Interpreting the intent-centered landing challenges from UniSwapX and AA

Intent-centric protocols and infrastructure are seen as a new engine for facilitating the adoption of Web3.

Intent-centric protocols and infrastructure are seen as a new engine for facilitating the adoption of Web3.Written by: Shisi Jun

Recently, in the article "Intent-Based Architectures and Their Risks" by the well-known Web3 venture capital firm Paradigm, "intent-centric protocols and infrastructure" ranked first among ten trends in the crypto space. This, combined with the years of exploration and accumulation of the Bob the Solver project and Anomo, DappOs at the ETHCC conference in Paris, has sparked significant industry attention on intent-centric architecture and this track. Its core goal is to greatly enhance user experience by completely obscuring the complex transaction details, thus being seen as a new engine for the widespread adoption of Web3.

In this Token2049 hackathon, I collaborated with the AstroX wallet technology team (which focuses on high ROI growth products for B2B services) to realize the second-place project in the DeFi track based on the intent concept: Ethtent. This article will discuss the journey of implementing the Solver and the applications of ERC4337 and UniSwapX in the context of intent-centric architecture.

What is "intent"? Can it be so beautiful? What are its applications? What are the challenges in implementation?

1. Review of What Intent-Centric Is

Just as the concept of account abstraction predates the development of Ethereum itself, the specific idea of "intent" can actually be traced back to the Wyvern Protocol's introduction of its design philosophy in 2018. The core point of this philosophy is that, unlike traditional trading, what ordinary users have always pursued is the consistency and accuracy of results, rather than the meticulousness of the execution process.

Assuming a scenario where I want to complete a swap of a certain token:

- In traditional trading: I need to perform three transactions: transfer ETH as gas, give approval for the transaction, and then submit the swap transaction.

- In intent trading: The user only needs to sign, stating that they are willing to swap X tokens for Y tokens as quickly and as much as possible, with a 1% fee.

We can understand intent-centric protocols as a set of signed contracts that allow users to outsource the transaction process to third parties without relinquishing complete control over the transaction.

Users only need to clarify their intent of what they want to do; one signature can complete all operations.

In comparison to the development history of the traditional internet, it has undergone a similar evolution, shifting from what service providers sell to what users need, and then to intelligent service platforms. Looking back over 20 years of internet ups and downs, the core trajectory is:

Early vertical services (various portal entries where users search for numbers, find workers, and buy services themselves)

Mid-term service aggregation platforms (like 58.com, which aggregates traffic to match service providers with user needs)

Later intelligent platforms (combining algorithmic matching recommendations to improve intent accuracy, such as Didi's cross-city ride-sharing and customized services)

It can be said that the intent-centric concept is indeed beautiful, and the development history of web2 has also validated that this is a key path to expanding the user base. But can it really be so beautiful? Let's first look at the market application situation.

