Glassnode data research: BTC is experiencing an unprecedented low volatility period

For Bitcoin, such a degree of consolidation and price compression is a very rare event.

For Bitcoin, such a degree of consolidation and price compression is a very rare event.Original Title: 《Volatility Crush》

Author: Checkmate, Glassnode

Compilation: Deep Tide TechFlow

Summary

Bitcoin is known for its volatility, yet the market is currently experiencing extreme volatility compression.

The futures market is noticeably stable, with trading volumes for Bitcoin and Ethereum reaching historical lows, and spot trading and arbitrage yields at 5.3%, slightly above the risk-free rate.

The implied volatility in the options market is undergoing significant volatility compression, with the volatility premium being less than half of the benchmarks from 2021-22.

The put/call ratio and the 25-delta skew indicator are both at historical lows, indicating a bullish bias in the options market, while the pricing of put options suggests very low future volatility.

A Calm Period

The Bitcoin market is experiencing a very calm period, with many volatility indicators dropping to historical lows. In this article, we will explore the extraordinary nature of this quiet period from a historical perspective, and then examine how the derivatives market is pricing it.

First, we note that the spot price of Bitcoin is above several long-term moving averages widely observed in the industry (111 days, 200 days, 365 days, and 200 weeks). These averages range from a low of $23,300 (200DMA) to a high of $28,500 (111DMA). The chart also highlights similar periods in the past two cycles, which often align with macro uptrends.

We can observe a very similar situation using on-chain realized prices, which simulate the cost basis of three groups:

? The entire market (actual price).

? Short-term holders (coins held for less than 155 days).

? Long-term holders (coins held for more than 155 days).

The spot price is again above these three models and shows strong consistency with the classic technical analysis tools mentioned above.

It has been 842 days since the peak of the bull market in April 2021. Compared to history, the recovery in 2023 is actually somewhat better, with a decline of -54% compared to the all-time high, while historical declines have been -64%.

We also note that before the market accelerated past the -54% retracement level, both the 2015-16 and 2019-20 cycles experienced a 6-month period of sideways boredom. This may suggest a potential for future boredom.

After a hot start in early 2023, both quarterly and monthly price performances have cooled. We can again see many similarities with previous cycles, where the initial momentum of the bottom rebound was strong, but then entered a prolonged period of consolidation.

Bitcoin analysts often refer to this period as a re-accumulation phase.

Volatility Collapse

The realized volatility of Bitcoin over the observation window of 1 month to 1 year in 2023 has significantly decreased, reaching multi-year lows. The 1-year volatility level is now at levels not seen since December 2016. This is the fourth extreme volatility compression period:

The bear market at the end of 2015 entering the re-accumulation phase of 2016.

The bear market at the end of 2018 occurred before the November sell-off of 50%. However, a recovery rebound occurred in April 2019, rising from $4,000 to $14,000 within three months.

After March 2020, as the world adapted to the COVID-19 outbreak, the market saw consolidation.

The market adjustment at the end of 2022, when the market was digesting the failure of FTX, and our current market situation.

The price range between the highest and lowest prices within 7 days is only 3.6%. Only 4.8% of trading days have experienced a smaller weekly trading range.

The 30-day price range is even more extreme, with prices fluctuating within only 9.8% over the past month, and only 2.8% of months have had a smaller range. Such a degree of consolidation and price compression is a very rare event for Bitcoin.

This calm period is also visible in the derivatives markets for Bitcoin and Ethereum. For both assets, trading volumes in futures and options are close to or at historical lows.

The current derivatives trading volume for Bitcoin is $19 billion, while the Ethereum market has only $9.2 billion in daily trading volume, marking a low point since January 2023.

The market also maintains a relatively risk-averse stance, with Bitcoin's dominance in the futures market gradually increasing. During the period from 2021 to 2022, the trading volume and open interest in Ethereum futures steadily increased relative to Bitcoin, peaking at 60 BTC : 40 ETH in the second half of 2022.

This year, Bitcoin has regained its dominance, indicating that lower liquidity and reduced risk appetite continue to drive funds up the risk curve.

In the past month, Bitcoin's open interest in the futures market has also remained relatively stable at $12.1 billion. This is similar to levels in the second half of 2022, when Bitcoin prices were about 30% cheaper than today, and the FTX exchange was still active. This also resembles the bullish period in January 2021, when Bitcoin prices were 30% higher than now, and the market was less mature, with leveraged speculation just beginning to heat up.

From a comparative perspective, the options market has seen significant growth in dominance and growth, with open interest increasing more than double over the past 12 months. Now, the options market is on par with the futures market in terms of open interest scale.

On the other hand, the open interest in the futures market has been steadily declining since the end of 2022 (when FTX collapsed), with only slight increases in 2023.

With low trading volumes and lackluster activity in the futures market, the next goal is to identify which opportunities keep traders active in the digital asset derivatives space.

