Blofin: Q1 2024 Bitcoin and Ethereum Price Research, as well as Predictions for Highs and Lows

Since BTC is a product of the cyber universe, the central bank's liquidity manipulation magic is ineffective against it. The dollar price of BTC may fluctuate, but 1 BTC is always 1 BTC. Native crypto investors use BTC as an investment and a store of value to combat inflation under fiat currency standards.

Since BTC is a product of the cyber universe, the central bank's liquidity manipulation magic is ineffective against it. The dollar price of BTC may fluctuate, but 1 BTC is always 1 BTC. Native crypto investors use BTC as an investment and a store of value to combat inflation under fiat currency standards.Author: Matt Hu, Blofin CEO & Griffin Ardern, Blofin Macro Trader

Source: Wu Says Blockchain

"Institution's Darling": Why BTC?

In the contemporary financial system, central banks are the source of liquidity in financial markets. When central banks begin to release or tighten liquidity, the changes in liquidity are reflected in real-time in the price movements of bonds, commodities, foreign exchange, and financial derivatives, as well as in stock indices. Bitcoin, as a new member of the "macro club," has not been around for long. However, the U.S. government holds the most Bitcoin; the number of ETFs incorporating Bitcoin into their portfolios is also gradually increasing, with issuers including top asset management firms like Fidelity.

Bitcoin ETF list and holdings as of July 17, 2023. Source: Bitcoin Treasuries

Compared to other cryptocurrencies, BTC is truly decentralized. The story of Satoshi Nakamoto is well-known, but no one knows "who he really is." However, "who he is" may no longer matter; the Bitcoin network has matured, and any individual's influence on the Bitcoin network can be ignored—this "true decentralization" attribute is also one of the characteristics of a qualified macro investment target. Gold and minerals are generated from the universe; agricultural products are produced by nature; Bitcoin comes from algorithms and the cyber universe formed by information.

Since BTC is a product of the cyber universe, the central bank's liquidity manipulation magic is ineffective on it. The dollar price of BTC may fluctuate, but 1 BTC is always 1 BTC. Native crypto investors regard BTC as an investment and a store of value to combat inflation under fiat currency standards.

For fund managers from traditional markets, they pay more attention to the role BTC plays in diversifying risk. The price performance of BTC has never reached a "strong correlation" level with gold, and its correlation with U.S. stock indices has also dropped to near 0 in 2023. At the same time, since BTC belongs to a completely different major asset class, this means BTC can diversify the overall risk of a portfolio to some extent. The compliance of BTC is also widely recognized; this greatly reduces the legal risks of investing in BTC.

BTC and gold 90-day price correlation changes from July 2020 to present. Source: CoinMetrics

BTC price correlation with U.S. stock indices from January 2021 to present. Source: Block Scholes

Macro hedge fund managers are more concerned with liquidity. Their strategies typically invest in bonds, foreign exchange, commodities, stock indices, etc., and they tend to trade through derivatives rather than based on spot. "Liquidity" is the core reason—macro trading requires accurately grasping the timing of liquidity changes and entering and exiting at the fastest speed and lowest cost. As an emerging asset, with the global liquidity of the Bitcoin network and a rich array of derivatives, BTC's liquidity can rival that of foreign exchange.

More importantly, due to the high speed and low transaction costs brought by the Bitcoin network and crypto infrastructure, traders can deploy and exit liquidity within seconds, without needing to negotiate constantly with numerous third-party institutions over the phone or waiting for bids to be accepted in illiquid over-the-counter trading systems. These advantages make BTC more sensitive to market sentiment and macro event changes, reflected in its price volatility and volatility changes.

BTC price changes from January to July 2023. Source: blofin.com

Note the purple sections in the chart, corresponding to the March banking crisis, May Fed rate hikes, and the submission of BTC spot ETFs around July.

BTC DVOL volatility index compared to realized volatility levels from May 2021 to present. Source: Amberdata Derivatives

It is not difficult to see that the BTC volatility index is sensitive to macro changes.

BTC DVOL volatility index compared to "volatility of volatility" levels from August 2022. Source: Amberdata Derivatives

Compared to volatility, BTC's volatility changes are more rapid and sensitive.

In summary, whether it is crypto believers, fund managers from traditional markets, or macro hedge fund traders, BTC meets the requirements of different types of investors in terms of utility, compliance, risk management, liquidity, and trading. It is hard to find a macro target that can satisfy all these demands at once; in other words, BTC is a natural macro trading target.

