Layer1 Transforms into Layer2: A Discussion on the Business Behind "Ethereum Layer2"

Doing L2 seems to have become a trend recently. From emerging projects to established public chains, there is active exploration and implementation of L2 solutions.

Doing L2 seems to have become a trend recently. From emerging projects to established public chains, there is active exploration and implementation of L2 solutions.Author: David, TechFlow Research

Doing L2 seems to have become a trend recently.

From emerging projects to established public chains, everyone is actively exploring and implementing L2 solutions.

On July 17, the modular L2 solution Mantle Network, incubated by BitDAO and using Optimistic Rollup, launched its mainnet;

On July 18, the L2 solution Linea developed by Consensys, the parent company of MetaMask, also opened its mainnet Alpha version;

Earlier, Coinbase also announced the test network for its L2 solution BASE.

Recently, even the established public chain Celo released a proposal in its internal forum, calling for a shift in its development direction from an independent Layer 1 public chain to an Ethereum-compatible L2 solution.

I vaguely remember the new public chain competition two years ago, where various factions appeared as "Ethereum killers," trying to "take down" Ethereum; now, the rush to do L2 seems more like "Ethereum Builders," aiming to "share" Ethereum's performance issues through technical optimization.

I vaguely remember the new public chain competition two years ago, where various factions appeared as "Ethereum killers," trying to "take down" Ethereum; now, the rush to do L2 seems more like "Ethereum Builders," aiming to "share" Ethereum's performance issues through technical optimization.

These are two completely different approaches: the former is direct competition, while the latter is an elegant parasitism.

Now, why is everyone so keen to embrace L2, while the phenomenon of clustering around new public chains has diminished? Is it that new public chains are no longer appealing, or can L2 indeed bring new narratives and benefits?

L2, a business with quicker returns

We won't elaborate on solutions like Mantle and Linea that are aimed at L2 from the start; their external narrative is simply about improving ETH's scalability and reducing costs to create a better interactive experience for applications and users.

On the other hand, Celo, which is originally an L1 public chain, choosing to do L2 gives an initial impression of "compromise and regression" ------ public chains competing with ETH are trying to solve Ethereum's shortcomings through a "no pain, no gain" approach, claiming "I can do it better"; yet, choosing to become an L2 of Ethereum seems to imply a sense of surrender and joining.

To understand the reasons behind this, let's first see what Celo has to say:

The benefits brought by compatibility, security, and liquidity are undeniable, but I believe it does not touch upon the core interest: what exactly determines a project's choice to either independently pursue an L1 or leverage Ethereum's ecosystem through L2 to carve out a niche?

The answer is cost and benefit.

An article from Lightning HSL titled “Doing Rollup is a Good Business” provides a very good business perspective: whether developing L1 or L2, it is all about solving existing problems and creating value. However, from a commercial standpoint, L2 seems to be more profitable.

Business Model: L2 --> Equivalent functionality to ETH main chain --> Lower gas fees, faster speeds --> Attract dapps and users --> Increase on-chain transaction volume;

L2 Revenue: Gas fees paid by users for transactions on the L2 chain;

L2 Expenses: L2 operators periodically batch and upload Rollup transactions to Ethereum L1, incurring gas fees;

The difference between revenue and expenses represents the approximate gross profit of operating the L2 rollup model; therefore, the more applications and TVL on L2, the more potential user transactions can be generated, allowing L2 operators to increase revenue while keeping expenses relatively fixed, thus improving profits.

In terms of costs, Rollup does not require the development of a complex consensus mechanism, and theoretically does not need a token (even though current projects may have one); it only requires a single server to start running, with the core technical components built using Optimistic or Arbitrum, equivalent to having a complete open-source solution, making it certainly easier than independently developing an L1.

In contrast, the cost and difficulty of developing a new public chain (L1) are much higher:

First, you need to develop a consensus mechanism that the market can accept, which requires substantial R&D resources, time, and accumulation;

Second, you need to attract enough nodes to participate in your network to ensure its security and decentralization;

Finally, you need to build some differentiated narratives, such as focusing on privacy or security…

At the same time, data also supports the cost-benefit analysis.

