Delphi: Large investors are pouring into DSR, can the 8% interest rate be sustained?

When the DSR utilization exceeds 20%, the deposit interest rate will soon decrease.

When the DSR utilization exceeds 20%, the deposit interest rate will soon decrease.Author: Joo Kian, Analyst at Delphi Digital

Compiled by: Luffy, Foresight News

Source: https://makerburn.com

MakerDAO recently increased the deposit rate for its stablecoin DAI from 3.19% to 8% (the rate increase is achieved through the EDSR mechanism), aiming to stimulate the growth and demand for DAI by enhancing the attractiveness of the DSR. As a result, DAI now offers the highest yield among stablecoins, surpassing various money market yields and returns from decentralized exchange LPs. The increase in DSR has led to a significant influx of DAI, with the total rising from approximately $340 million to $1.18 billion.

Source: https://makerburn.com

Source: https://makerburn.com

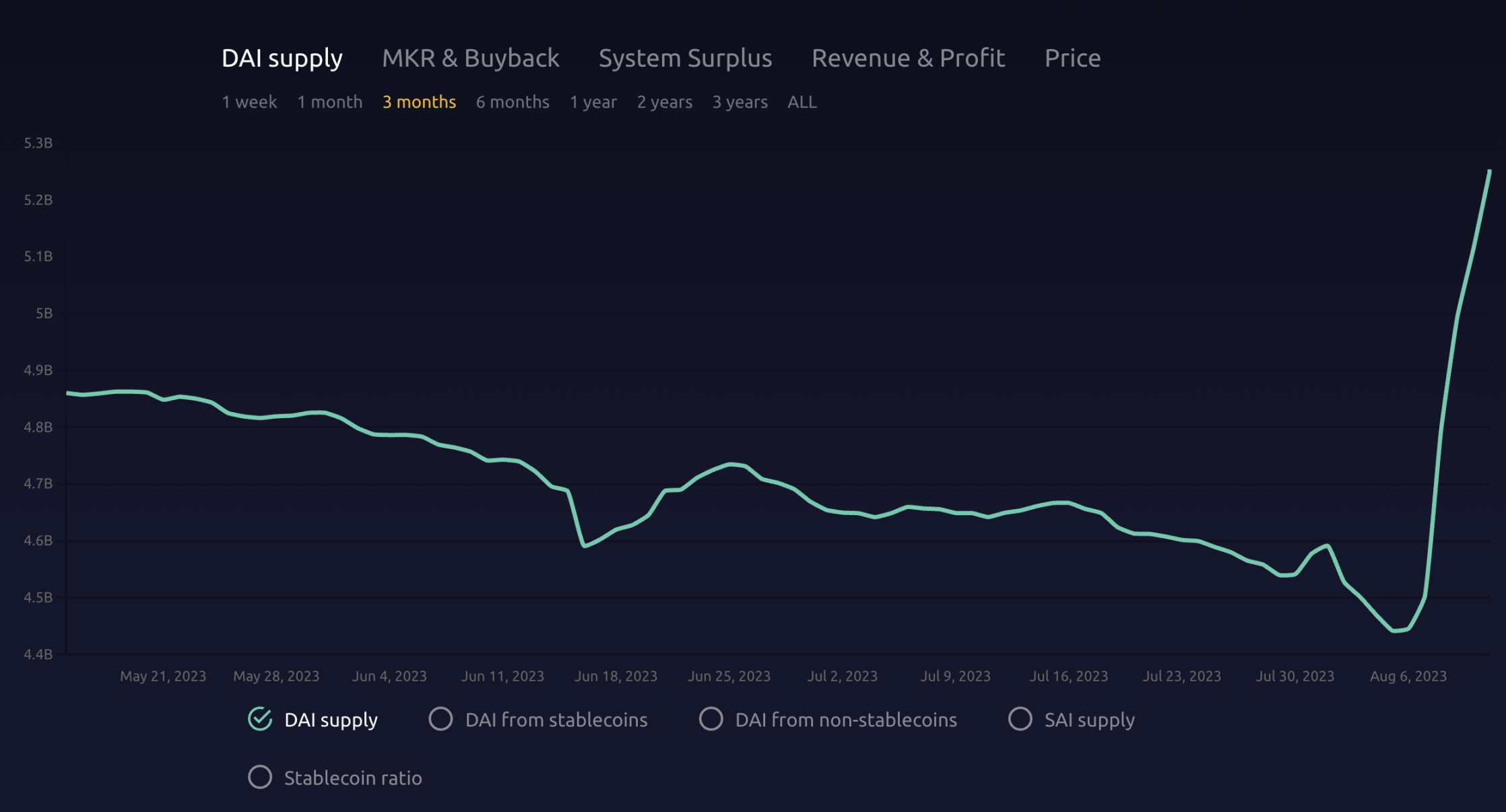

The change in DSR has also incentivized depositors to mint more DAI through the Maker vaults, with the supply of DAI shifting from a continuous decline before August to a clear upward trend.

