The most likely area for short- to medium-term RWA to explode is the Web3 government bond business

In the short to medium term, the segment most likely to experience explosive growth in terms of scale and user base is government bond-related RWA.

In the short to medium term, the segment most likely to experience explosive growth in terms of scale and user base is government bond-related RWA.Author: Colin Lee, Mint Ventures

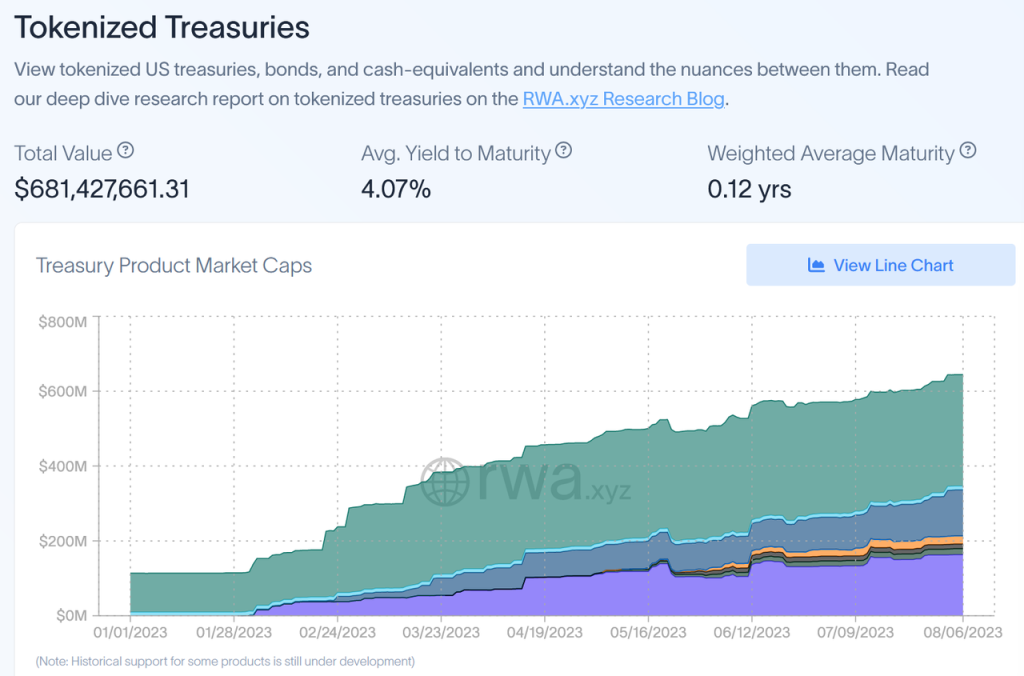

In the previous article, we mentioned that the subcategory of RWA most likely to experience explosive growth in scale and user base in the short to medium term is sovereign bond RWA. According to data from rwa.xyz, the current tokenized sovereign bond assets (excluding U.S. Treasury bonds in MakerDAO) have approached $700 million, representing a growth of approximately 240% since the beginning of the year. Additionally, the sovereign bond RWA in MakerDAO has also rapidly grown to several billion dollars. Overall, the growth rate of sovereign bond RWA is quite fast.

Source: https://app.rwa.xyz/treasuries

Source: https://app.rwa.xyz/treasuries

Based on the above industry background, we will analyze the mainstream sovereign bond RWAs in the market.

1. Significance of Sovereign Bond RWA

In previous discussions on how to define the native benchmark interest rate in the crypto world in the articles "How Should the Native Benchmark Interest Rate in the Crypto World Be Defined?" and "Outlook of the 'Native Bond Market' in the Crypto World", we explored the native benchmark interest rate and the potential bond market in the crypto world. We can roughly consider the PoS yield of public chains as the risk-free rate of public chains, around which a bond market may gradually develop.

