Messari: U.S. Treasury Bonds Drive Rapid Development of RWA

Tokenizing assets in the simulated world brings more diverse collateral, income sources, fractional ownership, and reduces costs and volatility for DeFi.

Tokenizing assets in the simulated world brings more diverse collateral, income sources, fractional ownership, and reduces costs and volatility for DeFi.Original Title: 《The Search for Crypto-Native Business Models》

Author: Messari

Compiled by: Terry, Huzi Guan Bi

Since the advent of smart contract platforms, incorporating real-world assets (RWAs) into DeFi collateral has been a dream for many in the cryptocurrency space. Tokenizing assets from the physical world promises to bring more diverse collateral, revenue streams, fractional ownership, and reduced costs and volatility to DeFi.

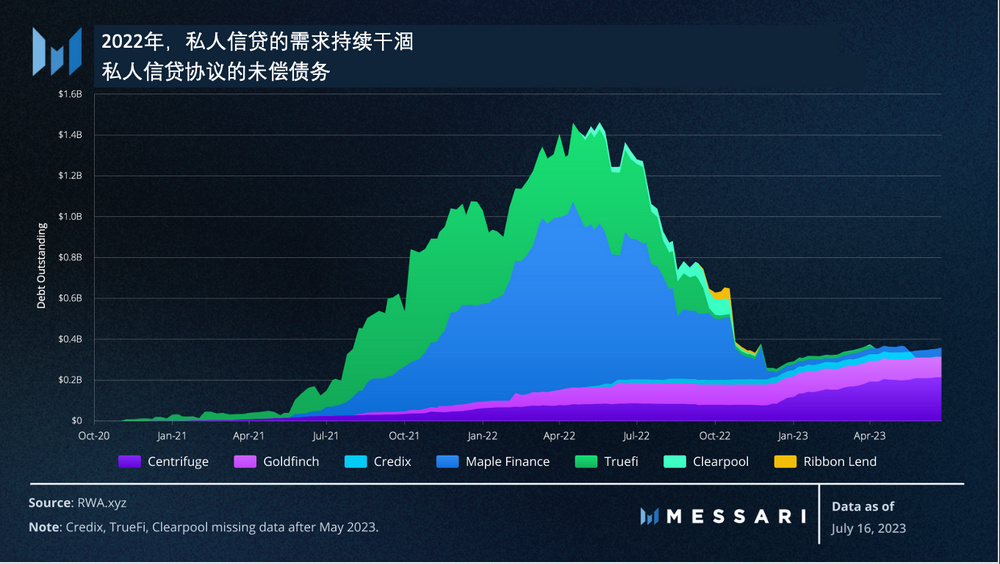

After a wave of initial tokenized real estate projects failed to take off in 2018 and 2019, RWAs seemed to gain legitimate momentum for the first time during the bull market of 2021, thanks to private credit protocols like Maple Finance, TrueFi, Goldfinch, and Centrifuge. The idea behind these protocols is that stablecoin lenders can enjoy above-average returns by lending to under-collateralized borrowers vetted by the protocol.

In theory, borrowers use these funds for productive investments in the real world. However, a closer look reveals that much of the borrowing growth in late 2021 and early 2022 was primarily driven by crypto-native businesses using Maple Finance and TrueFi. These businesses are likely using the funds for cheap leverage or on-chain arbitrage strategies rather than providing entirely new services in the real world.

While private credit protocols like Centrifuge and Goldfinch are steadily growing, they pale in comparison to the newer RWA subcategory that has consistently grown in 2023: on-chain U.S. Treasuries.

