Head Game Guilds in a Bear Market: Some Thrive While Others Quietly Fall Behind

The roller coaster of YGG prices over the past two weeks has refocused the market's attention on the gaming guild sector. This article will provide a comprehensive review of the gaming guild sector from four perspectives: business capability, investment capability, risk control capability, and valuation.

The roller coaster of YGG prices over the past two weeks has refocused the market's attention on the gaming guild sector. This article will provide a comprehensive review of the gaming guild sector from four perspectives: business capability, investment capability, risk control capability, and valuation.Author: Scarlett Wu, Mint Ventures

The rollercoaster ride of YGG's price over the past two weeks has refocused the market's attention on the gaming guild sector. At the beginning of the rise, I shared a summary from the treasury perspective on gaming guilds on Twitter titled "Comparison & Valuation Summary of Gaming Guild Treasuries: $YGG, $MC & $GF, Which Valuation is More Reasonable?" At that time, I was most optimistic about $MC, which has now risen by 50%, while YGG's price has rapidly fallen back to the level before the summary was written after doubling. This article is a revision and expansion of that summary, providing a comprehensive review of the gaming guild sector from four perspectives: business capability, investment capability, risk control capability, and valuation.

Many gaming guilds, quest platforms, gaming information aggregation platforms, and pay-later NFTfi protocols are essentially segments of the same service. This is because game developers have only three needs:

- User acquisition

- User engagement

- To further promote in-game consumption

Web3 players, on the other hand, have only two needs:

- A sense of companionship

Due to the demand for upfront capital investment brought by the Ponzi schemes from 2020 to early 2022 (for example, when Axie prices were over a thousand dollars, guilds purchased NFTs to rent to Southeast Asian players and took a cut from their subsequent earnings), and the wealth effect generated by the wildly inflated economic system, people mistakenly believed that the music of passing the parcel would never stop, giving rise to another important function of Web3 gaming guilds:

- Fronting capital

The premise for the need for companionship is that users will spend a sufficient amount of time on the game, which is something that all non-Ponzi Web3 games currently fail to meet. Moreover, if guilds invest in purchasing "shovel" NFTs to rent to users, they need a Web3 game with a continuously expanding economy—if the capital invested two weeks ago has already started to incur losses, any institution fronting capital would be on edge. The fact is, aside from the crypto game Ponzi pioneer Axie Infinity, there has not been a single game in the industry that has seen sustained user growth for over six months. Given that the premise of Ponzi profits is user growth, guilds willing to front capital need to spend two months finding a game that "can make money steadily," observe for another two months that "this game can indeed make money steadily," and after implementing the plan for two months, they will despairingly find that the fronted capital cannot be recovered because "scholars" (the term for players under the guild) may take ten years to break even.

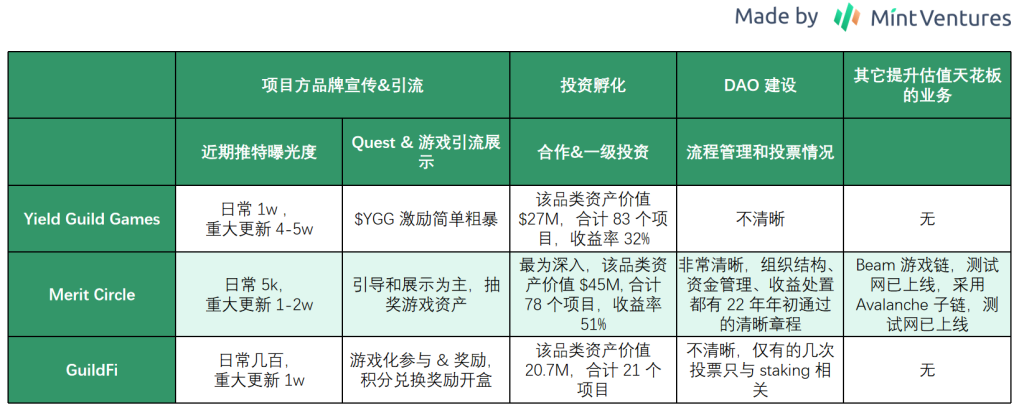

Guilds have clearly recognized this issue earlier. Under the reality that no Ponzi can replicate the heat of Axie, and that the demand for companionship from every game cannot be strong enough to charge fees through live streaming (the income source for traditional gaming guilds), guilds have shifted from "serving players" to "serving project parties": on one hand, guilds hold a large number of player resources (this point is now indeed questionable and will be discussed later), and on the other hand, guilds have a substantial amount of funds in their treasuries (although liquidity is likely questionable, which will also be discussed later), allowing them to enjoy the growth dividends of the Web3 gaming sector through investments. Of course, there are also entities like Merit Circle, which collaborates with Avalanche's subchain to enhance valuation imagination through the narrative of gaming public chains.

1. Business Data Comparison: YGG and MC are still active, GF has fallen behind in terms of visibility

Currently, the main traffic battlegrounds for major guilds are:

- Quest systems

- Discord

Among these, Discord can be quite deceptive; even with YGG's 70,000-member DC group chat, without hot games/tasks, the General Chat only sees a little over a hundred messages daily, half of which are "gm" and "hi," while the other half are links to Medium/official site responses to members' questions from the team.

Twitter, on the other hand, allows for a clearer view through engagement metrics. Even though YGG has 180,000 Twitter followers, Merit Circle has 100,000, and GuildFi has 120,000, YGG's Twitter content engagement remains stable at a few thousand to tens of thousands, with only major updates reaching 40,000 to 50,000 views; Merit Circle is slightly behind, with daily content engagement around 5,000, and major updates over 10,000; GuildFi is even more dismal, with regular updates barely reaching 1,000 views, and semi-annual reports only garnering 10,000 views. In comparison, my Twitter account with over 2,000 followers can easily achieve hundreds of views on casual tweets, and more in-depth summaries can reach tens of thousands of views—under the transparent data display of Twitter, the inflated data of gaming guilds has nowhere to hide.

The Quest system can also be explored from two aspects: project situation and incentive situation:

- YGG Guild Advancement Program: Recently, YGG launched the Guild Advancement Program Season 4, where players can complete tasks and upload proof to share in the corresponding task prize pool. Among these, Axie's rewards still dominate, with a single reward reaching up to 2,700 $YGG (approximately $900 at the current $YGG price), while rewards for other games range from 30 $YGG (about $10) to over 1,000 $YGG. For players still capable of competing for the Axie Infinity prize pool, the rewards offered by Axie are undoubtedly more attractive (worth tens of thousands of dollars), while for players of other crypto games, the prize pools to be shared with competitors, totaling tens to hundreds of dollars, are not very appealing. Rather than spending a lot of time completing low ROI tasks, it is better to use that time to chase airdrops. From the user's perspective, YGG's Quest System is unlikely to attract significant attention.