However, even if a crypto-native bond market similar in scale to the current traditional bond market does not rapidly develop on-chain in the future, the emergence of "on-chain risk-free rate" LSD still holds significant importance for investors: investors using public chain tokens (such as ETH) as their accounting unit can still obtain low-risk returns in a bear market. From this perspective, some investment strategies from traditional markets can be more smoothly migrated to the crypto-native industry, such as the stock-bond balance strategy.

Sovereign bond RWA, like LSD, can introduce the risk-free rate from traditional financial markets into the on-chain world, allowing U-based investors to employ traditional allocation strategies. The benefits of this are several:

U-based investors still have a relatively safe and stable income-generating venue after the market turns bearish. For example, in the stablecoin market, after the market began to gradually turn bearish in mid-2021, the overall stablecoin market shrank from $188 billion to less than $130 billion today. The reduction in stablecoin scale has also affected the overall liquidity of the market.

Mixed stock-bond financial products are easier to launch and be accepted by the market, as mixed financial products are familiar to most investors in traditional markets. This will also promote innovation in the DeFi asset management sector.

Source: https://defillama.com/stablecoins

Source: https://defillama.com/stablecoins

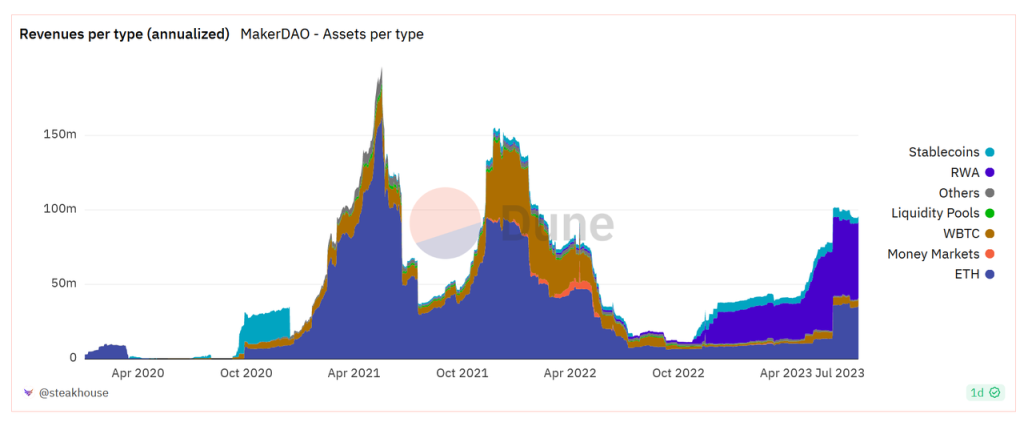

Currently, the most typical example is MakerDAO. After the market downturn and a significant increase in U.S. Treasury yields, MakerDAO incorporated U.S. Treasury bonds into its investment scope, leading to a substantial improvement in its profitability after entering 2023.

Source: https://dune.com/SebVentures/maker---accounting_1

Source: https://dune.com/SebVentures/maker---accounting_1

Therefore, it is reasonable to believe that other DeFi projects, upon seeing MakerDAO's "demonstration," will also hope to improve project profitability through more diversified strategies such as RWA. Especially in a bear market, RWA can provide a robust and sufficient source of income for the stable operation of projects.

2. Business Models of Sovereign Bond RWA

Currently, there are mainly five business models for sovereign bond RWA: agency model, platform model, infrastructure model, self-operated model, and hybrid model.

Agency model does not directly participate in the underlying asset packaging process or provide user KYC services, mainly acquiring customers through crypto-native methods, focusing on business marketing, capital acquisition, and the expansion of ecosystems and application scenarios. Representative projects include TProtocol, etc. This type of project is not different from the basic infrastructure used daily, such as Aave and Compound, often obtaining liquidity through the establishment of liquidity pools, then aggregating user funds, which are then lent out by a single borrower to purchase underlying assets like U.S. Treasury bonds.

