Pantera Capital Investment Methodology: How to Evaluate the Crypto Market Through Fundamentals and Macroeconomic Environment?

The maturity of the digital asset space may be similar to the turning points in the development of the stock market.

The maturity of the digital asset space may be similar to the turning points in the development of the stock market.Written by: Cosmo Jiang, Erik Lowe

Compiled by: Deep Tide TechFlow

In recent months, there have been some positive developments in the cryptocurrency regulatory environment in the United States. We all know about the ruling from the U.S. District Court for the Southern District of New York in the three-year lawsuit between the Securities and Exchange Commission (SEC) and Ripple Labs, which determined that XRP is not a security. We refer to this as a "positive" black swan event that few anticipated.

Cryptocurrency has recently achieved another unexpected victory. On August 29, the U.S. Court of Appeals made a ruling in favor of Grayscale in its lawsuit against the SEC regarding its spot Bitcoin ETF application, which was rejected last year. We believe this significantly increases the chances of approval for spot Bitcoin ETF applications submitted by firms like BlackRock, Fidelity, and others.

While the U.S. may seem to lag behind many regions of the world in embracing digital assets, many countries have taken measures that are as stringent, if not more so, than those regarding cryptocurrencies. However, the redeeming quality of the U.S. is its court system, which is committed to due process, ensuring there are avenues for correction when overreach occurs.

"The rejection of the Grayscale proposal is arbitrary and capricious, as the Commission failed to explain its different treatment of similar products. Therefore, we support Grayscale's petition and vacate that order."

------ Court opinion submitted by Judge RAO

We have long emphasized the need for trustless systems. In our industry, this means users can rely on blockchain-based architectures to execute designs fairly. We can rely on the U.S. court system to do the same, which helps shape a promising regulatory environment for the future of cryptocurrency, fostering more innovation to occur onshore.

We have long discussed the potential of spot Bitcoin ETFs, and now we see a glimmer of hope.

Similar Maturity of the Crypto Industry and Stocks

The maturity of the digital asset space may be akin to a turning point in the development of the stock market.

Tokens represent a new form of capital that may replace equity for an entire generation of companies. This means many companies may never list on the New York Stock Exchange and will only have tokens. This is a way to align the interests of businesses with management teams, employees, token holders, and potentially other stakeholders unique to digital assets, such as customers.

Currently, there are about 300 publicly traded liquid tokens with a market capitalization exceeding $100 million. As the industry expands, this investable universe is expected to continue growing. More and more protocols have product use cases, revenue models, and strong fundamentals. Applications like Lido or GMX did not exist two or three years ago. In our view, sifting through this vast universe for ideas could be a significant source of alpha, as not all tokens are created equal, just like stocks in the stock market.

Pantera focuses on finding protocols with product-market fit, strong management teams, and attractive and defensible unit economics, believing this is a widely overlooked strategy. We believe we are at a turning point for this asset class, where traditional and more fundamental frameworks will be applied to digital asset investments.

In many ways, investing in digital assets is similar to the significant turning points that the stock market has developed over time. For example, fundamental value investing today is taken for granted, but it only began to gain popularity in the 1960s when Warren Buffett launched his first hedge fund. He was a pioneer in applying Benjamin Graham's lessons in practice, which propelled the development of what we now know as the long/short equity hedge fund industry.

Investing in cryptocurrencies is also akin to emerging market investments in the 2000s. It faces criticisms similar to those of the Chinese stock market at the time, where many companies were small players in an irrational stock market driven by retail investors. You don't know if management teams are misleading investors or misappropriating funds. While there is some truth to this, there are also many high-quality companies with strong long-term growth prospects that present excellent investment opportunities. If you are a discerning, fundamentals-focused investor willing to take risks and put in the effort to find these good ideas, you can achieve incredible investment success.

Our main point is that the prices of digital assets will increasingly trade based on fundamentals. We believe the rules applicable in traditional finance will also apply here. There are now many protocols with real revenue and product-market fit, attracting loyal customers. More and more investors are using a fundamental perspective, applying traditional valuation frameworks to price these assets.

