GRVT Hybrid Exchange: The Dawn of "Triple Witching Day" for the New Generation of Exchanges

"We are weak because of our ignorance of the unknown, our misunderstanding of randomness, our misreading of probability, and our beliefs about risk and decision-making." — "The Black Swan"

"We are weak because of our ignorance of the unknown, our misunderstanding of randomness, our misreading of probability, and our beliefs about risk and decision-making." — "The Black Swan"Author: Kit, CatcherVC

Black swan events have always been a mirror reflecting the blind overconfidence of individual and institutional investors in data interpretation and statistical probabilities. Since the release of the Bitcoin white paper, the crypto market has experienced several black swan events, including Mt Gox, The DAO, bans, exchange shutdowns, and the insolvency of FTX. The FTX collapse in 2022 brought the warning "Not your keys, not your coins" back to everyone's ears. As a result, CEXs jointly issued nominal Proof of Reserves (PoR), and technologies like MPC, homomorphic encryption wallets, and zero-knowledge proofs have rekindled the crypto community's interest in DEXs and self-custody.

At this moment, GRVT was born. GRVT is a Layer 3 exchange that provides cross-asset hedging perpetual contracts and options, built on the Layer 2 data availability foundation of ZKSync, and plans to use the Validium solution to offer users a trusted high-performance trading experience. Co-founded by Hong Gyu Yea, Matthew Quek, and Aaron Ong, their original intention was to create a new generation of Hybrid Exchange (HEX) using existing ZK encryption, blockchain technology, and high-performance trading systems to solve the dilemma faced by centralized exchanges between high-performance trading and user fund security. According to GRVT founder Hongyea, GRVT plans to develop a testnet in the fourth quarter of 2023 and launch the mainnet in the first quarter of 2024.

Key Point 1: Current Status of CEX/DEX

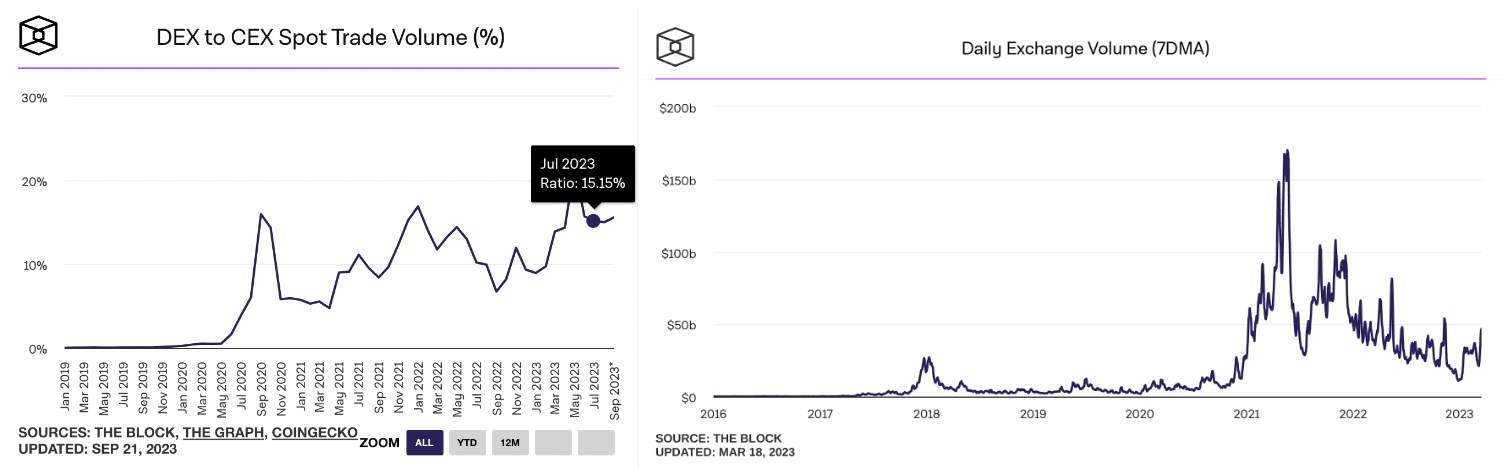

( Source: TheBlock)