Platform model means that the project only provides a series of service solutions such as on-chain, sales, KYC, etc., but does not personally engage in asset packaging. Representative projects include Desmo Labs, etc. This type of project generally provides three types of services: (1) asset/equity tokenization services; (2) on-chain verifiable information services; (3) user KYC services, etc. This type of project can theoretically assist in packaging any type of asset/equity from traditional markets, not limited to sovereign bond RWA, and is commercially closer to an internet platform model. To stand out in this track, the ease of use of the one-stop solution provided by the project must be considered, as well as the project's customer acquisition capabilities.

Infrastructure model provides services such as RWA on-chain, asset purchasing, and asset management, but does not directly interact with C-end/B-end users purchasing sovereign bonds. Representative projects include Centrifuge, Monetalis Group, etc.

Self-operated model means that the project itself seeks corresponding assets, establishes a business structure with external partners, ensures risk isolation of the assets, and tokenizes the assets/equities. Currently, there are many projects of this type, such as MakerDAO, Franklin OnChain U.S. Government Money Fund, Frax Finance, etc. This type of model is relatively more complex than the previous two models in terms of off-chain business, requiring investment in legal, corporate business structure establishment, and asset and partner selection. However, an important advantage of this type of project comes from this: the underlying assets are relatively controllable, and the project can actively manage risks.

Hybrid model can be a combination of the above four models. Projects of this type can provide corresponding services such as on-chain, KYC, etc., while also seeking assets themselves and directly providing corresponding investment opportunities to users. A representative of this type of project is Fortunafi. For example, Fortunafi provides four types of services: (1) Access Capital, which provides financing parties with funding acquisition pathways; (2) Earn Yield, where users can directly invest in already packaged assets after completing KYC; (3) Protocol Services, which provide governance, treasury management, and other services to other protocols; (4) whitelabeled products, which provide full-process services for RWA on-chain. Of course, the RWA services of this type of project are not limited to sovereign bonds and can also provide on-chain packaging services for other assets.

In addition to the above five models, there are also more purely trading infrastructure serving RWA, such as DigiFT, etc. However, these types of projects do not participate in the screening, on-chain, sales, and other processes of the underlying assets, so we will not elaborate further here.

3. Asset Side: Underlying Assets and Asset Architecture

3.1 Underlying Assets

Currently, there are several types in the market:

U.S. Treasury Bond ETFs. Projects using this type of underlying asset include Backed Finance, Swarm, MakerDAO, and ARKS Labs, etc. The advantage of this type of solution is its simplicity: the management of the underlying assets is entrusted to the ETF issuer and manager, including liquidity and bond rollover issues, which do not need to be managed directly by the project team. U.S. Treasury Bond ETFs have not encountered significant risk issues so far, so for these types of project teams, there is no particular concern about operational risks in asset management; they only need to include the largest and most liquid assets available in the market.

U.S. Treasury Bonds. Projects using this type of underlying asset include OpenEden, TrueFi, Matrixdock, etc. These types of projects often choose shorter-term U.S. Treasury bonds, which are also similar to cash in terms of liquidity. However, since the projects directly seek cooperative entrustors, they need to bear the risks associated with asset management, making it very important to select suitable partners.

A combination of U.S. Treasury Debt, U.S. Government Agency Debt, and cash/repurchase agreements. Projects using this type of underlying asset include Franklin OnChain U.S. Government Money Fund, Superstate Trust, TProtocol, Arca Labs, Maple Finance, etc. Similarly, these types of projects will delegate the management of the underlying assets to professional managers, and issues related to the renewal and liquidity of the underlying assets will be directly related to the project team. On the operational level, if the project team does not select sufficiently high-quality managers, problems may arise.