Even data service providers are beginning to resemble those in traditional finance. But they are not Bloomberg and M-Science; they are Etherscan, Dune, Token Terminal, and Artemis. Their purpose is essentially the same: to track key performance indicators, profit and loss statements, management team actions and changes, and more.

In our view, as the industry matures, the next trillion dollars entering this space will come from institutional allocators who embrace these fundamental valuation techniques. By investing using these frameworks today, we believe we are at the forefront of this long-term trend.

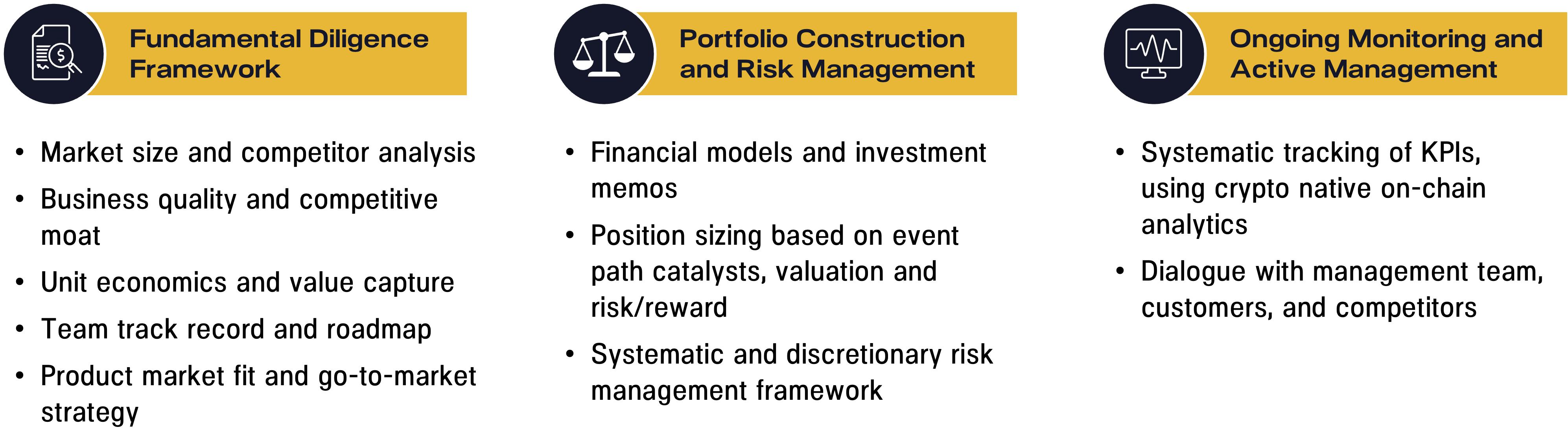

Fundamental-Based Investment Process

The fundamental-based investment process for digital assets is similar to that for traditional equity assets. This may be a pleasant surprise for investors in traditional asset classes and a key misunderstanding.

The first step is to conduct fundamental due diligence, answering the same questions as when analyzing public stocks. Is the product market fit? What is the total addressable market (TAM)? What is the market structure? Who are the competitors, and what is their differentiation?

Next is business quality. Does this business have competitive moats? Does it have pricing power? Who are their customers? Are they loyal, or will they leave quickly?

Unit economics and value capture are also very important. Although we are long-term investors, cash is ultimately crucial, and we want to invest in sustainable businesses that can eventually return capital to their token holders. This requires sustainable profitable unit economics and value capture.

The next layer of our due diligence process is to study the management team. We care about the management team's background, track record, incentive alignment, and their strategy and product roadmap. What is their go-to-market plan? Who are their strategic partners, and what is their distribution strategy?

Compiling all this fundamental due diligence information is the first step for each investable opportunity. This will ultimately lead to building financial models and investment memoranda for our core holdings.

