Comparing from the perspective of token economic models and ecological development: Should we do Layer 1 or Layer 2?

This article further deepens the discussion on Cosmos, Polkadot, and Layer2 Stack solutions from the perspective of token economic models and ecological development, summarizing the points that projects need to consider when deciding whether to become Layer1 or Layer2.

This article further deepens the discussion on Cosmos, Polkadot, and Layer2 Stack solutions from the perspective of token economic models and ecological development, summarizing the points that projects need to consider when deciding whether to become Layer1 or Layer2.Written by: Gryphsis Academy

Introduction

In the first article of this series, after the preliminary 《Sorting out the technical solutions of Cosmos, Polkadot, and ETH L2s Stack》, we gained insights into the network architecture and core technologies of CP and Layer 2 Stacks solutions. Currently, CP's technology far exceeds that of Layer 2 Stacks, but what about the community and ecological conditions?

Next, this article will describe the respective token economic models and ecological development aspects. By sorting out the scenarios for token value capture and comparing various dimensions of each solution, we aim to help readers understand the potential development trends of each token and the strengths and weaknesses of the solutions.

I. Token Value

As CP and Layer 2 continue to develop cross-chain networks, what role will their ecological tokens play, or what additional possibilities does the development of cross-chain networks bring to these tokens?

To discuss the future development trends of tokens, this article first sorts out their respective token models and analyzes their similarities and differences; then it delves into the potential impacts that each solution may have on the tokens and explores the corresponding investment values. Now, let’s take a look at how their token economic models fully stimulate their potential.

1.1 Cosmos

In fact, if one can understand the Cosmos framework, it becomes clear that under its advocacy for sovereignty and freely customizable chains, the $ATOM token of Cosmos Hub has little demand in practical application scenarios, as each chain has its own native token, and $ATOM is not essential. However, at the Cosmos 2.0 conference, the team established the ATOM 2.0 plan, aimed at bringing additional utility and value to the $ATOM token.

1.1.1 Token Distribution

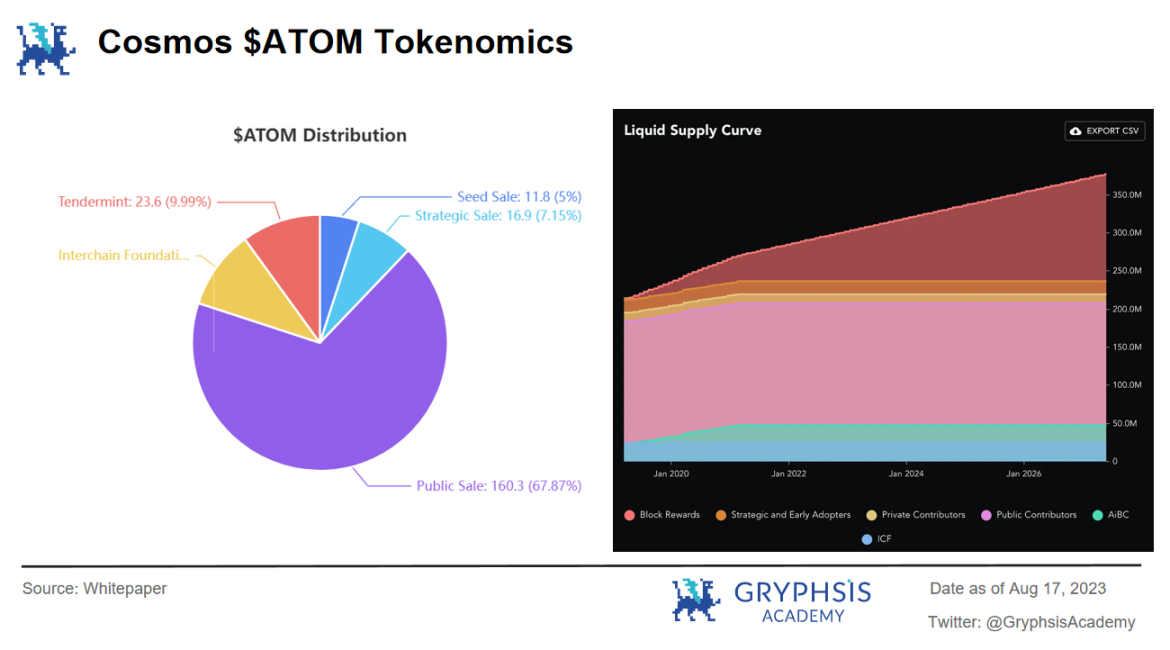

The supply of $ATOM is unlimited, with 290 million $ATOM currently issued in the market. Among them:

- Seed Sale: 11.8 million ATOM at $0.025 per token

- Strategic Sale: 16.9 million ATOM at $0.079 per token

- Public Sale: 160.3 million ATOM at $0.10 per token

- Interchain Foundation: 23.6 million ATOM

- Tendermint: 23.6 million ATOM

1.1.2 Token Value

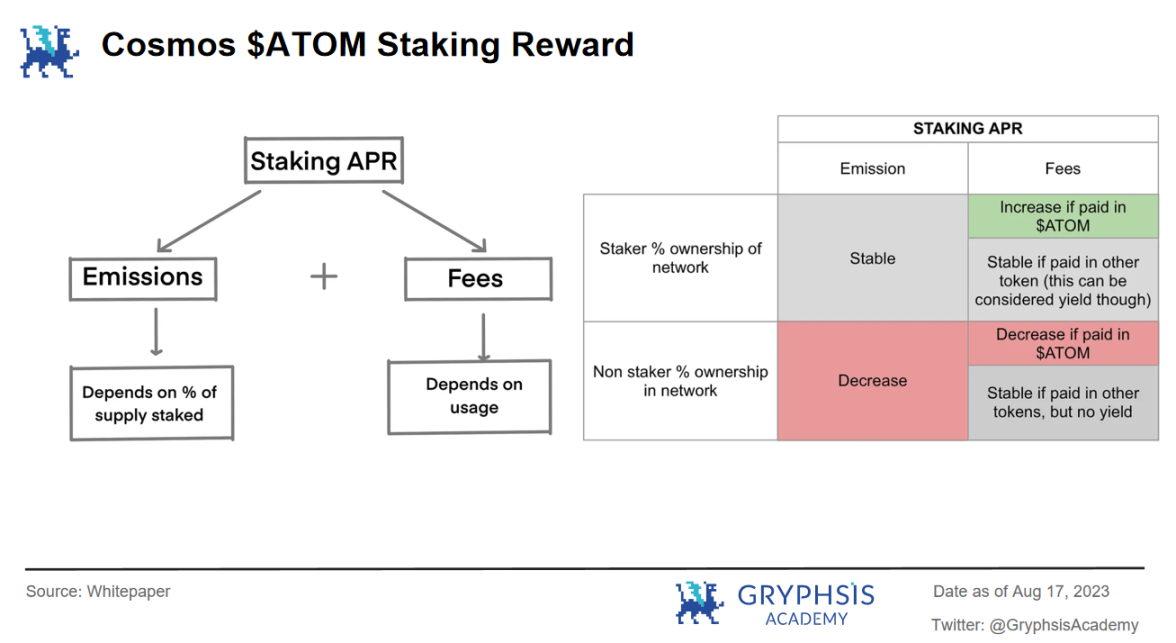

(1) Validators Staking

Since the Cosmos ecosystem consists of POS chains, the tokens staked by nodes reflect their contribution to the network. Cosmos has also established relevant measures for the Staking mechanism, mainly by adjusting the network staking rate and token inflation rate to coordinate together.