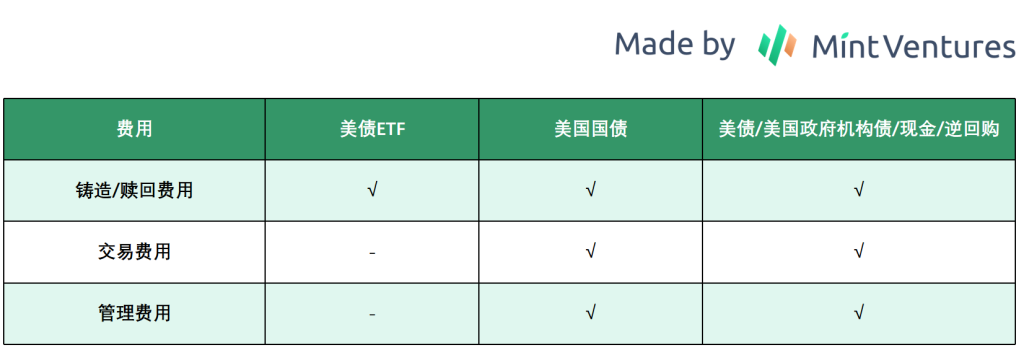

3.2 Fee Structure

The three types of underlying assets discussed above lead to different fee structures. Ignoring gas fees caused by on-chain transactions, the main fee rate structure is as follows:

Since the management of U.S. Treasury Bond ETFs is entrusted to ETF managers, the main fee issues arise from the minting and redemption processes, with fees typically ranging from 0.05% to 0.5%; the latter two involve management and transaction fees related to the underlying assets, with management costs around 0.3% to 0.5%, and transaction fees, such as bank transfer fees, around 0.2%.

Since the management of U.S. Treasury Bond ETFs is entrusted to ETF managers, the main fee issues arise from the minting and redemption processes, with fees typically ranging from 0.05% to 0.5%; the latter two involve management and transaction fees related to the underlying assets, with management costs around 0.3% to 0.5%, and transaction fees, such as bank transfer fees, around 0.2%.

3.3 Asset Business Architecture

The differences in underlying assets also affect the overall business logic architecture. Currently, there are several categories in the market:

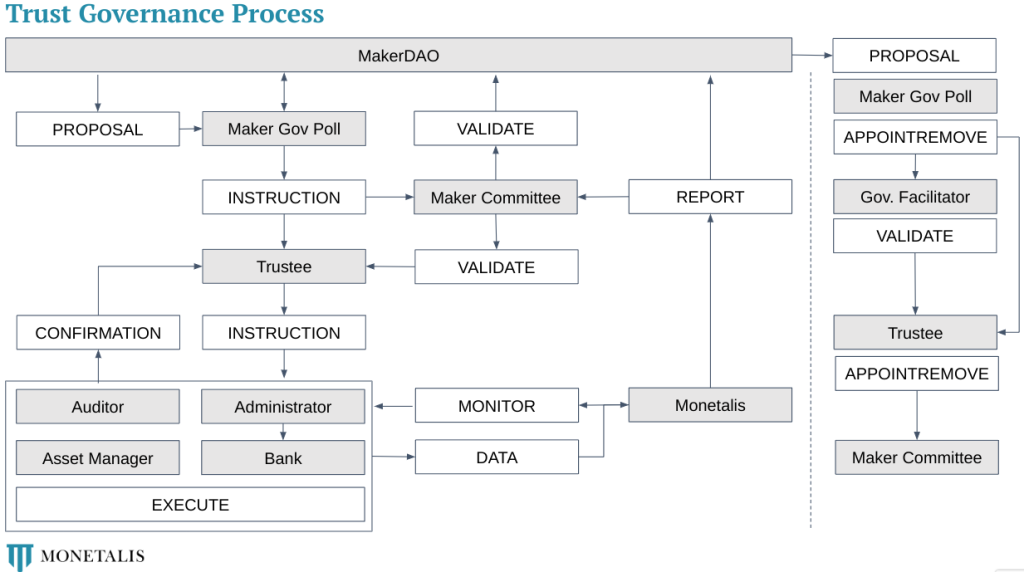

- Trust Structure: Projects using this solution include MakerDAO, etc.