- From the project party's perspective, YGG's collaboration with games will likely receive cash or other game assets, while the rewards given to players are valued in $YGG, which is essentially YGG exchanging its tokens for other cash/game assets.

https://www.yieldguild.io/gap/season-4

https://www.yieldguild.io/gap/season-4

- Merit Circle Gaming:

- Compared to YGG's straightforward task system, Merit Circle Gaming offers a more user-friendly interface. This incentive system's official site is divided into four parts: homepage (highlighting game introductions and activity timelines), games (showcasing key games and summarizing related information), academy (game tutorials and basic Web3 operation teaching), and task system (completing tasks for experience and game NFT lottery rewards).

- In YGG's Quest system, players can have a more straightforward ROI calculation (though the ROI is low, it still holds some appeal for the Southeast Asian demographic), while Merit Circle's Quest system leans more towards information aggregation and game showcasing, with task rewards mostly distributed through lotteries.

Merit Circle -- Homepage

Merit Circle -- Homepage

Merit Circle -- Key Game Display

Merit Circle -- Key Game Display

Merit Circle -- Academy

Merit Circle -- Academy

Merit Circle -- Task Reward System

Merit Circle -- Task Reward System

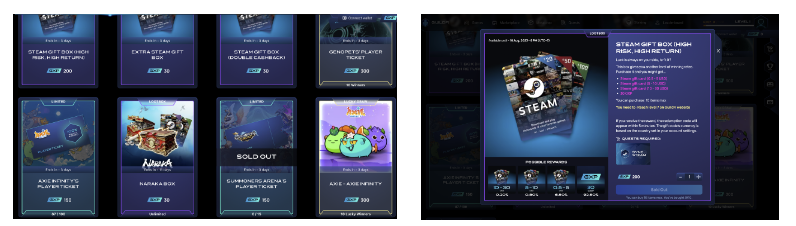

- GuildFi Quest & Achievements

- GuildFi has created a task & achievement system using in-game points, where players earn corresponding points for completing tasks and achievements.

GuildFi Quest & Achievements

GuildFi Quest & Achievements

Points can be redeemed for gift cards, game tickets, whitelists, treasure chests, NFTs, etc. However, currently, the products that can be redeemed with GuildFi experience are quite limited, mainly consisting of Steam gift cards (with a probability of obtaining gift cards worth $0.5 to $30, and possibly a 15% cost refund), Genopet and Axie game tickets, Axie NFTs, and CyBall NFTs (distributed through limited-time lotteries). This lottery blind box redemption model for Steam gift cards/game items has already been widely used in traditional game information aggregation and casual gaming platforms. On one hand, they collaborate with game developers to distribute game assets (though it can be seen that GuildFi's BD capabilities are quite limited, collaborating only with older projects), and on the other hand, they directly convert a small portion of their income into assets that players already value, gamifying the process to mitigate inflation.

GuildFi Marketplace

GuildFi Marketplace

In GuildFi's semi-annual summary, they stated, "In the past year (second half of 2022 - first half of 2023), the platform's purchase volume exceeded 200,000 times, a 42% increase from the previous year, indicating that our community's enthusiasm for the gaming products on our platform is rising. Notably, the Lootbox event for Diablo IV achieved over 65,000 purchases, while the KOF Lootbox surpassed 30,000 purchases." Under such collaborations, GuildFi brought a total of 92,000 pre-registrations for 21 partners over the year—averaging less than 5,000 registrations per game—considering that pre-registration usually does not require wallet interactions, it is easy for opportunists to create multiple accounts on decent projects, making the actual number of effective users even more concerning.

Source: GF Semi-Annual Summary

Source: GF Semi-Annual Summary

Combining the above, it is not difficult to see that the energy of gaming guilds in the market has significantly diminished, with YGG and Merit Circle remaining relatively active, while GuildFi has fallen behind in terms of business resources and content output.

2. Financial Situation Comparison: MC has balanced financial and business development, YGG has strong business capability but lacks financial strength, GF's market value is less than the value of its blue-chip and stablecoin assets

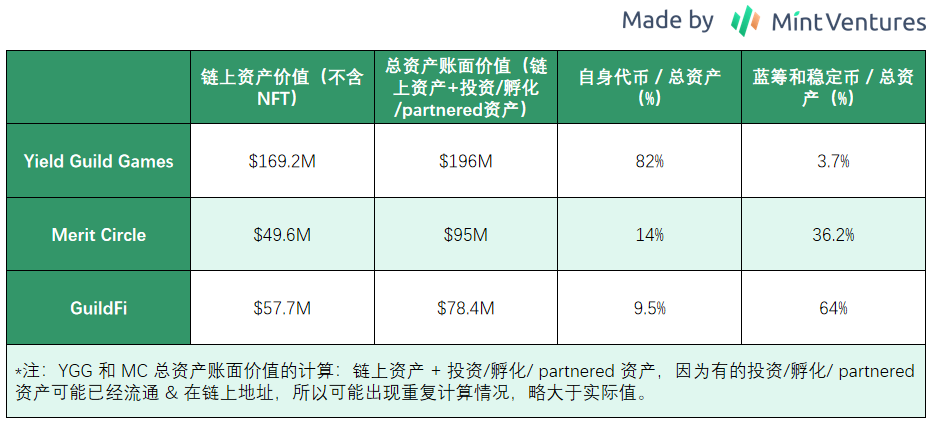

YGG: Gaming dissemination platform + gaming investment fund, treasury is almost entirely in YGG, with less than 4.4% in high liquidity assets

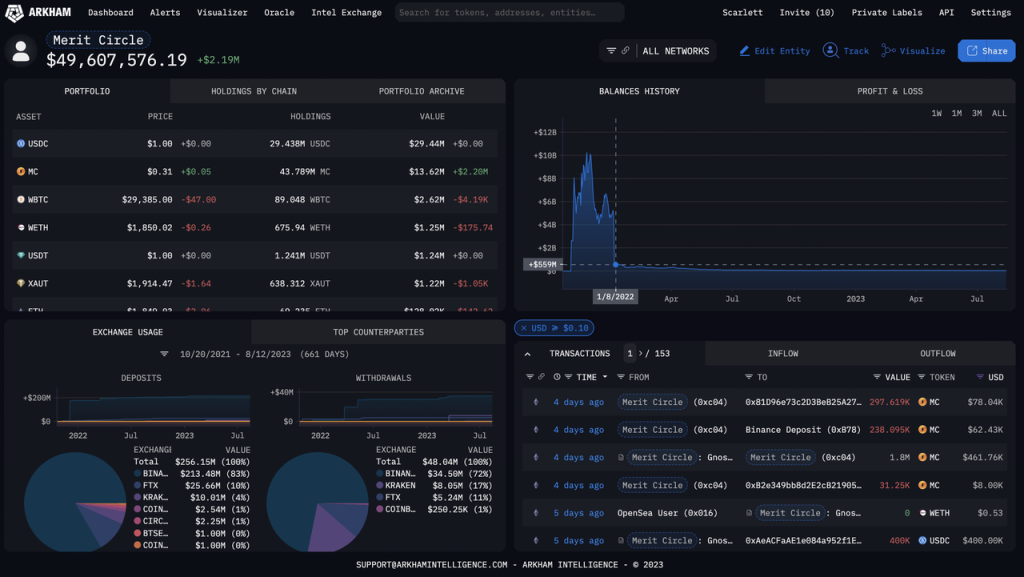

Due to the significant depreciation and poor liquidity of gaming NFTs currently on the market, we can directly estimate the situation of project party treasuries from FT. According to the address publicly disclosed by YGG, 95% of YGG's on-chain treasury consists of its own token $YGG, with less than 4.4% in high liquidity stablecoins and blue-chip assets ($USDC / $USDT / $ETH, etc.), indicating a highly imbalanced asset allocation.