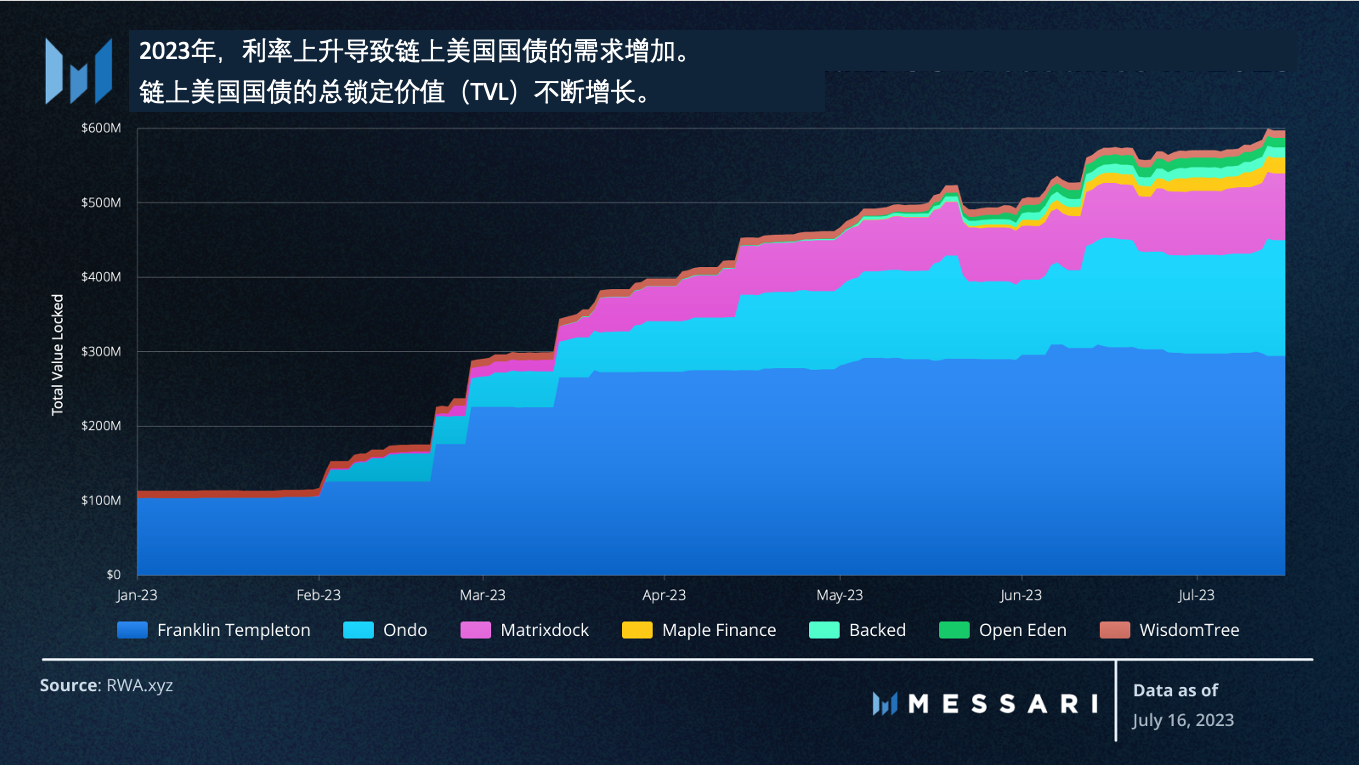

Over the past 15 months, demand for U.S. Treasury yields has surged with the Federal Reserve's historic rate hikes, raising the federal funds rate from 0.25% in March 2022 to 5.25% today. Currently, the stablecoin yields offered by top cryptocurrency lending protocols are around 3%, while U.S. Treasury yields provide a more attractive low-risk alternative. This has led to the emergence of some protocols that transfer these offline yields on-chain. Two of the most notable protocols include:

Franklin Templeton's U.S. Government Money Market Fund—this is the largest on-chain fund with nearly $300 million in total investments. The fund has been tokenized on Stellar, but its filing with the U.S. Securities and Exchange Commission (SEC) states that any offline ledger will take precedence over the blockchain in the event of a dispute.

Ondo Finance's OUSG—this is a stablecoin that effectively wraps U.S. Treasury bill ETFs and passes the interest to its holders. Ondo's services are only available to qualified purchasers (individuals or families with investments over $5 million), and OUSG can only be transferred between whitelisted addresses. Ondo offers a variant of Compound V2 called Flux Finance, allowing OUSG to be used as collateral to borrow stablecoins like USDC, USDT, and Dai.

While these projects are a step in the right direction, their limitations make it nearly impossible for the average cryptocurrency investor to utilize them. Most protocols restrict their services to non-U.S. users, and KYC (Know Your Customer) measures prevent tokenized assets from integrating with permissionless DeFi services. It is again emphasized that clear regulatory guidelines are needed for tokenized Treasuries to gain legitimacy in the crypto economy.

In the short term, U.S. Treasuries will continue to play a significant role in the two largest stablecoin protocols in cryptocurrency. On June 21, MakerDAO purchased an additional $700 million in U.S. Treasuries, bringing its total holdings to $1.2 billion. The $2.3 billion in RWA collateral has now become the largest component of the protocol's assets, accounting for 49% of Maker's assets. These RWA components have also brought substantial fee revenue to the protocol. According to data from MakerDAO's strategic finance core unit, stable fees from RWAs account for 78.5% of all stable fees to date. This shift indicates Maker's commitment to building a diversified collateral base that can withstand DeFi's volatility.

On the same day that Maker made its recent Treasury purchase, Circle reaffirmed its commitment to using Treasuries to back its USDC stablecoin. Last month, the company liquidated all $24 billion in Treasuries during the U.S. debt ceiling standoff, opting instead for overnight repurchase agreements. With the debt ceiling conflict resolved on June 3, Circle resumed purchasing Treasuries for its USDC reserve fund managed by BlackRock, planning to allocate its exposure between short-term Treasuries and repurchase agreements.

Key Events

Pendle

Pendle has become the best-performing DeFi asset this year with a 1700% price increase. This yield derivative protocol allows users to split interest-bearing tokens into separate principal tokens (PTs) and yield tokens (YTs), speculating on yield fluctuations. With the rise of the Ethereum staking ecosystem, this has become an increasingly popular service. Pendle recently achieved the most impressive performance over the past 30 days, with a price increase of 70.5% and a TVL increase of 37.5%.

The growth in TVL has been primarily driven by deposits of stETH and GLP, along with the recent addition of Aura Finance's swETH pool. The swETH pool is the first LST pool on Pendle, allowing both parties to earn yields; users earn base staking rewards from Swell's swETH while also earning loan yields from lending bbaWETH on Aave.