Source: https://forum.makerdao.com/t/mip65-clydesdale-governance-framework-setup/16565

Source: https://forum.makerdao.com/t/mip65-clydesdale-governance-framework-setup/16565

The trust operation mechanism involves the initiator transferring assets to an SPV to establish a trust relationship, with the initiator obtaining the trust income rights, which are then transferred to ordinary investors. Taking MakerDAO's U.S. Treasury RWA structure as an example, it includes various roles such as managers and auditors, but part of the off-chain business structure is built by Monetalis Group. Corresponding asset purchases, periodic reporting, and on-chain processes are all completed by Monetalis Group. In this structure, MakerDAO influences details such as scale and underlying asset purchases through governance.

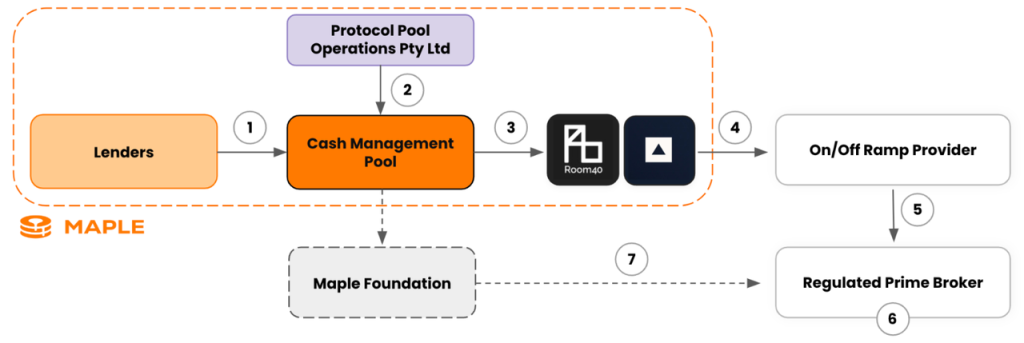

- Limited Partnership SPV Business Structure: Projects like Maple Finance and Matrixdock use this type of business structure. The project will participate in the process of finding assets and acquiring liquidity.

SPV, or "Special Purpose Vehicle," primarily functions to finance investors during the asset securitization/asset purchasing process. The original design purpose was to achieve bankruptcy risk isolation. Strictly speaking, the first type of trust structure can also be considered a type of SPV structure. The development of SPVs has matured, offering several advantages beyond bankruptcy risk isolation: (1) simplifying financial management processes, avoiding issues of excessive departmental involvement and unclear business flows in traditional corporate structures; (2) facilitating penetrative management, as typically, a single SPV corresponds to a single project/asset, which may avoid management issues. For example, in a commercial bank, it is challenging for investors to gain insight into the status of underlying assets because banks do not disclose many details, and such information may only be revealed at the internal management accounting level. For personal housing loans, the characteristics of such loans are not disclosed in external financial statements or annual reports, let alone specific information about individual debtors. However, if personal housing loans are packaged into an SPV, more detailed loan information must be disclosed, such as term, interest rate, collateral, loan amount, and sometimes even specific details about individual loans. In this way, the information provided by the SPV becomes much richer; (3) reducing taxes, as SPVs may have lower tax standards for certain underlying assets.

Source: https://downloads.eth.maple.finance/docs/legal/abe08ded-5d07-42cf-b435-a0d8d8156ca5/CashMngtT\&C.pdf

Source: https://downloads.eth.maple.finance/docs/legal/abe08ded-5d07-42cf-b435-a0d8d8156ca5/CashMngtT\&C.pdf

This business structure has two layers:

The first layer, users and SPV: what users receive is actually the debt rights of the SPV, and the guarantee of user returns depends on the SPV's ability to perform on time.

The second layer, SPV and commercial banks: the SPV will participate in the U.S. Treasury market and also engage in repurchase operations in the interbank market. In this process, if a repurchase agreement between banks defaults, it may carry greater risks than directly holding U.S. Treasury bonds.