For stakers, Cosmos provides two types of rewards: Emission (block rewards) + Fee (network fees). When the network staking rate exceeds 66%, the system will reduce the inflation rate (to a minimum of 7%); when the network staking rate is below 66%, the system will increase the inflation rate (to a maximum of 20%). In summary, the system balances the network staking rate and the earnings of stakers through algorithms. Those users who do not stake will bear the losses brought by inflation, indirectly prompting them to participate in staking.

Why increase the staking rate? Because the economic security of Cosmos Hub depends on the amount of $ATOM staked; the more $ATOM is staked, the higher the cost of attacking the network. Therefore, the more $ATOM locked, the greater the economic security of the network.

(2) Validators Rewards

The rewards for validators mainly come from block rewards. Since it is a POS mechanism, the share of rewards received by validators is related to the amount of $ATOM they stake.

Here, a concept is introduced: Delegators, referring to those who hold $ATOM but do not have the ability or willingness to become validators, can delegate their tokens to chosen validators for staking. After receiving rewards, validators will return a portion of the rewards to the delegators based on their input ratio. Of course, validators can charge a commission from the income of the delegators.

Thus, the income of validators comes from: block rewards + delegator commissions.

(3) Transaction Fees

Interchain accounts have connected the entire Cosmos ecosystem, enhancing the use cases for $ATOM. As the native token of Cosmos Hub, $ATOM can serve as a relay chain to achieve seamless conversion of assets between different chains, facilitating direct trading of assets across different chains in the ecosystem and providing convenience for the interaction of various assets on different sovereign chains with $ATOM.

(4) Governance

Holders of $ATOM enjoy governance voting rights and can participate in the governance of Cosmos Hub, initiating proposals and voting on the future direction of the ecosystem. Additionally, $ATOM will be used in community management, providing one-time subsidies to the community or establishing developer funding flows and other incentive measures to better enable the community to provide suggestions for the Cosmos ecosystem.

The token mechanism of $ATOM encourages most users to choose staking, which increases the security of the network to a certain extent and prevents attacks. However, this also leads to low liquidity of the token, making it difficult to circulate within the ecosystem, especially affecting its positive role in the ecosystem's DeFi products.

However, it is worth noting that dydx has chosen to deploy on Cosmos, and Cosmos now supports the native USDC of CCTP. Additionally, in a recent community proposal, a solution for liquid staking of $ATOM was added, granting staked $ATOM the same liquidity as spot $ATOM. These updates and optimizations undoubtedly provide more demand scenarios for its tokens, and it is believed that the future development of $ATOM will be better than the present.

1.2 Polkadot

1.2.1 Token Distribution

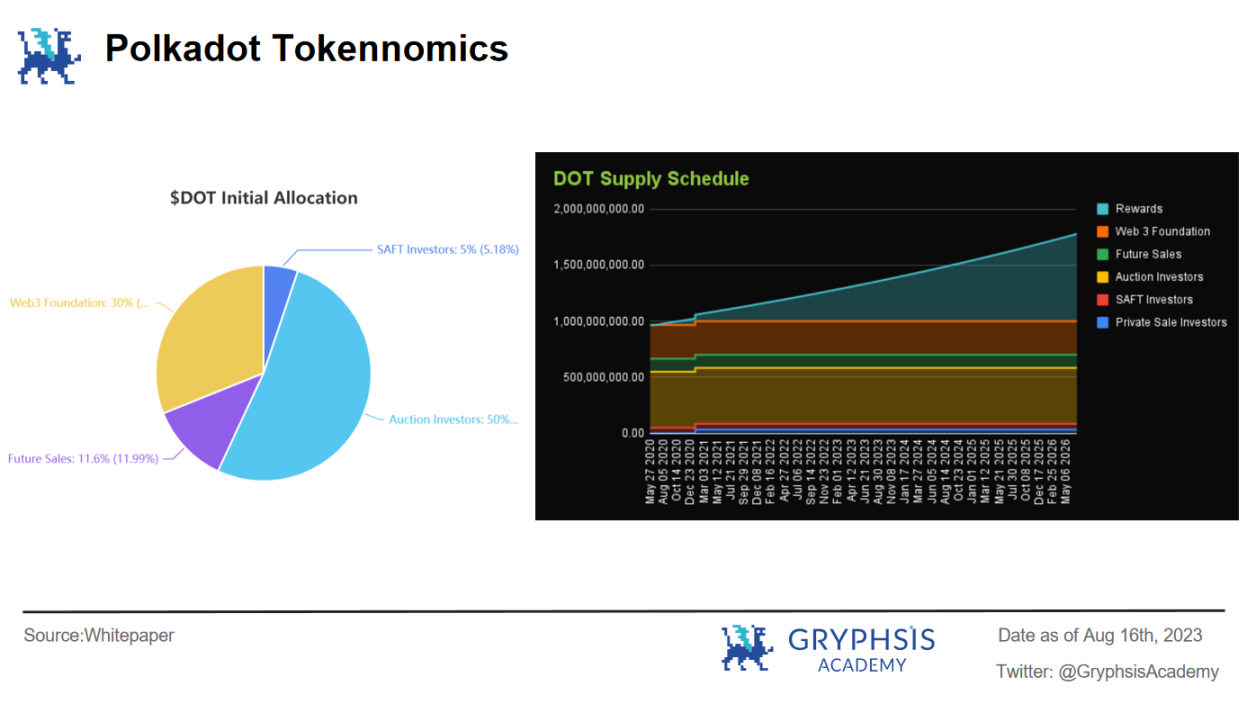

Polkadot's token $DOT has no supply cap, and its token distribution is as follows:

- 3.42% Private Investors

- 5.00% SAFT Investors

- 50.00% Auction Investors

- 11.58% Future Sales

- 30.00% Web 3 Foundation

1.2.2 Token Value

(1) Validators Staking

To become a Validator, one must first stake a certain amount of $DOT. Since the Polkadot network uses the NPoS (Nominated Proof of Stake) consensus mechanism, similar to Cosmos, the staking of validators helps maintain the security and decentralization of the network.

In the Polkadot network, there are three types of validators: Parachain Validators; Relaychain Validators; Other Validators. Each type of validator plays a role as follows:

- Parachain Validators validate the state of their own chain and submit candidate receipts to Polkadot's relay chain for adding more blocks.

- Relaychain Validators participate in the consensus of the relay chain to review the validity claims from other Polkadot validators, allowing blocks to be added.