Pendle employs a vote-escrowed (ve) governance system, allowing users to lock PENDLE in exchange for vePENDLE and share in the protocol's revenue. vePENDLE holders receive 80% of swap fees, 3% of fees generated from all yields from Pendle's yield tokens, and a portion of the yield from unredeemed principal and yield tokens after they expire.

Pendle's recent price growth has been driven by the "Pendle War" that began in early June. Following the launch of Penpie and Equilibria, they quickly became the largest vePENDLE holders, subsequently leading to a reduction in the circulating PENDLE supply. This supply change is correlated with a 101% price increase within 30 days of Penpie and Equilibria's launch.

Another potential driver for future growth in the Pendle ecosystem is support from other DeFi protocols for Pendle-based assets as collateral. Dolomite, a DEX and money market built on Arbitrum, added support for Pendle's PT-GLP as a lending collateral on June 28, making it the first lending protocol to allow Pendle users to gain leverage on Pendle assets. In the future, more integrations could bring further growth to Pendle's emerging ecosystem.

Drift's Super Stake SOL

As the Solana ecosystem continues to recover from the collapse triggered by SBF in 2022, SOL staking is becoming an attractive source of yield within the ecosystem. Drift Protocol launched its Super Stake service, allowing users to gain leveraged exposure to SOL staking yields in a manner similar to using looping lending strategies on Ethereum.

The Super Stake looping process is as follows:

Users deposit mSOL, a liquid staking token provided by Marinade Finance.

Borrow SOL against mSOL.

Stake the borrowed SOL to earn more mSOL.

Repeat the above process.

Super Stake allows users to execute the looping process with a single click and can use up to 3x leverage for looping. The Super Staking process has quickly become a popular service on Drift, with over 100,000 mSOL deposited. Drift plans to add support for other popular Solana liquid staking tokens after developing reliable Pyth oracles for stSOL and jitoSOL.

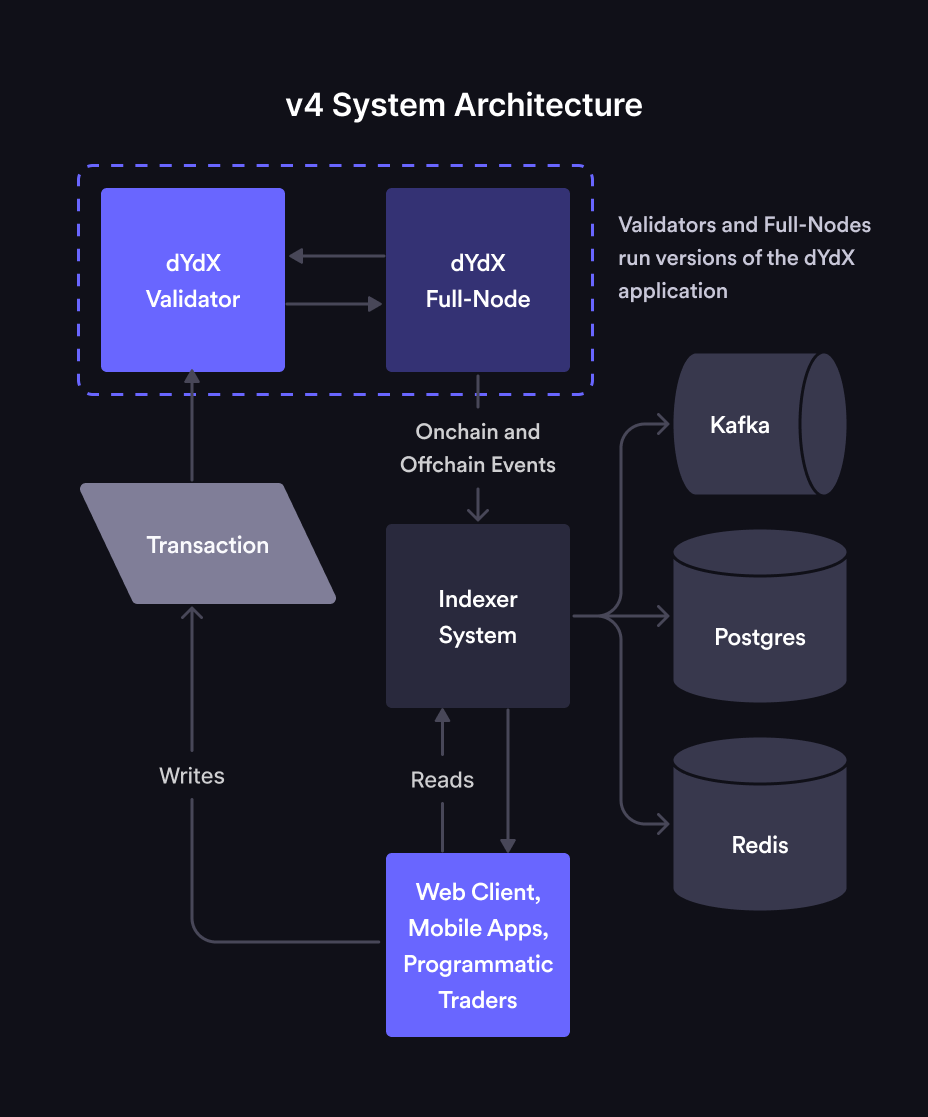

dYdX V4 Testnet

The highly anticipated dYdX V4 was launched on the testnet on July 5. Although the V4 testnet currently only supports BTC and ETH, it includes over 10 wallet integrations, including popular options like Metamask and Coinbase Wallet. This is significant because most Cosmos-based networks lack support for the most popular wallets suitable for EVM-compatible chains. Supporting these wallets should help dYdX V4 attract users from EVM networks while abstracting away the relationship between dYdX and Cosmos, which has been emphasized by dYdX founder Antonio Juliano.

