrency companies are laying off employees, with Yuga Labs, Ledger, and Chainanalysis announcing large-scale layoffs last week.

Despite being in a bear market, some well-known protocols have successfully raised significant funds. This indicates that investors have not completely given up on cryptocurrencies and DeFi. In fact, Blockchain Capital recently raised $580 million to invest in DeFi, gaming, and infrastructure projects. So I hope this blog post can help these funds find the bottom of the market.

When asked about the current fundraising market from the perspective of DeFi builders, Jaimin commented, "The market is as bad as it has been in the past few years, mainly due to the macroeconomic environment." Sachi from Polygon Ventures shared a similar view, stating, "The overall sentiment in crypto venture capital is bearish. Due to negative sentiment, fewer early-stage projects are raising funds."

Anon provided a figure, stating, "There may only be 10% of the funding amount compared to a bull market."

Compared to past bear markets, Etiënne noted, "Unlike in 2019, there is real capital on the sidelines now; in 2019, there was almost no capital on the sidelines."

This is why there are still huge opportunities in the market. Anon, Etiënne, and Sachi all agreed that now is a good time to look for opportunities, as project valuations are no longer as crazy as during the bull market. Sachi pointed out that investors "can take their time to conduct due diligence on each project, but VCs focus on user metrics and actual adoption."

Interestingly, this is precisely the hardest thing to achieve for early-stage projects. Jaimin stated, "Investors want to see exponential growth, whether in revenue, users, TVL, or trading volume. Sustainable growth in this market is very difficult because there is little new user influx, low volatility, stagnant prices, and poor sentiment. Simply selling a vision is often not enough."

Sachi optimistically summarized, "Investing now makes sense because some of these projects will perform well in the next cycle."

Why Do We Need VCs?

There is a lot of distrust, hostility, and negative sentiment towards VCs in the crypto space. The main reason is obvious: institutional investors can dump on retail investors.

Algod stated on Twitter that the best projects will be those that launch fairly without venture capital because people realize they do not want to exit liquidity. In another article, he also mentioned that venture capital will become a bearish factor compared to 2021 because "the community is key, and projects are starting to realize that scale is driven not by venture capital but by ordinary people."

Some non-crypto investors also agree with this view.

For example, in an interview with Bloomberg, angel investor Jason Calacanis, who has invested in Robinhood, Uber, and Superhuman, warned about the potential impact of "scam" VCs dumping cryptocurrencies on retail investors.

Calacanis believes that many of these tokens are securities sold by VCs to unsuspecting retail investors. He predicts that companies and VCs that intentionally sell "worthless" tokens will face significant lawsuits and may even face criminal charges.

So, can we completely skip crypto venture capital? The most concerning aspect is how "fair" a "fair launch" really is.

Anon stated, "Fair launches are not so fair because teams and insiders already know about them before the actual launch and may weaken liquidity." Jaimin also expressed similar skepticism, questioning whether current launches are truly "fair," as they can be manipulated in various ways, and "dumping on each other is always present."

Etiënne agreed, stating, "Regardless of whether a fair launch occurs, the motivation to make money remains the same. Retail investors are not innocent; they are just less funded gamblers."

Sachi mentioned that fair launches might "suit projects led by founders who already have experience running cryptocurrency companies." All interviewees seemed to agree that for inexperienced founders and those without initial resources, fair launches are a tough game, especially if the project "is not a fork or an easily achievable goal," as Anon put it.

Personally, I love the story of fair launches. The birth of YFI remains one of my fondest memories from the summer of DeFi in 2020. I hope to see truly fair launches in the upcoming bull market.

But I dare say that venture capital plays an important role in the cryptocurrency space, including initial capital injection, guidance, providing networking opportunities, and even bringing credibility to the entire project industry.

What Can We Learn from VCs?

This is the main reason that prompted me to write this blog post. As the chart of Bitcoin prices and crypto project fundraising amounts shows, fundraising amounts follow Bitcoin price trends rather than set them, which is somewhat disappointing. People expect savvy VCs to predict market trends, double down at the end of a bear market, and cash out during a bull market.

Sachi provided valuable insights, "Not all VCs follow market trends. Some VCs, especially American ones, tend to invest based on market trends. But many Asian venture capital firms do not, in fact, they become more active during bear markets because there are good opportunities."

Anon added that projects raise funds during bear markets, but they "will announce when it makes more sense for them."

Additionally, there are token lockups in venture capital, complicating monetization strategies. I believe that investing during bear markets allows VCs to sell during the token appreciation period after the lockup expires. On the other hand, if a venture capital firm invests during a bull market, they may have to wait until a bear market to sell, further suppressing already low altcoin prices.

Timing does not seem easy. Anon shared, "There is some uncertainty with TGE (Token Generation Event) because this is usually when the unlock timer is activated. I feel that at least for major products, as long as they wait for the best listing opportunity and have a good lockup structure, it is still possible to make money after unlocking."

Sachi told me that Polygon Ventures considers the quality of the project when determining unlock times, preferring shorter lockup periods, but they take into account the team's crypto-native level. "Managing tokens requires skill (e.g., listing on exchanges, market making, etc.). The higher the team's crypto-native level, the greater the likelihood of long-term success for the project."

So, what lessons can we learn from VCs?

Etienne was blunt:

Haha, you can't learn anything. In fact, stop listening to the nonsense of VCs. I recommend that 95% of VCs remain silent across all platforms. I strongly recommend old foxes like Howard Marks, Nassim Taleb, Warren Buffett, Stan Druckenmiller, Ed Thorp, Jim Simons, and Mark Spitznagel. I would only listen to VCs like Mike Moritz or Doug Leone, who have a 30-year track record. Not "I was lucky to get token XYZ, now let me teach you how to invest," those people are the worst, and there's nothing to learn from them.

Anon’s advice is simple. Don't put all your eggs in one basket. "Even some VCs make this mistake and suffer heavy losses." As cryptocurrency users, "we should strive to introduce these projects to people, share feedback and suggestions, etc. This is very valuable for advanced users."

Sachi provided practical advice, "It's important to ask the right questions and do research. For example: Are these real user metrics? Is the founder legitimate?"

Retail investors should understand that whenever a project makes an announcement (e.g., establishing partnerships with big companies or projects), things are not just as simple as they seem on the surface. Completing deals and incentives involves many parts that may not be part of the announcement (e.g., token swaps, grants, incentives, etc.). Retail investors should always consider whether the appeal of the protocol is organic and invest accordingly. - Sachi Kamia, Polygon Ventures

Jaimin also emphasized risk management, but his final advice resonated with me as well. "I also advise people to improve their skills, read, and never stop learning. DeFi is evolving very quickly, and understanding the areas you are interested in can be beneficial: you can reason and add value to the entire project."

Interestingly, as I was writing this blog post, Sachi had just tweeted

We retail investors can also do well in the crypto space. Like retail investors, VCs also invest in hot projects due to FOMO. My advice is to do your research and lead the narrative instead of following it.