YGG Treasury Address Asset Situation Arkham, Mint Ventures Chart

YGG Treasury Address Asset Situation Arkham, Mint Ventures Chart

Excludes assets on non-EVM chains, which amount to approximately $220,000 and can be ignored in calculations.

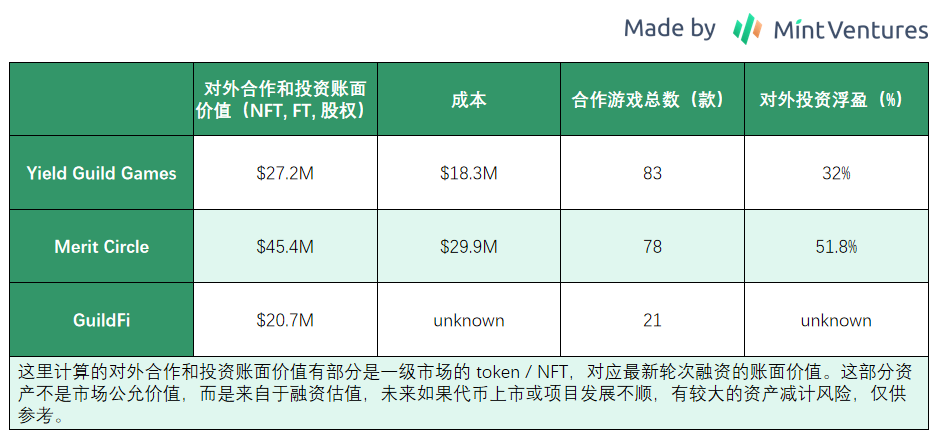

Additionally, in the 2023 Q2 Community Update released by YGG in early August, they provided a valuation of the assets from investment/collaboration projects: YGG holds a total of $27.2M worth of gaming assets (NFTs, tokens, equity, etc.), with a corresponding cost of $18.3M, showing a paper profit of 32%.

Source: YGG Medium

Although YGG has been relatively candid about the market price declines of Gaming NFTs, the valuations of tokens/NFTs in the Games section may have some inflated calculations: even if YGG secured good prices at the time of investment, under the current market conditions, the on-paper value of primary investment game tokens is likely to plummet after listing, and in the current situation of extremely poor NFT liquidity, attempting to liquidate NFTs will require significant discounts. The same situation applies to Merit Circle and GuildFi.

YGG Partnered Games (held assets, including primary investments and secondary market purchases, chainplay.gg incomplete statistics)

YGG Partnered Games (held assets, including primary investments and secondary market purchases, chainplay.gg incomplete statistics)

Merit Circle: Steady business development, best balanced treasury funds, stable income and high-risk assets split evenly

Merit Circle (hereinafter referred to as MC) defines itself on its official website as a Gaming DAO with four functions: investment, game studio, reward system, and infrastructure (building a gaming chain Beam through Avalanche's subchain). In terms of communication transparency, MC is also superior to the other two guilds: the treasury fund dashboard is updated in a timely manner, containing not only on-chain verifiable FT/NFT data but also disclosing non-liquid assets like primary investments. Here, we mainly analyze two parts: the situation of investment and incubation, and the allocation of treasury funds.

Merit Circle Official Website

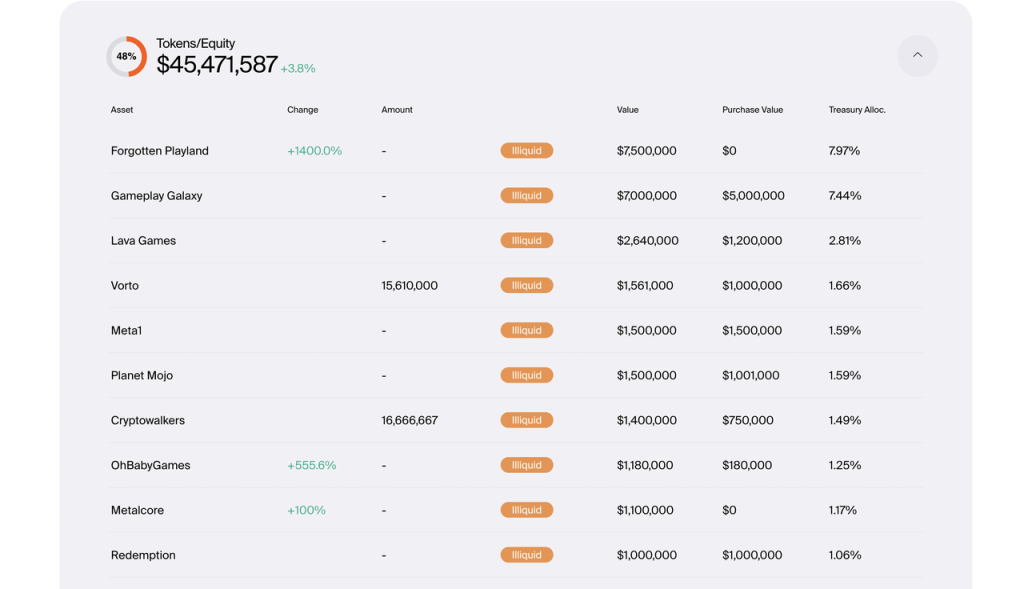

First, looking at investment and incubation, according to the publicly available data from MC's treasury, as of June 2023, MC holds equity/tokens from 79 gaming projects, including several large projects with good team backgrounds and financing backgrounds such as OhBabyGames and Xterio. The value of these assets is $45.4M, of which $1.6M is publicly tradable, while 43.8M is non-liquid assets, and 0.3M is $MC. Additionally, based on the disclosed purchase prices, the total cost of these assets is $29.9M, showing a paper profit of 51.8%.

https://treasury.meritcircle.io/treasury MC investment project incomplete screenshot

Moreover, the quality of on-chain treasury funds is also significantly stronger in MC than in YGG, with only 27.4% of its funds being its own token $MC, while 69.5% consists of high liquidity stablecoins and mainstream assets.

