Analysis: Why friend.tech does not experience a wave of popularity like other SocialFi platforms, and the hidden risk points

Compared to once-popular products like Voice created by Block One, which attracted billions of dollars from investors, Deso that made the market believe DeSocial was truly coming, and the protocol-level Lens, why is friend.tech able to attract more real users willing to participate with real money, and why is it currently so resilient?

Compared to once-popular products like Voice created by Block One, which attracted billions of dollars from investors, Deso that made the market believe DeSocial was truly coming, and the protocol-level Lens, why is friend.tech able to attract more real users willing to participate with real money, and why is it currently so resilient?Written by: Misty Sea, PANews

The overall market in the cryptocurrency space is quiet, but a group of explorers is constantly refreshing the friendtech product page, buying and buying. Communities that usually discuss tokens and NFTs have turned into places where members recommend promising KEYs to each other. But who would have thought that just half a month ago, 90% of the voices online were bearish and filled with FUD, with labels like Ponzi scheme and one-time flow tightly attached to friendtech.

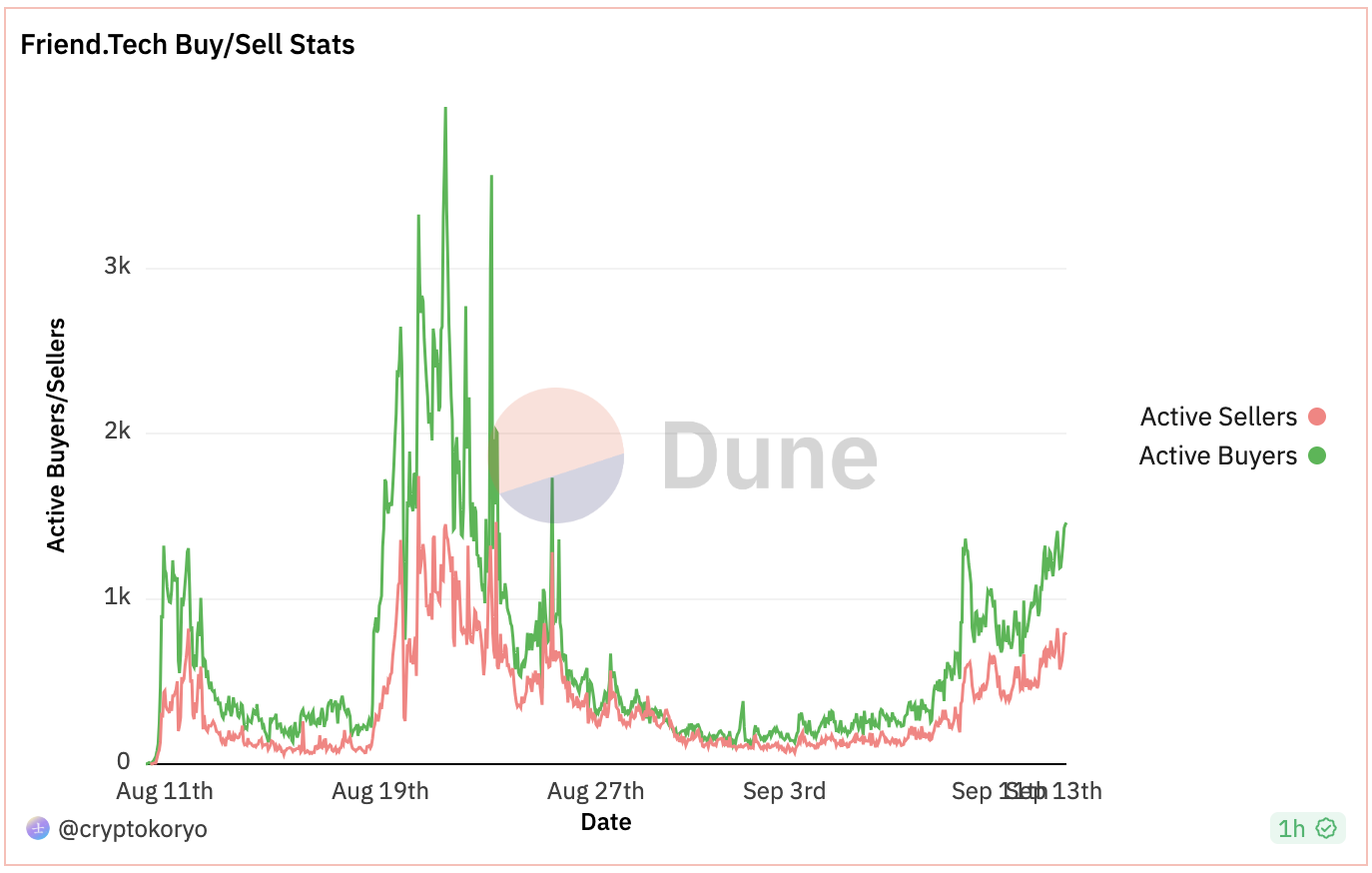

From the data, friendtech has gone through three waves of development since its inception. On August 10, 2023, friendtech officially launched. On August 11, the Chinese community began to spread the news vigorously, driven by its novel model, expectations for airdrops, and a keen sense of the need to participate in new gameplay. On that day, there were 130,000 transactions, with 1,000 active buying accounts and 500 accounts sold.

However, the good times didn't last long. After a wave of novelty, the number of active buying accounts dropped to around 300 on the third day, and the transaction count fell to about 30,000. During this period, a large amount of negative discussion about the product emerged. Until August 19, when the official announcement of seed round investment from Paradigm was made, the number of active buying accounts surged to a daily high of 4,000, with transaction numbers exceeding 500,000, and TVL rising from just over 1 million to 7 million. However, the market did not respond positively, and after three days, the enthusiasm declined again. The number of active buying accounts fell to even lower levels, dropping to just over 100, and transaction numbers returned to their initial levels, with TVL stabilizing around 5 million after a decline.

