LSD Track Analysis: With Many Competitors Arising, Why is Lido Still Viewed Favorably?

Compared to other agreements with periodic business, liquidity staking agreements should receive a higher valuation multiple.

Compared to other agreements with periodic business, liquidity staking agreements should receive a higher valuation multiple.Original Title: Lido Finance --- The Most Liquid Staking Protocol

Original Author: Arthur0x, Founder of DeFiance Capital

Compiled by: Shenchao TechFlow

Abstract

- Liquid staking is one of the few areas in cryptocurrency where protocols have achieved a unique product-market fit by addressing the capital efficiency issues faced by token holders on proof-of-stake (PoS) blockchains. This has led to the sector having the largest total value locked (TVL) in decentralized finance (DeFi) at $22 billion. If the capital efficiency issues of PoS chains persist, there will be a long-term demand for liquid staking solutions.

- As the value of the chains serviced by the protocol grows, the liquid staking market is also expanding. Today, the top five liquid staking protocols on smart contract chains generate over $800 million in revenue annually. Additionally, due to its utility and non-volatility, the profitability quality of this industry surpasses that of other DeFi sectors.

- With Lido establishing strong network effects around stETH and having a good track record of reliability along with the adoption of decentralized validator technologies like SSV and Obol, it is well-positioned to capture industry growth.

- We believe that in the medium term, Lido's revenue has the potential to triple, primarily due to: 1) the increase in Ethereum's market capitalization, 2) the rise in Ethereum staking ratios post-Shanghai upgrade, 3) the growing market share of decentralized liquid staking protocols, and 4) Lido's continued dominance.

Liquid staking protocols have achieved a good product-market fit by solving the capital efficiency issues faced by stakers.

Today, the top smart contract chains ranked by total value locked are all running PoS or variants of PoS, such as delegated proof-of-stake, authorized proof-of-stake, etc.

These blockchains allow users to stake their tokens in exchange for rewards that enhance network security. However, the tokens of stakers often need to go through an unbonding period, which varies in length depending on the protocol, typically ranging from a few days to several weeks. This presents a critical capital efficiency issue for stakers.

Liquid staking protocols emerged to allow users to stake their tokens in exchange for a receipt token that represents their claim on the staked assets and corresponding staking rewards. This receipt token can be freely transferred and used in DeFi activities such as trading, liquidity pools, and lending.

Most importantly, liquid staking protocols provide stakers with two key value propositions—1) the ability to generate yield and 2) the liquidity of staked assets, both of which address the capital efficiency issue. As a result, the liquid staking sector boasts a total value locked of $22 billion, making it the sector with the highest total value locked.

We believe that this product-market fit is unique to the liquid staking sector—if PoS-type chains remain popular, capital efficiency will continue to be an important issue, leading to long-term demand for liquid staking solutions.

Liquid staking protocols provide a sustainable source of revenue for a large market.

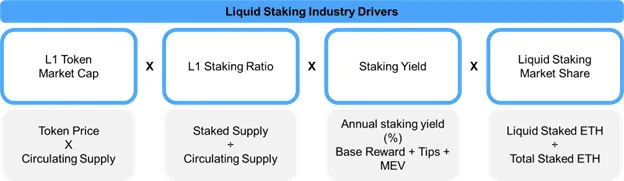

From a macro perspective, the potential scale of liquid staking revenue is determined by four growth drivers: the market capitalization of L1 tokens, the staking ratio of L1, staking yields, and the market share of staking service providers.

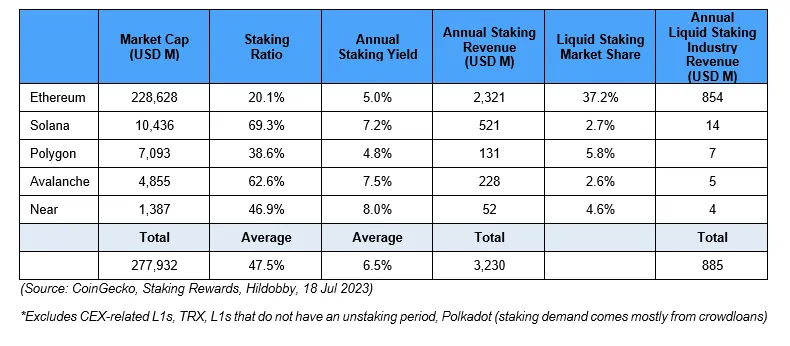

In summary, these drivers have given rise to an industry that generates millions of dollars in revenue annually. The top five PoS smart contract platforms alone generate $893 million in rewards, which belong to liquid staking protocols.

Moreover, compared to other blockchain applications, the quality of this revenue stream is higher due to its repetitiveness. For example, the revenue of decentralized exchanges (DEX) is cyclical and highly dependent on market conditions. Generally, during bull markets, DEX trading volumes are high, while they gradually decrease during bear markets. This leads to unstable revenue sources at the protocol level. Unfortunately, this is also the case for many other blockchain applications—NFT markets see revenue declines during NFT bear markets, and money market revenues decrease with reduced demand for leverage. Therefore, we believe that the stable revenue source of the liquid staking sector is an often-overlooked advantage in a volatile and fast-reacting market.