Additionally, in this structure, users face an extra layer of risk: the SPV itself may also carry some risks.

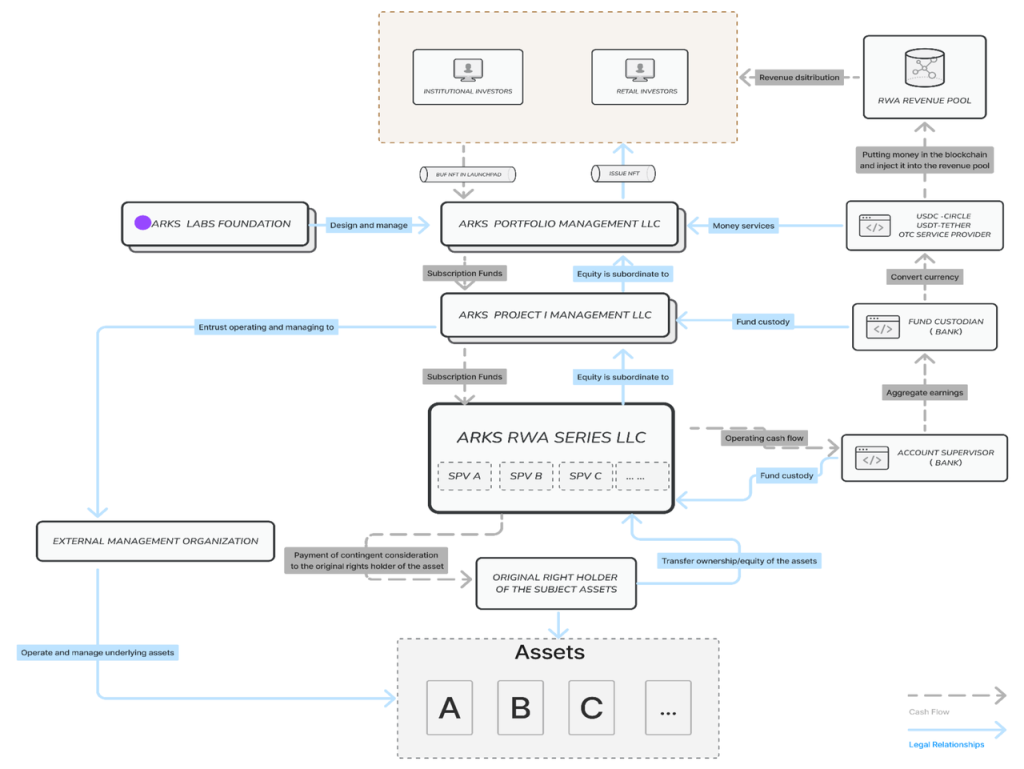

ARKS Labs has expanded the above business structure: embedding smaller SPVs within a larger business structure can achieve scalability, making it easier to operate when adding new underlying assets in the future. This is very similar to the structure of MakerDAO mentioned in the article "RWA Ramblings: Underlying Assets, Business Structure, and Development Path."

