Pantera Capital: Three Emerging Catalysts in the Crypto Space

This article discusses three aspects: the dawn at the end of the "Bitcoin-ETF" tunnel, the similarity in maturity between the crypto industry and stocks, and digital property rights and scarcity.

This article discusses three aspects: the dawn at the end of the "Bitcoin-ETF" tunnel, the similarity in maturity between the crypto industry and stocks, and digital property rights and scarcity.Original Title: "Emerging Catalysts in Crypto"

Original Source: panteracapital

Original Compilation: Kate, Marsbit

This article is written by three authors, discussing the "light at the end of the Bitcoin-ETF tunnel," the similarity in maturity between the crypto industry and stocks, and the concepts of digital ownership and scarcity.

"Light at the End of the Bitcoin-ETF Tunnel"

Authors: Portfolio Manager Cosmo Jiang and Content Director Erik Lowe

In recent months, there have been some positive developments in the U.S. crypto regulatory environment. In our previous blockchain letters, we wrote about the three-year lawsuit between the U.S. Securities and Exchange Commission (SEC) and Ripple Labs, in which the Southern District Court of New York ruled that XRP is not a security. We referred to it as a "positive black swan," something that almost no one anticipated.

Cryptocurrency recently achieved another unexpected victory. On August 29, a U.S. appeals court made a favorable ruling for Grayscale in its lawsuit against the SEC regarding the rejection of its spot Bitcoin ETF application last year. We believe this significantly increases the chances of approval for Bitcoin ETF applications from companies like BlackRock and Fidelity.

While the U.S. seems to lag behind many parts of the world in embracing digital assets, many countries have taken the same or even harsher measures against cryptocurrencies. However, the advantage of the U.S. is its court system, which is committed to procedural due process, ensuring there are corrective avenues when boundaries are crossed.

"The rejection of Grayscale's proposal was arbitrary and capricious, as the Commission failed to explain its different treatment of similar products. Therefore, we agree with Grayscale's request and vacate the injunction." ------ Opinion submitted to the court by Circuit Judge RAO

We have consistently emphasized the need for trustless systems. In our industry, this means users can rely on blockchain-based architectures to execute fairly as designed. Our reliance on the U.S. court system's ability to do the same may help shape a promising regulatory environment for cryptocurrency in the future, allowing for further innovation to occur domestically.

We have been discussing the possibility of a spot Bitcoin ETF, but now we see some light at the end of the tunnel.

Key Points of Grayscale vs SEC

Ruling: The D.C. Circuit Court ordered the SEC to vacate its rejection of Grayscale's Bitcoin ETF conversion.

The rejection of Grayscale's conversion to an ETF was "arbitrary and capricious," as the SEC failed to explain its different treatment of similar products (approving Bitcoin futures ETP while rejecting Bitcoin spot ETP).

This was a unanimous decision by a panel of three judges, 3-0, which is a resounding ruling rather than the expected split decision.

Note: Federal appellate courts rarely find an agency in violation of the Administrative Procedure Act.

Core of the Argument:

Grayscale argues that the regulatory framework for Bitcoin futures ETFs by CME should also satisfy Grayscale's spot ETF, as both products rely on the underlying price of Bitcoin.

However, the SEC believes Grayscale lacks data to determine whether CME's futures regulatory framework can also detect potential manipulation in the spot market.

The court summarized the arguments and its ruling in two points:

The SEC itself stated that when approving Bitcoin futures ETPs, fraud in the spot or futures markets could be detected through the regulation of the CME futures market.

The SEC's rejection based on "significant market tests" lacked a reasonable and coherent explanation.

The court found that the correlation between futures prices and spot prices is as high as 99.9%, meaning that fraud in the spot market would be reflected in the futures market.

Timeline: Both parties have 45 days to appeal the ruling, and the SEC can still find other avenues to reject Bitcoin spot ETF applications.

The SEC can appeal to the full judges of the U.S. District Court or to the Supreme Court, but this is unlikely as the case is not that significant from a legal standpoint (even though it is important for this specific industry).

Grayscale previously announced that after winning in court, it intends to seek ETF conversion, which may proceed after the appeal period ends.

The appeal timeline in mid-October also coincides with the SEC's deadline to respond to all other Bitcoin spot ETF applications.