In the futures market, the term structure indicates that annualized returns from spot arbitrage strategies can range between 5.8% and 6.6%. However, this is only slightly above the yields of short-term U.S. Treasury bills or money market funds.

The perpetual contract market is the most liquid trading venue in digital assets, where traders and market makers can lock in funding rate premiums to arbitrage futures and spot prices. This form of spot arbitrage is more volatile and dynamic, but considering this additional risk, the current annualized yield of 8.13% is more attractive.

Notably, since the end of 2022, the funding rate has maintained a stable positive growth, indicating a significant change in market sentiment.

In the options market, we can see the severity of the volatility compression, with the implied volatility of all contracts expiring at historical lows.

The volatility in the Bitcoin market is very high, with implied volatility for options trading mostly between 60% and over 100% during much of 2021-22. However, currently, the volatility premium in options pricing is at its lowest in history, with IV ranging between 24% and 52%, less than half of the long-term baseline.

The IV (implied volatility) term structure shows that the volatility premium has been contracting over the past two weeks. In just the past two weeks, the implied volatility of December contracts has dropped from 46% to 39%. The volatility premium for options expiring in June 2024 is slightly above 50%, which is relatively low historically.

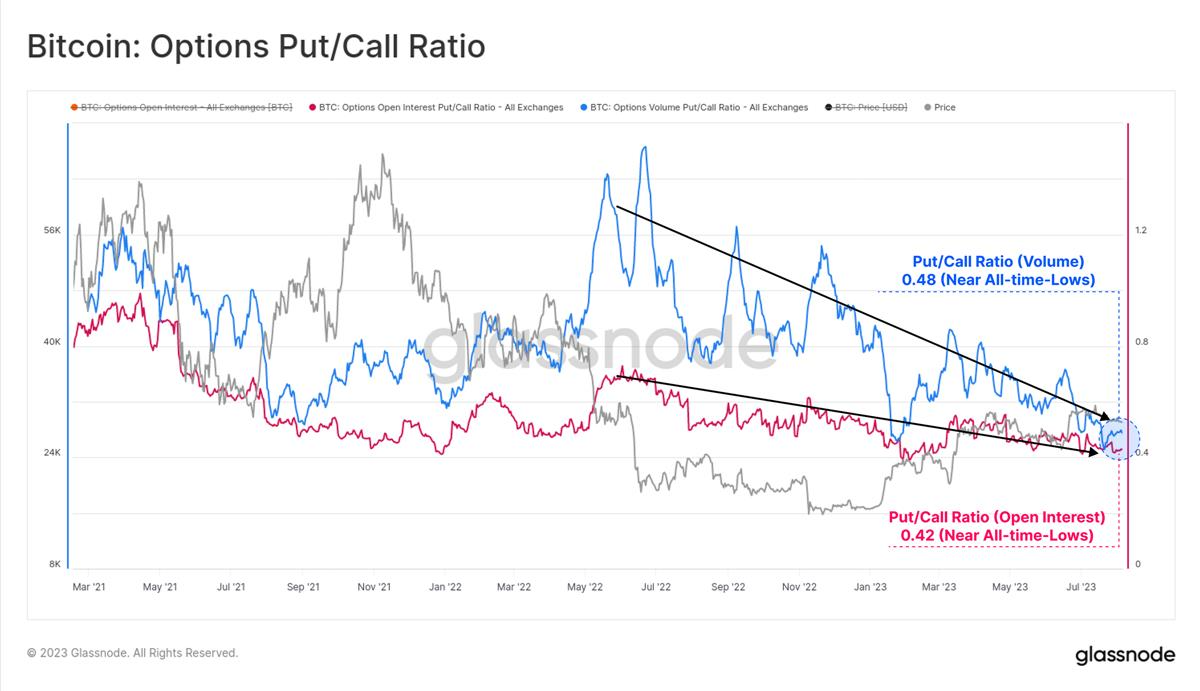

In terms of both volume and open interest metrics, the put/call ratio is at or near historical lows, trading in the range of 0.42 to 0.48. This indicates a net bullish sentiment in the market, with demand for call options still dominating.

As a result, put options have become increasingly cheaper relative to call options, reflected in the historical lows of the 25-delta skew indicator. Overall, this suggests that the options market (now comparable in scale to the futures market) believes that future volatility will be at historical lows.

Conclusion and Summary

Few headlines claim that Bitcoin is a price-stable and non-volatile asset, making the situation where the monthly trading range is below 10% particularly striking. Currently, the market's volatility can be said to be at an all-time low, raising questions about whether there will indeed be an increase in volatility in the future.

The cash arbitrage yield in the futures market ranges between 5.3% and 8.1%, slightly above the risk-free rate of short-term U.S. Treasury bills. The implied volatility premium in the options market is at historical lows, especially with very weak demand for put options.

Considering Bitcoin's volatility, are we entering a new era of price stability for Bitcoin, or is volatility mispriced?