Folius Ventures: Identifying the Competitive Landscape and Potential New Opportunities in Web3 Gaming

This research report outlines the competitive landscape of the web3 gaming industry and existing viable entrepreneurial opportunities.

This research report outlines the competitive landscape of the web3 gaming industry and existing viable entrepreneurial opportunities.Original Title: "Game Special: The Journey to Find the North Star of Web3 Games Through the Whirlpool of Liquidity Exhaustion, Identifying the Entrepreneurial Competitive Landscape and Potential New Opportunities"

Original Source: Folius Ventures

Original Author: Aiko

Report Summary

Against the backdrop of rising standards in the global gaming industry and overcapacity, Web3 has become one of the ways for game manufacturers to recover costs due to its high profit margins throughout the entire lifecycle, attracting many Web2 teams. However, the current supply side of Web3 is experiencing overcapacity, while the demand side is facing liquidity exhaustion, and the drawbacks have gradually emerged after two years of development. Therefore, this research report outlines the competitive landscape of the Web3 gaming industry and the existing viable entrepreneurial opportunities.

For teams still in the product development phase of Web3, it is essential to recognize that as an industry with imperfect infrastructure but extremely high profit margins, teams must possess versatile capabilities; meanwhile, there is a significant cognitive gap between mid-tier and top-tier teams, which needs to be addressed quickly to accelerate learning and iteration. At the same time, new business models continue to emerge, and teams can fully leverage Web3 commercialization tools for innovation and seize market opportunities; they should also capitalize on the changes in the distribution landscape to capture traffic-oriented super apps and entry points or independently carve out markets to become super apps themselves.

Moreover, for those teams still exploring and observing, they can first seize the parallel opportunities between Web2 and Web3 at a time when customer acquisition costs in Web2 remain high and business models are hitting bottlenecks, especially among the large player base driven by casual games and AI. Secondly, summarizing and digesting past successful/hot project experiences can provide valuable methodologies for operational finesse. Thirdly, they can create products that meet more user entertainment needs and have long-term business models based on high-traffic entry points. Fourthly, based on new asset forms, there are still opportunities for gamification and commercialization innovation. Lastly, for fully on-chain games, it is recommended that teams create excellent open-source racetracks rather than reinventing the wheel, as there may be opportunities to spark the next wave of trends. Finally, the future of the Crypto agent (crypto + AI) field will likely still be traffic-driven, and teams should adhere to a traffic-dominated path, as on-chain AI agents will inevitably tend to collaborate with quality traffic entry points in the near future.

Corresponding to our previous two research reports, this attempt summarizes the cyclical changes in the industry and provides some more universal, macro, and feasible suggestions for entrepreneurs at different stages. During the writing process, we deeply realized that the industry has entered a deep-water zone, with slow infrastructure progress and a lack of market liquidity, making entrepreneurship quite challenging; however, we hope developers can find some methodologies and breakthrough inspirations to cope with the market winter in this article, and we sincerely salute the seekers who continue to move forward.

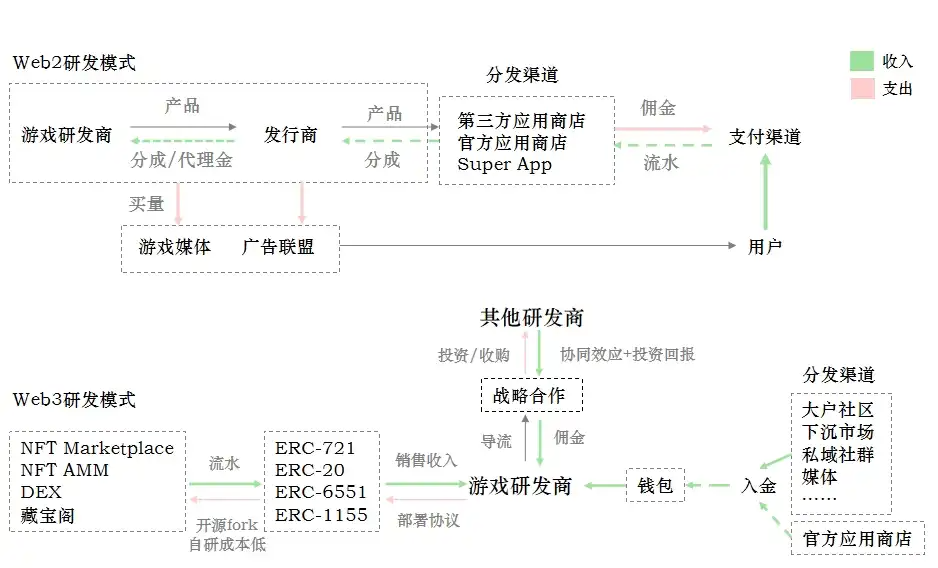

For many game manufacturers constrained by licensing and customer acquisition costs, Web3 is indeed a good choice

Web3 provides commercialization tools that encompass the entire lifecycle of games: NFT/FT/taxation. Compared to traditional R&D methods, Web3 is indeed an effective way to improve game profit margins and achieve globalization.