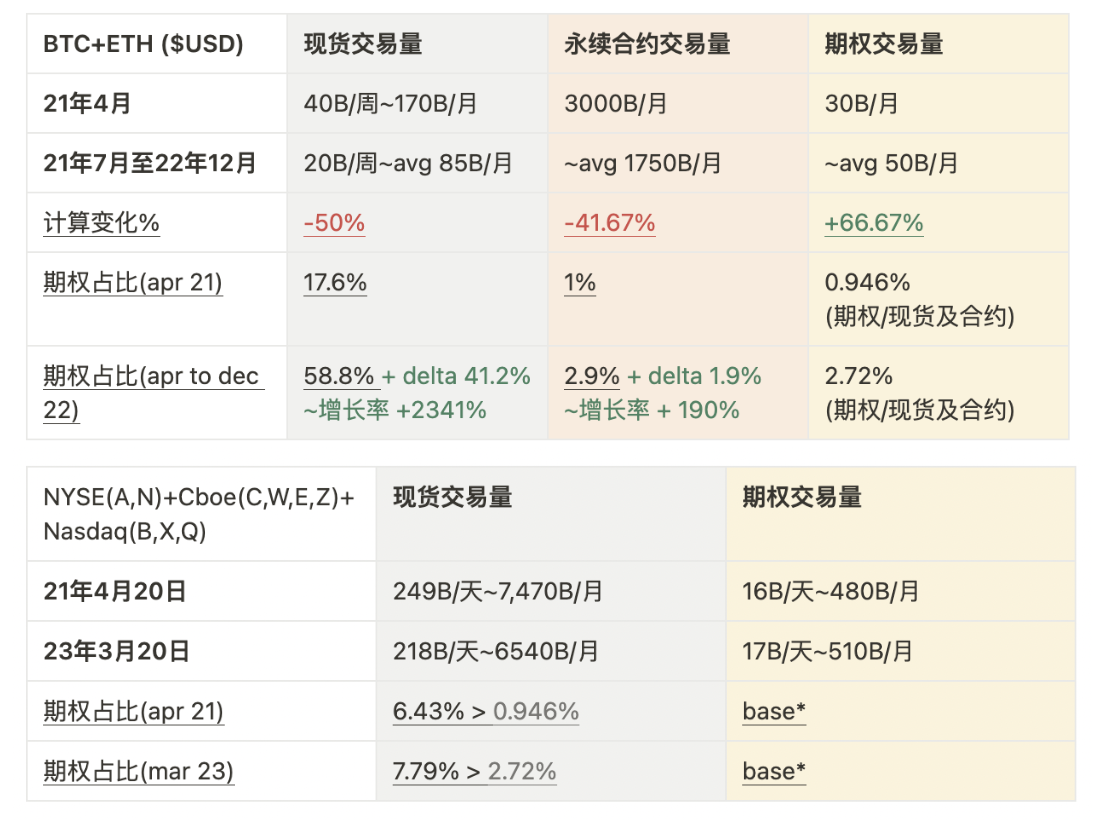

- Spot Trading: From 2017 to 2023, the 7-day average trading volume of cryptocurrencies on CEXs grew from $50 billion to $500 billion. The emergence of on-chain liquidity exchanges like Uniswap from 2019 to 2023 allowed DEXs to stand out from centralized exchanges. DEXs have grown from nothing to now occupy 15% of the spot market trading ratio, while native Ethereum applications like Uniswap and Curve have established an oligopoly effect on EVM-centric chains.