You can read the court's ruling here.

Similar Maturity of the Crypto Industry and Stocks

Author: Cosmo Jiang, Portfolio Manager

Today, the maturity of the digital asset space may resemble the inflection point of the stock industry’s maturity.

Tokens are a new form of capital formation that may replace equity for an entire generation of companies. This means that many companies may never list their stock on the New York Stock Exchange. Instead, they will simply have a token. This is how companies combine incentives with management teams, employees, token holders, and (unique digital assets) potential other stakeholders such as customers.

There are about 300 publicly traded liquid tokens with a market capitalization of over $100 million. As the industry expands, this investable space is expected to grow over time. There are more and more protocols with product use cases, revenue models, and strong fundamentals. Just two or three years ago, applications like Lido or GMX did not exist. In our view, a significant source of alpha may come from filtering ideas in this vast universe, as not all tokens are equal, just as not all stocks are equal.

Pantera focuses on finding protocols with product-market fit, strong management teams, and attractive, defensible unit economics, and believes this is a universally overlooked strategy. We believe we are at an inflection point for this asset class—traditional, more fundamental frameworks will be applied to digital asset investing.

In many ways, this is similar to the significant turning points in the evolution of the stock market over time. For example, fundamental value investing is taken for granted today, but it only began to gain traction in the 1960s when Warren Buffett launched his first hedge fund. He was an early pioneer and practitioner of applying the lessons of Benjamin Graham, who founded what we now know as the long/short equity hedge fund industry.

Cryptocurrency investing is also akin to emerging market investing in the 2000s. It faces many criticisms similar to those of the Chinese stock market at that time, where there were concerns that many companies were small players in a retail-driven, irrational market. You didn’t know if the management teams were misleading investors or misappropriating funds. While there is some truth to this, there are also many high-quality companies with strong long-term growth prospects that represent excellent investment opportunities. If you are a discerning, fundamentals-oriented investor willing to take risks overseas and work hard to find those good ideas, you can achieve incredible investment success.

The main point of our paper is that digital asset prices will increasingly trade based on fundamentals. We believe that the rules applicable to traditional finance also apply here. There are now many protocols with real revenue and product-market fit attracting loyal customers. Increasingly, investors are pricing these assets based on fundamentals using traditional valuation frameworks.

Even data service providers are beginning to resemble the traditional financial industry. But they are not Bloomberg and M-Science; they are Etherscan, Dune, Token Terminal, and Artemis. In fact, their purpose is the same: to track key performance indicators, profit and loss statements, management team actions and changes, and more.

We believe that as the industry matures, the next trillion dollars entering this space will come from institutional allocators trained in these fundamental valuation techniques. By investing within these frameworks, we believe we are ahead of this long-term trend.

Fundamentals-Based Investment Process

The fundamentals-based digital asset investment process is similar to the investment process for traditional stocks. This may come as a surprise to investors in traditional asset classes and is an important misconception.

The first step is to conduct basic due diligence—answering the same questions we would when analyzing publicly traded stocks. Does the product meet market demand? What is the total addressable market (TAM)? What is the market structure? Who are the competitors, and what is their differentiation?

Next is business quality. Does this business have a competitive moat? Does it have pricing power? Who are its customers? Are they sticky or quick to churn?

Unit economics and value capture are also very important. While we are long-term growth investors, cash is king, and we want to invest in sustainable businesses that can ultimately return capital to their token holders. This requires sustainable unit economics and value capture.

The next layer of our due diligence process examines the management team. We care about the management team's background, track record, incentives, and what their strategy and product roadmap are. What is their listing plan? What strategic partnerships do they have? What is their distribution strategy?

The first step is to gather all fundamental due diligence information for each investable opportunity. Ultimately, we build financial models and investment memorandums for all core positions.

The second step is to translate this information into asset selection and portfolio construction. For many of our positions, we have multi-year three-statement models with capital structures and forecasts. The models we create and the memorandums we write are at the core of our process-oriented investment framework, enabling us to have the knowledge and foresight to select investment opportunities and adjust position sizes based on event path catalysts, risk/reward, and valuation.