In the weeks leading up to the testnet launch, technical details of dYdX V4 were made public. Highlights of the new architecture include an off-chain order book and matching engine maintained by a validator set of the dYdX Chain, as well as a custom-built indexing system that transmits the state of the on-chain order book to dYdX's frontend.

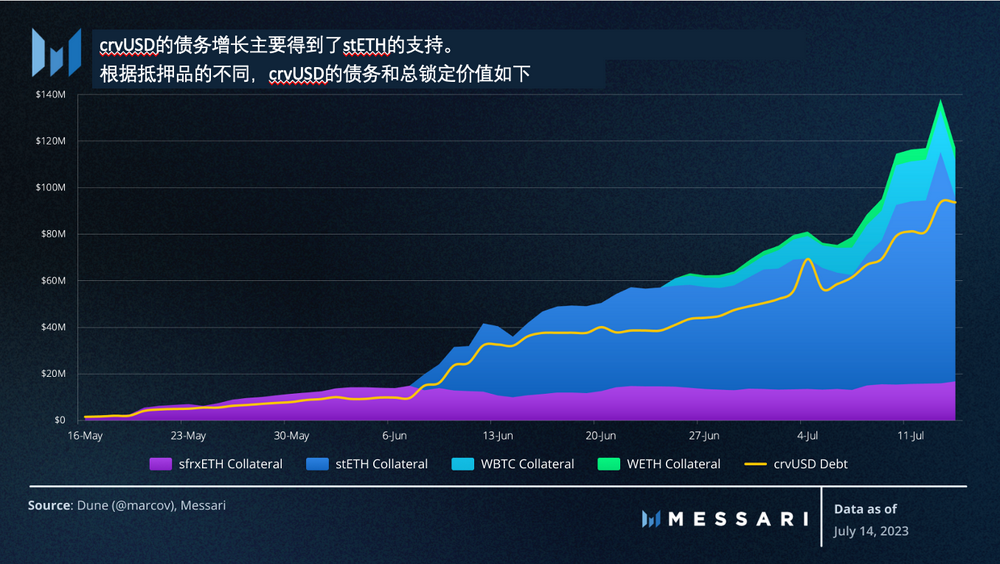

Increased Adoption of crvUSD

After a slow initial launch, the adoption of crvUSD has increased over the past month, with total locked value rising from $48 million to $147 million, and crvUSD debt increasing from $37.6 million to $91 million.

The growth has been primarily driven by the addition of wstETH as collateral on June 8, which now accounts for 71.9% of the total locked value of crvUSD. Recently, WBTC and WETH were included as eligible collateral types on June 18 and 20, respectively. WBTC is now close to surpassing sfrxETH as the second-largest collateral type by total locked value—wBTC accounts for 13.4% of total locked value, while sfrxETH accounts for 14.1%. To further align with the overall protocol, Curve's DAO also voted to allocate fees generated from crvUSD to veCRV holders. Despite recent increases in total locked value and trading volume, there are currently fewer than 400 addresses holding crvUSD, indicating that the stablecoin's use is highly concentrated among a few core DeFi users.

Aave GHO Launched on Ethereum Mainnet

In the future, with the long-awaited launch of Aave's GHO stablecoin on the Ethereum mainnet over the weekend, crvUSD will face increasing competition. The minting cap for GHO will initially be set at 100 million GHO, with a borrowing rate of 1.5%, and a 30% discount will be offered when using stkAAVE as collateral for minting.  With the introduction of GHO, Aave creates an additional revenue stream and gains more control over the supply side of its money market. This will lower Aave's stablecoin funding costs, as the protocol will no longer rely on attracting external stablecoins (like USDC) to meet user demand, thereby solidifying Aave's top-down supply service business model.

With the introduction of GHO, Aave creates an additional revenue stream and gains more control over the supply side of its money market. This will lower Aave's stablecoin funding costs, as the protocol will no longer rely on attracting external stablecoins (like USDC) to meet user demand, thereby solidifying Aave's top-down supply service business model.