Merit Circle Treasury Address Asset Situation, Arkham, Mint Ventures Chart

Merit Circle Treasury Address Asset Situation, Arkham, Mint Ventures Chart

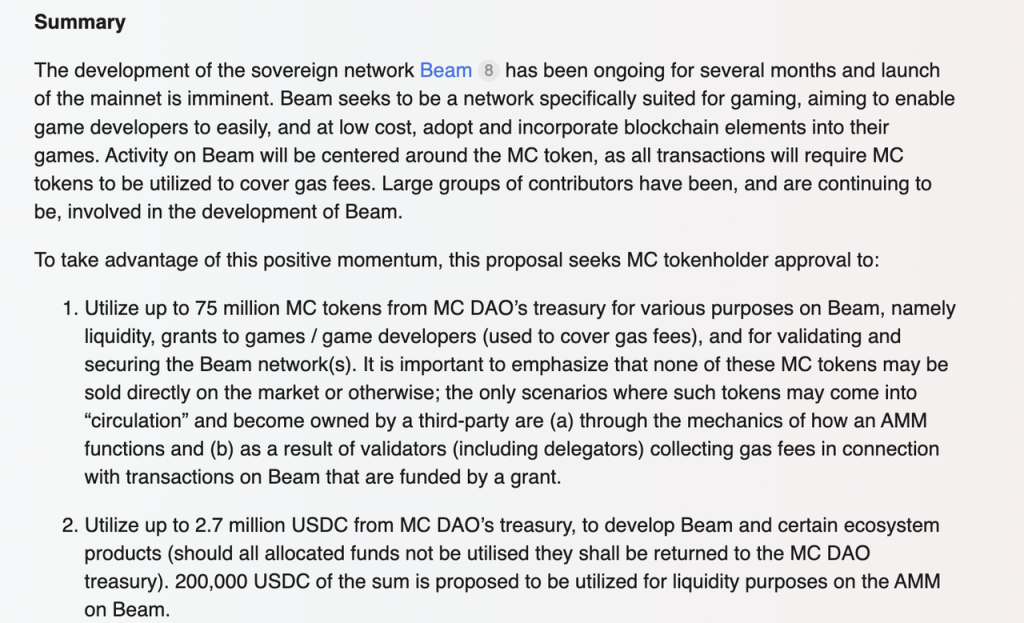

Additionally, MC has launched the testnet for the Avalanche subchain Beam, which is also an important event for future trends. Beam will adopt a Proof of Stake model, using $MC as the gas token, and will utilize LayerZero as the cross-chain infrastructure. Currently, three games are being developed based on Beam. On August 14, the team proposed a draft in the community governance section and opened it for discussion:

https://gov.meritcircle.io/t/beam-development-and-ecosystem-funding/822

https://gov.meritcircle.io/t/beam-development-and-ecosystem-funding/822

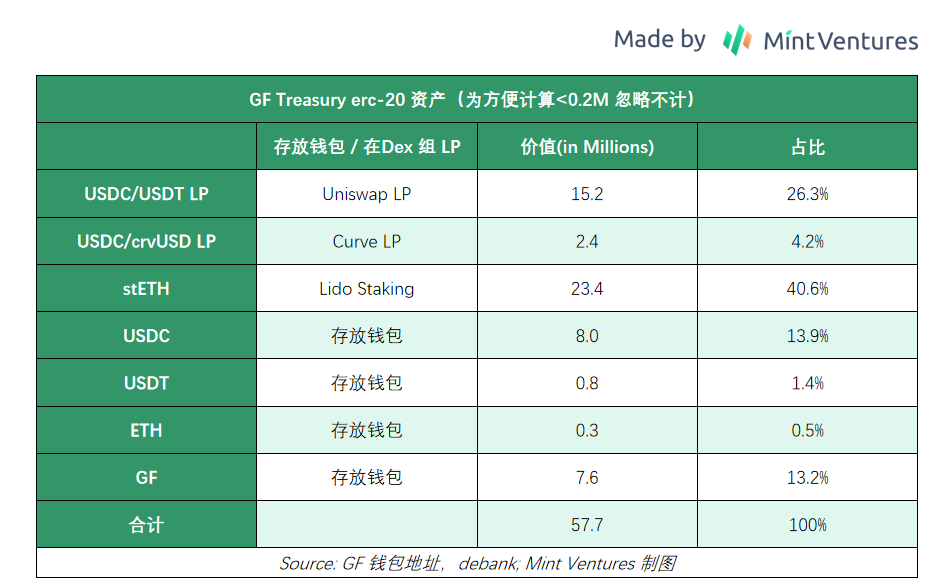

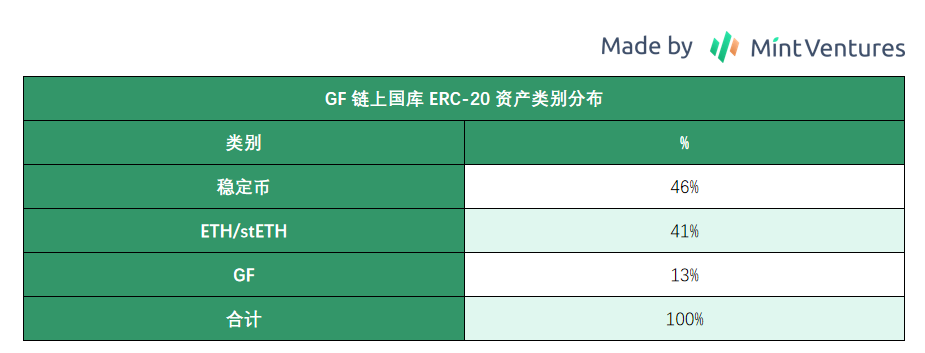

GuildFi: Weaker business capability, better balanced on-chain treasury funds, 13% GF, 46% stablecoins, 41% stETH seeking stable returns