ETH: A "Software Company" with a P/E Ratio of 312.58

Investors in the crypto market like to compare BTC and ETH; in terms of market capitalization, BTC and ETH rank first and second in the cryptocurrency market capitalization leaderboard, and every crypto trader will be involved with these two cryptocurrencies. However, investors from traditional markets are more cautious about ETH: regardless of the potential compliance risks of ETH, considering the influence of Ethereum's founders and developers on the development of the Ethereum blockchain, as well as Ethereum's "smart contracts as a service" model, it resembles a "software company" similar to IT giants like Amazon and Microsoft, rather than a "pure liquidity container" like the Bitcoin network.

In fact, some researchers and traders have begun to interpret ETH using a corporate finance framework:

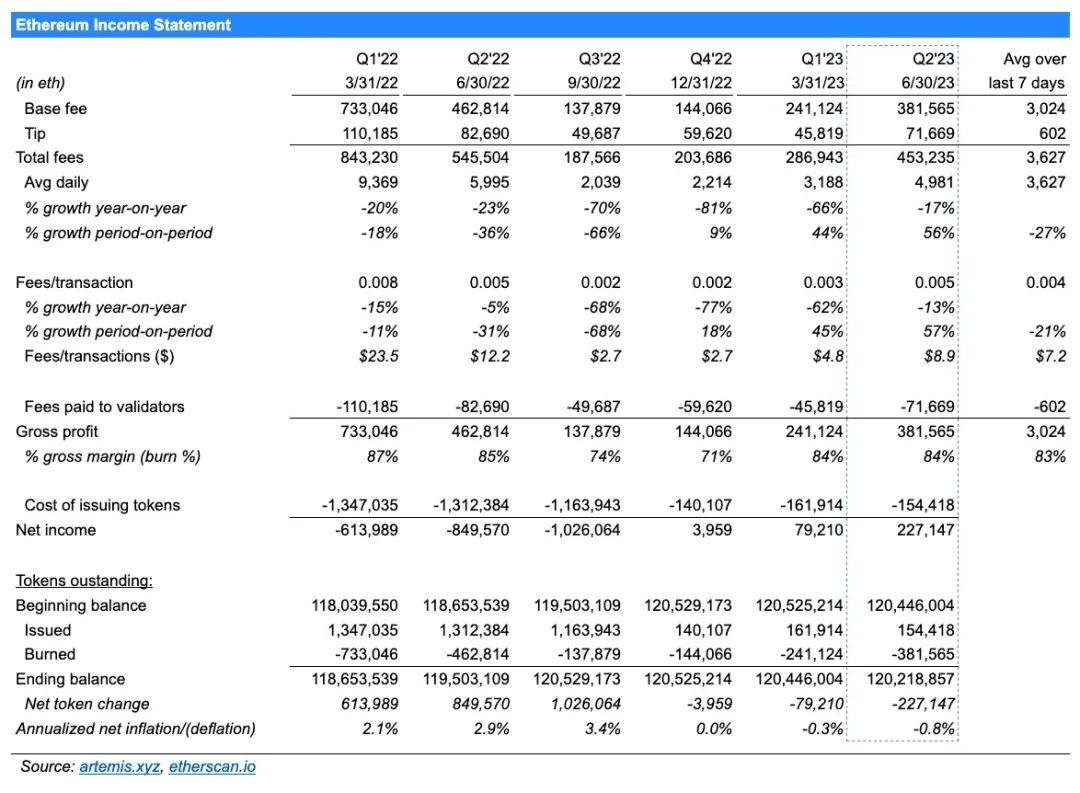

Ethereum Profit and Loss Statement. Source: artemis.xyz

Thus, analyzing ETH using a framework based on stock fundamentals seems reasonable. Fortunately, due to the transparency of blockchain itself, obtaining real-time supply and price of ETH is not difficult. Similarly, with the efforts of researchers like Sam Andrew, we have also obtained a relatively feasible way to understand the financial situation of the Ethereum network. Let's estimate the current P/E ratio of Ethereum:

Calculating from the official introduction of PoS, from Q4 2022 to Q2 2023, the total profit of the Ethereum network (in USD) is: (3,9591,301) + (79,2101,589) + (227,147*1,861) = 553,735,916 USD, equivalent to an annualized profit of approximately 738,314,555 USD;

The spot average price of ETH (July 17) is approximately 1,920 USD;

The real-time supply of ETH (July 17) is approximately 120,201,013;

Therefore, the P/E ratio of ETH = 1,920 / (738,314,555 / 120,201,013) = 312.58.

312.58! This is an astonishing P/E ratio figure. We provide the P/E ratios of the Magnificent 7 (the seven largest tech stocks by market capitalization) in the U.S. stock market for comparison*:

AAPL: 32.38

AMZN: 164.24

ETH: 312.58

GOOGL: 27.93

META: 38.32

MSFT: 36.92

NVDA: 207.62

TSLA: 82.76

*: All stock P/E ratios are calculated based on the closing prices on July 14. ETH's P/E ratio is based on the intraday average price on July 17.