DeFi Chartbook

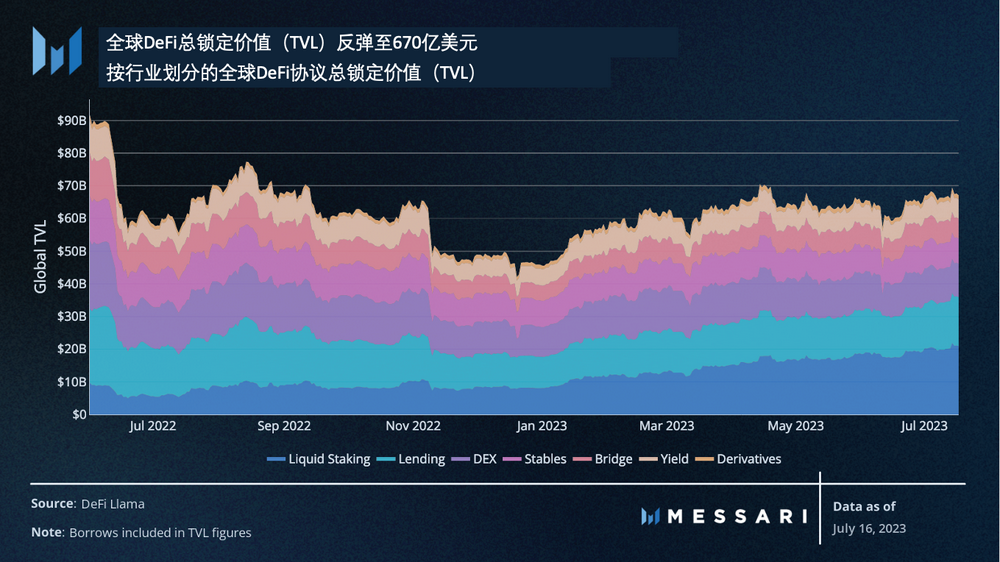

Global Total Locked Value (TVL)

The global total locked value (TVL) in DeFi experienced a regression over the past 30 days, following a sudden drop after the U.S. Securities and Exchange Commission (SEC) lawsuits against Coinbase and Binance US. The current total locked value (TVL) is $67 billion, close to the peak of $70 billion at the end of April 2023.

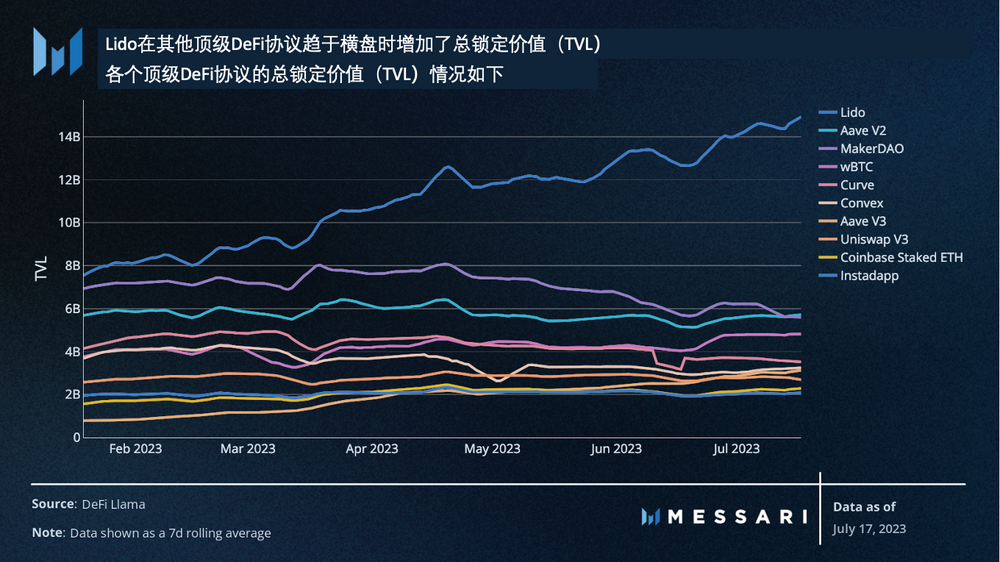

Lido continues to absorb the most total locked value (TVL) among all DeFi protocols. Over the past 30 days, this liquid staking giant has added $25 billion in TVL. For comparison, Lido's closest decentralized liquid staking competitor, Rocket Pool, has only $1.9 billion in TVL. Lido currently holds a 32% dominance in the staking space and is once again approaching the implied 33.3% cap, which would make Lido a single attack vector for Ethereum's vitality.