By comparing the monthly revenues of Uniswap and Lido, the leader in the liquid staking sector, we can easily illustrate the quality of revenue in this sector. Uniswap's monthly revenue peaked twice in May and November 2021, coinciding with the market tops in those months. Subsequently, during the following bear market, monthly revenue gradually declined as trading volume and liquidity decreased.

In stark contrast, Lido's revenue has remained stable over the past few years without significant fluctuations. This indicates the stability of staking income—regardless of market sentiment, as long as the blockchain continues to operate, liquid staking protocols will continue to generate revenue. We believe that an important implication of this phenomenon is that liquid staking protocols should command higher valuation multiples compared to other protocols with cyclical businesses.

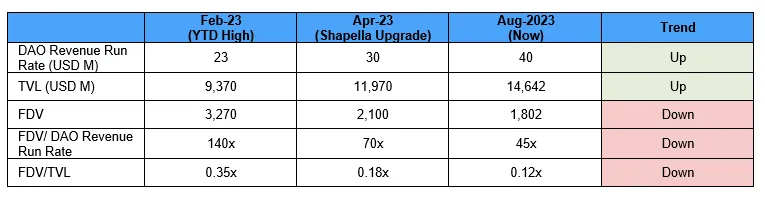

Lido is currently the market leader in the liquid staking space, with a total value locked close to $15 billion. In fact, it is also the DeFi protocol with the highest total value locked across all chains. Lido's ETH receipt token, stETH, is the most liquid staked ETH token and has the greatest composability. We are confident that Lido will continue to grow and leverage its established network effects to solidify its market share.

When assessing the advantages of specific liquid staking protocols, we also consider two additional parameters—1) market share and 2) the proportion of staking rewards captured. In the following sections, we will elaborate on the reasons for the growth of each driver and how they contribute to Lido's continued success.

1. Growth of L1 Token Market Capitalization

Lido will benefit from the growth of the underlying L1 chains it serves, as its total value locked (TVL) in USD is linearly correlated with the prices of these L1 tokens. Currently, Lido is actively serving three chains—Ethereum (98.9% of TVL), Polygon (0.7%), and Solana (0.4%). If these chains continue to grow, their tokens should reflect these fundamentals. Therefore, even if the TVL in token terms does not grow, Lido's TVL in USD will continue to expand.

It is worth noting that Ethereum's growth has a significant impact on Lido's fundamentals. Ethereum is by far the largest smart contract L1 chain, with a market capitalization six times that of the BNB chain and twenty-three times that of Solana. ETH also accounts for the largest share of Lido's TVL.

In this regard, we are particularly optimistic about Ethereum's long-term prospects, having witnessed the successful upgrades of major protocols, such as the London upgrade (EIP-1559—improving the user experience of transaction fees and ETH token economics), the Paris upgrade (PoS—reducing energy consumption and laying the groundwork for scalability upgrades), and the Shanghai/Capella upgrade (ETH withdrawals). From an adoption perspective, Ethereum remains the preferred platform for secure L1 DeFi activities, with applications like Aave and Uniswap enabling users to trade and lend easily. At the same time, it continues to serve as a secure settlement layer for numerous scaling solutions, from zkRollups (Polygon zkEVM, zkSync, Starknet) to Optimistic rollups (Arbitrum, Optimism), facilitating cheap and fast transactions and contributing to ETH transaction fees. Therefore, we believe Lido will derive substantial benefits from this native advantage.

Additionally, we view Lido's multi-chain operations as a bullish option on the growth of alternative L1 chains. We believe that developers and users have different needs that can be met by other chains. From Lido's perspective, servicing these chains is a wise means of decentralized business.

2. Growth of L1 Staking Ratios

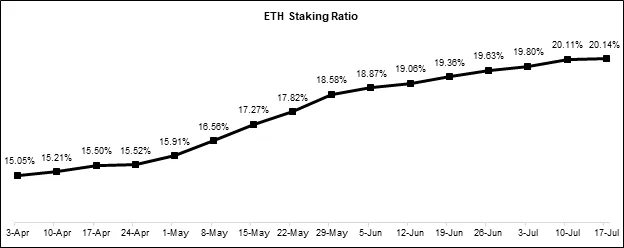

We believe that Ethereum's staking ratio will continue to rise, especially following the successful Shanghai/Capella upgrade. When Ethereum first implemented staking on the Beacon Chain, early stakers did not fully ensure the technical feasibility of their assets and the withdrawal timeline when depositing ETH, resulting in a relatively low staking ratio compared to other PoS chains. With the completion of the Shanghai/Capella upgrade, this risk factor has largely been mitigated, becoming a key driver of the growth in staking ratios. In fact, the staking ratio of ETH has steadily increased from about 15% at the time of the Shanghai/Capella upgrade to approximately 20% today.