Undoubtedly, Ethereum, as a "software company," significantly exceeds our original expectations. Considering its lack of dividends and its current phase of rapid growth post-transition to PoS, such a high P/E ratio is similar to NVDA under the influence of AI; compared to AMZN's P/E ratio, as a core infrastructure provider in the crypto industry, ETH's high P/E ratio is also understandable. Overall, investors have given ETH a high valuation, anticipating the infinite possibilities of ETH's future development.

However, while Ethereum can fully align with corporate logic, BTC and ETH have officially embarked on different paths.

Parting Ways

Under the narrative of "Crypto 3.0," where will BTC and ETH head?

BTC: Crypto Is Macro

There is no doubt that the price of BTC will depend on changes in the macroeconomic situation and the internal macro conditions of the crypto market. Therefore, for BTC, interest rates and market share will be important influencing factors. Interest rates affect profit expectations, while market share affects market capitalization.

• From the interest rate market perspective, the Federal Reserve is unlikely to cut rates in the next six months; the European Central Bank will also not show weakness under high inflation threats. This situation means that high interest rates will continue to suppress BTC's performance. However, some potential positive factors are also supporting BTC's price, such as the possible listing of BTC spot ETFs.

The Fed's latest possible interest rate path as of July 17, 2023. Source: CME Group

• In addition, the internal distribution of liquidity in the crypto market will also affect BTC's price and market capitalization. From early 2021 to the end of 2022, influenced by the bull market and "altcoin season," BTC's market share gradually decreased from over 60% to between 40% and 45%. Subsequently, benefiting from institutional buying and the return of liquidity, BTC's market share began to rebound from January 2023. By July 2023, BTC's market share was approximately 50%.

Changes in the market share of mainstream cryptocurrencies as of July 17, 2023. Source: Coinmarketcap

• At 0% interest rates, the total market capitalization of the crypto market was about 3 trillion USD. At 5.25% interest rates, the total market capitalization of the crypto market is about 1.2 trillion USD—approximately 40% of the peak. From November 2021 to March 2022, due to the Fed's expectation management, the crypto market lost about 1 trillion USD in market capitalization. In March, the Fed raised rates by 25 basis points, at which point the total market capitalization of the crypto market was about 2 trillion USD—67% of the peak.

• Considering that the Fed is not expected to implement the unlimited quantitative easing policy of 2020-2021 in the coming years, the market capitalization changes in the crypto market due to expectation changes will not exceed 1 trillion USD at most.

Changes in the total market capitalization of the crypto market as of July 17, 2023. Source: Coinmarketcap

Let's expand based on the above logic:

• Considering the current lack of external liquidity entering the crypto market, we assume that BTC's future price will depend entirely on interest rates and changes in market expectations, reflected in changes in market share.

• Under the scenario of sustained high interest rates at 5.25% and a lack of external liquidity entering, it will be difficult for the total market capitalization of the crypto market to see significant increases before January 2024. Even if "expectations lead," in the most optimistic scenario, the internal market capitalization growth brought by expectations will not exceed 500 billion USD.

• The total supply of BTC is approximately 19.43 million coins, and there will not be a significant change of more than 5% in total supply within a year.

Let's consider three scenarios:

1. Investors have no further expectations, and internal market capitalization growth in the crypto market is limited. The total market capitalization of the crypto market will stabilize between 1.2 trillion and 1.4 trillion USD, and BTC's market share will not change significantly, maintaining around 50%. This means BTC's market capitalization will fluctuate between 600 billion and 700 billion USD, with prices fluctuating between 30,880 and 36,026 USD;

2. BTC spot ETF is approved, bringing good expectations for investors. The market capitalization of the crypto market rebounds to around 1.5 trillion to 1.6 trillion USD.

If BTC's market share does not increase, BTC's market capitalization will stabilize around 750 billion to 800 billion USD, with prices potentially reaching 41,173 USD at their peak; even if the rebound is not strong, BTC's price will still be above 38,500 USD;

If the approval of the spot ETF leads to an increase in BTC's market share to 60%, in the best case, BTC's market capitalization will reach 960 billion USD, with a unit price exceeding 49,400 USD; even if the overall rebound of the crypto market is not strong, BTC's market capitalization will return to 900 billion USD, with a unit price reaching 46,300 USD.

3. Expectations of rate cuts combined with positive expectations from the spot ETF and Bitcoin halving drive a full return of liquidity in the crypto market, with the market capitalization rebounding to over 1.7 trillion USD.

If BTC's market share does not increase, BTC's market capitalization will exceed 850 billion USD, with prices rebounding to over 43,700 USD;

If BTC's market share increases to 60%, BTC's market capitalization will exceed 1.02 trillion USD, with prices reaching around 52,500 USD.

In summary, macro factors are relatively favorable for BTC, and the ultimate price level BTC can reach depends on interest rates and market expectations.