The second step is to translate this information into asset selection and portfolio construction. For many of our holdings, we have multi-year three-statement models with capital structures and forecasts. The models we create and the memoranda we write are at the core of our process-oriented investment framework, enabling us to knowledgeably and foresightedly select investment opportunities and adjust position sizes based on event path catalysts, risk/reward, and valuation.

After making investment decisions, the third step is to continuously monitor our investments. We have a systematic data collection and analysis process to track key performance indicators. For example, for our investment in the decentralized exchange Uniswap, we actively collect on-chain data in our data warehouse to monitor the trading volume of Uniswap and its competitors.

In addition to monitoring these key performance indicators, we strive to maintain dialogue with the management teams of these protocols. We believe it is essential to conduct field research calls with management teams, their customers, and various competitors. As a mature investor in this space, we can also leverage Pantera's broader network and connections within the community. We see ourselves as partners and are committed to helping management teams in areas such as reporting, capital allocation, or best management practices, contributing to the growth of these protocols.

Fundamental-Based Investment Practice: Arbitrum

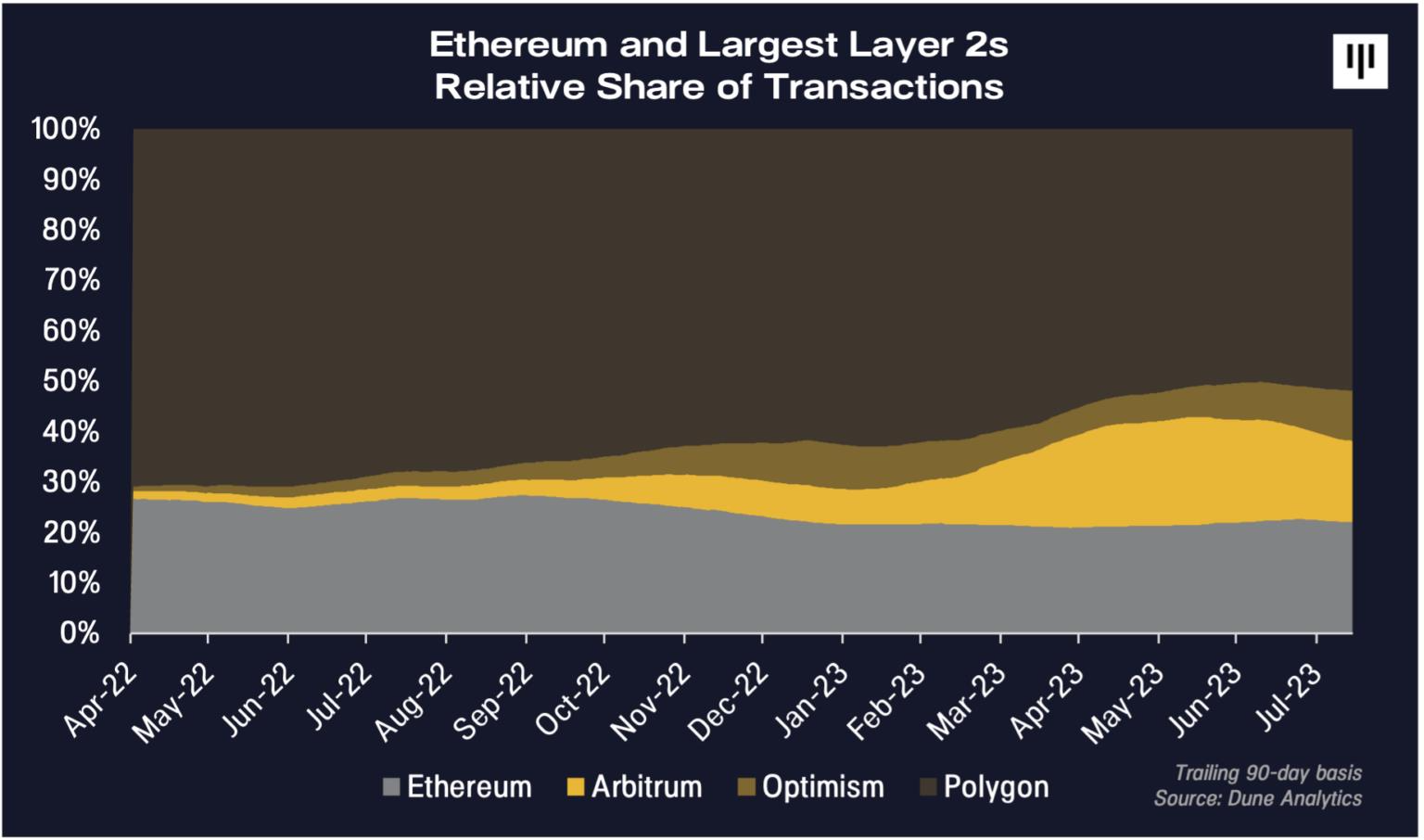

One major criticism of Ethereum is that during periods of increased activity, transactions on the base layer can become slow and expensive. While the roadmap for creating scalable platforms has been contentious, second-layer solutions like Arbitrum are emerging as viable solutions.

Arbitrum's primary value proposition is simple: faster and cheaper transactions. Compared to trading on Ethereum, its transaction speed is 40 times faster and costs 20 times less, while being able to deploy the same applications and maintain the same security as trading on Ethereum. Thus, Arbitrum has found product-market fit and has shown strong growth both absolutely and relative to its peers.

For fundamental investors looking for evidence of traction in growth, Arbitrum ranks high on that list. It is one of the fastest-growing second-layer solutions on Ethereum and has captured a significant share of the trading market over the past year.