Supply Side: However, against the backdrop of elevated standards in both Eastern and Western gaming industries, Web3 has become the only outlet to absorb much of the excess productivity, and after two years of development, problems have gradually emerged.

Demand Side: We have entered an era of liquidity scarcity, with a limited existing market, scarce attention, and rapid shifts. Therefore, teams should focus on refining products and incentive models at this stage, striving to break through and acquire customers to catch the fast train of the liquidity-rich era.

What is the current competitive landscape for Web3 game entrepreneurship?

Analyzing from four dimensions: industry profit margins, team cognition, business models, and the market.

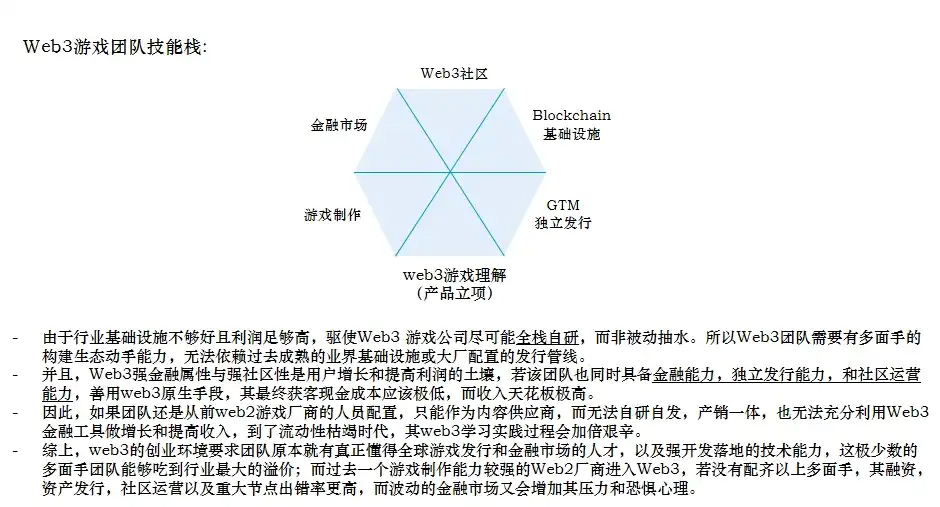

1. Web3, as an industry with imperfect infrastructure but extremely high profit margins, allows versatile teams to reap the greatest rewards, while teams lacking versatility will face greater difficulties and higher error rates.

2. There is a significant gap between mid-tier and top-tier manufacturers, and most manufacturers may not yet meet the threshold for competition, requiring teams to possess strong evolutionary capabilities and iteration speeds.

3. Business model innovations are emerging continuously. The more liquidity is exhausted, the more it demands new changes; Web3 business models are evolving with market hotspots/new asset forms, and teams need to innovate with a thorough understanding of the market and economic models.

4. The traffic potential of L1/L2 and platforms is gradually declining, with super ecosystems and traffic entry points rising above single L1/L2, expecting to compete in the next cycle. Project parties need to quickly choose the right trees to roost or actively explore new UA paths.

So, what directions are worth exploring for Web3 game teams during the liquidity exhaustion cycle?

1. Look for parallel opportunities between Web2 and Web3 games, especially as customer acquisition costs in Web2 are high and commercialization is hitting bottlenecks, catching up with new user consumption habits and AI experiences.

Phenomenon 1: Facing the same user group, customer acquisition costs in Web2 have risen again.

The growth of the global gaming market in 2023 has largely benefited from casual genres such as match-three, simulation management, and casual casino games. However, the cost of acquiring users in these genres is high, and after the explosive success of "Seeking the Dao of the Universe," the cost of acquiring users for traditional H5 mini-games has tripled. Web3 faces the same user habits but with lower customer acquisition costs and higher profit margins. Suggestion: Teams focusing on casual games can avoid platform-based strategies to compete for retention rates and instead leverage the characteristics of casual games, which have large traffic and quickly shifting attention, by continuously releasing products and using mutual advertising and token swaps in their self-built DEX to channel traffic and liquidity into new games.