Global User Count

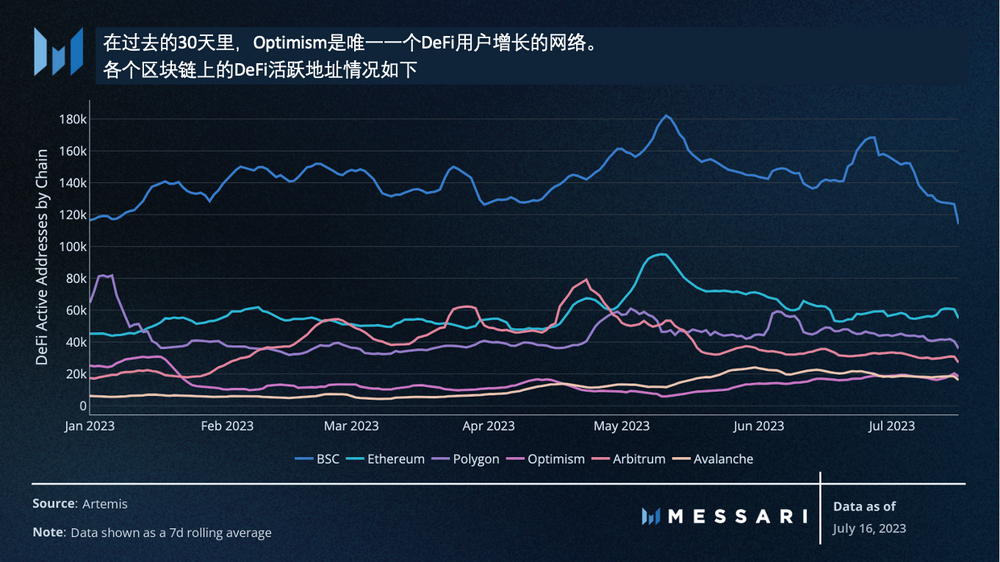

After a sharp decline in June, the Binance Smart Chain regained some DeFi users, but the network's user change over the past 30 days remains negative. This trend is consistent across all tracked networks except for Optimism. Active DeFi addresses on Optimism grew by 9.8%. The growth in active addresses on Optimism is primarily due to increased trading activity on Uniswap and DEX aggregators Matcha and 1inch.

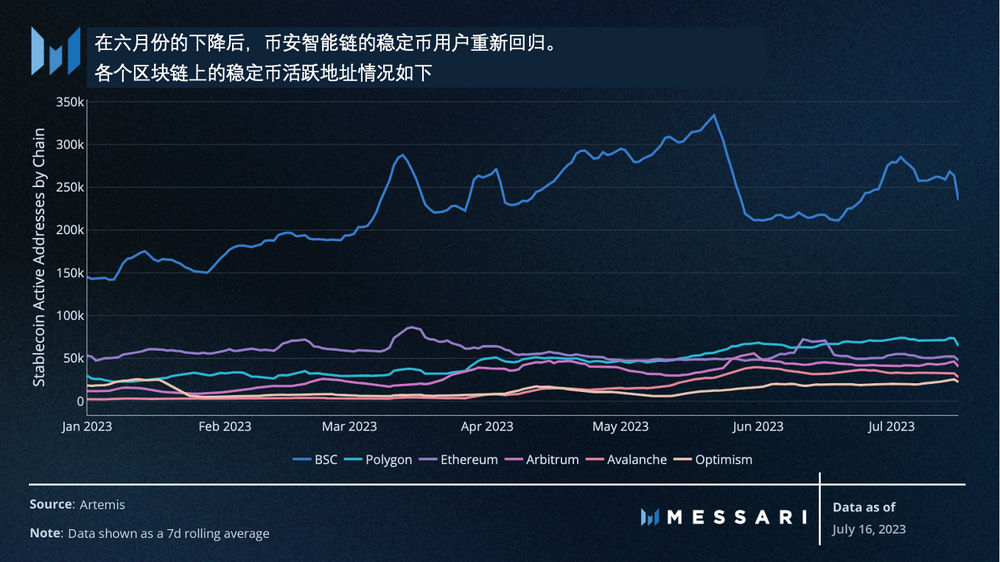

After a sharp decline in June, the Binance Smart Chain regained some DeFi users, but the network's user change over the past 30 days remains negative. This trend is consistent across all tracked networks except for Optimism. Active DeFi addresses on Optimism grew by 9.8%. The growth in active addresses on Optimism is primarily due to increased trading activity on Uniswap and DEX aggregators Matcha and 1inch.  In terms of stablecoin users, Binance Smart Chain has regained a significant portion of the active addresses lost in June, growing by 10.1%. Optimism is the only other network to see growth in stablecoin addresses, increasing by 11.8%. Notably, Ethereum's stablecoin active addresses have decreased by 24% again, continuing the trend following the meme coin frenzy on the Ethereum mainnet in May.

In terms of stablecoin users, Binance Smart Chain has regained a significant portion of the active addresses lost in June, growing by 10.1%. Optimism is the only other network to see growth in stablecoin addresses, increasing by 11.8%. Notably, Ethereum's stablecoin active addresses have decreased by 24% again, continuing the trend following the meme coin frenzy on the Ethereum mainnet in May.