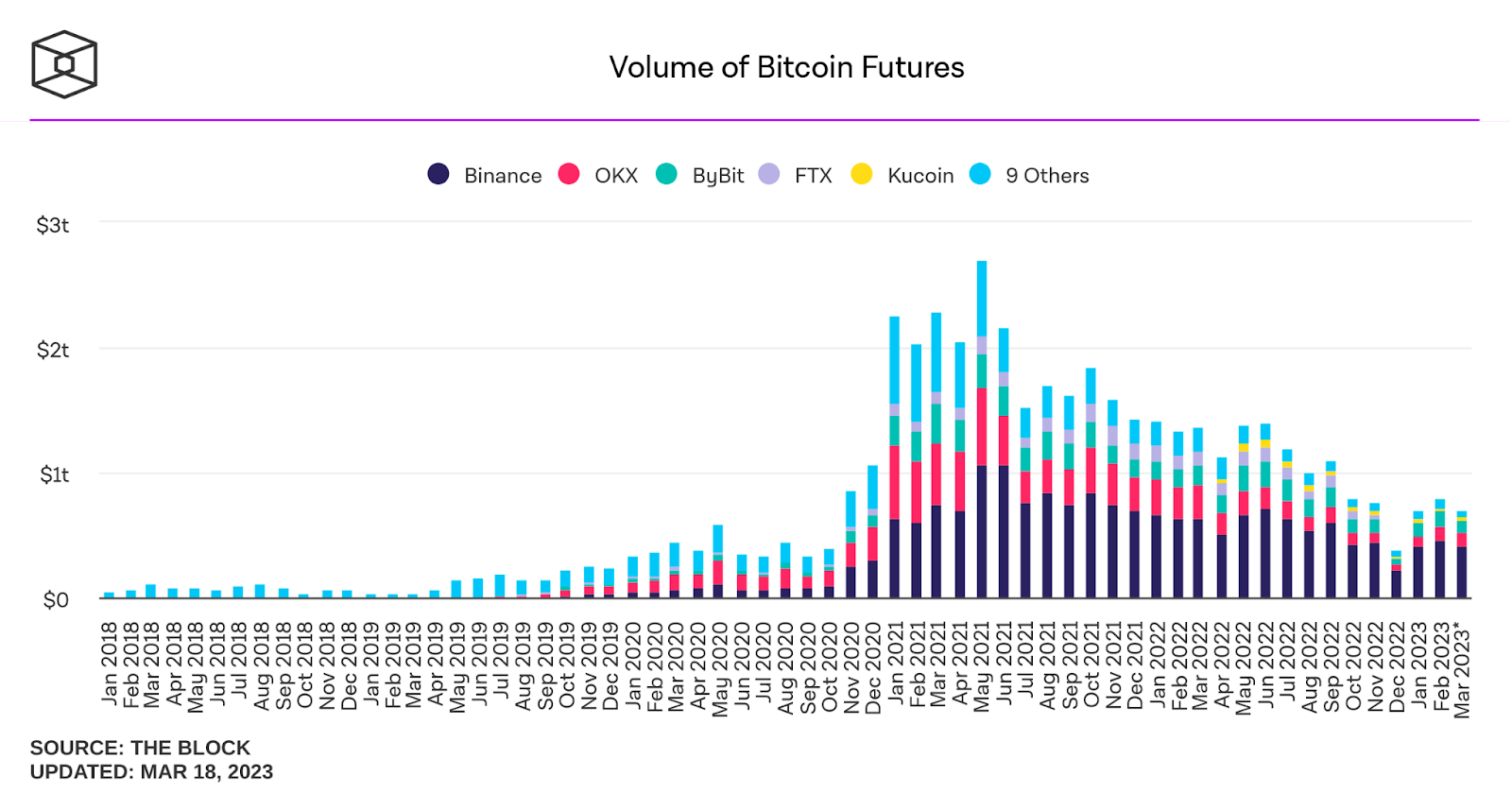

( Source: TheBlock)

- Perpetual Contracts: Since Bitmex launched perpetual contract trading in 2016, major exchanges have also introduced leveraged contract trading systems. The trading costs and high-performance experience of centralized trading systems provide convenient custodial services for investors and generate substantial profits for exchanges. However, centralized services have also been criticized for their opaque "pinning" counterparty trading, single point of failure hacking risks, and the risk of misappropriating user assets. According to TheBlock data, the average monthly trading volume of BTC and ETH perpetual contracts in 2022 exceeded the total average monthly trading volume of all cryptocurrencies, indicating that if Old Money institutions and market makers enter the market, their biggest concern should be the counterparty trading risks of centralized exchanges. Leveraged trading should be a double-edged sword for market funds, not a black hole for counterparty exploitation.