Phenomenon 2: The gacha business model has hit a bottleneck, with little room for innovation.

The gacha (pay-to-win) business model was introduced from Japan to China and has been around for nearly a decade. However, in the past six months, especially after the domestic licensing restrictions were lifted, it has been found that player spending power is weakening, and the overall scale of user payments is declining. On the other hand, games like "Nirvana in Fire" have achieved success with light payment models and high DAU. Suggestion: Web3 has many commercialization tools suitable for innovation; it is recommended to read our previous two research reports to maximize the profit space of NFT + token + taxation.

Phenomenon 3: Simplified experiences lead to high-frequency engagement.

Finding a game that is easy to pick up and addictive, and mobile-optimizing it, can be seen from "Vampire Survivors" to "Shell Shockers," where a gameplay prototype from "Crazy Knights" has spawned several top-ranked games on WeChat mini-programs. It is evident that as user aesthetic fatigue sets in, more and more users choose to spend fragmented time on high-frequency stimulating mini-games. Suggestion: Simplifying and designing incentive mechanisms based on gameplay prototypes aligns better with the capabilities of Web3 teams. Moreover, the closer the design is to primitive stimuli like loot boxes, the more similar it is to the economic incentive pleasure of Web3 itself, thus allowing for more reference templates and overlapping user profiles. Web3 teams can also consider adding idle gameplay experiences to make the game itself have an "electronic board" effect, rather than allowing unlimited gold farming for 24 hours. Therefore, the previously mentioned "energy value system" design is also very important.

Phenomenon 4: Developing in parallel with AI and the gaming industry.

There are indeed parallel opportunities in the gaming industry led by AI, but it is advisable not to add physical entities unnecessarily. For teams that originally faced challenges or came to Web3 due to intense traditional competition, they should reconsider this industry transformation opportunity, especially in the context of facing regulatory scrutiny domestically and being unable to use large foreign models. It is best to leverage AI to create novel experiences and next-generation products while directly utilizing Web3 for global distribution and higher-leverage commercialization. Suggestion: Focus on economic/diplomatic/agency aspects for design. For example, the agent based on SLG games mentioned in the article. This also implies more trading and profit space for AI.

2. Seize the window period to digest previously validated Web3 strategies, using clever tactics in the early to mid-operation stages.

Early Stage:

- Find the right data pool: (Refer to Friend.tech) When incentivizing creators on X (formerly Twitter) and triggering social media dissemination effects, they accessed this open data source (API interface or data scraping) and quickly completed the financialization of KOLs (Share). Perhaps entrepreneurs in this direction can also explore other suitable data pools. After all, the core of their business model is to select important off-chain Pow and traffic for packaging on-chain, with the purpose of renting valuable data, information, and people.

- Batch invitation system: (Refer to STEPN, Friend.tech) Gradually release users in batches using an invitation mechanism while completing product testing at various stages. Allowing FOMO social virality to serve as a precursor to economic incentives, slowing down user entry speed in the early stages actually extends the overall operational lifespan of the project.

- NFT operation experience: (Refer to Memeland, Matr1x) Given that the NFT market has left behind enough cases and gameplay, operating this game in an NFT-driven manner has many playbooks to reference, and even has a relatively complete industrial chain (centered around NFT operators, whitelist intermediaries, and KOLs). (1) Early marketing on Twitter and alpha communities to deepen community engagement; (2) Small liquidity and easy control to create wealth effects; (3) Continuous anticipation of several NFT series can help maintain favorable prices; (4) Whether for issuance or speculation, it can help teams earn some money without spending a dime; (5) Ultimately solidifying through products + FT Airdrop + cash flow.

- Customer acquisition/Regional arbitrage: (Refer to Axie, Hooked) Conduct more UA testing channels, capturing users in low customer acquisition cost regions for on-chain arbitrage; simultaneously establish local promotion & distribution systems (guilds) and add a token incentive layer, where the wealth effect of tokens is more pronounced compared to local per capita income levels, leading to opportunities for dissemination and breaking through.