ETH: "How to Be a More Profitable Company"

Considering that BTC has become the protagonist of the macro narrative, it may be wiser for ETH to focus on applications. Therefore, for ETH, the factors influencing its price mainly come from its new narrative and whether it can achieve further widespread application in the future. Since these factors will be reflected in the net income of the Ethereum network, we can infer possible price changes for ETH based on changes in the P/E ratio.

Similarly, let's consider three scenarios:

- The Cancun upgrade significantly enhances Ethereum's Layer 2 speed and reduces transaction costs, driving an explosion in the Ethereum Layer 2 ecosystem. The profitability of the Ethereum network continues, with quarterly revenue rising by 50% before the Cancun upgrade and doubling net income per quarter after the Cancun upgrade.

Assuming the P/E ratio of ETH does not change significantly, strong investor expectations keep the P/E ratio around 300. The net income for Q2 2023 is 423 million USD, Q3's net income is 635 million USD, and Q4's net income is 953 million USD. In this scenario, the total revenue of the ETH network for 2023 will reach 2.137 billion USD. Considering ETH's deflation will reduce the total supply to 120 million, the average price of ETH at the beginning of 2024 may exceed 5,300 USD and break through 9,700 USD in the first quarter after the Cancun upgrade.

If investor expectations are relatively neutral, causing the P/E ratio of ETH to fall to around 150 (close to comparable companies like AMZN), in this scenario, the average price of ETH at the beginning of 2024 will be around 2,670 USD and approach 4,900 USD in the first quarter after the Cancun upgrade.

- The profitability of the Ethereum network is relatively stable, with quarterly revenue rising by 25%, and the first quarter after the Cancun upgrade sees a 50% increase compared to Q4 2023.

- Assuming the P/E ratio of ETH does not change significantly, strong investor expectations keep the P/E ratio around 300. The net income for Q2 2023 is 423 million USD, Q3's net income is 529 million USD, and Q4's net income is 661 million USD. In this scenario, the total revenue of the ETH network for 2023 will reach 1.739 billion USD, and the average price of ETH at the beginning of 2024 may exceed 4,300 USD and break through 6,500 USD in the first quarter of 2024. If the P/E ratio falls to around 150, the average price of ETH at the beginning of 2024 may be around 2,150 USD and break through 3,200 USD in the first quarter of 2024.

- The profitability of the Ethereum network shows marginal diminishing returns, with revenue increases of 20% and 15% in Q3 and Q4, respectively, and the benefits brought by the Cancun upgrade only curbing the trend of diminishing profitability in the first quarter.

- Assuming the P/E ratio of ETH does not change significantly, strong investor expectations keep the P/E ratio around 300. The net income for Q2 2023 is 423 million USD, Q3's net income is 508 million USD, and Q4's net income is 584 million USD. In this scenario, the total revenue of the ETH network for 2023 will reach 1.641 billion USD, and the average price of ETH at the beginning of 2024 may exceed 4,100 USD and break through 5,400 USD in the first quarter of 2024. If the P/E ratio falls to around 150, the average price of ETH at the beginning of 2024 may be around 2,050 USD and break through 2,700 USD in the first quarter of 2024.

In summary, ETH's development is highly correlated with its own profitability. The combination of narrative support and sustainable, continuously growing profitability is key to driving ETH's price increase—this is distinctly different from BTC.

Junction

In fact, the "parting ways" in the crypto market is not only theoretical but also exists not just between BTC and ETH. Statistics show that in 2023, not only has the correlation between BTC and ETH significantly decreased, but the correlation between BTC and mainstream altcoins has also significantly decreased. BTC seems to be charting its own course, while the correlation between ETH and different types of coins like XRP, LTC, and BNB is also weakening, but it still maintains a solid correlation with public chain coins like ADA and project tokens like CRV that are deeply rooted in the Ethereum public chain.

As the correlation between coins continues to weaken, the previously fully or partially reusable analytical logic and trading strategies become ineffective. Pair trading no longer shows the ideal correlation return, and the general investment framework based on market capitalization and sectors is also becoming less applicable—this means that further analysis based on the fundamentals of the projects themselves becomes more important.

Changes in the correlation of BTC with other major cryptocurrencies excluding ETH as of June 2023. Source: Kaiko

Changes in the correlation of ETH with other major cryptocurrencies excluding BTC as of July 2023. Source: CoinMetrics

It is time to adopt two or even multiple completely different logics to view the crypto market. The Crypto 3.0 version has arrived; the times are advancing. Bitcoin will become more closely integrated with the macro economy and traditional markets, while Ethereum needs to become a "great company"; other cryptocurrencies must also find their own paths. In the rapidly changing macro and micro structures of the crypto market, we need to keep pace with the times.