To delve deeper into this last point, Arbitrum is one of the few chains that showed growth in trading volume throughout the bear market, while overall usage was relatively weak. In fact, when looking at the data separately, you will find that Arbitrum has contributed 100% of the growth in the Ethereum ecosystem this year among Ethereum and all its other second-layer solutions. Arbitrum holds a massive share within the Ethereum ecosystem, while Ethereum itself holds a significant share across the entire cryptocurrency space.

Arbitrum's network is in a virtuous cycle. According to our field research, developers are attracted to the growing usage and user base on Arbitrum. This is the positive network virtuous cycle: more users mean more developers interested in creating new applications on Arbitrum, which in turn attracts more users. But as fundamental value investors, we must ask ourselves, does all this matter unless there is a way to monetize this activity, right?

The answer to this question is why we believe this is a good fundamental investment opportunity—Arbitrum is a profitable protocol with multiple upcoming potential catalysts.

In this space, many ordinary investors may not realize that there are actually some protocols that can generate profits. Arbitrum generates revenue by charging transaction fees on its network, batching those transactions, and then paying the Ethereum base layer to publish those large batches of transactions. When a user spends 20 cents on a transaction, Arbitrum collects that fee. They then bundle those transactions into large batches and publish them to the Ethereum first layer, paying about 10 cents per transaction. This simple math means Arbitrum can earn about 10 cents in gross profit per transaction.

We have found a protocol that has achieved product-market fit and has reasonable unit economics, which ultimately leads us to believe its valuation is sound.

Growth in Key Operating Metrics for Arbitrum

Here are some charts that illustrate some fundamentals.

Since its launch, the number of active users has consistently grown, with nearly 90 million transactions per quarter. Revenue for the second quarter was $23 million, with gross profit reaching nearly $5 million in the second quarter, annualizing to $20 million. These are key performance indicators that we can track and verify daily on the blockchain to monitor whether Arbitrum aligns with our investment thesis and financial forecasts.

Currently, there are about 2.5 million average monthly users, each conducting an average of 11 transactions per month, resulting in an annual transaction count of approximately 350 million. Based on this data, Arbitrum is essentially a business with an annual revenue of $100 million, generating about $50 million in standardized gross profit. Suddenly, this becomes a very interesting business.