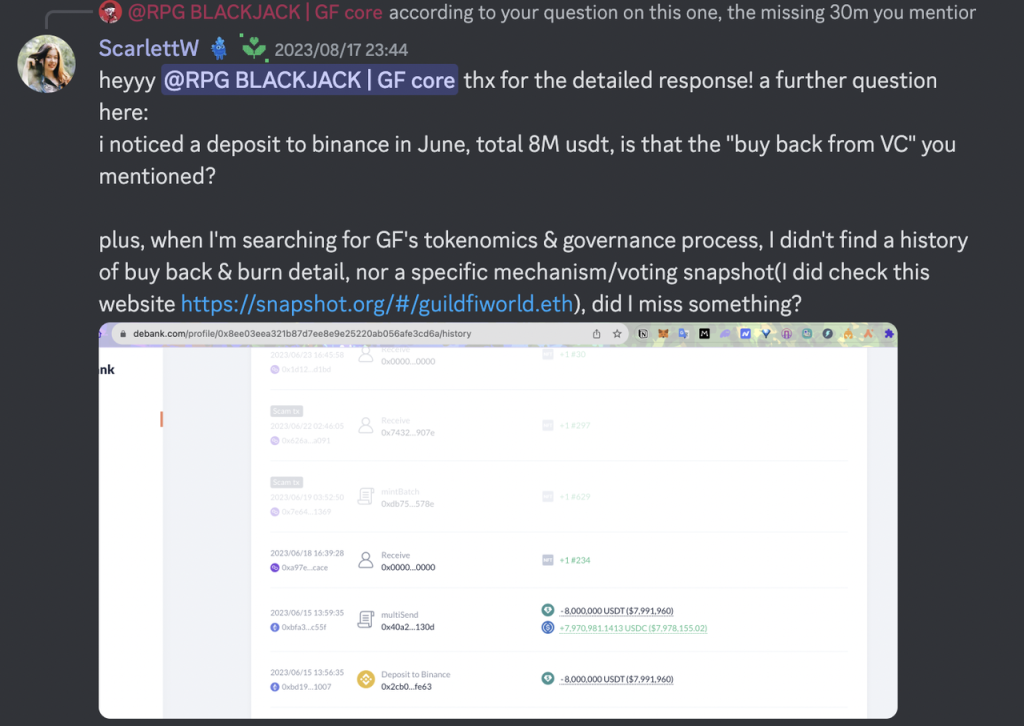

Due to many of GF's assets being used for LP on Uniswap, it is difficult to directly display them through Arkham. The following chart shows the on-chain asset statistics of the publicly disclosed wallet's ERC-20 assets: it can be seen that GF's on-chain treasury consists of 46% stablecoins, 41% ETH/stETH, 13% GF, and some small investments in gaming-related tokens, totaling $57.7M.

Compared to GF's semi-annual financial summary data, the official on-chain assets have shrunk by 19% from $71M at the time of the summary release, mainly due to token price declines and the transfer of $8M USDT to Binance. The official team stated that the assets stored in CEX are mainly used for daily operations and repurchases from investors.

Source: Debank

Source: GuildFi

Source: GuildFi

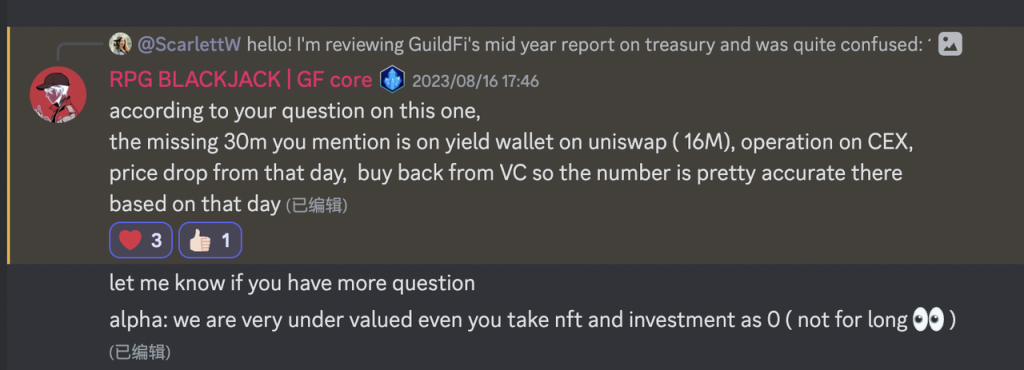

However, when further asked "Is there a public repurchase mechanism & repurchase history?", aside from a two-day "please be patient," no reasonable answer was provided.

Discord Q&A Record

Discord Q&A Record

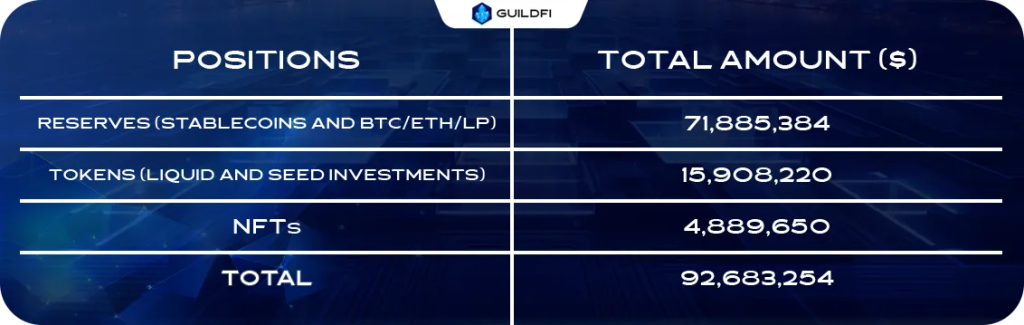

In the semi-annual summary, in addition to the $71M in assets in the Reserve (currently totaling $57.7M on-chain), there are also $15.9M worth of primary market investments and other game tokens, as well as $4.8M worth of NFTs.

GF Partnered Games

GF Partnered Games

3. DAO Construction and Governance Capability Comparison: Merit Circle Far Surpasses Competitors

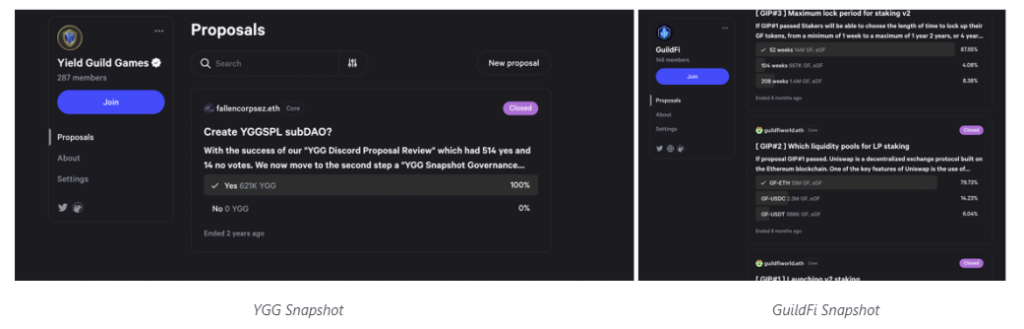

Although both YGG and GuildFi expressed in their white papers released in 2021 that the ultimate goal of this gaming guild is to become a Gaming DAO, in reality, it is Merit Circle that has truly achieved this goal.

Opening YGG and GuildFi's Snapshot, we can only see a few long-standing votes:

- YGG: A proposal for SubDAO two years ago.

- GuildFi: Three proposals and details about the launch of the Staking System eight months ago.