After a low-key development period of half a month, recently, friendtech's transaction numbers suddenly surged, doubling compared to before. TVL began to grow sharply, reaching 31 million dollars. The number of independent accounts reached 140,000, while the daily active address count has not yet reached previous highs. Thus, after experiencing a market peak following financing, friendtech is currently undergoing a new wave of enthusiasm.

Why is friendtech so resilient?

Compared to once-popular products like Voice, created by Block.one, which harvested billions from investors, or Deso, which made the market believe that DeSocial had truly arrived, or the protocol layer Lens, why are more real users willing to participate with real money in friendtech, and why is it currently so resilient? PANews believes there are four key factors.

1. User Base

According to PANews observations, the recent explosion of friendtech comes from various institutions and project founders in the English-speaking community, as well as high-traffic and reputable bloggers continuously joining, bringing real money and guiding overall market attention. Subsequently, high-traffic domestic bloggers also joined in, attracting some observers to try it out.

At the same time, friendtech's incentive rules are designed to eliminate low-quality accounts from the outset. Whether it's Voice, Deso, or even the still highly anticipated Lens, social products inevitably create or even welcome the model of one person having multiple accounts, accelerating the product's rapid journey into a bubble phase. In the absence of follow-up strength, users who came to exploit or arbitrage exacerbate the stampede, leading to the product's accelerated decline.

Looking back at friendtech's early users, many were focused on airdrops, habitually registering multiple accounts to maximize airdrop value. However, friendtech's point distribution rules do not incentivize invitations or low-quality accounts, so the multiple addresses used by users aiming for greater airdrop value became inactive, leaving behind users who deeply engaged with friendtech.