2. Typical Applications of Intent-Centric

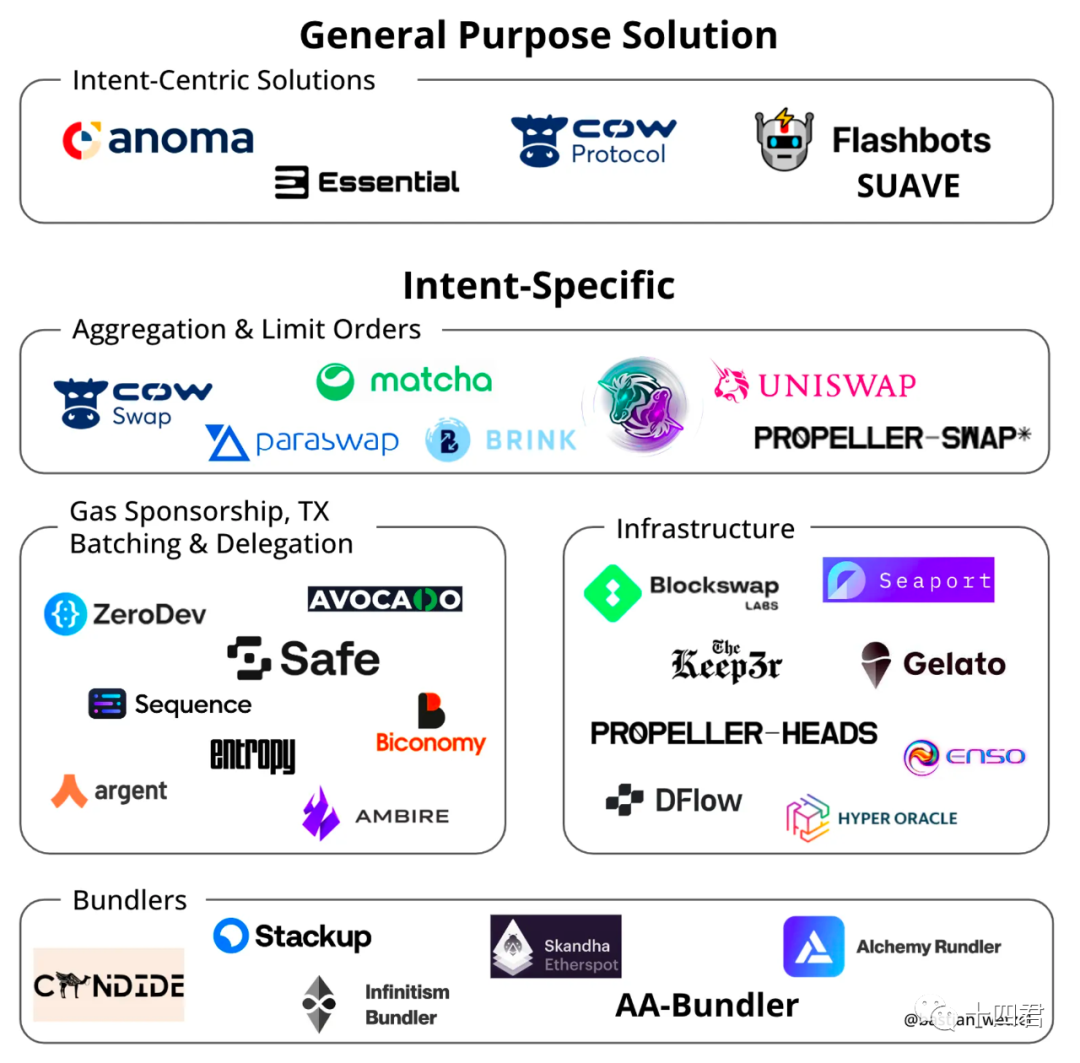

Although the concept of intent-centric has just been proposed, the number of projects involved is already considerable, or many projects in implementation are also centered around user intent. In Bastian Wetzel's article, various mainstream projects are categorized.

As shown in the figure below, many protocols are not general intent solutions but specific intent solutions, such as Uniswap and Seaport. This is a necessary developmental path for intent-centric solutions, similar to how web2 has successfully developed vertical solutions.

ERC-4337 serves as an infrastructure to assist intent, as the existence of bundlers reduces the necessity for users to have gas.

However, our core goal is still to explore the business models of these projects and whether they are sufficient to support the implementation of intent. In my view, the projects currently at the forefront of implementation are UniswapX, which realizes trading intent, and ERC4337, which will serve as a necessary infrastructure for intent.