In contrast, Merit Circle shows users how a well-operating, risk-aware Gaming DAO/Investment DAO should function: over the past two years, Merit Circle's Snapshot has had 26 proposal votes, covering DAO governance, investment risk management (authorization mechanisms for exits and investment amounts), game development, etc. Notable proposals include:

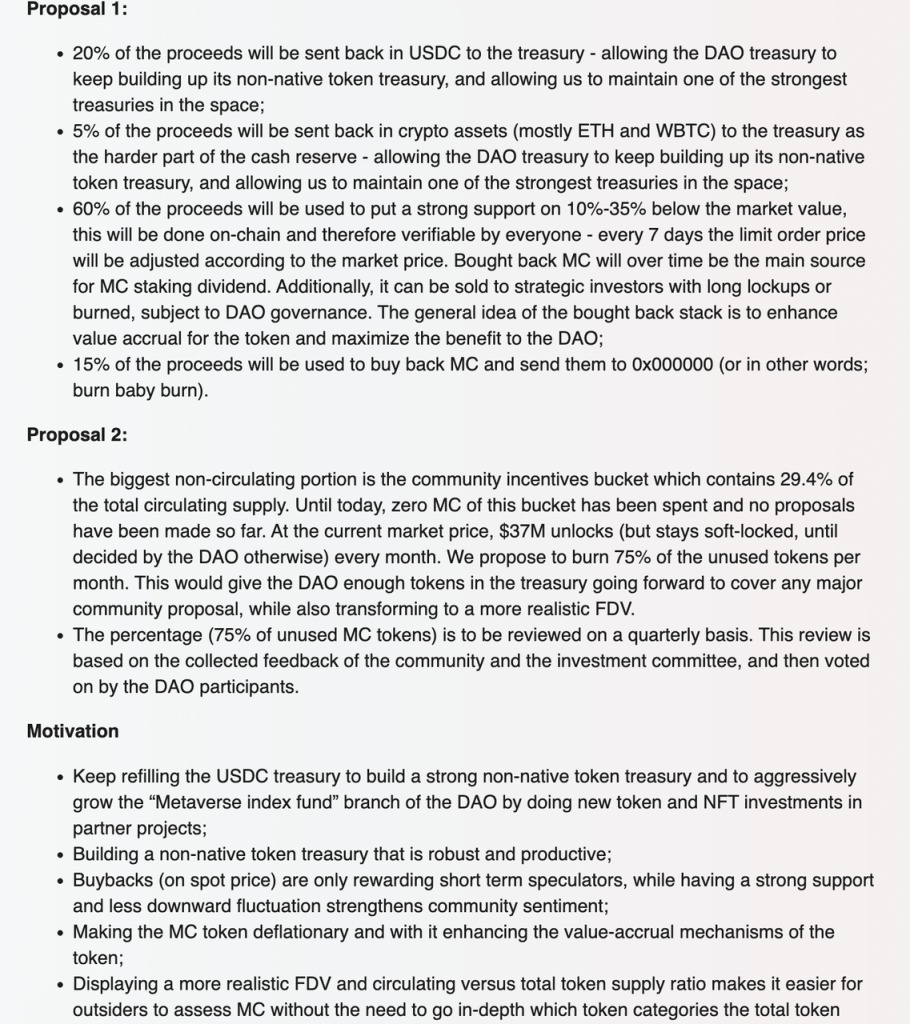

- 2022.01 MIP-7, determining profit distribution and token destruction. 20% of profits are kept in the treasury in the form of $USDC, 5% in $ETH/$WBTC, 60% are used for low-price repurchases at appropriate times to maintain token price stability (repurchases occur when below 10-35% of the 7-day average price, with this $MC mainly entering staking rewards, and can also be sold to strategic investors willing to lock in for the long term), and 15% of profits are used for direct repurchase and destruction of $MC. Additionally, since most token unlocks are released for "community incentives," it was decided to destroy 75% of the unlocked "community incentive" tokens monthly (the ratio can be modified by community vote). This provides enough tokens for the DAO's financial treasury to cover any major community proposals, transforming mCap into a more realistic FDV. It is hard not to be impressed by the foresight of $MC and the calmness in the face of great temptation—actively destroying 75% of the tokens released to the community is not an easy decision, and the completeness of the mechanism is the foundation of the balance in $MC's treasury funds.