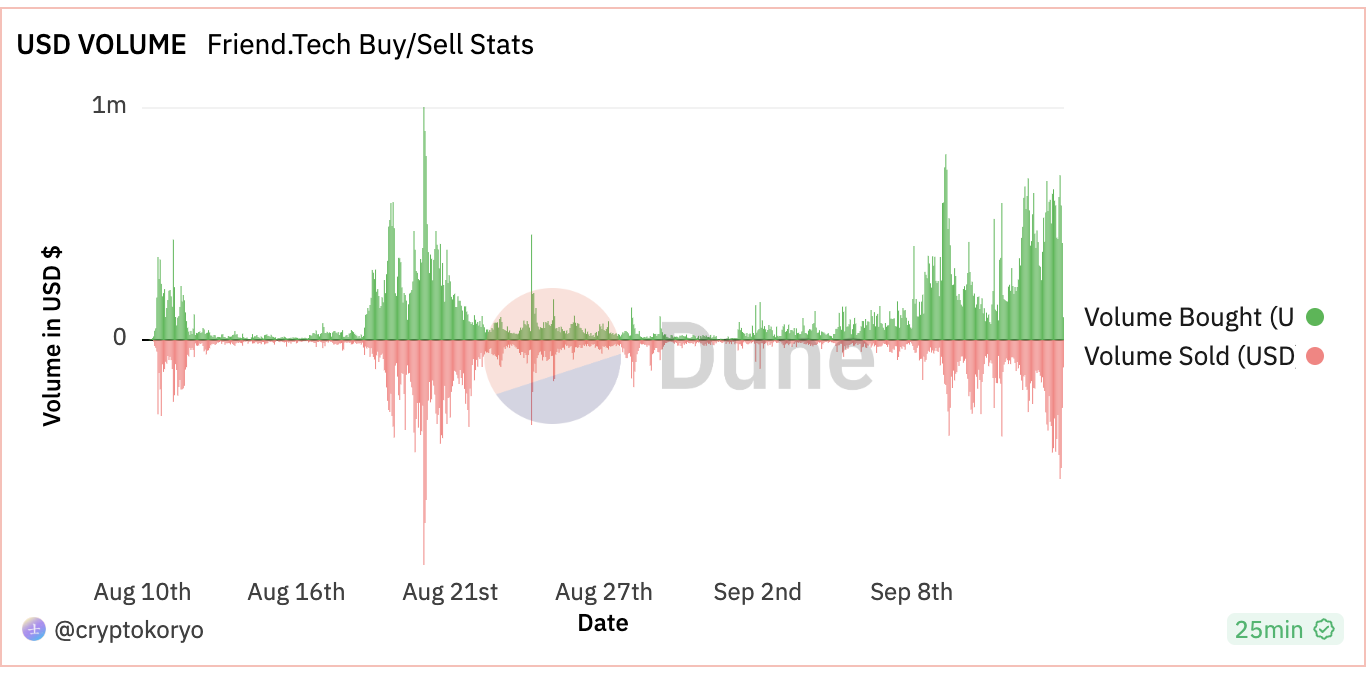

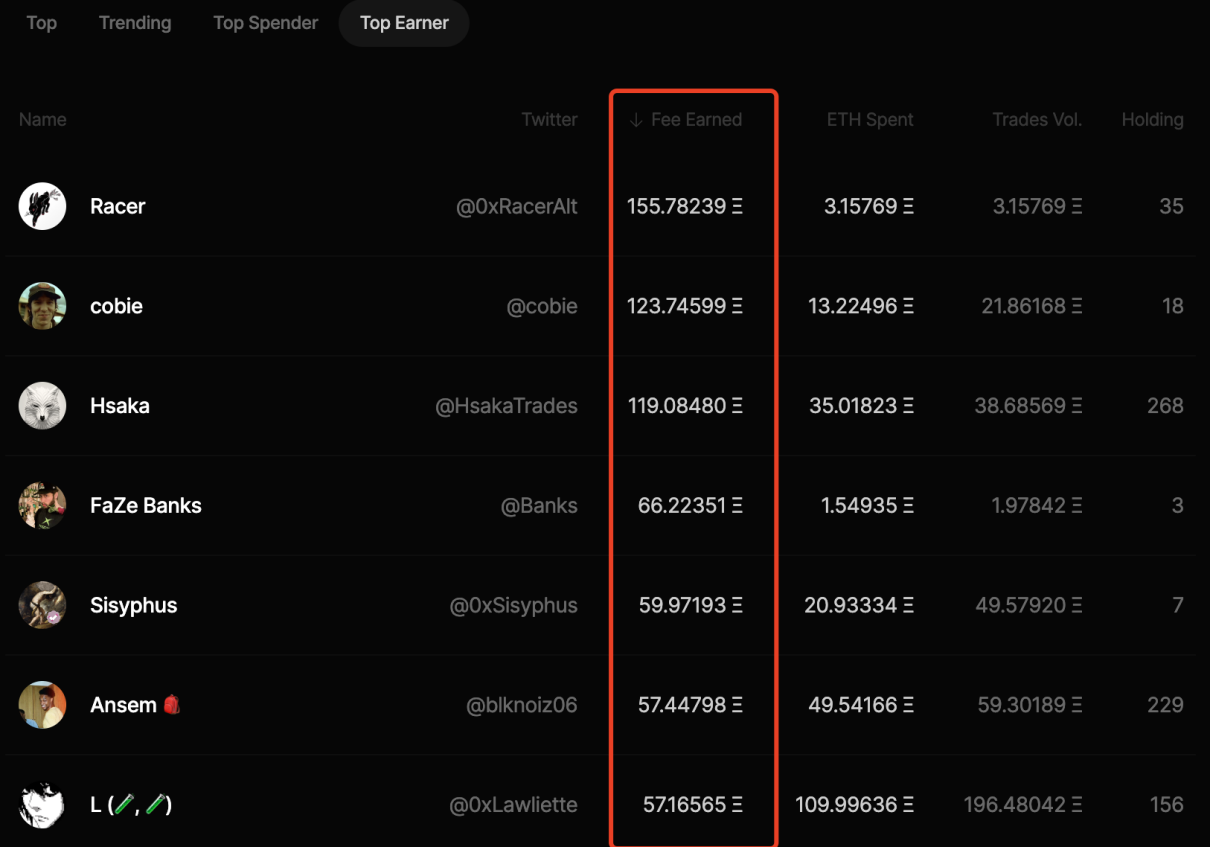

Additionally, friendtech's registration mechanism is strongly tied to the Twitter platform, and half of the 10% transaction cost is shared with room owners. This not only perfectly leverages external forces for a cold start but also provides substantial incentives for room owners to join and share. According to Dune data, as of September 14, friendtech has generated a total of 8.37 million dollars in revenue for room owners.

2. Airdrop Expectations

In addition to the 5% incentive for room owners based on transaction volume, friendtech will distribute a total of 100 million points to users weekly over the next six months. The community currently expects that these points are highly likely to be closely related to the project's token airdrop. The community generally optimistically estimates that friendtech's total circulating market value at launch could reach 2 billion dollars, meaning each point would be valued at 2 dollars based on a 10% airdrop share.

According to the official disclosure of the point distribution rules, the influencing factors are room activity * total amount of KEY assets held * holding duration. Community members analyze that the weight of total KEY assets held * holding duration accounts for 85%, while room activity accounts for 15%.

From the point distribution rules, it can be inferred that if users want to earn more points, the optimal choice is to hold long-term. This has led to the expectation that the price of KEY held by room owners will rise as more funds and users enter. Additionally, a (3,3) phenomenon has emerged in the community, where users buy and hold without selling to achieve higher points together.

How to obtain points/airdrops more cost-effectively?

1) Bots, information asymmetry, and price differences. Although bots also compete with each other, as long as they are faster than manual users, it suffices. The technical barrier is low, focusing on discerning conditions.