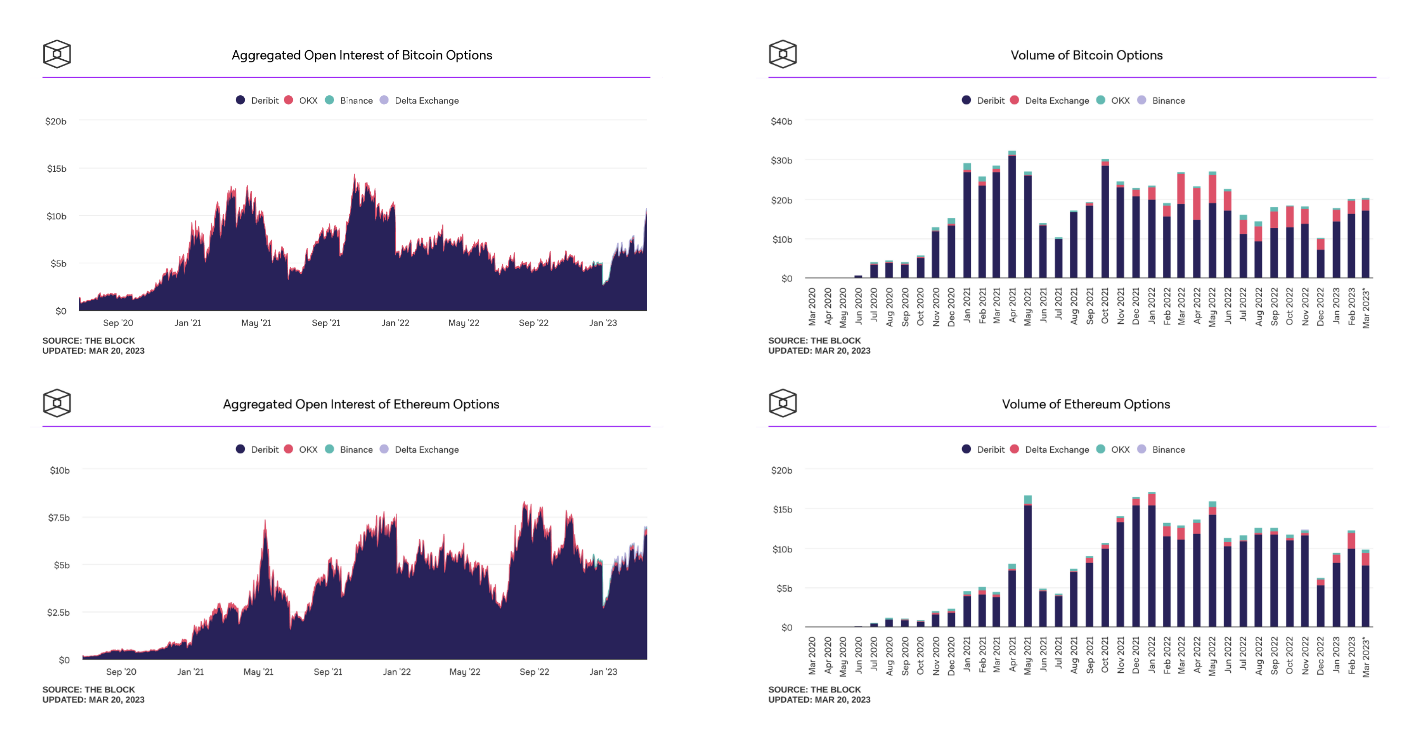

( Source: TheBlock)

- Options: The cryptocurrency market has experienced two cycles of wild growth, and we have seen a new trend: "The emergence of professional investors and mature derivative trading tools has led to a decrease in market volatility returns (distribution chart price volatility 123Sigma), while the activity and trading volume of the options market are rapidly increasing." This not only reflects the importance of options as hedging tools but also reveals their enormous growth potential. As of March 2023, TheBlock data shows that the trading volume of BTC and ETH options reached $45 billion in monthly trading volume during the bull market from 2020 to 2021, and has already recovered to the previous bull market peak in the first quarter of 2023, maintaining strong trading volume. This understated data fully reflects the activity and growth potential brought by professional traders entering the options market. With changes in the macro environment and uncertainties surrounding the next halving, the demand for hedging tools among professional traders is also increasing.