$MC Repurchase and Destruction Announcement https://treasury.meritcircle.io/

$MC Repurchase and Destruction Announcement https://treasury.meritcircle.io/

https://gov.meritcircle.io/t/mip-7-sustainable-future-vision/192

https://gov.meritcircle.io/t/mip-7-sustainable-future-vision/192

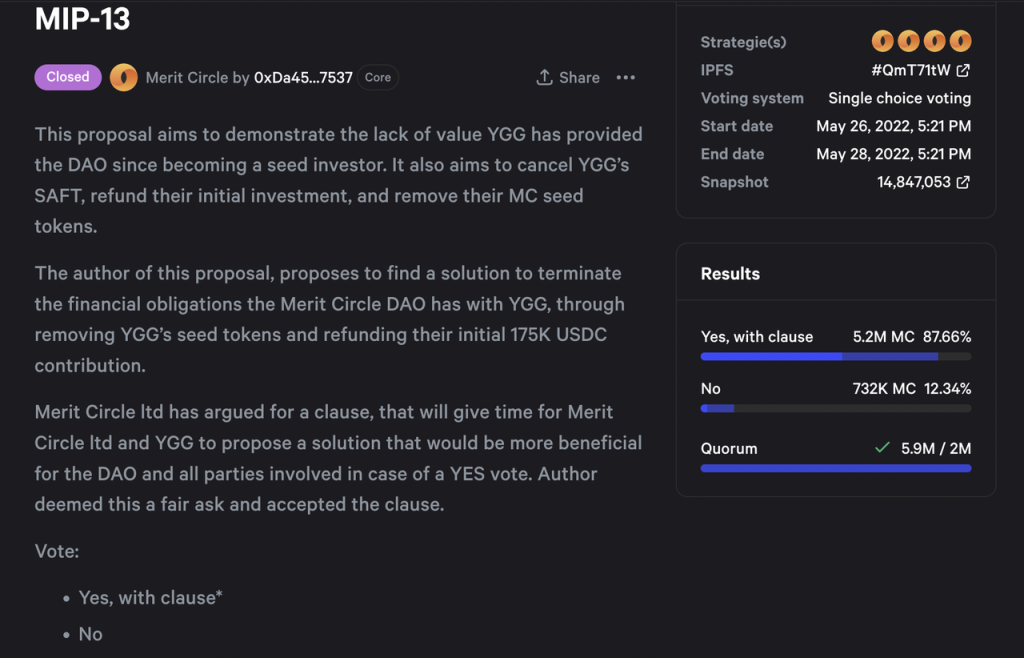

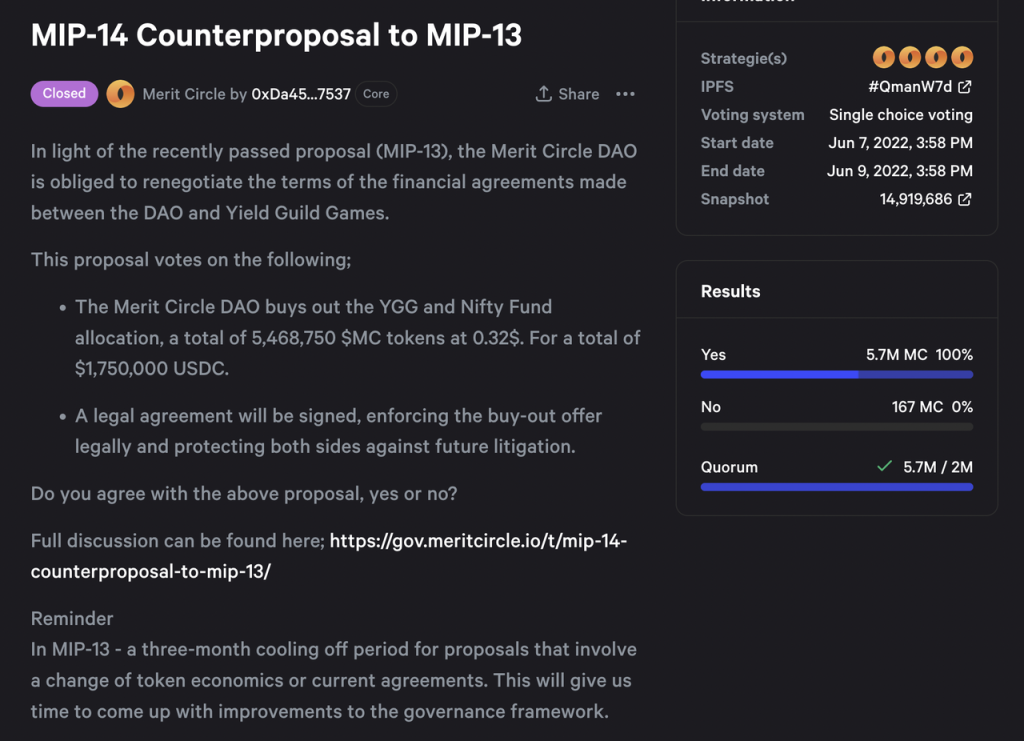

- 2022.05-06 Returning YGG's investment. Dissolving relationships with investors who provide no substantial help.

https://snapshot.org/#/meritcircle.eth/proposal/QmT71tWtTwk6q5Cd2kvhoLzxm76SpNaQGBR9RE7pCxBM58

https://snapshot.org/#/meritcircle.eth/proposal/QmT71tWtTwk6q5Cd2kvhoLzxm76SpNaQGBR9RE7pCxBM58

https://snapshot.org/#/meritcircle.eth/proposal/QmanW7dTyF2LvvU9iAGwj3i9D4F3TS7ZbxR33jVCmKMrgR

https://snapshot.org/#/meritcircle.eth/proposal/QmanW7dTyF2LvvU9iAGwj3i9D4F3TS7ZbxR33jVCmKMrgR

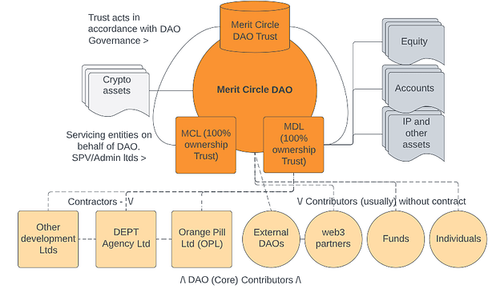

- 2022.07 Restructuring of DAO architecture.

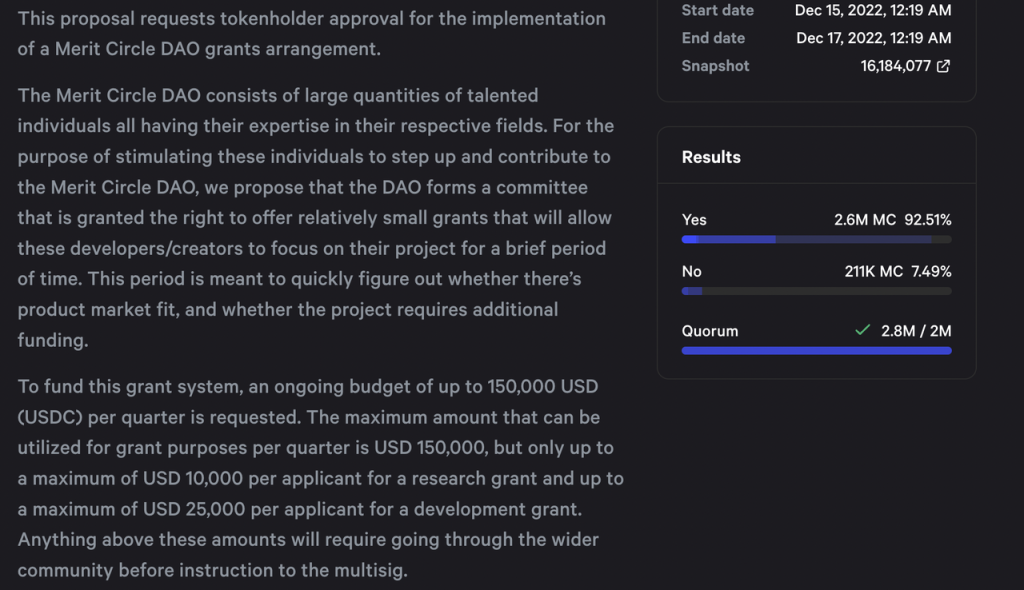

- 2022.12 Proposal for Merit Circle Grants. Allocating $150k quarterly for small incentive research and game development, with Research Grants capped at $10k and Development Grants capped at $25k.