Source: https://makerburn.com

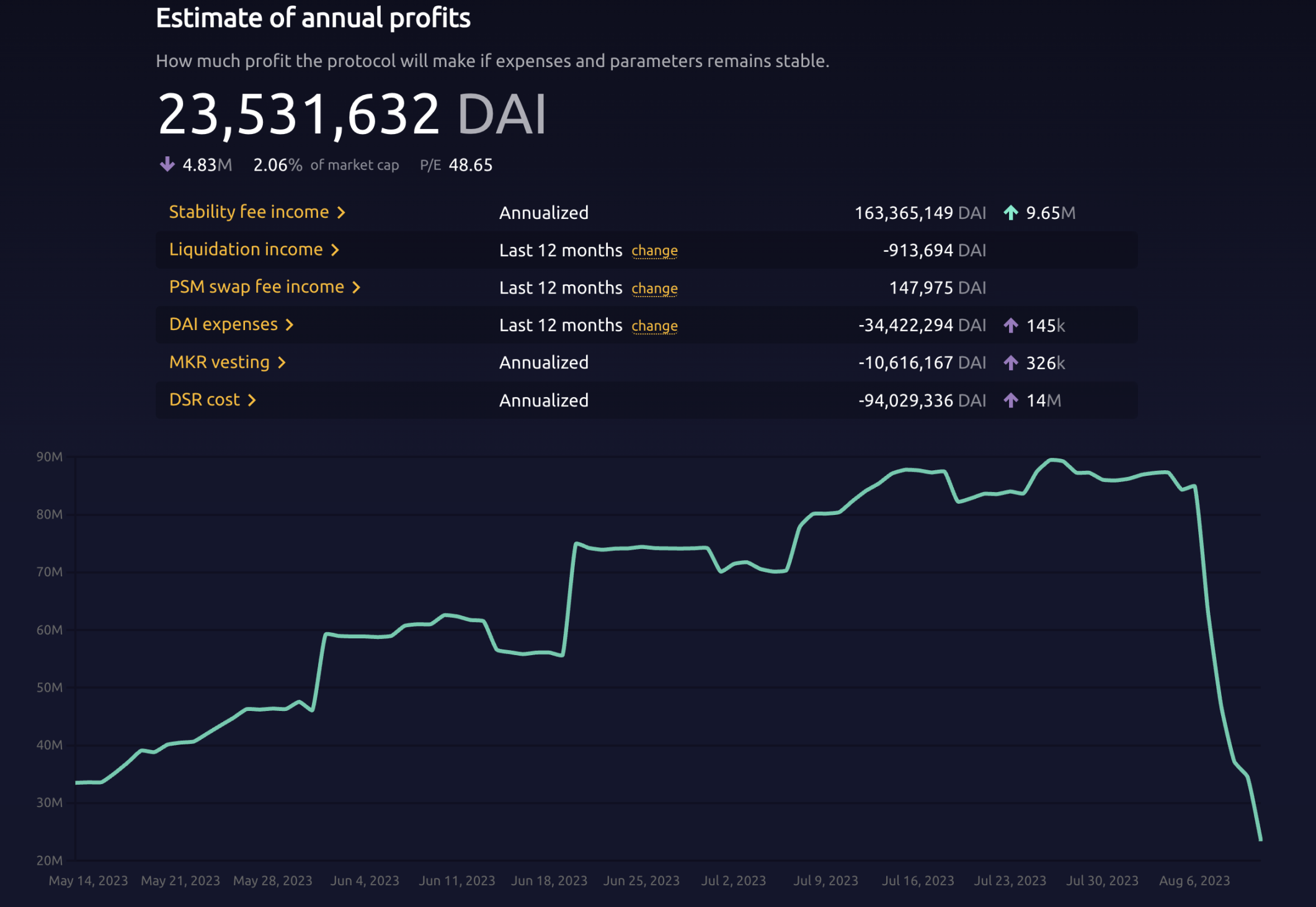

However, this expansion has also brought significant financial implications. With the DSR currently set at 8%, Maker's annual operating costs are projected to be $54 million. Consequently, this will reduce Maker's expected annual profit from $84 million at the beginning of August to $23 million per year. Nevertheless, this decrease in protocol revenue is viewed as a customer acquisition cost to reignite DAI demand.

Is this mechanism sustainable? Here are my theoretical deductions. Based on current data, EDSR is three times the base DSR rate of 3.19%. As the utilization of DSR increases, the deposit rate will decrease (with a cap at 8%).

- When DSR utilization is 0-20%, the deposit rate is 3x DSR = 8%

- When DSR utilization is 20-35%, the deposit rate is 1.75x DSR = 5.58%

- When DSR utilization is 35-50%, the deposit rate is 1.3x DSR = 4.15%

Here, I use the current ratio of "DAI supply" to "New DAI Supply" in DSR to predict potential DAI supply growth. Additionally, since EDSR will revert to the base DSR of 3.19% when DSR utilization exceeds 50%, it is reasonable to assume that DSR utilization will not exceed this threshold, as it would not be economical for depositors.

As more DAI is minted, Maker will earn more interest from the newly minted DAI than it pays in interest for DSR (note: Maker earns returns from other channels by leveraging the collateral backing DAI). With the increase in DSR deposits, this dynamic will put pressure on Maker's profits, leading to a decline in profitability unless the EDSR level reaches 4.15%.

Conclusion: Yes, the new DSR rate mechanism is sustainable.

Compared to U.S. Treasury bonds, the enhanced DAI DSR offers an attractive on-chain yield alternative. Given its higher yield, DSR utilization is likely to stabilize below 35%, aligning with the current Treasury bond rate benchmark of 5.5%. This initiative aims to drive Maker's growth and lay the groundwork for the introduction of Maker SubDAO to increase the demand and utility of DAI and MKR tokens.

Translator's note: The original text was published on August 8. Due to significant changes in current data, the translator has updated the relevant figures to the latest data as of August 11.

Risk warning Risk warning

Risk warning Risk warning