After making investment decisions, the third step is to continuously monitor our investments. We have a systematic process for collecting and analyzing data to track key performance indicators. For example, for our investment in the decentralized exchange Uniswap, we actively extract on-chain data from data warehouses to monitor Uniswap and its competitors' trading volumes.

In addition to monitoring these KPIs, we also strive to maintain dialogue with the management teams of these protocols. We find it important to conduct field surveys with management teams, their customers, and various competitors. As mature investors in this space, we are also able to leverage Pantera's broader network and connections with the community. We see ourselves as partners and are committed to adding value where we can help management teams and contribute to the development of these protocols, particularly in areas like reporting, capital allocation, or management best practices.

Fundamentals-Based Investment Practice: ARBITRUM

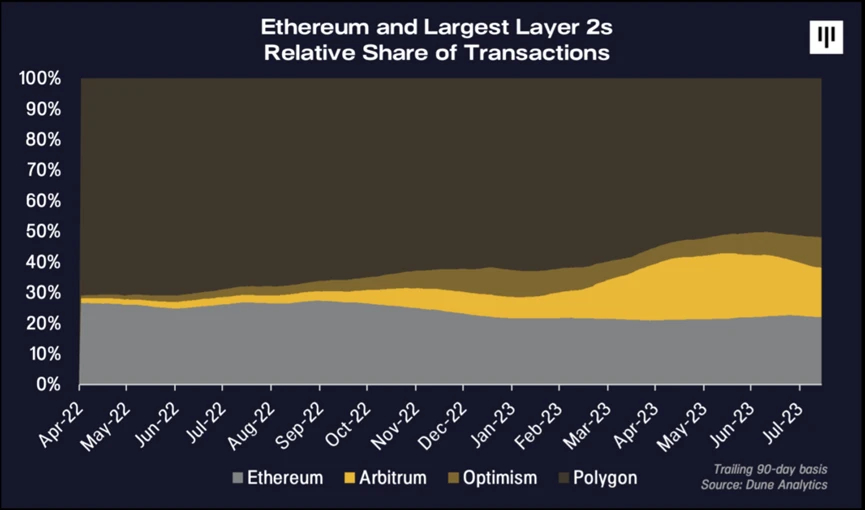

A major criticism of Ethereum is that transactions on the base layer can be slow and expensive during periods of high activity. While the roadmap for creating scalable platforms has been contentious, second layers like Arbitrum are emerging as viable solutions.

Arbitrum's key value proposition is simple: transactions are faster and cheaper. Its transaction speed is 40 times faster than Ethereum, at a cost 20 times lower, while being able to deploy the same applications and maintaining the same security as Ethereum transactions. Thus, Arbitrum has found a product-market fit and has shown strong growth, both in absolute terms and relative to its peers.

For an investor focused on fundamentals, looking for evidence of fundamental traction growth in protocols, Arbitrum would rank highly. It is one of the fastest-growing Layer 2s on Ethereum, capturing a significant share of the trading market over the past year.

To delve deeper into this point, Arbitrum is one of the few blockchains that has seen growth in trading volume throughout the bear market, while overall usage has remained weak during this period. In fact, when breaking down the data, you will find that Arbitrum has contributed 100% of the incremental growth to the Ethereum ecosystem this year, compared to Ethereum and all other Layer 2s. Arbitrum is a massive share recipient within the Ethereum ecosystem, and Ethereum itself is a massive share recipient across the entire cryptocurrency space.

The network flywheel of Arbitrum is turning. Based on our field surveys, it is clear that developers are attracted to Arbitrum's growing usage and user base. This is a positive network flywheel: more users mean more developers interested in creating new applications on Arbitrum, which in turn attracts more users. But as fundamental value investors, we must ask ourselves, is this activity meaningful unless there is a way to monetize it?

Answering this question is why we believe this is a great fundamental investment opportunity—Arbitrum is a profitable protocol with multiple potential catalysts.

Many transient investors in this space may not realize that some protocols can actually generate profits. Arbitrum generates revenue by charging transaction fees on its network, batching these transactions, and then paying fees to the Ethereum base layer to publish this large merged transaction. When users spend 20 cents on a transaction, Arbitrum collects that fee. They then bundle these transactions together and publish them to Ethereum Layer 1, paying about 10 cents per transaction. This simple math means that Arbitrum has a gross profit of about 10 cents per transaction.