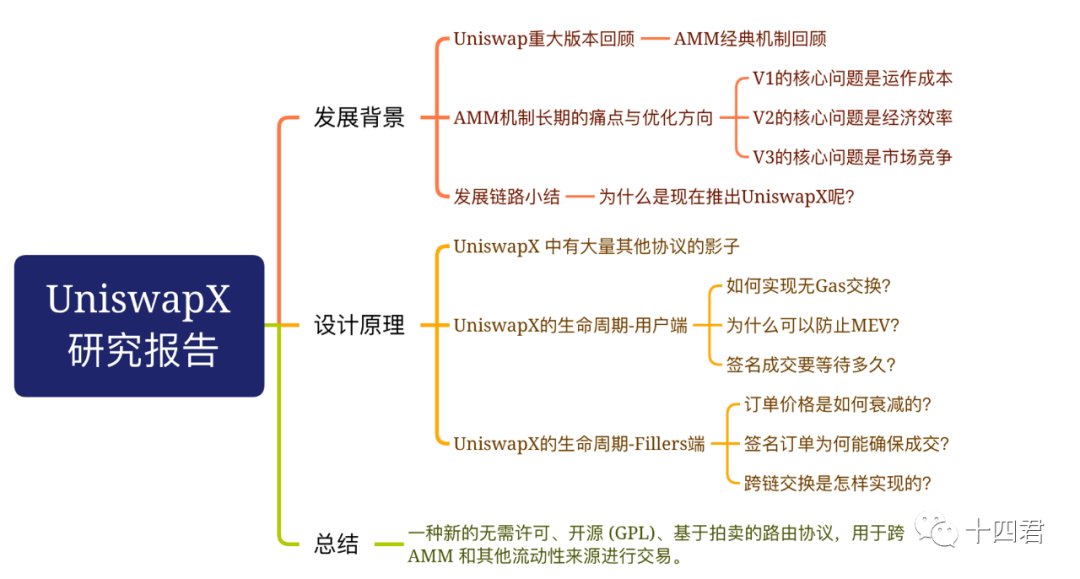

2.1 Looking at Intent-Centric from the Economic Design of UniSwapX

After the official announcement of UniSwapX, I participated as a Filler and as a quote provider in the RFQ system. The reason I say it is one of the most advanced intents is that it is the most mature system that directly addresses the economic incentive issues of counterparties regarding intent.

2.1.1 Why UniSwapX?

Summarizing the development of Uniswap V1-3, it can be said that past AMM protocols have faced specific issues such as user costs, transaction prices, trading links, routing services, LP incentives, and so on. Nowadays, the market situation for swaps can be described as MEV completely surrounding the on-chain memory pool, where every large-scale swap almost faces being sandwich attacked. Users always transact at the worst prices, with the profits being taken by MEV.

The launch of UniswapX attempts to address the above issues by fundamentally changing the AMM transaction mechanism from another dimension.

2.1.2 What is UniSwapX?

In definition: UniswapX is a new permissionless, open-source (GPL), auction-based routing protocol for trading across AMMs and other liquidity sources.

In fact, the operational model of the Web3 trading market can be broadly categorized into three types, besides the AMM model:

On-chain matching with on-chain order book model. Further reading: Contract Interpretation: CryptoPunk, the World's First Decentralized NFT Trading Market

Off-chain matching with on-chain order book model. Further reading: X2Y2 NFT Market System Operation Architecture

UniswapX transitions from the AMM model of Uniswap V1-3 to the off-chain matching with on-chain order book model.

2.1.3 How Does UniSwapX Operate?

From the user's perspective, if the scenario is that the user wants to trade ETH<=>USDT at a price around 1900 (allowing for a 2% slippage), they only need to:

Select an order, with a price decay curve limiting the order's time limit (e.g., exchange 1 ETH for 1950U within 1 day, with a minimum of 1850U)

Sign the order and publish it to the order book service cluster.

Wait for the transaction, which needs to be discovered and completed by a Filler.

For the user, that’s all they need to do.

From the Filler's perspective, they are the ones who actively complete user transaction orders. They have ample funds, are skilled in cross-chain information services, and have built a full-chain DexPool state monitoring service. They need to:

Scan on-chain pools of various protocols to build the foundational data needed for real-time order calculations.

Scan the Mempool to estimate future price trends.

Scan the RFQ Fillers' dedicated network to gain priority execution rights by providing quotes.

Scan the order information from the public network of Fillers to analyze the optimal transaction path.

If revenue conditions are met, they participate in bidding (every minute counts here; in an auction model, the later you go on-chain, the lower the price).