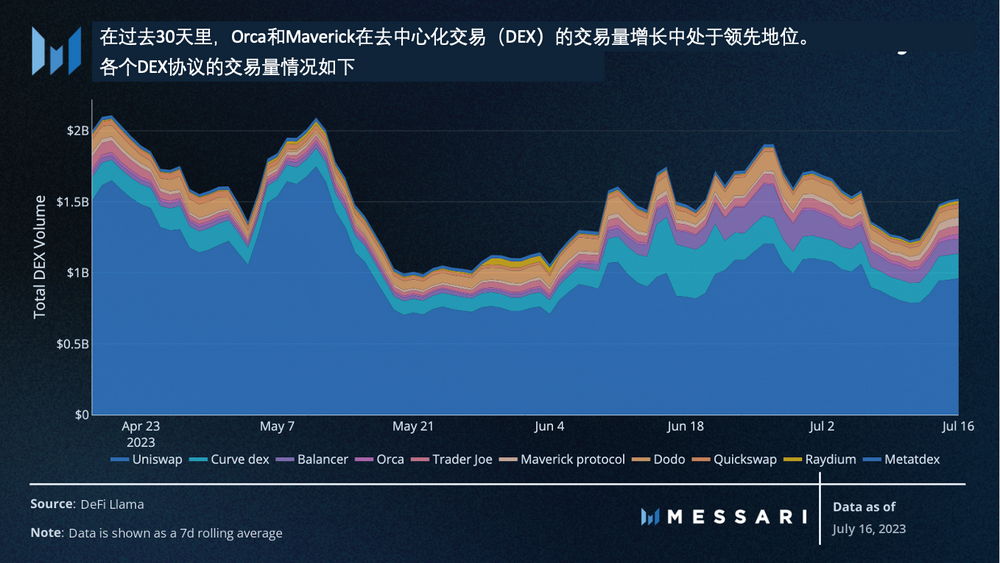

DEX Trading Volume

DEX trading volume has remained relatively stable over the past month. In recent weeks, Orca and Maverick have seen the fastest growth in trading volume. Orca's growth can be attributed to renewed attention on Solana DeFi in recent weeks, while Maverick's activity benefits from its recent token launch and incentive programs.

DEX trading volume has remained relatively stable over the past month. In recent weeks, Orca and Maverick have seen the fastest growth in trading volume. Orca's growth can be attributed to renewed attention on Solana DeFi in recent weeks, while Maverick's activity benefits from its recent token launch and incentive programs.

Lending Market

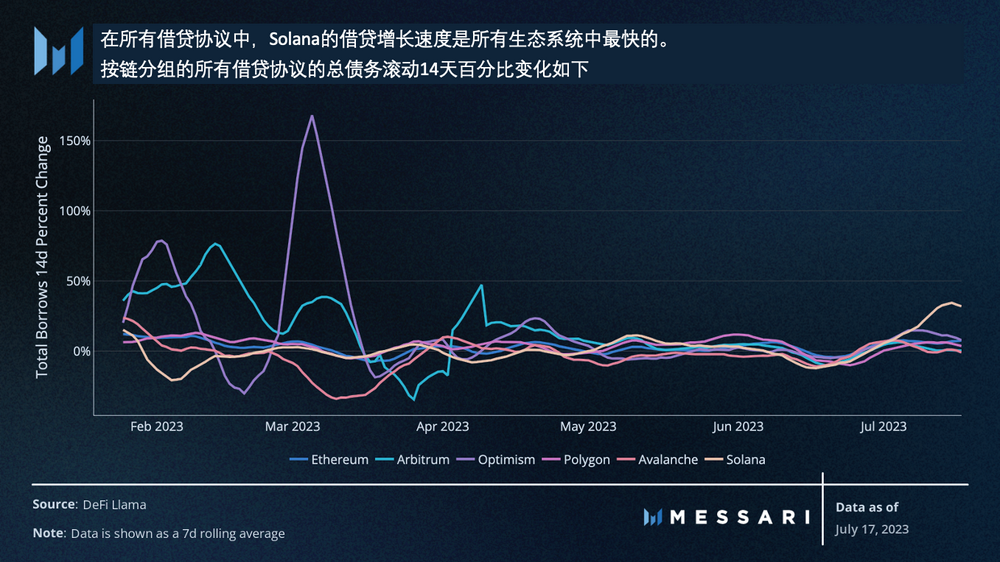

Global on-chain debt has grown by 14.7% over the past month, currently reaching $5.2 billion. Debt utilization has increased again, while Ethereum's price has remained stable over the past few months. Unlike the dramatic spikes in utilization over the past 18 months, the current growth is slow and steady.

Currently, Solana is experiencing the fastest growth in lending across various independent ecosystems. This is mainly because Solana's DeFi ecosystem is much smaller than others, so any increase in activity is likely to result in a larger percentage change. In addition to the development of Drift's Super Stake service, funds are flowing into MarginFi, hoping for potential airdrops related to lending activities on the protocol.