Source: ARKS Labs

Source: ARKS Labs

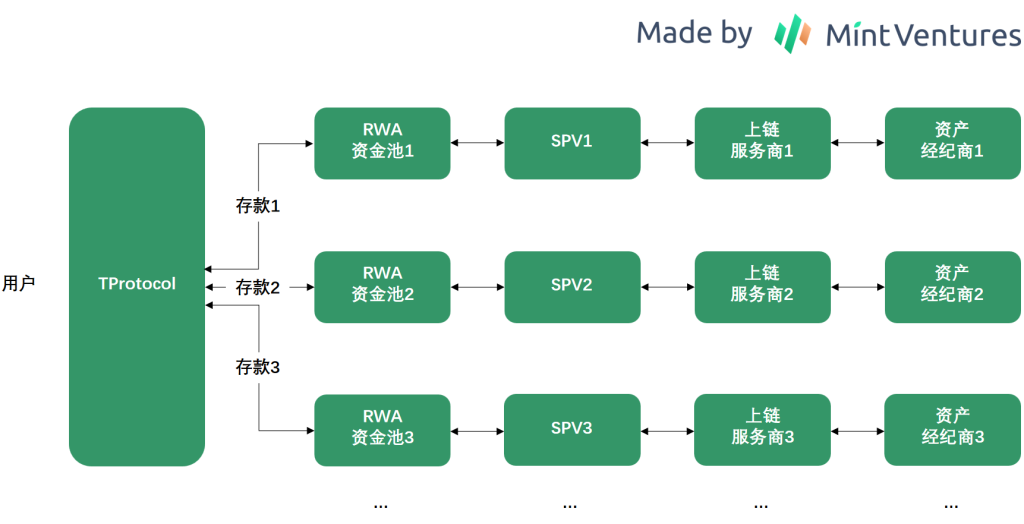

- Lending Platform + SPV Structure: Currently, TProtocol uses this type of business structure. The difference from the second type of SPV business structure mentioned above is that in the second type, one of the parties related to the SPV is the project party, which participates in the asset search and packaging process. In TProtocol, the SPV is not related to TProtocol but is the initiator of the RWA assets.

For example, the initiator of the SPV can be different institutions, and subsequent on-chain service providers and asset brokers can also differ. TProtocol's business structure is more flexible, but this does not come without costs: as the number of partners increases, the SPV's subsequent control, including the ability to inspect and manage service providers, may also decrease to some extent.

(4) On-chain Fund Shares: Similar to traditional fund purchasing strategies, detailed information about the purchasers must be known to correspond with addresses. Currently, Franklin OnChain U.S. Government Money Fund adopts this type of business structure. This type of project resembles what was previously referred to as "chain reform," where the project party puts off-chain assets and purchaser information on-chain, and future transfer information will also be recorded in a bookkeeping manner and subsequently documented on the blockchain.

(4) On-chain Fund Shares: Similar to traditional fund purchasing strategies, detailed information about the purchasers must be known to correspond with addresses. Currently, Franklin OnChain U.S. Government Money Fund adopts this type of business structure. This type of project resembles what was previously referred to as "chain reform," where the project party puts off-chain assets and purchaser information on-chain, and future transfer information will also be recorded in a bookkeeping manner and subsequently documented on the blockchain.

Although the RWA track is currently in its early stages, and user and capital scale do not impose high requirements on business architecture, as the value of sovereign bond RWA is gradually recognized by investors, the "scalability" of the architecture becomes very important. The ability to timely package new assets and connect with more off-chain service providers may be a decisive factor in the rapid development phase of the track.

4. User Side: KYC and Other Requirements

Due to the differences in underlying assets and business architecture, project parties have different requirements for the user side. Currently, the main differences exist in three aspects:

Minimum Investment Threshold: Projects led by MakerDAO, ARKS Labs, and TProtocol do not set limits on the minimum investment amount, while projects like Maple Finance, TrueFi, Arca Labs, and Backed Finance set clear minimum investment limits. "No minimum investment limit" is more in line with the current habits of DeFi users, while some projects with minimum investment amounts above $100,000 mainly target high-net-worth users.

KYC Requirements: Based on the difficulty of KYC, projects can be divided into three categories: no KYC projects, such as Flux Finance, ARKS Labs, and TProtocol; lightweight KYC, such as Desmo Labs, which only requires uploading passport information; and heavy KYC, such as OpenEden, Ondo Finance, Maple Finance, Matrixdock, etc., which require submission of KYC information comparable to traditional financial industries. A higher KYC threshold not only represents a barrier in traditional finance but is also hard for current DeFi users to accept.

Other Requirements: Some projects restrict their investors to certain regions, such as only serving non-U.S. users or only serving users outside the U.S., Singapore, and Hong Kong. Such restrictions are generally implemented by limiting IP addresses.