Analyze the bidding bottom line of other Fillers to find opportunities to prioritize their bids in the next profitable order (even if this reduces my single transaction profit, I will gain more volume).

So why do they have such a motivation to transact? This goes back to the economic model of UniswapX.

2.1.4 How to Evaluate the Intent Design of UniswapX

The willingness to publish intent itself is a key landing issue.

DEX has faced many limitations compared to CEX, such as trading costs, MEV, slippage loss, impermanent loss, etc. In the future, these will be countered by a more professional group of Fillers against the MEV group, gradually carving out a piece of the pie in technical competition, ultimately returning to the users and forming a positive development cycle (more users using UniswapX leads to more Fillers receiving fee dividends).

Moreover, the complexity of on-chain transaction routing will also be decentralized into the backend system, allowing users to simply submit orders without worrying about the complicated routing issues.

Thus, this is a virtuous economic cycle where both parties benefit; a healthy economic model will always land in practice.

Further reading: https://research.web3caff.com/zh/archives/10004?ref=shisi

2.2 Looking at Intent-Centric from ERC4337

In the application diagram above, the bottom section revolves around account abstraction (AA). For systems like UniswapX, since the transactions are submitted by Fillers, users can complete cross-chain transactions without gas.

However, throughout the entire transaction cycle, users still need to submit an approve transaction to allow UniswapX's on-chain contract to deduct the user's amount. If a pure intent trading model (completely without user-initiated transactions) is desired, ERC4337 is still needed as the account entity and paymaster's integrated design.

Regarding what ERC4337 is, its implementation principles, and development history, Shisi Jun has previously conducted live streams and summaries. Further reading: Explaining Account Abstraction in One Hour

In simple terms, ERC4337 is a set of infrastructure:

On-chain, it verifies user signatures through the entryPoint contract for authentication, ultimately driving the user's CA account as the identity entity.

Off-chain, it uses user-signed UserOperation as instructions, transmitted in the Bundlers network, where Bundlers batch package and execute on-chain.

The core optimization of this mechanism is that it can enhance local functions through the high customization capability of CA, such as social recovery wallets, or allowing project parties to cover gas fees for users, supporting USDT and other payment methods for gas.

However, today we will analyze the value of 4337 for intent from a business model perspective.

Looking back at why we consider UniswapX's business model good, it is because both parties in the token transaction (users and Fillers) benefit, with only MEV being the losing party. But looking back, ensuring the profits and willingness of counterparties through fees is merely one type of business model. In the future, most "intent" applications will likely adopt a direct To B revenue model or a main product To C subscription model, but the main product's services will not only satisfy "intent" services.

Just like payment systems, WeChat Pay or Alipay do not charge fees on C2C transactions but generally charge a 0.6% fee when merchants withdraw funds (which also requires payment to the underlying transaction system).

In the past decade of mobile internet battles, the goal has primarily been to achieve a high user base, with the revenue loop placed after the user base.

Thus, more Dapps will emerge in the future, and to allow users to experience and use their Dapps, they will be happy to provide gas-free servers. This is similar to the Lens social protocol, which will cover hundreds of thousands of dollars in fees weekly to cultivate user usage and content ecology on Polygon. Compared to the millions spent daily in the past ride-hailing wars, this is just a drop in the bucket.

Therefore, the most standard, universal payment mechanism, and the most trustworthy platform credit system, will inevitably be the paymaster system on ERC4337 (originating from meta-transactions but exceeding them).

It is a special smart contract account that can pay gas fees for others. The payment master contract needs to perform some verification logic for each transaction and check during the transaction process. The Paymaster contract can check if there is enough approved ERC-20 balance in the "validatePaymasterUserOp" method and then use "transferFrom" in the "postOp" call to extract it. (For specific execution logic interpretation, please refer to the Bilibili live stream recording in the further reading above.)

In summary, this is a more universal gas-free solution compared to meta-transactions, as it avoids the chaos of non-standardization and has no forward compatibility issues (meta-transactions require contract modifications for support).