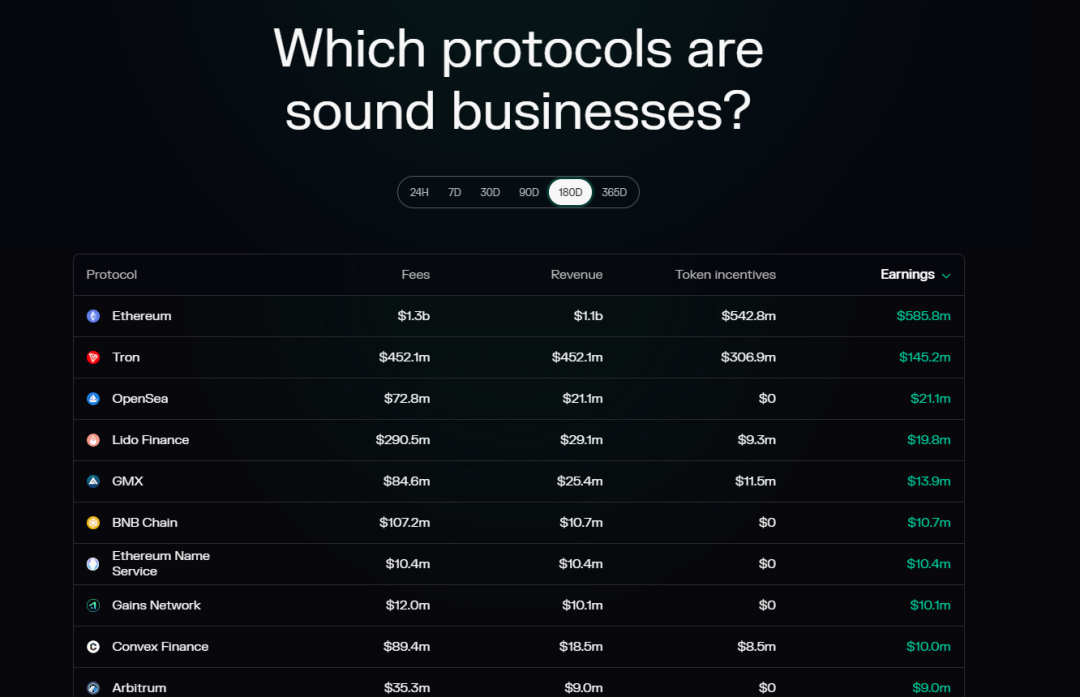

Data from Token Terminal shows that in the past six months, the top ten projects by revenue, if only looking at the public chain layer, only Ethereum, Tron, and BNB Chain made the cut, while Arbitrum from L2 also ranked in this list. Considering the comparison of the construction time of these L1s and Arbitrum, it is evident that Arbitrum offers a better cost-performance ratio in terms of pure revenue.

Additionally, in a bear market environment, it is harder to tell stories to VCs for funding, and retail investors are less likely to buy in; creating a new L1 inevitably faces twists and turns from the primary market to the secondary market, and project teams themselves find it increasingly difficult to monetize tokens through capital markets, making this path to profitability clearly more challenging than developing an L2.

Rather than starting from scratch to create a unique public chain, which requires a large investment and yields slow results, it is more practical and cost-effective to leverage L2 that is parasitic on Ethereum, requiring less investment and yielding relatively quicker results.

More importantly, there is the "traffic business," which refers to where users come from.

As mentioned earlier, TVL and transaction volume are key to whether L2 can generate revenue, which relies on the influx of more users.

When Coinbase, MetaMask, or Binance develop L2, they can naturally bring their existing users from their CEX or wallet services into L2 through product integration, giving them an incomparable advantage in customer acquisition costs;

Similarly, L1s like Celo transitioning to L2 can also migrate existing users from L1, although this may require more incentives and guidance.

However, regardless, projects and capital choosing to do L2 mostly start from their own product ecosystems or the existing user base within the Ethereum ecosystem, and then expand into more collaborative scenarios (such as Polygon's actions in the Web2 space).

Is L1 a Dead Sea, while L2 is nearing a Red Sea?

The above analysis only looks at some internal characteristics of L1 and L2, but from the perspective of the external competitive environment, choosing to do L2 becomes easier to understand.