Some projects verify user requirements, such as KYC and regional restrictions, through third-party KYC service providers, and the project parties do not directly participate in the KYC review process.

5. Revenue Distribution Strategies and Composability

5.1 Revenue Distribution Strategies

Currently, there are mainly two revenue distribution strategies in the market:

The first strategy is the most common, which directly distributes through debt relationships. Regardless of whether users hold SPV debt rights or obtain U.S. Treasury ETFs or bonds through other structures, users can ultimately receive the vast majority of the income generated by the bonds. After deducting the earnings from minting and burning, as well as intermediary institutions, users can expect around 4 percentage points of net income.

This revenue distribution method is very similar to LSD: most of the staking income is returned to users, with only a small portion deducted as fees.

The second strategy currently only appears in the MakerDAO project, which uses a deposit interest rate model. Since users' funds do not directly correspond to the underlying assets, MakerDAO employs a model similar to commercial bank interest rate spreads: on the asset side, it invests in RWA and other relatively high-yield assets; on the liability side, it adjusts the yield obtained by users through DSR. So far, DSR has undergone four adjustments: (1) from 1% to 3.49%; (2) from 3.49% to 3.19%; (3) from 3.19% to 8%; (4) from 8% down to 5%.

This strategy provides the project team with greater flexibility, but the downside may be evident: users lack a clearer analytical framework for future yield expectations. Originally, with sovereign bond RWA, users would directly understand that they should receive returns close to the sovereign bond yield, but through monetary policy, such as MakerDAO recently distributing excess earnings to deposit users, the yield soared to 8%. If the number of deposit users increases sufficiently, the yield may drop back to levels near U.S. Treasury yields, which is not friendly for investors hoping for stable yield levels.

For the yield of sovereign bond RWA, clear "predictability" is very important; therefore, the first revenue distribution strategy may be superior to the second. However, once projects adopting the second strategy clearly anchor to sovereign bond yields, there may be no difference between the two in terms of yield.

5.2 Composability

Due to KYC requirements, the composability of sovereign bond RWA tokens has also shown differentiation:

Some projects with strict KYC qualifications, such as Ondo Finance, Matrixdock, Franklin OnChain U.S. Government Money Fund, etc., have whitelist restrictions on addresses, so even if there are corresponding token trading pools on-chain, users cannot trade freely without access. For these types of projects, unless they can scale the underlying assets sufficiently, it will be challenging to gain support from numerous DeFi projects and thus achieve richer composability.

Projects without KYC currently do not face composability difficulties; the only limitations on the composability of these projects are factors such as the project's business resources, BD capabilities, and the project's own scale.

6. Conclusion

By summarizing the above sovereign bond RWA projects, we can vaguely see the business models that may succeed in the short to medium term:

Underlying Assets: Using U.S. Treasury Bond ETFs may be a relatively clever approach, entrusting liquidity management and other issues to traditional financial giants. If directly purchasing U.S. Treasury bonds or mixed assets, it tests the project team's ability to select partners.

Business Architecture: There are already relatively mature models that can be applied, preferably with strong scalability to facilitate faster expansion and the future inclusion of new asset categories.

User Side: In the short to medium term, projects without KYC and minimum investment requirements will have a broader user base. If regulations eventually mandate KYC, lightweight KYC projects may become the mainstream solution.

Revenue Distribution: To ensure that investors in sovereign bond RWA have more stable and reassuring yield expectations, the best solution is for the yields provided to users to maintain a consistent ratio with sovereign bond yields.

Composability: Before regulations impose restrictions on access to on-chain RWA assets, expanding the use cases of sovereign bond RWA tokens as much as possible is an important factor for each project to achieve greater business scale in the medium to long term.

In the medium to long term, competition may increasingly intensify due to deeper regulatory involvement, and some lightweight KYC projects may have greater opportunities.