Loki's Sharp Review of DAI's 8% Deposit APY: A Calculated Conspiracy and the Twilight of the Gods for USDC

The vision of xDAI or XUSD is still far off, but attracting more real yields, maximizing capital efficiency, and separating the functions of earning interest and circulation will be an inevitable path for on-chain stablecoins. Along this path, the twilight of USDC and others can be faintly seen.

The vision of xDAI or XUSD is still far off, but attracting more real yields, maximizing capital efficiency, and separating the functions of earning interest and circulation will be an inevitable path for on-chain stablecoins. Along this path, the twilight of USDC and others can be faintly seen.Author: Loki, New Fire Technology

Editor: Link, Geek Web3

Introduction: Loki believes that MakerDAO's Spark Protocol adjustment of DAI deposit APY (DSR) to 8% is essentially compensating users for the opportunity cost of holding traditional assets like ETH and USDC. Meanwhile, emerging stablecoins like eUSD and DAI will continuously encroach on the market space of established stablecoins like USDC due to high interest rates. At the same time, the income-generating and circulating attributes of DAI can be separated to improve the capital utilization efficiency of MakerDAO's DSR.

I. Starting from the Growth of DAI

First, there is a question: Why does MakerDAO offer a high yield of 8% on DAI? The answer is clear—Maker hopes to relinquish its profits, actively providing arbitrage opportunities for users/markets, and achieve DAI's growth in scale through subsidies.

According to MakerBurn data, the supply of DAI has increased from 4.4 billion to 5.2 billion in the past four days. Clearly, this is driven directly by the 8% high interest rate of DAI.

This new demand is reflected in two ways:

1) Re-staking of LSD. Since DSR offers an 8% high APY for DAI, while the interest rate for minting DAI using wstETH is only 3.19%, this creates an arbitrage opportunity. If one stakes ETH and then uses wstETH as collateral to mint DAI and deposit it into Spark DSR, assuming a staking value of $200 in ETH to mint $100 DAI, the yield can be calculated as:

3.7% + (8% - 3.19%) / 200% = 6.18%

This is clearly better than direct staking and other low-risk yields available in the market, leading stETH holders to adopt this method for arbitrage, thus increasing the circulation of DAI.

2) Exchanging other stablecoins for DAI. So how can players without ETH or stETH participate? It's simple: use USDT/USDC to exchange for DAI and then deposit it into DSR. After all, 8% is attractive enough both on-chain and off-chain, and this demand requires more DAI to satisfy, indirectly boosting the circulation of DAI.

With the growth of DAI, the estimate from EDSR (Enhanced DAI Savings Rate) shows a net increase of 90M in Income from new DAI.

This means that as the circulation of DAI increases, the protocol will also hold more USDC, which can be used to exchange for more dollars, purchase more RWA assets, and provide more real returns, creating a flywheel effect.

II. Where is the Endpoint of Arbitrage?

The second question is, where is the endpoint of DAI's growth? The answer is when the arbitrage space shrinks to a sufficiently small size. To answer this question, one must understand that the essence of the EDSR (Enhanced DAI Savings Rate) mechanism is to actively provide users with arbitrage opportunities.

For users staking stETH/rETH, stETH/rETH has little use beyond being collateral for minting DAI. Therefore, as long as the EDSR rate is higher than the minting fee for DAI, there is profit to be made.

The situation for USDT/USDC users is more complex. Since USDC/USDT does not need to be collateralized to mint DAI, they can be directly exchanged for DAI on DEX. From the user's perspective, USDC held in AAVE can yield about 2%, while converting to DAI and depositing in DSR can yield 8%, which is attractive, leading to continuous exchanges by users.

Here arises a question: if Maker continues to exchange the USDT/USDC deposited by users for RWA (while keeping the DSR deposit rate stable), there should be a lower limit to the DSR yield, and this lower limit must be above the on-chain risk-free yield of USDC/USDT. This means that this type of arbitrage should be sustainable for a long time, and DAI will continuously absorb market share from USDT/USDC.

III. RWA Returns and the Commonality with On-chain Staking Stablecoins: Eroding Traditional Stablecoins

Of course, DAI's path to encroach on Tether/Circle's market share may not be so smooth, as DAI itself has some shortcomings (such as security issues with RWA) and is at a scale disadvantage. But let's not forget that DAI is not the only player trying to invade USDT/USDC; besides DAI, there are crvUSD, GHO, eUSD, and even Huobi and Bybit have launched their own RWA assets.

Here arises a divergence among stablecoin factions: where does the underlying yield come from?

One faction is represented by Huobi/Bybit, where the underlying yield comes entirely from RWA returns, needing to return the portion of profits taken from Tether/Circle back to users. The other faction consists of purely on-chain staking stablecoins like crvUSD and eUSD, where the underlying yield comes from collateral staking returns in other protocols (which may expand to more scenarios in the future, such as debt notes serving as collateral). DAI's model actually combines both sources of yield.

But all these types point to the same endpoint—reducing opportunity costs, or compensating users for their opportunity costs (for example, holding USDC is actually users relinquishing opportunity costs to Circle to invest in traditional assets like U.S. Treasuries).

If you choose to mint DAI using wstETH, you can still earn staking rewards; you have not sacrificed any of your APY; if you choose to mint eUSD using ETH, Lybra will charge a small fee, but most of the staking APY still belongs to you. However, when you use USD to purchase USDT/USDC, the 4%-5% RWA yield is taken by Tether/Circle.