- Other Validators collectively form a distributed network validation, acting as a dual validation process to ensure the correct allocation of validators for higher throughput and lower latency.

(2) Validators Rewards

In Polkadot, validators earn corresponding Era Points through block production or other activities during an era, and rewards are allocated based on these points.

Rewards are sent at the end of each era, but considering the scores obtained by all validators in the current era and the inflation model of $DOT, the specific amount is unclear.

In addition, there is a Nominator role, which can be understood as the Delegator in Cosmos. These tokens can only nominate their $DOT to validators to earn rewards, and both parties can share a portion of the earnings.

(3) Transaction Fees

Polkadot has introduced a "Weight-Based Fee Model," considering the limited block resources, and has established a series of standards for the overall fee model.

For example, each relay chain must efficiently process transactions to prevent block congestion; each block must reserve space for high-priority transactions that are poorly processed; and fee changes must be slow to prevent traders from accurately predicting fees, etc.

(4) Governance

Polkadot launched a new governance scheme this year. Let's first understand Gov1 and PolkadotOpenGov (the new scheme) and the differences and improvements between the two.

In the traditional Gov1, the roles involved in governance include:

- Council: Executes governance, responsible for managing parameters, proposals, etc.

- Technical Committee: Manages upgrade schedules, etc.

- Holders: $DOT holders who participate in public voting.

In the newly issued governance scheme, the roles involved in governance include: holders and technical associations (Fellowship). Compared to the original governance scheme, the new scheme is more decentralized, and the relationship between Polkadot's governance and holders has become stronger.

a. Network Governance

In the Gov1 version, to make any changes to the network, the idea was to form a management team consisting of active token holders and the council to manage network upgrade decisions. Whether the proposal is initiated by the public (token holders) or by the council, it must ultimately go through a public vote, allowing all holders to make decisions weighted by their stakes.

For proposal elections, each proposal has the same weight, and holders can only vote on one proposal at a time (except for urgent proposals), with the voting period potentially lasting several weeks. Additionally, Gov1 supports alternating voting schedules, allowing voting every 28 days. However, in the new upgraded version OpenGov, the voting mechanism has changed, allowing for a broader and more flexible range of proposal voting.

- Transfers all responsibilities of the council to the public through a direct democratic voting system.

- Dissolves the council.

- Allows users to delegate voting rights to community members in more ways.

- Dissolves the technical committee and establishes the Polkadot Technical Fellowship.

- Eliminates the centralized council, achieving truly decentralized governance.

b. Treasury Mechanism

The treasury, as the name suggests, is the public finance department of Polkadot's network governance. When a proposal is approved, a portion of the funds will be allocated to implement that proposal for better network development.

The main sources of income for the treasury are:

- Transaction fees: 80% of transaction fee income is submitted to the treasury, 20% goes to validators.

- Staking rewards: Polkadot generates an ideal staking rate. When the actual staking rate of the network does not reach the ideal staking rate, the APY returns for stakers will decrease. To keep the inflation rate at 10%, the system does not reduce the number of tokens but transfers a portion of investors' total returns to the treasury. (Polkadot regularly burns a portion of the funds in the treasury, so the actual inflation rate is less than 10%.)

- Validators: When the number of validators or proposers decreases, a portion of their tokens will be transferred to the treasury.

- Transfers: Anyone can donate to the treasury, but generally, the recipient will return the funds they received for some reason.

Treasury funds are stored in accounts that no one can access, and when a proposal is accepted, it enters a waiting period for distribution. This is because if funds are immediately allocated for funding, there may be a need to retain at least 5% of the proposal expenditure as a deposit. If the proposal is rejected, this deposit will be partially deducted; if accepted, the deposit will be returned.

Proposals may include (but are not limited to): infrastructure deployment and ongoing operations, network security operations (monitoring services, continuous audits), ecosystem regulations (cooperation), marketing activities (advertising, paid features, partnerships), community activities and outreach (meetups, pizza parties, hackathons)…

Now, managing the treasury through OpenGov, how the funds are used depends on public voting.

c. Slot Auctions & Core Time

Parachains need to lock $DOT to obtain slots, which remain locked during the rental period, and will be automatically returned after the parachain exits. Additionally, users holding $DOT have the right to vote and govern the parachains, and can even directly allow a parachain to run on the network for free.

The original slot mechanism was not very flexible, as it was designed for long-term single chains. Although the parachain threads alleviated liquidity, teams focused on technology may need to raise funds for marketing, obtain $DOT, and then lock it to participate in this ecological network.

However, Polkadot recently proposed version 2.0, which may eliminate the slot auction mechanism and adopt a Core Time allocation method.

The mechanism of Core Time differs significantly from the current slot auction in that slot auctions lock $DOT for a period; whereas Core Time involves paying $DOT to purchase time, and $DOT will not be unlocked and returned.

Currently, this sale mechanism is divided into two types: bulk purchase & instant purchase.

- Bulk Purchase: Conducted once a month, selling 4 weeks of core time at a fixed price, non-fungible assets.

- Instant Purchase: Similar to the pay-as-you-go model of parachain threads, purchasing when there is a demand for use.

Polkadot's token governance mechanism is very well-developed and has updated the auction mechanism for parachain slots. Abandoning the staking unlock mechanism and adopting a purchase mechanism brings new value capture to $DOT. As more and more projects choose to deploy on Polkadot, the importance of $DOT will undoubtedly become more prominent.

1.3 Optimism

1.3.1 Token Distribution

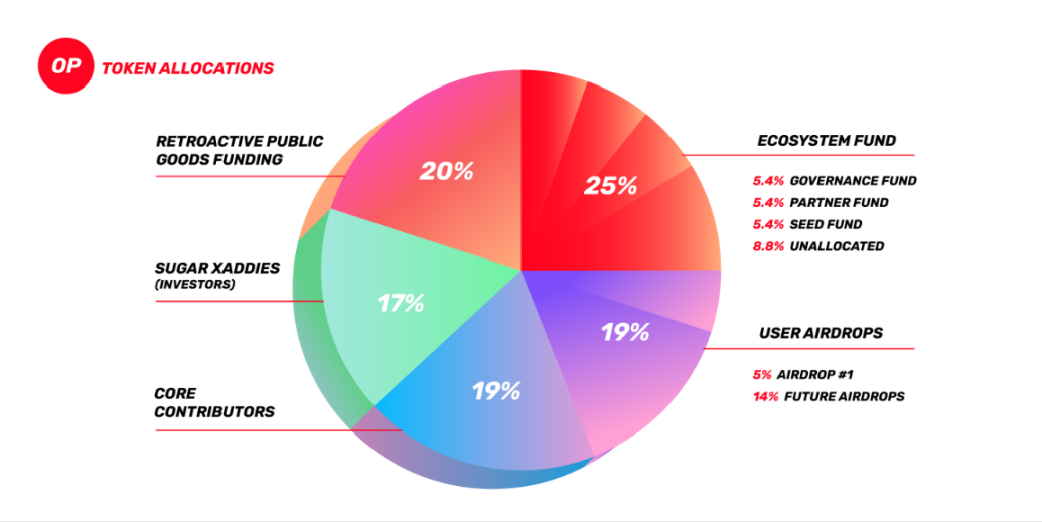

The initial supply of $OP is 4.3 billion, roughly distributed as follows:

- 25% Ecosystem Fund

- 19% Airdrop Users

- 19% Core Contributors

- 17% Investors

- 20% RPGF (Retroactive Public Goods Fund)

Source: Whitepaper

1.3.2 Token Value

Currently, there is no clear definition of the demand scenarios for $OP in the cross-chain network, but the OP Stack will be governed uniformly by the OP Collective.