We have identified a protocol that has found a product-market fit and has reasonable unit economics, which ultimately leads us to believe that the valuation is reasonable.

Key Operating Metrics Achieving Growth

Some of the charts below illustrate some fundamental principles.

Since its launch, active users have grown quarter over quarter, with quarterly transaction volumes approaching 90 million. Revenue for the second quarter was $23 million, with gross profit nearing $5 million, annualized to $20 million. These are some key KPIs that we can track and verify daily on the blockchain to monitor whether Arbitrum aligns with our investment thesis and financial forecasts.

Today, there are an average of 2.5 million users per month, each conducting an average of 11 transactions per month, totaling about 350 million transactions per year. Based on this data, Arbitrum's annual revenue is close to $100 million, with normal gross profit around $50 million. Suddenly, this becomes a very interesting proposition.

In terms of catalysts and factors making it a timely investment, a key part of our research process is following the entire Ethereum technology roadmap. The next significant step is the upgrade of EIP-4844, which will effectively reduce transaction costs for Rollups like Arbitrum. Arbitrum's main cost, the 10-cent transaction fee, could be reduced by 90%, down to 1 cent per transaction. By then, Arbitrum will have two options. They can pass the savings on to users, further accelerating user adoption, or they can take the savings as profit, or both. Either way, we expect this to be a material catalyst for increasing Arbitrum's adoption and profitability.

Valuation awareness is an important component of fundamental investing. Based on shares outstanding, Arbitrum currently has a market capitalization of $5 billion. In our view, this is quite attractive relative to other Layer 1 and Layer 2 protocols trading at similar market capitalizations, but its usage, revenue, and profits are just a small fraction of Arbitrum's potential.

From a growth perspective, we believe that Arbitrum's transaction volume will exceed 1 billion next year, with a profit of 10 cents per transaction. This translates to about $100 million in revenue, meaning that at a $5 billion market cap, the company's valuation is about 50 times expected earnings. From an absolute perspective, this may seem expensive, but in our view, it is reasonable for an asset still growing at triple-digit rates. Compared to real-world business valuations, if you look at well-known software companies with double-digit revenue growth rates, like Shopify, ServiceNow, or CrowdStrike, their average price-to-earnings ratios are around 50 times, and their growth rates are far lower than Arbitrum's.

Arbitrum is a protocol with product-market fit, growing rapidly (both in absolute terms and relative to the industry), with clear profitability, and its trading valuation is reasonable relative to its own growth, other crypto assets, and other assets in traditional finance. We will continue to closely monitor these fundamentals, hoping our thesis will play out.

Macro Catalysts

Some upcoming macro catalysts may have a meaningful impact on the digital asset market.

While institutional investor interest has waned over the past year, we are closely watching for events that may reignite investor interest in the future. Most notably, the potential approval of a spot Bitcoin ETF. Specifically, BlackRock's IPO is significant for two reasons. First, as the world's largest asset management company, BlackRock is under intense scrutiny and only makes decisions after careful consideration. Even in the regulatory fog and current market environment, BlackRock has chosen to double down on the digital asset industry. We believe this sends a signal to investors that cryptocurrencies are a legitimate asset class with a lasting future. Secondly, we believe ETFs will increase access and demand for the asset class faster than most expect. Recently, it was reported that a U.S. appeals court ruled in favor of Grayscale in its lawsuit against the SEC regarding the rejection of Grayscale's spot Bitcoin ETF application last year. We believe this significantly increases the chances of approval for Bitcoin ETF applications from companies like BlackRock and Fidelity, potentially as early as mid-October.

While the regulatory environment is starting to clarify, it may still be the biggest factor hindering the market, especially for the prices of long-tail tokens. In some respects, as courts begin to resist the SEC's "enforcement-heavy regulation," the situation seems to be shifting unfavorably for the SEC. In addition to the news about Grayscale's spot Bitcoin ETF, the court's support for Ripple in its case against the SEC is positive for interpreting digital assets as not being securities. This is a big deal because it suggests that regulation around digital assets can and should be more nuanced. Regulatory clarity is important not only for protecting consumers but also for entrepreneurs who need appropriate frameworks and guidance to confidently create new applications and drive innovation.