Mid Stage:

- Rolling server logic: (Refer to STEPN) Many people are now telling traditional manufacturers the story of "Web3 distribution" when acquiring IP, but many traditional manufacturers do not realize that Web3 is not the only way to view global distribution; you can even reissue on every chain. Given the significant differences in liquidity/user profiles/traffic support on each chain (especially in the era of high TVL), cross-chain issuance of new assets is like building head mines for users, who will continuously enter new chains to earn early-stage money. Alternatively, similar to rolling servers in traditional games, users can practice new accounts on a new starting line, validate their strategic assumptions, and gain positive feedback.

- Casual/fractal operation: (Refer to BAYC) For mature IPs, games can be seen as a tool to enhance community cohesion and attention during the operational phase, thus emphasizing high frequency and asset FOMO, without the need to create AAA and lengthy games.

3. Relying on high-traffic entry points, create products that meet more user entertainment needs and have long-term business models, in other words, spread existing entertainment needs + business models that have been successful in Web2 through new traffic channels and incorporate Web3 incentive layers.

Telegram bot:

After Uni bot quickly gained popularity, many entrepreneurs have jumped into the TG bot space to create clones, but currently, we only see minor adjustments in trading bots and GPT-like bots in terms of strategy/performance. Although trading bots have rapidly risen by meeting the trading needs of crypto users, their business models are singular, and the optimization ceiling for UI/UX and trading strategies is low, with user scales yet to break the ten-thousand mark, making it a long road to truly break through customer acquisition. Therefore, new TG bot entrepreneurs need to broaden their thinking, trying products that better align with the habits of the broader consumer base and establishing long-term stable business models. A low-cost trial-and-error method is to directly spread business models that have already been successful in Web2 (gambling) through new traffic channels (Telegram) and add Web3 incentive layers (token + NFT), with Rollbit as a representative case. Additionally, the following ideas are for reference:

Examples:

Game-related: Following the infrastructure development trajectory of WeChat mini-programs, TG bots can provide gaming performance and educate users from deep to shallow. It is advisable to conduct more testing, combining the main user distribution areas (India, Russia, the Middle East, etc.) and gaming preferences to pinpoint user profiles. It is speculated that TG's broad user base can accept elemental games, and breaking through and growing will rely on social and viral games, while crypto users are more likely to accept nurturing + PVP card gameplay. Simple elemental games - Link-up, Tetris. Social gathering games - Pictionary, Who's the Spy. Comparison and viral games - Jump Jump, Sheep Game. Idle card games - Currently ranking high on WeChat mini-programs, such as Seeking the Dao of the Universe, King of the Fish Market, etc.

Lottery-related: Given the increasing number of valuable assets, not only are there consensus blue-chip NFT assets (BAYC/Punk), but also IP co-branded assets and real-world collateral on-chain (like Pokémon cards on-chain), combined with various lottery gameplay and dividend incentive mechanisms, there are many ways to play. One Yuan Treasure Hunt - Everyone has a chance to participate in the NFT blind box lottery for valuable items with just 1 yuan. Game blind boxes - Similar to participating in tree-planting games to receive fruit blind boxes, participating in NFT games to receive NFT blind box lotteries. Bargain group buying - Group buying fragmented blue-chip NFTs or directly creating a TG launchpad bot, allowing low-cost acquisition or participation in lotteries through sharing and group buying, bringing the original Discord white-listing methods over.

Private domain: The first two involve the dissemination and virality of TG groups, and since TG is still in the early stages of content ecology, before the content matrix is established, it is advisable to combine DAO + creator ecology to build and commercialize private domains. Publishing links - Whether in group chats or channels, publishing links can earn commissions, tracing the conversion rates through browsing-clicking-downloading-sharing steps, and directly depositing rewards into users' wallets within the community. Creator community - Establish a ranking voting bot within the creator's community, with public announcements of competition results, and those ranking higher can receive token rewards.

4. There are still opportunities for gamification + commercialization innovation based on assets: Treasure Vault

Background 1: The overall liquidity of the NFT market is exhausted, and the NFT market needs new narratives and trading hotspots.

Background 2: At the application layer, the complexity of NFT-driven game assets has already risen, with many types and large quantities of assets under the same IP, intricately linked, with final value reflected in products and tokens. However, players still need to conduct off-market transactions in communities or manually search for and purchase NFTs that meet requirements one by one, making the trading methods very primitive.