- Traditional Options Market: Compared to traditional Nasdaq and CBOE options markets, although the current hedging level of the cryptocurrency options market is still relatively low, its growth speed and potential cannot be ignored. Especially in the context of shrinking spot and perpetual contract trading volumes, the rise in options trading volume demonstrates its important position in the market. The main oligopoly in crypto options, Deribit, officially launched collateral asset options on the same platform for hedging trading in 2020 and quickly captured the bulk trading market. Subsequently, OKX launched an internal customer options market, which accounted for only 1%-5%. The market share of Delta Exchange, launched in 2021, peaked at 10%-15%. In fact, products like Binance's dual currency win, Amber's shark fin, and OKX's options have been launched for a long time, but due to the correlation of volatility returns in cryptocurrencies and the aforementioned counterparty risks, these structured products based on vanilla and heterogeneous options with fixed income have not received enough attention in the early stages of the industry. In the second quarter of 2023, Binance's officially opened unilateral options trading section and OKX's launched snowball product section also proved that centralized exchanges have felt the subtle changes in the market and their determination to seize the high-certainty growth derivatives track.

Solution: RFQ + Cross-Asset Full Margin Hedging

The GRVT team believes that an options trading market without futures or contract full-margin collateral trading options cannot provide complex trading strategies and has low capital utilization. Conversely, a derivatives exchange without options trading cannot provide sufficient hedging tools for professional traders. Therefore, they designed full-margin hedging options from the outset of product design. Additionally, the RFQ inquiry system via Telegram and API can help traders and institutions quickly and conveniently inquire about the customization and execution of complex structured strategies. The margin system and the hedging function within the same platform are key designs that significantly improve collateral utilization. Therefore, the open ecosystem of on-chain derivatives interfaces and off-chain matching and settlement can provide a safe, rich, and powerful one-stop comprehensive trading platform for bulk traders while continuously developing underlying crypto technologies.

Key Point 2: Trust Crisis in Custodial Services

(Source: Vitalik, https://vitalik.ca/general/2022/11/19/proofofsolvency.html)

In 2022, the FTX collapse caused a $40 billion company to vanish in a week due to insolvency, leaving $8 billion in user assets owed. Since then, investors have deeply realized the internal accounting chaos and centralization of centralized exchanges, which forced exchanges like Binance to lead a coalition with other exchanges to launch hot wallet Proof of Reserves (PoR). In fact, PoR was first proposed by Kraken in 2014, and later Vitalik Buterin called for the use of zero-knowledge proofs (ZKP) with polynomial commitments (KZG) to replace the current deposit certificates generated by Merkle trees, ensuring higher security and improved privacy.

However, deposit certificates cannot prove whether a CEX is solvent. Customer assets only represent a portion of liabilities and do not include the exchange's credit and other businesses. Although public assets and addresses allow investors to track and analyze suspicious behavior, when insolvency and bank runs occur, user assets still cannot provide data scrutiny on the CEX's asset solvency or be frozen during the recovery litigation phase. In fact, the third-party liquidation of Mt Gox has always delayed applications to unscrupulously profit from investors.

Solution: High-Performance Engine + ZK Completeness

HongYea's original intention in founding GRVT was to protect user assets, allowing users to achieve one-click trading and low-latency experiences under self-custody accounts, similar to centralized exchanges. It is reported that GRVT's off-chain order book matching engine can achieve up to 600,000 TPS with latency below 2 milliseconds. When its trading execution combines with Validum ZK proofs, users can not only ensure the safety of their assets through Validum's data committee like DYDX (StarEx version) but also ensure the privacy of position information, liquidation lines, and other trading executions, significantly reducing the counterparty risks of current CEX solutions.

From the design stage, GRVT's system is compatible with ZK proofs and is built on the ZKSync Era Rollup. According to the current proof submission speed of ZKSync, all traders' assets can be confirmed and circulated on the Ethereum main chain within 2 to 24 hours. The speed of confirmation is crucial for the siphoning effect of large funds in TradeFi; if these large funds flowing into ZKRollup need to rely on a "third-party centralized cross-chain bridge" or "wait for a 7-day optimistic solution challenge period," the risks of theft, market instability, time dimensions, and settlement rates that these large funds bear are significant. The faster settlement speed of ZKRollup is one of the important factors needed for TradeFi Layer 2. Therefore, compared to derivative applications built on optimistic solutions like GMX and Lyra, users using GRVT on ZK scaling solutions do not need to bear the 7-day challenge period and the risks associated with third-party cross-chain bridge confirmations, making it safer and less costly, while the future potential for zero-knowledge expansion is also higher.