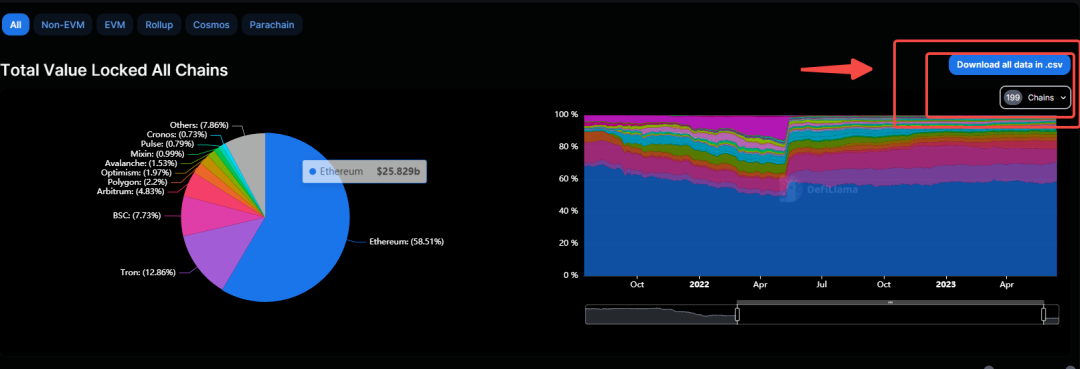

Data from DeFiLlama shows that there are currently nearly 200 public chains on the market. Excluding the dozens of L2s included, this roughly means we are facing nearly 190 L1 public chains.

Therefore, the current L1 track resembles a Dead Sea: the salinity (density) is too high, and competition is fierce.

There are only a few public chains occupying user mindshare, and with the black swan events and capital withdrawals in recent years, many once-popular public chains have disappeared from various metrics such as user activity, revenue composition, and transaction volume.

Most L1s still have their concepts, but they are not thriving. Choosing to jump into the Dead Sea from a business perspective is not a wise choice.

In contrast, the situation for L2 is somewhat better.

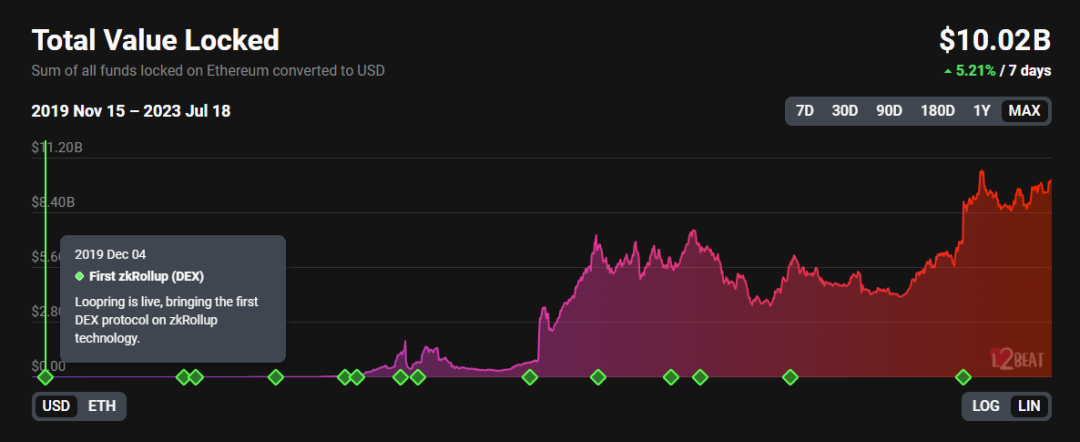

The total TVL of L2s, when viewed over a longer time frame, is still on an upward trend;