2) Top-tier, under the current model and expectations, not many people are selling. If more funds continue to enter, it may even lead to risk-free mining. However, a potential risk is that if early buyers reach their profit expectations, profit-taking may cause panic among others. According to Dune data, there are currently signs of profit-taking sentiment.

3) Use your A account to buy your B account, effectively exchanging 20% friction for points. However, registration is needed to prevent bot MEV attacks, which could lead to losses.

4) Join some bot communities that refresh new account user information in real-time, selecting those with many followers, and judging whether they are worth buying based on their offline reputation and on-chain asset status.

3. Strong Resources

According to official disclosures, the only investment institution in friendtech currently is Paradigm. Paradigm's capabilities have been proven by the market, with multiple projects it has invested in and guided, such as Uniswap, dydx, and Blur, growing into phenomenal products and market necessities.

Some community members believe that the products invested in by Paradigm all have a Ponzi-like model. Here, we won't discuss how common Ponzi schemes are in the investment circle or even in human society; rather, from a product perspective, Uniswap has often been criticized for providing no actual dividends to token holders, yet it has genuinely brought a new model to on-chain trading in the crypto space, which continues to this day. The same applies to the Blur token, which has provided significant convenience for NFT users to exit effectively. It can be said that without Blur, the NFT space would be a vacuum scam with prices but no market during a bear market.

Additionally, friendtech is built on the Base chain. The development and rise of a chain are undoubtedly reliant on the construction of quality projects, and it is clear that the Base official is also a strong stakeholder in friendtech. Behind the Base chain is Coinbase, which has top-tier influence in the space.