As for catalysts and reasons that make it a timely investment, a key part of our research process is tracking the entire Ethereum technology roadmap. The next significant step is an upgrade called EIP-4844, which will effectively reduce transaction costs for roll-ups like Arbitrum. Arbitrum's main cost, which is 10 cents per transaction, could be reduced by 90%, becoming 1 cent per transaction. By then, Arbitrum will have two options. They can pass these cost savings directly to users, further accelerating adoption, or they can retain these cost savings as profit, or both. Either way, we foresee this being an important catalyst for increasing Arbitrum's usage and profitability.

In fundamental investing, focusing on valuation is an important part. Based on the shares outstanding, Arbitrum currently has a market capitalization of $5 billion. In our view, this is quite attractive relative to some first-layer and second-layer protocols with similar market capitalizations but only a fraction of the usage, revenue, and profits.

To put this valuation in the context of growth, we believe that in the next year, Arbitrum's transaction volume could grow to over 1 billion transactions annually, with a profit of 10 cents per transaction. This implies about $100 million in revenue, which means that at a $5 billion market cap, the forward earnings valuation is about 50 times. From an absolute value perspective, this may seem expensive, but in our view, it is reasonable for an asset still growing at triple digits. Compared to real-world business valuations, if you look at popular software companies like Shopify, ServiceNow, or CrowdStrike, which have revenue growth rates in the double digits, the average trading multiples are about 50 times, while their growth rates are far below Arbitrum's.

Arbitrum is a protocol with product-market fit, growing very rapidly (both absolutely and relative to the industry), clearly profitable, and reasonably valued relative to its own growth, other assets in cryptocurrency, and other assets in traditional finance. We continue to closely monitor these fundamentals, hoping our thesis will be validated.

Macro Catalysts

Several macro catalysts are on the horizon that could have a significant impact on the digital asset market.

Although institutional investment interest has waned over the past year, we are watching for upcoming events that may spark renewed interest among investors. Most importantly, the potential approval of a spot Bitcoin ETF. In particular, BlackRock's application is a significant event for two reasons. First, as the world's largest asset management company, BlackRock is under intense scrutiny and only makes decisions after careful consideration. Even amidst regulatory fog and the current market environment, BlackRock has chosen to continue increasing its investments in the digital asset industry. We believe this sends a signal to investors that cryptocurrency is a legitimate asset class with a lasting future. Second, we believe ETFs will increase exposure and demand for this asset class faster than most expect. Recent news indicates that the U.S. Court of Appeals supported Grayscale in its lawsuit against the SEC regarding the rejection of its spot Bitcoin ETF application last year. We believe this significantly increases the chances of approval for spot Bitcoin ETF applications from firms like BlackRock, Fidelity, and others, potentially as early as mid-October.

While the regulatory environment is beginning to clarify, it may still be the biggest factor hindering market development, particularly for the prices of long-tail tokens. To some extent, the courts are starting to push back against the SEC's "enforcement regulation," which seems to be a counter to the SEC. In addition to the news about the Grayscale spot Bitcoin ETF, the court's support for Ripple in its case against the SEC is a positive interpretation that digital assets are not considered securities. This is an important event because it suggests that regulation of digital assets can and should be more nuanced. Clarity in regulation is essential for protecting consumers and for entrepreneurs who need appropriate frameworks and guidance to confidently create new applications and unleash innovation.

Finally, cryptocurrency is at what we call a "dial-up to broadband" moment. We have mentioned before in previous letters that cryptocurrency is at a stage similar to the internet 20 years ago. Ethereum scaling solutions like Arbitrum or Optimism are making significant progress, and we are seeing increased transaction speeds, reduced costs, and enhanced capabilities. Just as we cannot imagine how many new internet businesses were created after the internet transitioned from dial-up to broadband speeds, we believe the same will happen with cryptocurrency. In our view, we have yet to see the widespread application of new use cases brought about by this massive blockchain infrastructure and speed improvements.