3. What Are the Challenges of Implementing Intent?

In conclusion, intent is indeed beautiful, and it is bound to be a direction for continuous development and optimization. Beyond the challenges of business models, what technical details are the core difficulties of its implementation?

3.1 Contradictions with AI Integration

Although many analyses of intent suggest that the trading intent analysis capabilities provided by AI are optimization points for experience, I have previously worked in the security policy industry, and one major insight is that interpretability and reproducibility are the most important aspects of AI applications in policy scenarios. For example, in account bans, if the exact reason for the policy hit cannot be provided, it becomes difficult to justify once a user files a complaint. Similarly, for any financial system, pursuing stability and consistency is the top priority; no institution can guarantee that AI will not act maliciously once it has asset control.

Therefore, AI will only serve as an auxiliary tool for intent analysis for a long time, and on-chain data analysis requires a deep understanding of the principles of blockchain operation; otherwise, false positives are likely to occur.

Further reading: In-depth Risks Behind EVM - Contract Classification

3.2 IntentPool's Anti-Dos Risks and Solver Matching Issues

For IntentPool, similar to the memory pool of ERC4337, it will also be a significant bottleneck. First, IntentPool cannot reuse the MemPool mechanisms of existing Ethereum clients (Geth, Erigon), and must be built separately.

Even with ERC4337's BundlerPool as a reference, the MemPool designs have their own advantages and disadvantages.

Decentralized memory pool models: There are propagation mechanism issues because executing intents is a profitable activity for many applications. Therefore, nodes operating the intent pool have the incentive not to propagate to reduce competition when executing intents.

Centralized memory pool models: This solves the propagation mechanism issue but cannot avoid centralization audit and intervention problems.

In summary, designing an intent discovery and matching mechanism that is both compatible with incentives and not centralized is not an easy task.

3.3 Intent Privacy Risks

Signatures have an irrevocable characteristic; even if an expiration time is added to the signed content, there is still the issue of being unable to cancel the signature at low cost before this expiration time (any cancellation must send a transaction on-chain).

Thus, some general intent solutions attempting to address standardization and privacy, such as Anomo, have emerged.

Privacy protection is difficult to achieve through EVM systems, so currently, there are more cutting-edge developments around new privacy-preserving intent languages, such as Juvix, which is used to create privacy-focused decentralized applications. It can be compiled to WASM or compiled into circuits via VampIR for private execution on Anoma or Ethereum using Taiga.

4. Conclusion

It is indeed encouraging to see the concept of intent gaining traction; Web3 is finally starting to break through the bottleneck of truly popularizing for users, moving away from self-indulgent narratives. Only by focusing on the most practical needs of users, rather than getting lost in grandiose storytelling, and by providing considerate services, can we gradually win over a broader user base.

In the future, the intent model will either create revenue from fees to subsidize counterparties, like UniSwapX, or from the perspective of overall system user segmentation, with a small number of high-paying users and a large number of non-paying but important ecosystem users.

Thus, intent itself is about optimizing the product experience rather than being an end in itself.

Moreover, DeFi will be the first stage for intent to flourish. More than 20 DeFi protocols have already collaborated with DappOS, and Brink Trade has developed an intent engine that can encapsulate operations like Bridge, Swap, and Transfer within a single intent through one signature. Additionally, established protocols like CowSwap, 1inch, Uniswap, and LlamaSwap are continuously expanding their functionalities to meet more user intents.

