Revealed: How "magical" the Indian crypto market is that made Coinbase falter

In New Delhi, the cryptocurrency industry is still in a state of instability and uncertainty.

In New Delhi, the cryptocurrency industry is still in a state of instability and uncertainty.Author: 0xAyA, Odaily Planet Daily

As more South Asian faces appear on the Crypto stage, projects like Matic and Frontier are also shining in the decentralized world. However, when researching the Indian crypto market, local practitioners and investors can be said to be "unfortunate." In New Delhi, the crypto industry remains in a state of instability.

The Plight of "Foreign Guests"

Recently, TechCrunch reported that Coinbase has notified its customers via email that it plans to stop providing trading services for Indian users. Coinbase informed users that it would cease services starting September 25 and advised them to withdraw funds from their accounts. Additionally, Coinbase has banned new user registrations from India.

However, it is understood that this notification only applies to customers who violate the trading platform's standards, not all Indian customers. A Coinbase spokesperson revealed in an email on September 8: "We are reaching out to inform you that we will stop all Coinbase retail services related to your account because we will disable access to retail accounts that no longer meet the updated platform standards." The spokesperson added that during a recent routine review of the platform's systems, some accounts that no longer met the updated standards may have been identified. Therefore, the platform will deactivate these accounts and allow customers to update their information at a later date.

Just over a year ago, Coinbase entered the South Asian market and has since faced ongoing regulatory challenges.

In April last year, Brian Armstrong ambitiously stated in a blog post that Coinbase planned to hire 1,000 employees in India's tech hub, aiming to quadruple its workforce in India by the end of 2022. However, just two months later, the Indian team contributed 8% to Coinbase's latest round of layoffs, and insiders revealed that hiring in the Indian market had been "paused."

In fact, the cumbersome and slow bureaucratic system and cultural mismatches have made Coinbase's journey into India less than smooth. The previously hired former Snapchat India executive Durgesh Kaushik left his position as Senior Director of Market Expansion just a few months after taking office, and Brian Armstrong's efforts to implement India's Unified Payments Interface (UPI) support have not materialized.

Life, Death, and Taxes

Coinbase's experience could be tentatively referred to as "not welcomed by foreign guests," but in comparison, local exchanges are faring even worse. In July 2022, India implemented new trading tax laws for centralized virtual digital assets (VDA), including:

(a) A fixed tax rate of 30% on profits from VDA exchanges starting April 1, 2022;

(b) A 1% Tax Deducted at Source (TDS) on transactions exceeding 10,000 rupees starting July 1, 2022;

(c) A prohibition on offsetting tax losses starting April 1, 2022.

This policy stance aims to achieve three goals: tracking the VDA transactions of Indian residents and their corresponding income sources; curbing speculation and trading of VDAs; and establishing safeguards for financial stability.

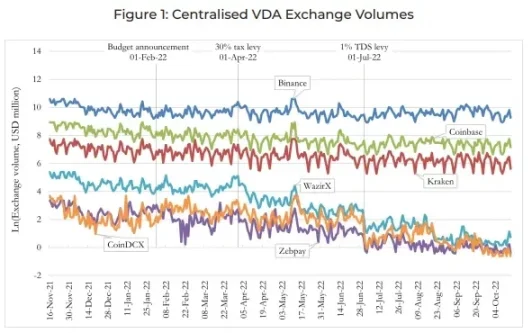

Although this move attempts to enhance the transparency of crypto assets and maintain macroeconomic stability, many experts believe that the current tax framework contradicts its original intent. The implementation of TDS has made Indian users reluctant to operate through local exchanges, preferring to choose "foreign guests." This is indeed the case, as the Indian think tank Esya compared local exchanges WazirX, CoinDCX, and Zebpay with overseas exchanges Binance, Coinbase, and Kraken in a report this year. The results showed that after the new tax policy was implemented, the trading volume of local exchanges plummeted.