Background 3: At the protocol layer, with the emergence of ERC-6551 and ERC-4337, although the underlying technical issues of account abstraction wallets have not yet been resolved (e.g., they do not support stable wallet generation with private keys), as infrastructure improves, the granularity of accounts and assets will differ significantly from now. Just as ERC-721 and ERC-20 have completely different interaction forms/financial property logics, future asset forms will be: multi-entity + multi-granularity nested, making unified pricing more challenging, thus making the financial interaction forms and scenarios of future assets more interesting.

5. Fully on-chain games: Create excellent open-source racetracks rather than reinventing the wheel, finding sufficiently wealth-generating innovative mechanisms and productizing + gamifying them to ultimately break through and acquire external liquidity.

Background 1: Fully on-chain narratives inherit liquidity from NFTs and GameFi. Loot emerged alongside BAYC, Punk, etc., with its market price peak coinciding with the highest participation in the fully on-chain game pioneer Dark Forest community. Fully on-chain competitive games (like Wolf Game, Sunflower, etc.) also appeared after Axie and GameFi summer, but FDV remains below $5M, which is one-fourth of Axie's and one-fifth of STEPN's, indicating that the likelihood of social competitive fully on-chain games emerging in the context of liquidity exhaustion in both NFTs and GameFi is low, and even if they explode, it is unlikely to break through customer acquisition.

Background 2: To prevent fully on-chain games from ultimately becoming raw and brutal POS/POW competition and to optimize UI/UX, teams need to delve into technical issues, with a gradual emergence of trends toward self-built Appchains/L2 for fully on-chain games, digging deeper layer by layer. The closed environment of games and test networks has only a few dozen test users, making it easy to reinvent the wheel and lacking universality, with no signs of open-source development, making it a long road to achieving permissionless and interoperable solutions.

Analyzing past innovations in fully on-chain games, three commonalities can be summarized: 1) Innovations in fully on-chain games may not appear in main quests but rather in side quests. If valuable side quests can be identified and productized in this process, it may lead to the creation of universal infrastructure, and if financialized + gamified on top of the product to significantly lower user thresholds, it can drive new liquidity influx. 2) Games centered on simple yet FOMO-inducing asset gameplay with wealth effects are more likely to drive breakthrough innovations: For example, the prize pool dividend mechanism in Fomo3D and the breeding deflation mechanism in CryptoKitties that leads to asset appreciation can create excellent racetracks.

6. In the era of AI agents, traffic remains king. Traffic-driven + crypto agents are more likely to scale and find good commercialization paths, while backend AI can continuously optimize + modularize and seek collaboration with quality traffic entry points.

Disclaimer

The information in this presentation has been prepared by Folius Ventures LLC ("Folius"), which believes it to be reliable and has been obtained from sources deemed reliable. Folius Ventures makes no representations as to the accuracy or completeness of such information. The opinions, estimates, and projections in this presentation constitute Folius Ventures' current judgment and are subject to change without notice. Any forecasts, projections, and estimates contained herein are inherently speculative and based on certain assumptions. Furthermore, the matters described are subject to known (and unknown) risks, uncertainties, and other unpredictable factors, many of which are beyond Folius Ventures' control. No representations or warranties are made regarding the accuracy of such forward-looking statements. It is expected that some or all of such forward-looking assumptions will not be realized or will differ significantly from actual results. Therefore, any forecasts are merely estimates, actual results may vary, and may differ significantly from the forecasts or estimates shown. Any investment strategy, including the strategies described herein, involves a high degree of risk. There is a possibility of loss, and all investments involve risks, including the loss of principal. This presentation does not constitute an offer to sell any investment fund securities or an invitation to purchase any such securities, nor does it constitute a recommendation to buy or sell any digital assets or securities. This presentation does not consider or provide any tax, legal, or investment advice or opinions regarding the specific investment objectives or financial situation of any person. If any matters described herein or any opinions, projects, forecasts, or estimates described herein change or subsequently become inaccurate, Folius Ventures has no obligation to update, amend, or revise this presentation or otherwise notify its readers. The graphics, charts, and other visual aids are for reference only. These charts, graphs, or visual aids should not be used to make investment decisions. They do not indicate that they will assist anyone in making investment decisions, nor do any charts, graphs, or other visual aids capture all factors and variables necessary for making such decisions. The descriptions of Folius Ventures' methods and the target characteristics of its strategies and investments are based on current expectations and should not be construed as definitive or guaranteed that methods, strategies, and portfolios will actually have these characteristics. These descriptions are based on information available as of the date of this presentation and may change over time. Past performance of these strategies does not necessarily indicate future results.