In simple terms, it adopts a Two-House System governance structure, including the Token House and Citizens' House, with mutual checks and balances to avoid excessive concentration of governance power.

The Token House is composed of OP holders, responsible for deciding business parameters. However, if token holders can fully decide business matters, it is likely to tilt the system's economy in their favor, which may not be friendly to other stakeholders. The Citizens' House adopts a one-person-one-vote mechanism, responsible for long-term value judgments. Different types of decisions supervise each other, providing a broader perspective for evaluation. Optimism hopes to establish a governance system that can withstand the test of time through this new iteration of the model, helping collective prosperity and development.

Recently, Base and OP launched an economic cooperation agreement, with Base providing OP two revenue models (whichever is higher), one being a 2.5% sequencer fee or a 15% profit; while OP will give Base 2.75% of $OP (specific details will be elaborated in the third article).

OP has already begun its experimental revenue distribution plan, and based on market capitalization, OP is actually profiting from this cooperation. In previous L2s, the main source of income relied on transaction-generated Gas fees (L2 gas + L1 gas), while OP has pioneered a new rental model. As Base, which uses the OP Stack solution, needs to pay for the profits it obtains, this is undoubtedly a positive development for OP.

However, how should the revenue from this model be returned to $OP token holders? Currently, it can be confirmed that ecological governance rights will be provided, and how future application scenarios will unfold is crucial for OP, which currently ranks first in the L2 Stack.

1.4 Arbitrum

1.4.1 Token Distribution

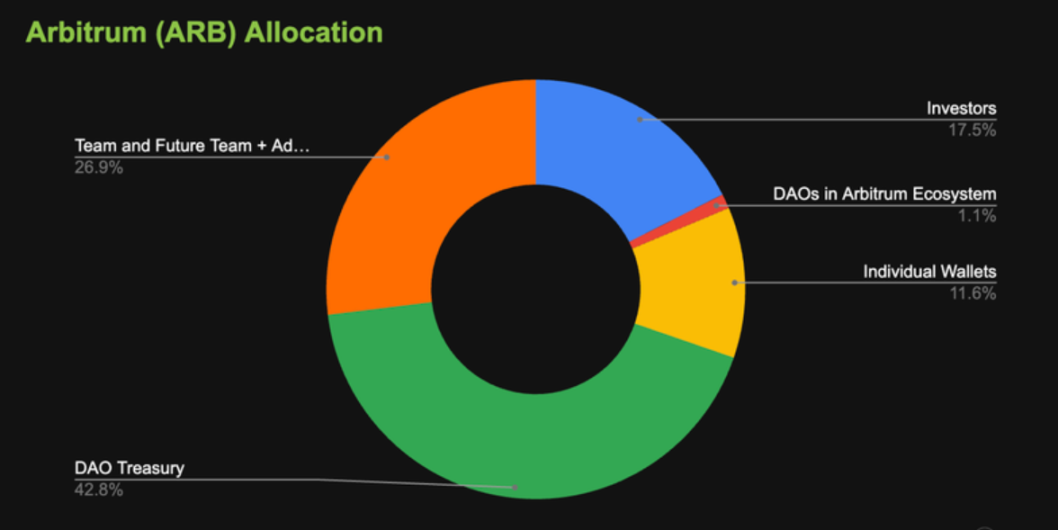

$ARB was first issued on March 23, 2023, with a total supply of 10 billion and a current circulating supply of 1.2 billion.

- 17.53% Investors

- 1.13% Arbitrum DAOs

- 11.62% Individual Wallets

- 42.78% DAO Treasury

- 26.94% Team and Advisors

Source: CoinGecko

1.4.2 Token Value

Currently, the official has not released specific demand scenarios for $ARB in the cross-chain network, but it is certain that regardless of whether the cross-chains have issued native tokens and management mechanisms, Arbitrum DAO will use $ARB to fully manage all cross-chain networks and community and technical updates.

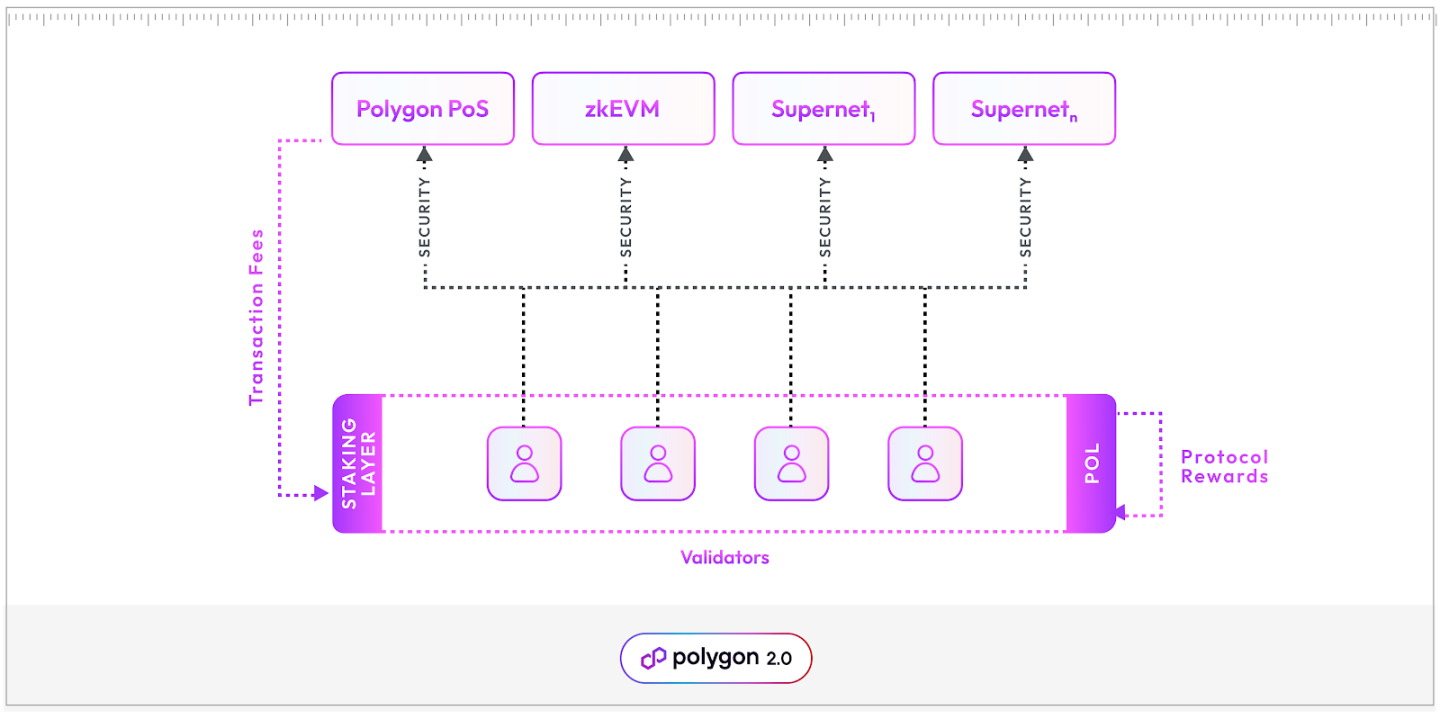

1.5 Polygon 2.0

Polygon issued its token economic white paper for the Polygon 2.0 cross-chain network in July this year, hoping to govern the network through the issuance of $POL.