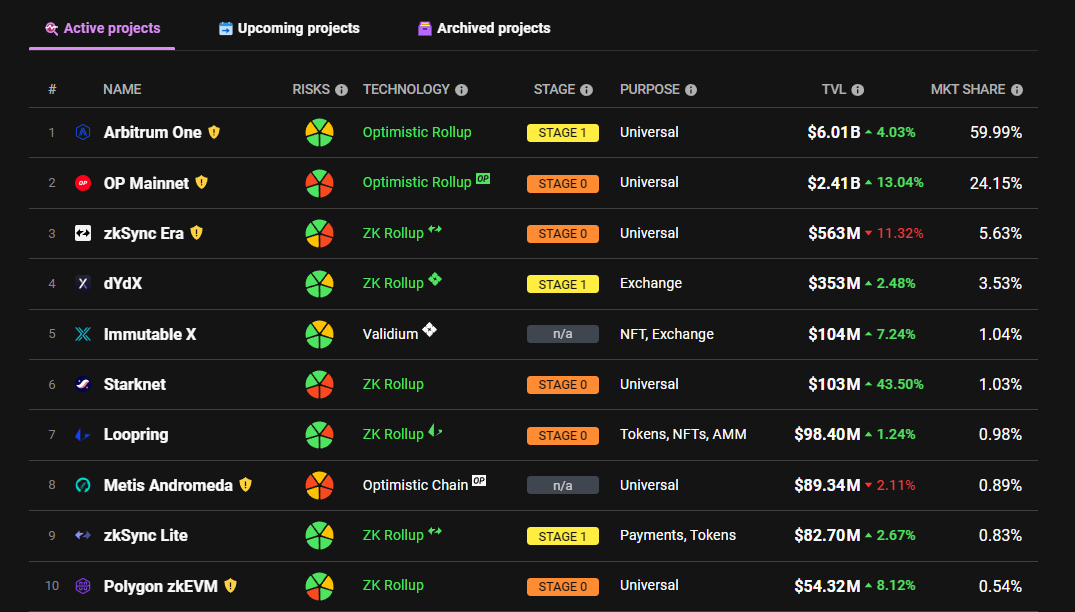

In terms of competitive landscape, L2Beat currently tracks 26 L2s, meaning the competitive pressure is about one-seventh that of L1. While the market share has seen Arb and OP as the two major players, the market share of other projects is relatively scattered and average, providing a greater opportunity for another major player to emerge.

In terms of competitive landscape, L2Beat currently tracks 26 L2s, meaning the competitive pressure is about one-seventh that of L1. While the market share has seen Arb and OP as the two major players, the market share of other projects is relatively scattered and average, providing a greater opportunity for another major player to emerge.

However, considering the technical architecture, different technology stacks of L2s in the existing market already have typical representatives:

Optimistic rollup solutions like OPtimism and Arbitrum;

Zk-Proof solutions like Zksync and Starknet;

Base, built on OP Stack;

Linea, an EVM-compatible chain launched by Consensys;

Zk-EVM launched by Polygon, etc….

While it may not be a blue ocean, there are still opportunities compared to L1.

With the completion of Ethereum's technical upgrades this year and several subsequent upgrades, the narrative focusing on performance will persist for a long time, and L2s still have a considerable development window; moreover, there are not many narratives and tracks that can maintain heat during a bear market, giving L2s an advantage in continuous attention amidst a scarcity of attention and funds.

Therefore, from the perspective of competitive landscape and external environment, doing L2 currently seems to be a profitable business.

Who does the L2 business serve?

Beyond business, I sense a kind of "redundancy" within the circle.

We often see a project migrating from one L1 to another, or from supporting one L2 to supporting multiple L2s. Projects are hopping chains while the number of chains continues to grow.

Switching ecosystems allows for another round of resource gathering and user acquisition. L1s and L2s, to some extent, resemble undeveloped colonies; ignoring the technical differences, the same business can be replicated in a different location.

Do we need so many "places"? Who do all these places serve?

Capital needs, yield farming needs, scams need, narratives need… only normal demand may not be necessary.

If all L2s indiscriminately talk about lower fees and faster speeds, what is their essential difference?

After all, for the end user, the technical process is not important; when the usage results are the same, increasingly competitive L2s can serve as substitutes for each other.

History shows that after a round of the new public chain movement, Ethereum remains the same Ethereum, and has even grown stronger in competition.

Will the current state of L2 be the same? From blue ocean to red sea to dead sea, after a round of cash splashing, the density of projects increases, and ultimately only one or two remain on the surface, while the number of users in the pool may be minimal.

The L2 business can yield quick results, but hopefully, it won't exhaust the resources.

Risk warning

Risk warning Risk warning

Risk warning