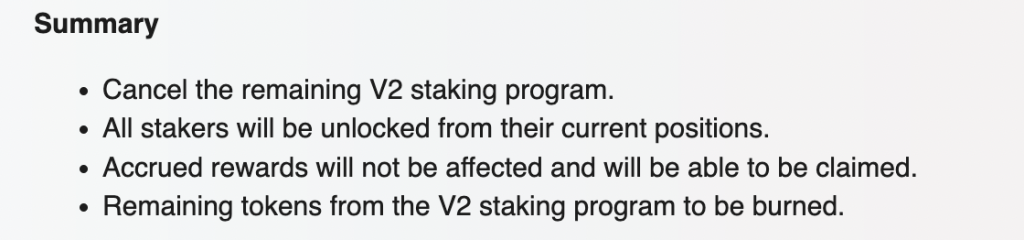

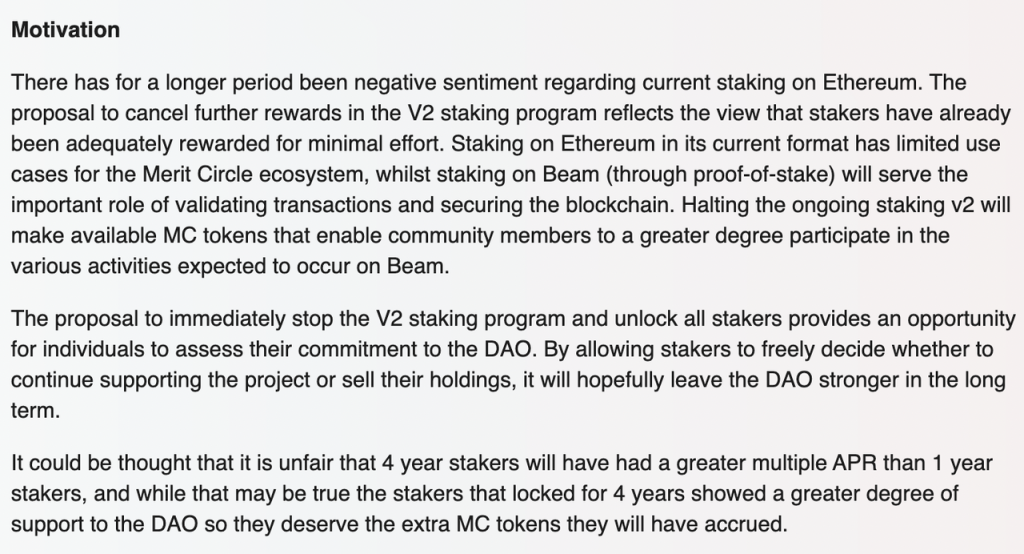

- 2023.07 Canceling future Staking rewards for Uni V2 and destroying this portion of future rewards. This decision was mainly based on the consideration that the existing Staking model would not bring much benefit to Merit Circle, while future staking on Beam (the game chain MC intends to build, proof-of-stake) has a clear use case, thus canceling V2 rewards and concentrating future staking rewards on Beam.

https://gov.meritcircle.io/t/mip-26-cancel-all-future-v2-v3-staking-rewards-and-unlock-all-v2-stakers-proposal/803

https://gov.meritcircle.io/t/mip-26-cancel-all-future-v2-v3-staking-rewards-and-unlock-all-v2-stakers-proposal/803

From the analysis of several proposals, it can be seen that although the proposers are mainly the team and the number of voters is not large (basically around 5M $MC), Merit Circle's team has a very clear strategic vision, willing to sacrifice short-term benefits to maintain the long-term interests of the community, and governance is relatively transparent.

4. Summary Comparison: Business Capability, Investment Capability, Risk Control Capability, and Market Value Comparison

4.1 Business Capability: MC has a more diversified business, YGG has a broader user base, GF has fallen behind

Additionally, from an organizational structure perspective, YGG's model is a product of the Axie era—YGG has regional sub DAOs extending from it, facilitating regional member access and management, and lacks an up-to-date risk control system. In contrast, Merit Circle resembles a large gaming company, excelling in investment (with a complete risk control system), incubation, promotion, and infrastructure across various dimensions. GuildFi's investment capability and market activity are inferior to the first two.

4.2 External Cooperation and Investment Capability: MC ranks first, YGG second in scale and yield, GF is the smallest in scale with unknown yield

4.3 Risk Control Capability: MC ranks first, GF second, YGG performs poorly

The evaluation criteria for this section are twofold:

- Whether the team's trading, management, and control of assets are transparent and comply with pre-established mechanisms; in this regard, MC >> GF/YGG

- The impact of asset tokens on the total asset price; if the proportion of "own token/total assets" is too high, it indicates poor risk control capability. Position management ranks GF > MC > YGG.

Overall, MC ranks first, GF second, and YGG performs poorly.

4.4 Valuation Comparison: $MC has entered a high position, $YGG is returning to normal, $GF's weak business leads to a market value < value of treasury stablecoins + blue-chip total value

Due to the nature of guilds' business, the treasury assets of projects can partially reflect business conditions. As mentioned earlier, the core functions of guilds currently are:

- Serving game developers based on the players they have

- Investment and incubation

These functions correspond to project assets, with part entering the value of external cooperation and investment (NFTs, FTs, equity), and part possibly converted into stablecoins and blue-chip assets remaining in the treasury. Therefore, comparing treasury assets can partially reflect the valuation situation of guild projects.

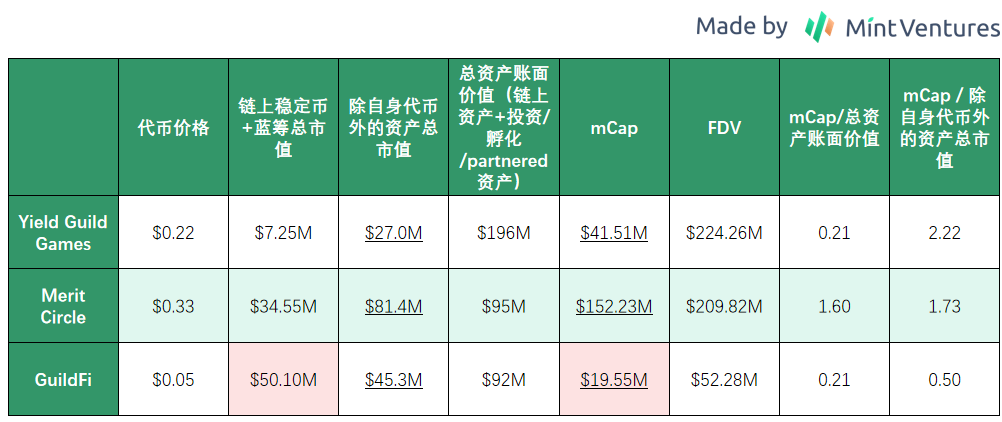

Before the recent surge of $YGG, its daily trading volume was only a few million dollars, with very limited liquidity. The proportion of $YGG in YGG's treasury is as high as 82%, meaning that any sell-off would have a devastating impact on the price. Therefore, we will compare both "mCap/total asset book value" and "mCap/total market value excluding own tokens" for objectivity. Considering all factors, the value support is $GF > $MC >= $YGG (note that both "total asset book value" and "total market value excluding own tokens" include "stablecoins + blue-chip" and "FT/NFT from investments/external cooperation," with the latter's valuation not being market fair value but derived from financing valuations, posing significant asset write-down risks if tokens are listed or projects develop poorly in the future. Furthermore, regarding "FT/NFT from investments/external cooperation," only Merit Circle has disclosed the costs and book values of all projects, while the other two have not provided specific calculation methods, which may also lead to statistical discrepancies.)

Since the unlocking of $MC is already more than half completed, but $YGG and $GF still have a large number of tokens locked, from the perspective of FDV/mCap, the potential downside risks are $YGG > $GF > $MC.

Aside from $MC having a clear token repurchase mechanism, the other projects lack such mechanisms, with GF having a staking mechanism with fixed reward release amounts, while YGG has no staking at all. Coupled with GuildFi's weakness in business aspects, even if $GF's market value is less than the total value of its on-chain stablecoins and blue-chip assets, it is difficult to conclude that it is "undervalued."

Looking at future upside, MC has the narrative of a gaming chain ahead, and the staking profit capture value of a POS chain is logical, while YGG's future plans involve launching a new Quest System on Base. GF currently lacks breakthroughs in business narratives.