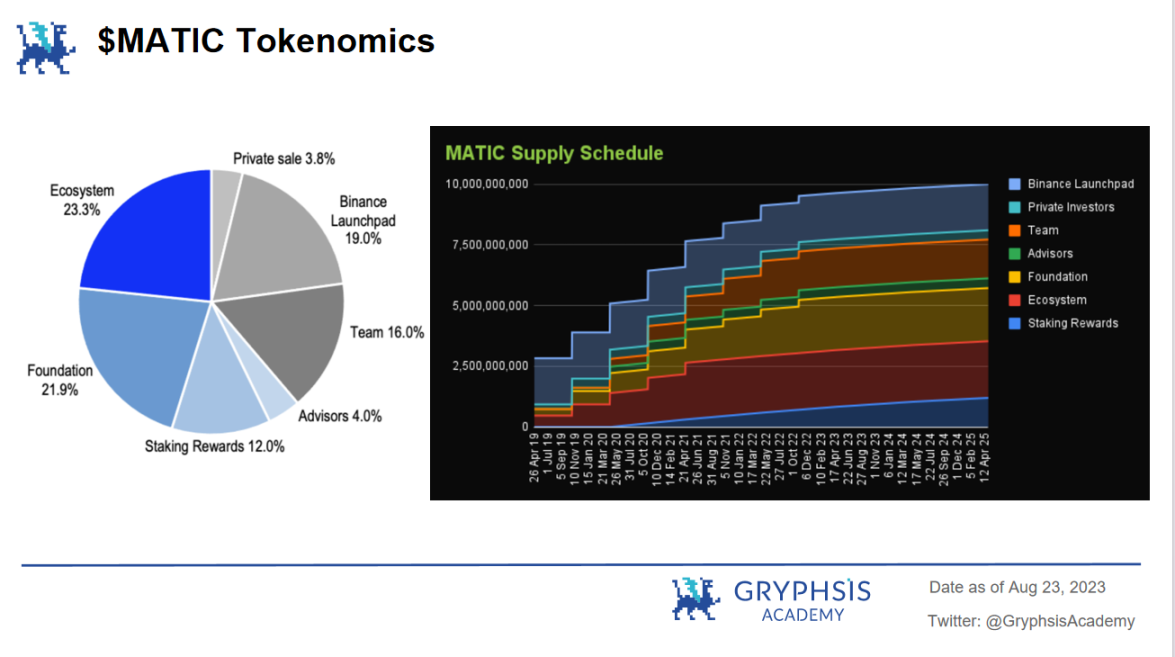

Essentially, $POL is an upgrade and renaming of $MATIC, with a 1:1 exchange rate, and the two will not coexist; $POL will completely replace $MATIC in the future. Therefore, we will temporarily use the token distribution model of $MATIC to replace $POL.

1.5.1 Token Distribution

- 12.00% Staking Rewards

- 23.33% Ecosystem Community

- 21.86% Foundation

- 4.00% Advisors

- 16.00% Team

- 3.80% Private Investors

- 19.00% Binance Launchpad

1.5.2 Token Value

(1) Validators Staking

As a POS chain, to become a Validator in Polygon 2.0, one must stake $POL tokens. Once staked, they can join the validator pool and be eligible to validate any Polygon chain.

(2) Validators Rewards

To incentivize Validators, the Polygon network provides rewards for validators, which are mainly divided into three parts:

- Protocol Rewards: The protocol continuously sends $POL to the validator pool as a base reward, distributed based on the proportion of validators' staked shares.

- Transaction Fees: Validators can freely validate any number of chains, so they can collect transaction fees from these chains. Notably, Polygon allows each chain to decide which token to use for Gas payments, not mandating the use of $POL, hence the transaction fees received by validators vary.

- Additional Rewards: To attract more validators, some Polygon chains may choose to introduce additional rewards, not limited to token types, as an incentive.

(3) Governance

Owning $POL tokens grants governance rights, although specific details have not yet been listed in the white paper.

Source: Polygon Whitepaper

Polygon 2.0 allows each cross-chain to use its own tokens as transaction fees, which is a very key and special move. It fully respects the native autonomy of each cross-chain, but to some extent, it also cuts off an important source of token capture.

Currently, all Layer 2 Gas Fees are settled in ETH. If Polygon 2.0 gives up this source of income, how will it attract token holders? Even with governance rights, will it be able to provide additional benefits to holders?

The author believes that based on the current disclosed token uses, the incentives for holders may not be as rich compared to CP, but this does not rule out updates to its development strategy in the future.

II. Ecological Comparison

2.1 Cosmos & Polkadot

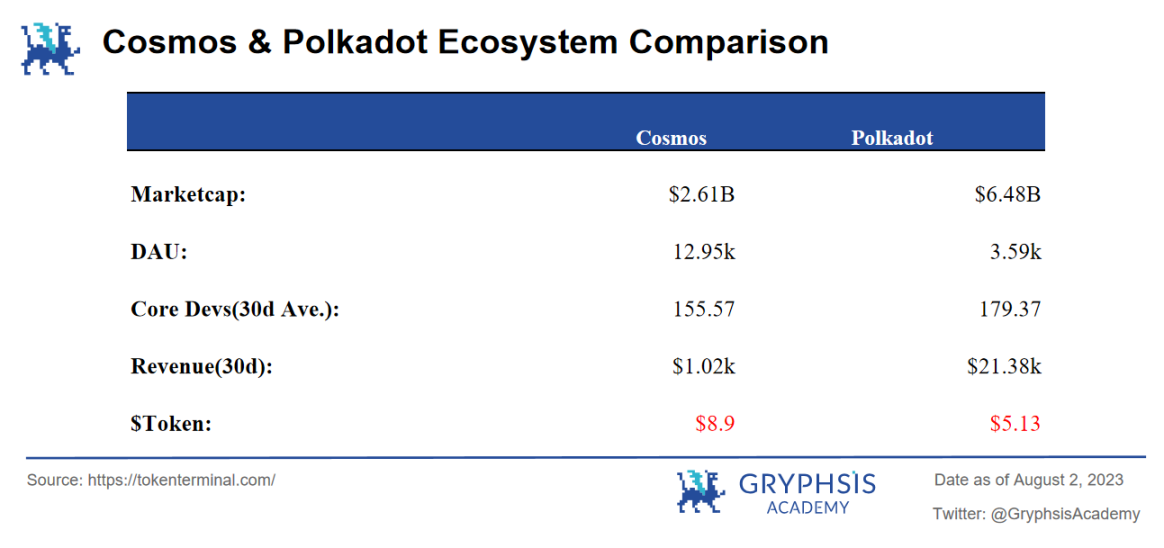

1) Ecological Data

From the chart, it can be seen that Polkadot's market value is about three times that of Cosmos, but the Cosmos ecosystem has higher stickiness, with 12.95K daily active users; the core developers of both are roughly similar, but Polkadot's network revenue is far higher than that of Cosmos.