Although Validum proofs cannot yet preserve all historical trading execution records, with the evolution of ZK proof algorithms, according to Zhang Ye from Scroll Tech, ZK scaling solutions can achieve forced proof recovery. In the event of a black swan event or illegal data tampering, users can submit ZK proofs to question the safety of funds, thereby recovering frozen or lost funds. Compared to PoR's "ensuring the total amount of funds is correct," GRVT adheres to Vitalik Buterin's advocacy of using ZK proofs to guarantee users' "absolute withdrawal" rights.

Key Point 3: Compliance and Scrutiny

With the collapse of SBF and FTX, the U.S. decision to step into the crypto industry was also urgently halted. Uncertainties prompted A16Z to announce the establishment of a European office, Coinbase's Brian Armstrong to announce the vigorous development of Coinbase's derivatives trading platform in South America, the U.S. digital asset deposit and withdrawal channel Silvergate to be choked, and Binance to be summoned by the SEC. These pieced-together clues form a comprehensive crackdown by the U.S. on the crypto industry regarding regional, cultural differences, racial faces, and offshore funds. Due to regulatory pressure and the crackdown on giants, the emergence of a new generation of decentralized exchanges will be more difficult than in the previous cycle, and future on-chain regulations and restrictions will become increasingly severe and centralized. The arrest of Tornado developers, Consensys Metamask's default IP monitoring RPC, and Uniswap's integration of centralized purchasing channels also indicate that on-chain crypto natives are compromising on potential AML/KYC for large-scale users. In fact, Vitalik Buterin has also called for providing partial auditability to law enforcement agencies through ZK proofs to address the AML deficiencies that the Tornado project cannot achieve, facing an increasingly severe on-chain scrutiny system.

(Source: Vitalik, Blockchain Privacy and Regulatory Compliance: Towards a Practical Equilibrium, https://papers.ssrn.com/sol3/papers.cfm?abstractid=4563364)

Solution 3: Team Experience + AML/KYC

The GRVT team has rich experience in privacy data development and practical operations in traditional financial compliance. Founder HongYea is from South Korea and is based in Hong Kong, being an experienced trader with 9 years of experience in financial executive roles at Credit Suisse and Goldman Sachs in Hong Kong. Matthew serves as the Chief Operating Officer and previously led the blockchain and payments team at DBS Bank in Singapore to study traditional financial application scenarios for blockchain. Aaron is the Chief Technology Officer of GRVT and has served as the technical lead for two data privacy frameworks at Meta. According to the GRVT team, the project will provide a new generation of one-stop trading platform for global digital asset derivatives trading users, focusing on AML/KYC compliance, security, and high performance.

According to the disclosed seed and pre-seed round financing, the seed round was led by Matrix Partners, which has cross-domain venture capital experience, and ABCDE, which has a founding background in digital asset exchanges. Other institutions that invested in the seed and pre-seed rounds include Delphi Digital, a U.S.-based digital asset research-driven media, QCP Capital, a seed investor in Deribit, SIG, HackVC, Folius Ventures, Metalpha, CMS Holdings, Appworks, Fisher8 Capital, Kronos Research, 500 Global, Token Metrics Ventures, and Primal Capital, CatcherVC.

Conclusion

In summary, the innovation of the GRVT team lies in their commitment to creating a brand new and unique digital asset derivatives trading platform, which will establish a new hybrid trading standard among existing exchanges, decentralized trading platforms (DEX), and investors, as well as between spot, futures, and options. They leverage existing on-chain crypto blockchain technology and combine it with off-chain high-performance matching engines and OTC RFQ inquiry bots to provide a new hybrid trading platform (HEX) for the crypto industry, which is under regulatory pressure, facing centralized opacity risks, and low trust issues.