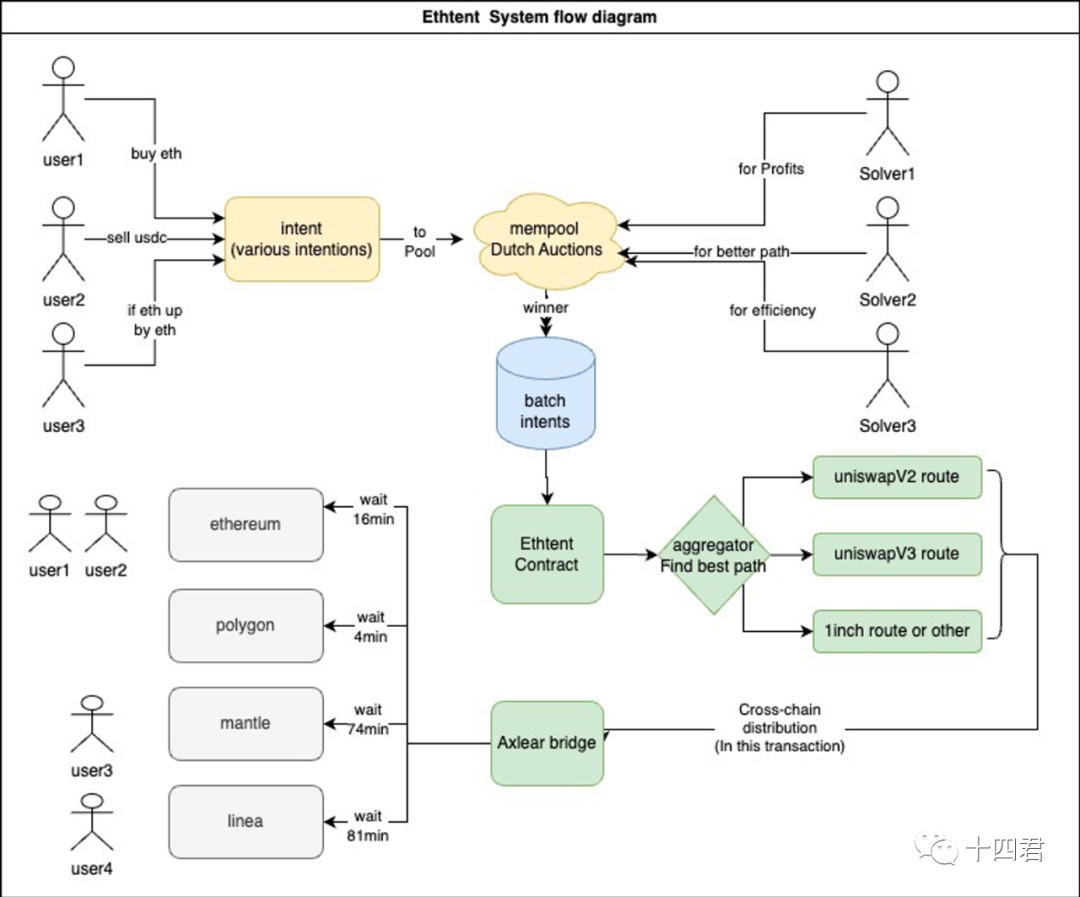

In this Token2049 hackathon, I also participated in the DeFi track, solving an intent solver for a cross-chain Swap + strategy-assisted investment scenario (the operation of the Ethtent system is shown in the figure below).

It is worth noting that implementing fixed-demand vertical intents on the existing EVM infrastructure is not difficult. The real challenge lies in the future emergence of a market for intent solvers, or a collaborative framework of collaborative standards, which allows different solvers to further combine and reuse to achieve universally standardized intent solutions while also coordinating economic models to address both parties' willingness.

Standardization often requires top-down standard definitions. Currently, DappOS and Anomo are at the forefront of this path, which is worth looking forward to.

Appendix: "Intent-Centric Track Ten Thousand Word Research Report: Can 'Intent-Centric' Architecture Become a New Engine for Large-Scale Adoption of Web3?" https://research.web3caff.com/zh/archives/11091#comment-1393?ref=shisihttps://github.com/neeboo/ethtenthttps://www.paradigm.xyz/2023/06/intents#the-middlemen--their-mempoolshttps://www.xiaoyuzhoufm.com/episode/64eca0013fa4090b747de18fhttps://bwetzel.medium.com/intent-based-architectures-and-projects-experimenting-with-them-c3ee63ae24c