Image source: Esya's survey report

Esya also provided its conclusions in the survey report:

(a) Compared to other countries with high VDA adoption, India's VDA tax policy is the most lethargic;

(b) The implementation of TDS has had the greatest impact, with trading volumes on Indian centralized VDA exchanges dropping by nearly 81% within four months of its imposition (from July to October 2022);

(c) Following these regulatory events, Indian investors have massively shifted from Indian centralized VDA exchanges to foreign exchanges (over 170,000 people from February to October 2022);

(d) Cumulative trading volume of nearly $38.52 billion flowed from Indian centralized VDA exchanges to foreign exchanges during the period from February to October 2022, with $30.55 billion transferred abroad within six months of the current fiscal year;

(e) The current tax framework will lead to a cumulative trade volume loss of $1.2 trillion over the next four years. We recommend strategies to mitigate these unintended adverse effects.

A Bloomberg report in September of that year stated: "Since India imposed a 1% TDS on crypto transactions in July, daily trading volumes on Indian crypto platforms have dropped by over 90%. Meanwhile, Binance's app downloads in India surged to 429,000, the highest this year, nearly three times that of the second-place CoinDCX, while FTX's downloads in India reached nearly 96,000."

Affected by this, CoinDCX recently announced layoffs due to revenue impacts from the prolonged bear market. A spokesperson stated that the trading platform would lay off 71 employees, claiming their roles no longer align with current business priorities. The company previously had around 590 employees, with multiple teams affected by the layoffs.

Despite benefiting from the policy, CZ also stated during a panel discussion at a fintech conference in Singapore that India's heavy taxation on crypto trading could "stifle the local crypto industry."

The Digital Rupee Dilemma

Compared to unregulated cryptocurrencies, the Indian government prefers to control a central bank digital currency (CBDC). On July 7, the Deputy Governor of the Reserve Bank of India, Sankar, stated that they hope to launch the CBDC in a measured and adjusted manner.

According to insiders, India aims to launch the digital rupee nationwide by the end of 2023. Last year, India initiated two CBDC pilot projects, one starting on November 1, 2022, called CBDC-W, with nine banks participating. The other, CBDC-R, launched on December 1, 2022, by the Reserve Bank of India (RBI), piloted in four cities with four banks involved. Each participating commercial bank will test the digital rupee among 10,000 to 50,000 users, and both customers and merchants must download a dedicated digital rupee wallet. CBDC-W is limited to financial institutions and aims to improve interbank payment efficiency, while CBDC-R is applicable to the private sector and Indian citizens. Although the government informed Parliament that India would release CBDC-R within the 2022-23 fiscal year, it remains unclear when it will be implemented.

The RBI is working with various banks to introduce new features to promote the digital rupee. New features include allowing customers to conduct digital rupee transactions offline and connecting it with UPI. The Reserve Bank of India has been urging banks to achieve interoperability between the digital rupee and UPI through QR codes, which will allow payments to be made via the widely used UPI QR codes. This functionality was announced in June this year and has been activated by major banks, including the State Bank of India, the largest bank in India.

However, currently, the average daily number of retail digital rupee transactions is about 18,000, far below the RBI's target of reaching an average of 1 million transactions per day by the end of 2023.

Conclusion

For local practitioners, the skies over New Delhi remain filled with clouds: an immature market, unclear regulatory policies, high taxes, corruption and inefficiency stemming from a bureaucratic system inherited from the British colonial era, and even the lingering effects of past Rug projects… With all these factors combined, it is not hard to understand why most practitioners prefer to "go abroad" to explore new opportunities.

At the recently concluded G20 summit, countries reached a consensus on the rapid implementation of a cross-border framework for crypto assets, which will promote global information exchange on crypto assets starting in 2027. Countries will automatically exchange information on crypto transactions across different jurisdictions each year, including transactions conducted on unregulated crypto exchanges and by wallet providers. Several countries, including Argentina, Australia, Brazil, the United States, China, and France, will be affected by this framework—of course, including India.

During this meeting, Indian Prime Minister Modi called for global cooperation to further develop cryptocurrency regulations and stated that as the G20 presidency, India is "willing to take on the task of advocating for the establishment of a comprehensive global cryptocurrency regulatory framework."

------ Although India itself does not even have a relatively comprehensive regulatory framework, it still chooses to "take strong measures."