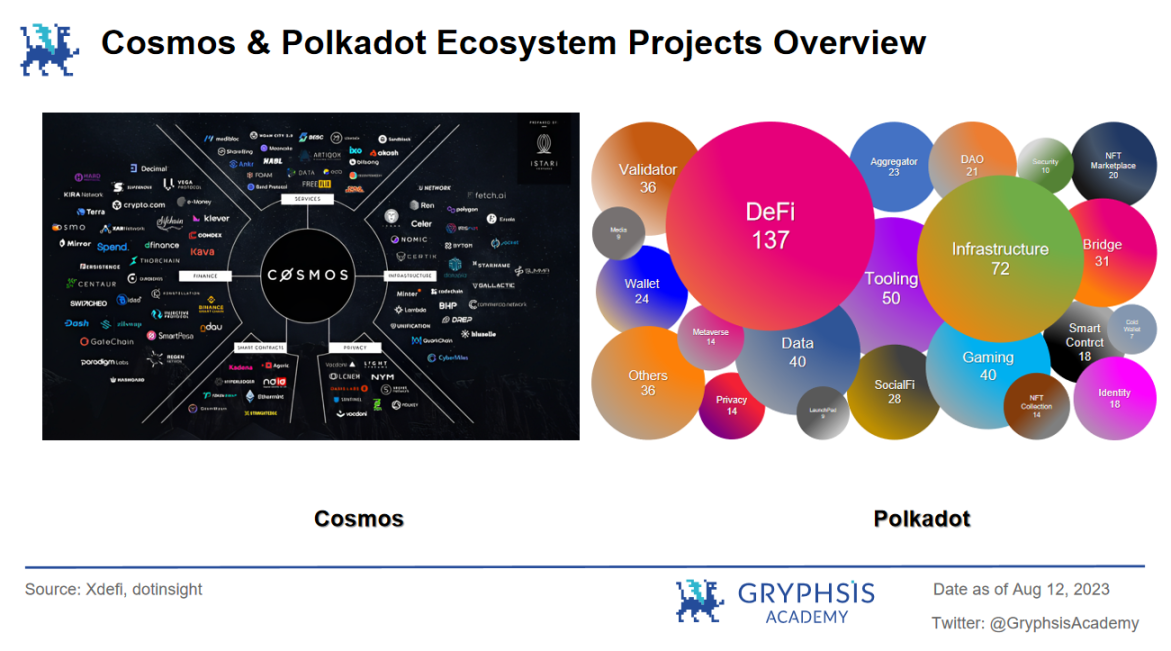

2) Ecological Projects:

From the distribution of ecological projects between the two, it can be seen that:

In Cosmos, besides the well-known Sei network, financial projects account for a high proportion and cover a wide range, including decentralized exchanges (DEX), lending, and stablecoins. For example, the derivatives exchange dydx, DEX like Osmosis, and the Kava lending platform. Additionally, the stablecoin Terra is also among them, but after the collapse of UST, Cosmos's stablecoins have not had particularly outstanding projects.

However, it is worth noting that CCTP USDC has been successfully deployed in Cosmos, greatly solving the liquidity problem of Cosmos and accelerating the development of the ecological community.

On the other hand, Polkadot's ecological projects are mainly concentrated in infrastructure projects, such as network and blockchain development tools. Notable projects include Acala Network and Moonbeam, an EVM-compatible smart contract platform… Polkadot's Substrate framework makes it easier for developers to create their own independent consensus blockchains, thus attracting more infrastructure projects.

In summary, from the distribution of ecological projects, the Cosmos ecosystem mainly focuses on financial projects, while the Polkadot ecosystem has more infrastructure projects, resulting in slightly stronger ecological diversity. The different characteristics of the development tools, Cosmos SDK and Substrate framework, have attracted different projects, leading to the current situation.

3) Version 2.0 Updates

Both CP have released their respective 2.0 versions, comprehensively optimizing ecological governance and token empowerment.

In Cosmos 2.0, most of the new mechanisms introduced focus on how to redistribute $ATOM. This includes interchain schedulers, interchain allocators, interchain security, and liquid staking, among others, deeply integrating $ATOM into these aspects. Specifically, this is manifested as:

Liquid staking chains join Hub consumption chains, obtaining $stATOM and $qATOM by staking $ATOM, which can be used for trading and other interchain activities; modifying the $ATOM issuance policy to reduce the issuance amount over a 36-month period. After 36 months, a portion of the transaction fees generated by Hub consumption chains will be redistributed to stakers, nodes, and community pools. The issuance of $ATOM, interchain schedulers, and interchain allocators will distribute profits to the treasury to support ecological growth and the development of $ATOM as a public asset.

Additionally, the latest community proposal of Cosmos Hub will optimize the liquid staking model (LSM) for $ATOM on September 13, allowing staked $ATOM to enjoy the same liquidity as spot $ATOM. This move allows the originally high staking rate of 68% for $ATOM to be released into DeFi scenarios, accelerating the overall development of the ecosystem. Furthermore, additional limits on liquid staking, validator guarantees for staking, and immediate liquid staking management measures have been added.

In Polkadot 2.0, the mechanism for parachain slot auctions has been modified to Core Time, thereby lowering the entry threshold and optimizing flexibility. Through bulk purchases and instant purchases, it can circulate in primary and secondary markets, no longer providing the original slot auction's unlocking of $DOT, optimizing the liquidity of $DOT.

Moreover, in 2.0, Polkadot aims to shift from the previous relay chain-centric paradigm, where users might want to use an application on chain A and also want to use that application on chain B, thus involving seamless cross-chain deployment of applications. For this cross-chain deployment paradigm, Polkadot has developed the XCM cross-chain communication protocol, a descriptive language framework that helps describe what you want to do, but it is difficult to ensure that the recipient will faithfully translate this information. Therefore, the Accord protocol was created to ensure behavioral fidelity. Additionally, Polkadot is also creating other mechanisms such as Hermit Relay, Project CAPI, etc., to help the relay chain free up space and transfer functional application layers to parachains.