We expect the growth in staking ratios to benefit the liquid staking sector, as while staking risks have decreased, users still face the same capital efficiency issues. By converting to Lido's stETH, ordinary ETH holders, who occupy a large portion of the ETH supply, can now enjoy the actual yield of ETH while retaining most of the on-chain composability.

3. Growth of Staking Yields

We acknowledge that, all else being equal, staking yields will compress as staking ratios increase. However, the current level of on-chain activity pales in comparison to historical bull market levels. Any increase in on-chain activity on Ethereum, such as the minting of NFTs and a surge in decentralized trading volume, will drive up transaction fees and MEV. This will help alleviate the compression of base rewards and contribute to the stability of Lido's revenue.

4. Growth of Liquid Staking Market Share

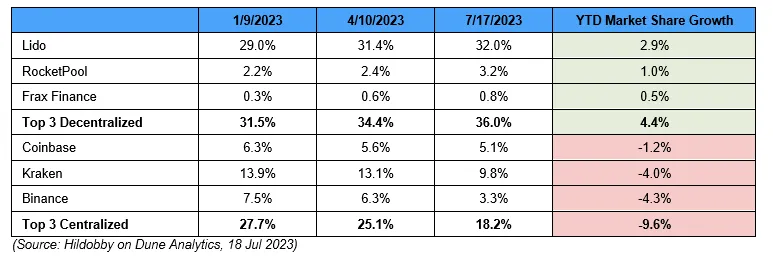

We expect the liquid staking sector to benefit in the context of increased regulatory scrutiny on staking services provided by centralized participants. To date, the top three centralized staking service providers have relinquished 9.6% of market share, a portion of which has been absorbed by their decentralized counterparts. Notably, Lido has been the largest beneficiary of this trend, with its market share increasing by 2.9%. We believe this indicates that due to the liquidity and composability of stETH in DeFi, it remains one of the preferred options for most stakers.

5. Growth of Lido's Market Share

Driven by industry trends, we believe Lido will be able to maintain its dominant market share, thanks to the unique network effects it has built around stETH, which stem from the token's liquidity and composability. Currently, Lido holds 86% of the liquid staking ETH market share, nearly six times that of the second-largest decentralized participant (rETH).

This is due to the power-law dynamics formed around the liquidity and utility of the stETH token. stETH is the most liquid staked ETH derivative on DEXs. On Ethereum alone, the liquidity of stETH/wstETH is approximately $700 million (paired with WETH and ETH), which is eight times that of rETH. Therefore, it can be said that among all alternatives, Lido best achieves the primary goal of liquid staking protocols—providing stakers with optimal liquidity.

With a substantial liquidity foundation established, the liquidity moat of stETH is further strengthened as more use cases for the token are unlocked. One example is using liquid staked ETH as collateral in money market protocols. Liquidity is a key parameter in assessing whether an asset is suitable for use as collateral, as only assets with sufficient liquidity depth can effectively handle asset liquidation. Therefore, it is no surprise that stETH is also the most widely used staked ETH derivative as collateral in money market protocols.

6. Lido's Value Capture

Currently, Lido implements a 5% capture rate on staking rewards, which goes directly into the DAO treasury managed by $LDO token holders. This allows us to easily understand Lido's potential revenue under specific parameters.

Considering all of Lido's value drivers, we believe there is still considerable growth potential in Lido's fundamentals in the medium term. Below, we outline some rough numbers to illustrate Lido's potential market opportunity.

- We expect Ethereum's staking ratio to reach 30% in the next 12 months as users begin to digest the reduced risk of withdrawals.

- In this scenario, staking yields are expected to decline to around 4%.

- Over time, we also believe that liquid staking protocols can capture 50% of the market as users demand capital efficiency for their assets.

- Additionally, if ETH returns to its historical peak price of $4,000 (a market cap of $500 billion), this would imply $3 billion in annual revenue from the Ethereum liquid staking sector alone.

- Assuming Lido's market share in the Ethereum liquid staking market slightly increases to 90%, the annual revenue for Lido DAO could reach $135 million, with a reward capture rate of 5%.

- This means that under Lido's current fully diluted valuation of $1.8 billion, the forward FDV/Revenue ratio would be 13.5 times.

Final Thoughts

Once again, we are optimistic about the prospects of the liquid staking sector, as leading projects provide unique value propositions for the large and growing market they serve. We further outlined four key drivers supporting the growth of the industry and detailed how each metric can further expand.

We also discussed how Lido will continue to dominate market share, driven by the strong network effects it has established around stETH, stemming from the liquidity and composability of the token. If our view on mid-term growth in the industry proves accurate, we have demonstrated that Lido has a five-fold revenue growth opportunity from here.

In the short term, the market seems to have shifted from the initial hype surrounding the Shanghai/Capella upgrades. This is evident from the rise in Lido's total value locked (TVL) and revenue growth rate, while valuation multiples have compressed. We believe this divergence between valuation and fundamentals will not last forever, and LDO now offers some of the best risk-adjusted returns.