4. Upward Socialization

Currently, products related to social interaction in the cryptocurrency space aim to solve issues like content data rights confirmation and cross-platform compatibility at the protocol layer. However, if we set aside the blockchain facade, platforms like WeChat, Twitter, Telegram, and Discord have perfectly met user needs. Adding a layer of decentralization is more of a self-indulgent conceptual gimmick to fool capital into believing there is a need.

The emergence of friendtech addresses a significant gap in the current market: upward socialization. Products like Knowledge Planet in the internet space partially fill this need, but there has not been a similar product for proven project founders and institutions in the cryptocurrency space, and venture capital groups have no need to actively interact with users of relatively lower cognitive levels.

Moreover, professionals from fields such as healthcare and education have already opened friendtech accounts to provide corresponding services. Compared to physical institutions, their communication or inquiry prices are more favorable and convenient.

In response to these needs, friendtech has created a product that allows users to access levels that were previously difficult to reach and communicate with, and they can obtain 1-on-1 consultations at prices lower than the market rate.

What are the potential risks of participating in friendtech?

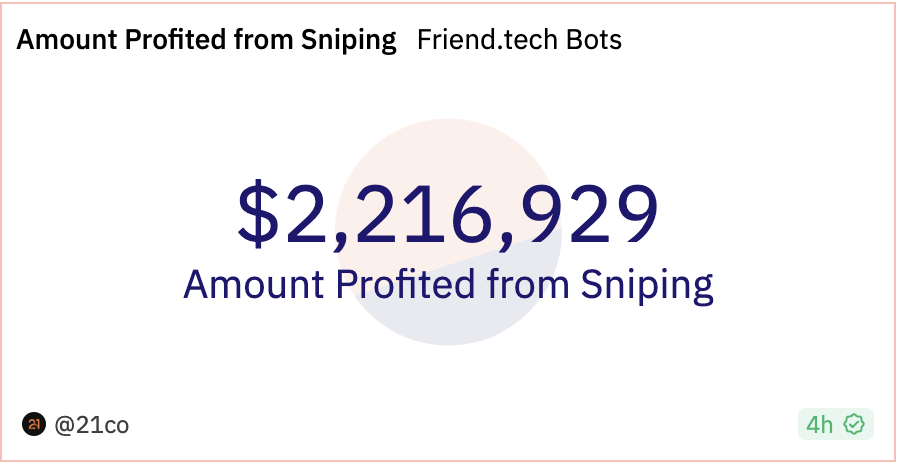

1. High Bot Profits

Due to community expectations that more influential bloggers will have higher KEY values, bots have found opportunities to analyze data and purchase ahead of normal users, then sell after achieving a certain level of profit. Even if some users try to prevent bots from analyzing data by enabling Twitter's privacy mode, there are still bots that conduct MEV attacks based on on-chain secondary trading situations.

According to Dune data, currently, over 140 bots have collectively earned 2.2 million dollars through friendtech, with their profits accounting for as much as one-quarter. This raises the entry barrier for normal users and may also exacerbate the degree of collapse when reverting to normal conditions.