Overall, Cosmos 2.0 mainly focuses on interchain scheduling and allocation to redistribute the value of $ATOM, while Polkadot 2.0 primarily modifies the use cases of $DOT, adds new empowerment methods, and aims to create cross-chain applications to achieve a fully decentralized cross-chain network.

2.2 L2s Comparison

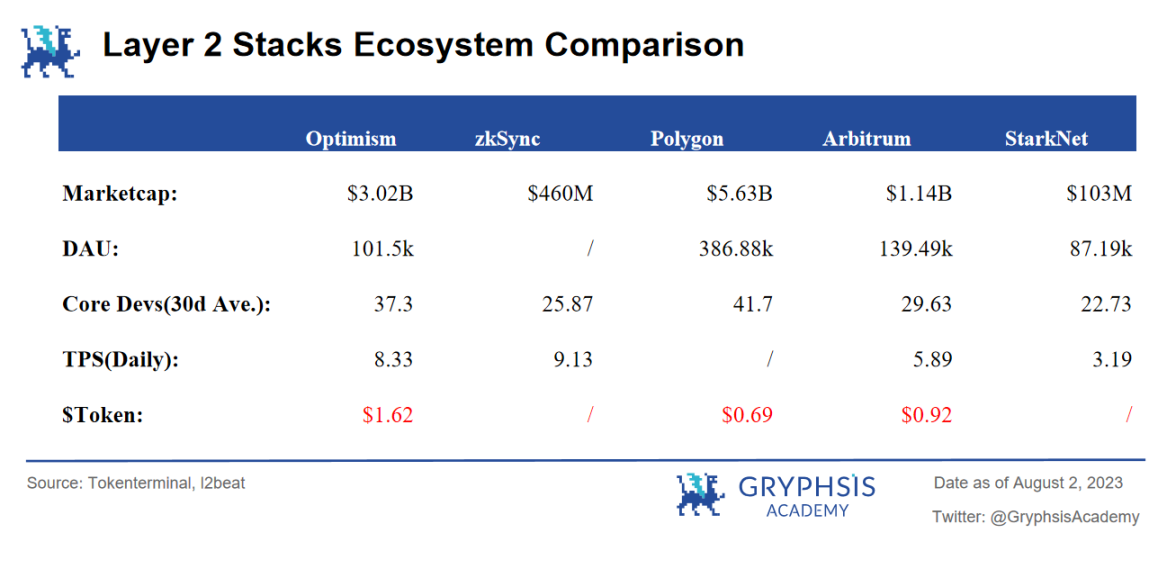

1) Development Status:

From the chart, it can be seen that Polygon has the highest market value, daily active users, and core developers; zkSync has the highest TPS; excluding Starknet and zkSync, which have not issued tokens, $OP currently has the highest price.

2) Ecological Resources

Recalling the public chain battle of 2021, Solana gained recognition from SBF due to its innovative PoH (Proof of History) technology, with FTX backing the creation of its own DEX, and its backer Multichain leveraging its resources to help Solana expand its ecosystem, leading to a surge in $SOL prices; BSC was endorsed by the top exchange Binance, hosting multiple hackathons to produce top DEXs, quickly importing Binance's traffic; Avalanche created the Avalanche consensus to enhance chain performance, receiving investments from top funds like A16Z, Polychain, and Three Arrows Capital, with TVL skyrocketing tenfold in half a month…

If L2s want to grow their networks, they must focus on three levels: developers - projects - users, and behind this, ecological resources are extremely important. If there is strong support from top exchanges/VCs, it will attract more developers and projects, thereby attracting more users and forming a positive cycle. So do these L2s that have launched Stack solutions have their core ecological resource barriers?

Polygon ($450 million):

- The founding team comes from Matic Network, with core members from well-known companies like PayPal, Google, 0x, and Coinbase.

- Completed several rounds of financing, with investors including Coinbase Ventures, Binance Labs, Mark Cuban, and received support from the Ethereum Foundation's ETH and Financial Grants, as well as support from the Polkadot Ecological Foundation.

- Actively collaborates with traditional web3 industry leaders, such as joining Disney's accelerator program, working with Meta to develop NFTs for Instagram, and releasing NFTs on the Polygon chain with well-known brands like Adidas and Prada, possessing a large number of web2 company membership NFTs, becoming a leader in the web3 industry.

Optimism ($179 million):

- Initially developed by the Plasma Group, with core member Karl Floersch also being one of the founding team members of Uniswap, closely related to Ethereum.

- Completed seed and Series A financing, with investors including Coinbase Ventures, Binance Labs, Paradigm, and received support from the Ethereum Foundation.

- Synthetix, a well-known synthetic asset DeFi, was one of the earliest supporters of Optimistic Rollup.

zkSync & Matter Labs ($258 million):

- zkSync was founded by the Matter Labs team, with core members from top universities and research institutions like Stanford, MIT, and the Technion, boasting strong technical capabilities.

- Completed multiple rounds of financing, with investors including Coinbase Ventures, Paradigm, Framework Ventures, and Three Arrows Capital, and received multiple development and research grants from the Ethereum Foundation.

Arbitrum ($140 million):

- The founding team of Arbitrum, Offchain Labs, consists of technical experts including Princeton University professor Ed Felten.

- Completed multiple rounds of financing, with investors including Pantera Capital, Coinbase Ventures, Ribbit Capital, and Naspers Ventures.

- Has deployed multiple top projects, such as Reddit, dydx, and Chainlink, with its most important perpetual trading platform GMX adding significant value to its ecosystem.

Starknet (No financing, Starkware $261 million):

- Starkware, as the core R&D team of Starknet, consists of several cryptography and blockchain experts.

- The Starkware team has received multiple research and development grants from the Ethereum Foundation.

- Starknet has partnered with companies like Nvidia to enhance computing speed using GPUs; it has also collaborated with other well-known companies to explore applications in supply chain finance.

It can be seen that among these L2s, Polygon has the strongest financial strength; the Optimism team has a close relationship with the Ethereum team, with higher community recognition; zkSync, as the first team to use zk technology, pioneered ZK Rollup; Arbitrum, although having the least financing, occupies half of the L2 TVL and has many out-of-the-box projects; Starknet takes a different approach, based on ZK Rollup for scalability solutions, but utilizes the native StarkEx mechanism to achieve parallel computing Rollup.

III. To Be Layer 1 or Layer 2?

Cosmos and Polkadot have continuously improved and developed their ecosystems over the past few years, successively launching version 2.0. So, in the face of the development of L2s, can their 2.0 versions maintain some characteristics to keep their advantages from being overly affected?

The 2.0 versions of Cosmos and Polkadot have optimized aspects such as consensus mechanisms, cross-chain interoperability, and token value distribution. It can be said that compared to L2s, CP has more mature experience in creating cross-chain networks. Currently, the market value of CP is nearly 10 billion, and L2s need to invest more effort to surpass them. However, since L2s rely on Ethereum, Ethereum's strong consensus and large community will also help the development of L2 Stack.