Yield

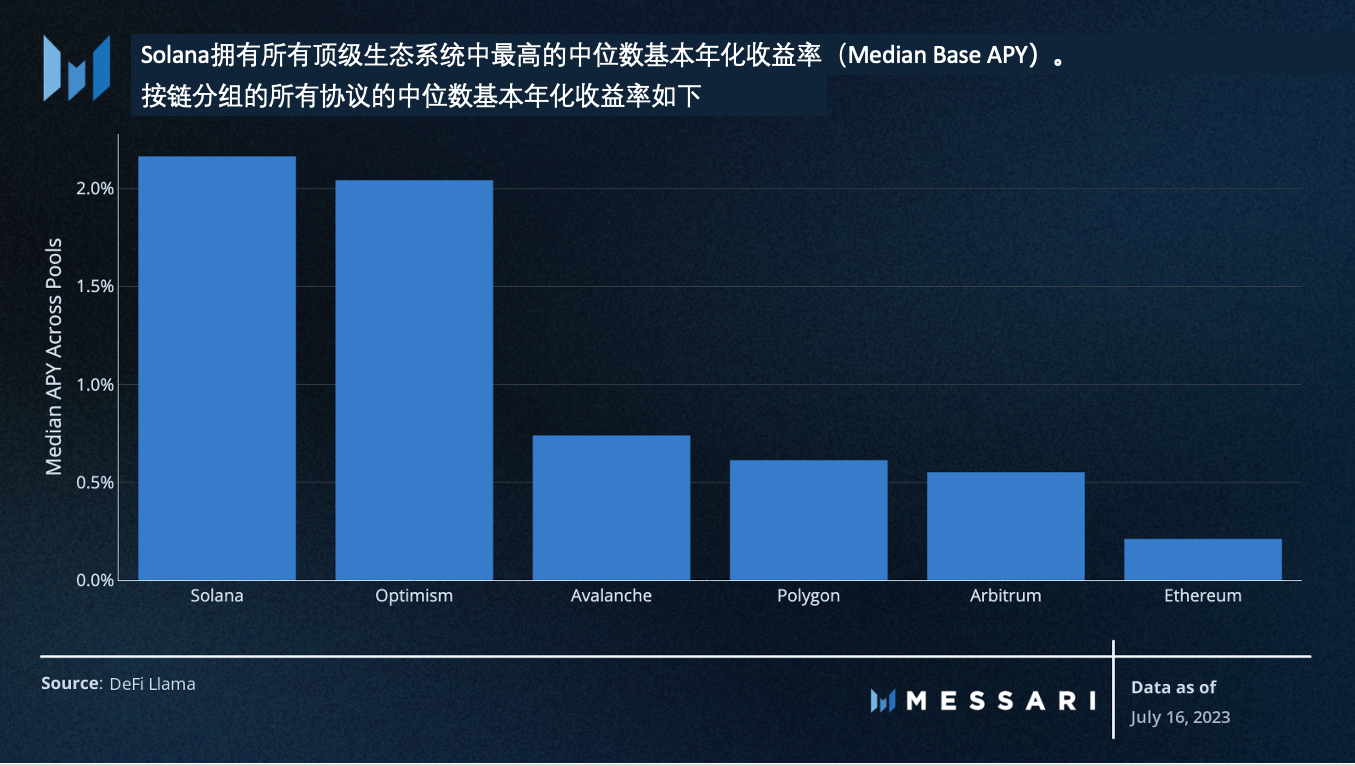

The renewed focus on Solana's DeFi ecosystem is also reflected in Solana surpassing Optimism to become the highest-yielding ecosystem (based on the median across all pools).

The emerging Credix continues to offer double-digit USDC yields to users willing to lend to businesses in the traditional world, while Solana's top decentralized exchange Orca continues to generate high yields in its concentrated liquidity pools.

Funding

- Alluvial Protocol - $12 million Series A

Alluvial, the development company behind Liquid Collective, completed a $6.2 million seed round in January this year, and just six months later, it has completed a $12 million Series A funding round. Liquid Collective currently comprises Coinbase Prime, Bitcoin Suisse, and Hashnote, aiming to provide enterprises with a compliant liquid staking experience.

The supply of Liquid Collective's liquid staking token LsETH is only 2,500 ETH, but this new round of funding indicates that investors are confident in Alluvial becoming a major player in the enterprise ETH staking space in the coming years. This round of funding was co-led by Ethereal Ventures and Variant.

- Ambient Finance - $6.5 million Seed Round

Previously known as CrocSwap, Ambient Finance announced the completion of a $6.5 million seed round, bringing the protocol's valuation to $80 million. Ambient is an innovative decentralized exchange that supports concentrated liquidity and environmental liquidity (X*Y = K), as well as native limit orders. Liquidity pool fees can be dynamically adjusted and automatically reinvested into the liquidity pool for compound returns.

Ambient launched on the Ethereum mainnet on June 12 and has attracted $6.5 million in total locked value (TVL) at the time of writing. Similar to the yet-to-be-released Uniswap V4, Ambient has the opportunity to gain attention before competitors launch similar services later this year or early 2024.

- Maverick Protocol - $9 million Venture Round

Another decentralized exchange, Maverick Protocol, raised $9 million in a funding round led by Founders Fund, bringing its total funding since its founding in 2021 to $18 million. Maverick differentiates itself from competing decentralized exchanges by automatically adjusting concentrated liquidity positions during price fluctuations.

Since its initial launch on the Ethereum mainnet in March 2023, Maverick has had the highest turnover rate (trading volume / TVL) among all decentralized exchanges and has also become the largest decentralized exchange on zkSync Era. Shortly after the funding on June 21, Maverick released its governance token.

- One Trading - $33 million Series A

Bitpanda Pro has become a new entity—One Trading—and raised $33 million in Series A funding. This Austrian exchange targets institutional and professional European traders and adopts a membership model rather than relying on a pay-per-trade business model. This round of funding is the latest example of increasing international capital, showing investors' continued commitment to strengthening overseas exchange infrastructure amid regulatory uncertainty in the U.S. This round of funding for One Trading was led by Peter Thiel's Valar Ventures.

Original link: https://messari.io/report/us-treasuries-fuel-real-world-asset-growth?referrer=all-research