Tether's net profit reached $1.48 billion in Q1 2023 alone. If DAI could completely replace Tether/Circle, it would bring $5-10 billion in real income to the cryptocurrency market each year. We often criticize cryptocurrencies for lacking real yield scenarios, but we overlook the biggest and simplest scenario—just returning the yields/opportunity costs that belong to currency holders. (For example, Spark can offer up to 8% DAI deposit rates, returning the opportunity costs incurred by dollar holders due to inflation back to users.)

In my view, whether to embrace RWA or detach from RWA, to insist on decentralization or to cater to regulation, these different choices may coexist, but the route of encroaching on the centralized stablecoin market share is clear. As long as the APY advantage of Spark or Lybra remains, the market share of USDC/USDT will continue to be eroded. In this regard, the stability of RWA collateral models is consistent with the stability of on-chain native collateral models.

IV. A More Efficient Future: Separating Income Generation and Circulation

MakerDAO's Spark DSR also has a problem: Entering DSR means exiting circulation, so the growth of circulation does not truly serve actual business but becomes a game of capital idling. Therefore, the question to consider is whether there is a better solution? My answer is to separate income generation and circulation.

The specific implementation is as follows:

(1) Separation of DAI's Income Generation Attribute

Currently, DAI deposited into Spark becomes sDAI, and the income generated by DSR accumulates on sDAI. For example, if you initially deposit 100 DAI and exchange it for 100 sDAI, as the DSR income accumulates, when you withdraw, you can exchange your 100 sDAI for 101 DAI, with the extra 1 DAI being your income.

The drawback of this mechanism is obvious: income generation and circulation present a binary choice for DAI; once DAI enters DSR, it loses its circulation ability, turning it into a game of capital idling.

Now, suppose we take a different approach where users do not directly deposit assets into Spark but first deposit DAI into another protocol (let's call it Xpark). Xpark then invests all DAI into Spark for income accumulation. At the same time, Xpark issues an xDAI to users. Xpark always guarantees a 1:1 exchange between xDAI and DAI; however, the DSR income is only distributed based on the amount of DAI deposited, and xDAI holders cannot obtain any income.

The benefit of this approach is that xDAI can enter circulation, serving as a means of transaction, collateral, payment, or used as LP in DEX. Since xDAI can achieve a rigid exchange with DAI, treating it as an equivalent of 1 USD poses no issues. (Of course, it would be better if xDAI were issued by Spark itself or MakerDAO.)

There is a potential issue here: if the ownership of xDAI is too low, will it be insufficient to support its role as a trusted circulating asset? This issue also has corresponding solutions, for example, in DEX scenarios, a virtual liquidity pool (or called super liquidity staking) can be implemented:

1) The protocol first absorbs a pool of $1m ETH and $1m DAI, where 80% of DAI is deposited into DSR, and 20% DAI and ETH are pooled together.

2) When users swap, the remaining 20% is used for settlement, and if the proportion of DAI rises or falls to a threshold (e.g., 15%/25%), the LP pool can redeem or deposit from DSR.

3) If under normal circumstances, the LP mining APY from trading fees is 10%, and the DSR APY is 5%, then using a virtual liquidity pool under the same conditions, LP can achieve:

10% + 50% * 80% * 5% = 12% APY, achieving a 20% increase in capital efficiency.

(2) More Thorough Separation

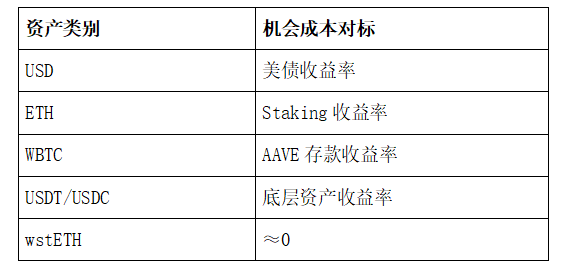

Now, let's imagine a scenario where a stablecoin's collateral includes government bonds RWA, ETH, WBTC, USDC, and USDT. The way to achieve the highest APY is to let RWA earn dollar returns, ETH earn staking returns, WBTC earn AAVE's floating returns, and USDT-USDC be put into Curve for LP. In summary, the goal is to maximize the income-generating state of all collateral.

Based on this, the issuance of a stablecoin, tentatively called XUSD, which cannot generate income, allocates all collateral returns according to the amount minted and the type of collateral to the minters of XUSD. This approach differs from the previously mentioned Xpark idea in that it separates income generation and circulation functions from the very beginning, maximizing the utilization efficiency of funds from the outset.

Of course, the vision for XUSD seems far off, and even xDAI has not yet appeared, but the emergence of a circulating DAI DSR certificate is a certainty. If MakerDAO/Spark does not act, I believe a third party will soon take on this task. Meanwhile, Lybra v2 also plans to achieve this thorough separation, with peUSD as the circulating currency and the exchanged eUSD as the income-generating asset.

In summary, the vision for xDAI or XUSD is still distant, but attracting more real yields, maximizing capital efficiency, and separating income generation and circulation functions will be an inevitable path for on-chain stablecoins. On this path, the twilight of USDC and others can be faintly seen.

Risk warning

Risk warning Risk warning

Risk warning