Finally, cryptocurrency is at what we call a "dial-up broadband moment." In previous letters, we mentioned that cryptocurrency is somewhat similar to the internet 20 years ago. Ethereum's scaling solutions (like Arbitrum or Optimism) are making significant progress, and we see transaction speeds improving at lower costs, along with increasing functionality. Just as we could not imagine the breadth of internet businesses created after the speed of the internet accelerated from dial-up to broadband, we believe the same will happen with cryptocurrency. In our view, we have yet to see the surge of new use cases that will come from significant improvements in blockchain infrastructure and speed.

Digital Ownership and Scarcity

Author: Matt Stephenson, Head of Crypto Economics

Digital scarcity is a powerful force. Facebook's initial explosive growth was driven by requiring users to register with an email address from "Harvard.edu," Amazon used digital rights management technology to sell e-books, and the iPhone dominated Generation Z because using green text messages was seen as shameful.

But this scarcity is essentially artificial: Apple can choose any color for text it wants. Harvard can issue any number of email addresses. And Amazon's e-books are not infinite.

True internet-native scarcity seems to have emerged with the advent of Bitcoin. Unlike the endless replication machines of the open internet, and unlike the centralized strategic decisions around Kindle e-book pricing, Bitcoin's supply is closer to natural scarcity. This is a fact about the world, encoded in shared code, and difficult to revoke.

Creating Minimal Viable Scarcity

In mathematical logic, there is a phrase (one that is sure to make you popular at dinner parties) that describes how blockchains create digital scarcity: "entity abstraction." Entity abstraction refers to the process of generating abstract properties from a process. For example, the way keratin coherently moves in space is considered a wool scarf.

Great strategist Thomas Schelling pointed out that enforcement and mutual perception can generate this abstract process. In the scarf example, physics provides the enforcement, while our shared visual system manages mutual perception. But Schelling provided numerous examples, the most notable being national borders. These borders are created through enforcement and mutual perception (via maps), often appearing real enough that it is not surprising for people to do things like travel to the "Four Corners," where the borders of four U.S. states meet at right angles, so they can "stand in four different states at once." These boundaries are enforced and mutually perceived, making them effectively real.

It is perhaps not surprising that blockchains use these same mutual perception and enforcement characteristics to create scarcity. The scarcity of your cryptocurrency is mutually perceived on an open digital ledger, and the rules governing its use are reliably enforced by the protocol. Thus, scarcity is real.

Digital Scarcity Gives Rise to Digital Ownership

How blockchains create mutual perception is quite intuitive: there is an open digital ledger. This is similar to Schelling's map example. Blockchains also promise enforcement, but note that this is often a special kind of enforcement: the enforcement of property rights.

The two pillars of property rights are exclusivity and transferability. That is, you can exclude others from the cryptocurrency you own, and you can "alienate" yourself from it by selling, transferring, or burning it. These two aspects of property rights stand out more than other conferred property rights. Also, note that in economics, these are not essentially legal concepts—they may simply arise from cooperative actions.

In the blockchain environment, these "cooperative actions" are non-legal agreement rules. These rules are largely maintained because they require massive coordination efforts (e.g., a 51% attack) to change.

Reversal of Web2 Business Models

The enforcement of scarcity on blockchains is credible because the cost of violating protocol rules in a blockchain environment is very high. This is a large-scale coordination problem, essentially the same large-scale coordination problem that Web2 uses against us. But as Vitalik Buterin described, the goal of crypto economics is to create and maintain "the security and vitality of complex systems of coordination and cooperation."

That is to say, Web2 business models use network defenses to lure users, while crypto uses them to solidify ideal rules. Web2 users wanting to exit a Web2 social media platform face a massive coordination problem because they must get all their friends to exit as well, preferably at the same time. Web3 users can simply fork the protocol because we have enabled that forking capability.

Utopians of the early internet believed that ignoring scarcity could create abundance. In the vacuum they left behind, predatory Web2 business models emerged, trying to lure users into a corral to show them ads. But it has been leveraging scarcity to create abundance. For the first time in the digital realm, we have it.

Risk warning

Risk warning Risk warning

Risk warning