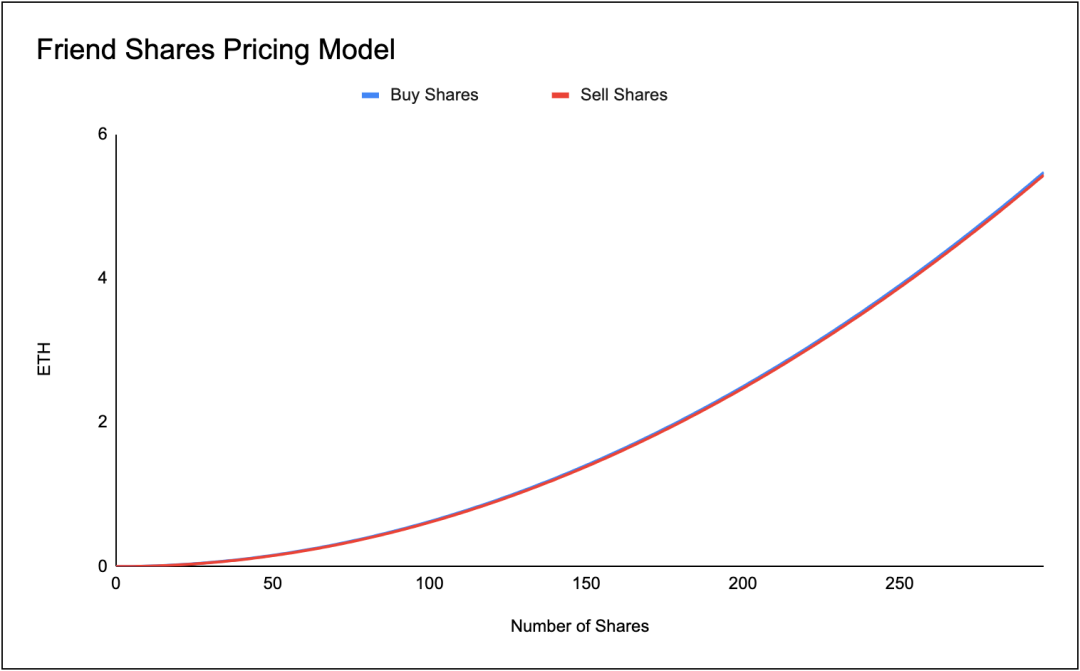

2. Steep Curve, Exacerbating Death Spiral

The price curve for friendtech's user KEY is defined as: price (ETH) = (Total Keys^2) / 16000. For the earliest discovered users, the cost is almost zero, but once the number of purchased KEYs exceeds 20, the price difference between users rapidly widens.

This has led to situations in the community where someone buys a certain KEY and calls for others to follow; as long as more than two users follow, the caller makes a profit. If multiple KEYs are bought, short-term multiples can easily rise, leading to the current PVP phenomenon within groups.

Additionally, high multiples attract more users, but once the number of people who can be spread to reaches its limit, early users start to take profits, causing prices to plummet and triggering panic selling, leading to a death spiral. Later buyers not only have to bear the 20% friction sunk cost but also inevitably suffer losses in KEY prices.

The impact of this is that once prices fall, liquidity becomes virtually nonexistent. According to the nature of cryptocurrency users, basic social interactions will stagnate, reverting from the original (3,3) to -(3,3). According to PANews' tests, purchasing a KEY to enter a room, no matter how actively the room owner shares, when the room's KEY price does not rise or trading stagnates, the room will begin to fall silent, and prices will start to collapse.

3. Product Logic Contradicts Profit Model

Friendtech's incentive model for points encourages users to hold long-term, and based on the normal user's basic needs, entering a room to enjoy the room owner's long-term service should also imply long-term holding. However, the profit model for friendtech officials and room owners relies on users trading more frequently, similar to an exchange logic, extracting transaction fees.

This means that the official takes on the role of an exchange, ensuring a constant income from transaction fees. However, for room owners, if the room's KEYs are held more rather than traded multiple times for fee sharing, they will earn nothing, leaving them with no motivation to provide services to room users.

Over time, this will lead to more speculative room owners earning more profits, while those providing long-term services earn very little, causing rooms to inevitably fall silent. This creates a negative cycle for the entire ecosystem. Product data indeed reflects this, with speculative room owners capturing the vast majority of profits.

Conclusion

Compared to previous social products, friendtech has not followed the path of pseudo-needs wrapped in blockchain, but has genuinely captured a market gap. Furthermore, it has not succumbed to the numerous exploitative groups but has naturally filtered them out through rule design. Additionally, its strong backing generates more speculation in the market, motivating users to try it out. Friendtech currently enjoys the highest level of enthusiasm and attention in the market.

However, after firsthand experience, aside from the highly anticipated airdrop expectations and potential secondary trading profit expectations, the product's inherent user logic has significant flaws.

Its original intention is to serve room owners, indirectly serving more users. However, the value provided to the platform that truly generates energy is very low, while the value of providing speculative sentiment is extremely high, leading to substantial profits. Not to mention that over a quarter of the profits are divided among bots that add no value.

At this point, we can only hope that the officials will introduce rules to change the current situation, allowing the platform to truly generate long-term value. For users considering participation, it is always our investment philosophy to try market innovations and new concepts, but it is crucial to remember: prioritize position management.