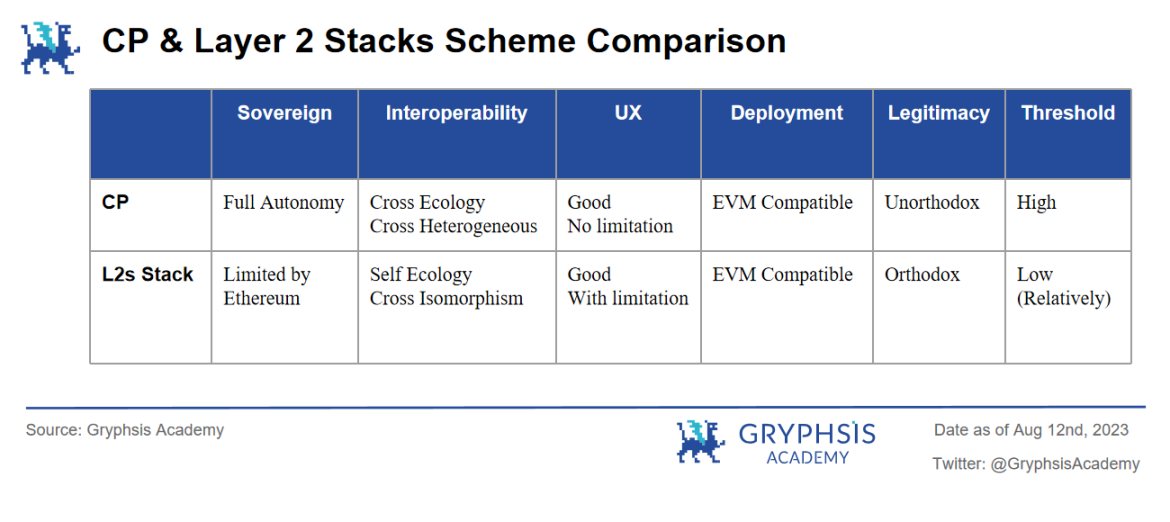

Here, we roughly summarize the characteristics that CP and L2s will attract projects to deploy:

- Sovereignty: CP allows application chains to choose validators, issue tokens, govern themselves, and enjoy complete autonomy. Although L2s Stack allows developers to modify stack modules and customize their chains, it does not grant them the right to self-govern. The consensus of transactions ultimately relies on Ethereum and other L1s, with governance completely controlled by L2. Therefore, for those needing highly customized public chains or application chains and wanting control over parameters and governance, CP is the preferred choice.

For example, recently the founder of dydx chose to deploy the V4 version on Cosmos. He believes that Ethereum-based L2 has several issues: performance is not strong enough; Ethereum L2 currently operates through centralized sequencers, which have the ability to censor and block transactions. Although it is possible to bypass the sequencer to access L1 directly to avoid censorship, Ethereum L1 is too slow and expensive to meet the needs of dydx's core products.

Thus, even though Ethereum currently appears more decentralized, its L2's least decentralized component, the sequencer, cannot meet application needs, leading to the choice of Cosmos.

- Cross-chain Interoperability: CP supports communication and asset transfer between heterogeneous chains, not limited to its own ecosystem but also compatible with the Ethereum ecosystem. For instance, the Cosmos ecosystem currently relies on Axelar Network and Gravity Bridge to bridge assets from the ETH ecosystem, with security relying on third-party bridges, hence the lower TVL. Although cross-EVM bridge compatibility is currently not ideal, it still offers broader cross-chain possibilities.

Projects can achieve communication with other public chains like Ethereum and even L2s cross-chains on CP. In contrast, the interoperability protocols of L2s are somewhat singular, relying solely on shared cross-chain bridges to achieve internal ecosystem communication, unable to interact with other non-EVM public chains. Therefore, for those requiring full-chain interaction platforms, they may lean more towards CP.

- User Experience: As an independent blockchain, CP is not limited by Ethereum, achieving higher throughput and transaction speeds through communication protocols; while L2s, although using Rollup technology to transfer most transaction processing work to their chains, will still have their ultimate security and consensus limited by Ethereum. If a project seeks transaction speed and user experience, it can choose to deploy on CP; for those needing a large amount of off-chain storage space and processing transactions off-chain, choosing L2s would be more convenient, as CP chains have limited space.

- Deployment Difficulty: Currently, both CP and L2s are compatible with Ethereum EVM, but relatively speaking, L2s may have more mature compatibility than CP. L2s have already taken on Ethereum's rich Dapps, guiding these projects to migrate and deploy, making the deployment difficulty and willingness to do so easier than on CP.

- Legitimacy: Relating to deployment difficulty, in terms of deployment willingness and community consensus, users have a higher recognition of Ethereum. Therefore, for projects that have developed within the Ethereum ecosystem, it is difficult for CP to attract them to join the ecosystem. Thus, for those needing to quickly utilize various tools and protocols on Ethereum, deploying on L2 can provide the richest ecological resources and is also very secure.

- Entry Threshold: If nodes want to deploy on CP, they need to stake $ATOM / collateralize $DOT to auction slots, which has a higher screening threshold. In contrast, L2s like Optimism only require collateralization of a certain amount of ETH, and zkSync has no special requirements; anyone with certain technical capabilities can become a node. Therefore, Ethereum L2s have a lower threshold compared to CP, making it easier for nodes to deploy.

Overall, Cosmos and Polkadot have advantages in interoperability, performance, scalability, and governance, but Ethereum's Layer 2 has higher security and a more mature ecosystem.

Conclusion

This article further deepens the discussion on CP and Layer 2 Stack solutions from the perspectives of token economic models and ecological development, summarizing the points that projects need to consider when becoming Layer 1 or Layer 2. We analyzed the role of ecological tokens in the network as CP and Layer 2 develop, and how the development of cross-chain networks brings more possibilities for these tokens. These analyses provide strong evidence for understanding the long-term impacts and values of these technical solutions.

Although these L2s each have corresponding resources, how to utilize these resources effectively to build their ecosystems raises a new question: How will L2s develop their cross-chain networks? We will elaborate on this in Series 3.

References: https://medium.com/@eternal1997L https://medium.com/polkadot-network/a-brief-summary-of-everything-substrate-and-polkadot-f1f21071499d https://tokeneconomy.co/the-state-of-crypto-interoperability-explained-in-pictures-654cfe4cc167 https://research.web3.foundation/Polkadot/overview https://foresightnews.pro/article/detail/16271 https://v1.cosmos.network/ https://polkadot.network/ https://messari.io/report/ibc-outside-of-cosmos-the-transport-layer?referrer=all-research https://stack.optimism.io/docs/understand/explainer/#glossary https://www.techflowpost.com/article/detail_12231.html https://gov.optimism.io/t/retroactive-delegate-rewards-season-3/5871 https://wiki.polygon.technology/docs/supernets/get-started/what-are-supernets/ https://polygon.technology/blog/introducing-polygon-2-0-the-value-layer-of-the-internet https://era.zksync.io/docs/reference/concepts/hyperscaling.html#what-are-hyperchains https://medium.com/offchainlabs

Risk warning Risk warning

Risk warning Risk warning