OKX Ventures: Embracing All Markets, How RWA Helps DeFi Devour the World

Deconstructing and analyzing the RWA track to further explore the integration and evolution trends of DeFi and TradFi.

Deconstructing and analyzing the RWA track to further explore the integration and evolution trends of DeFi and TradFi.Author: *Sally Gu, * OKX Ventures

The content of this article is provided by OKX Ventures researcher Sally Gu and does not constitute any investment advice. Please cite the source when quoting, and contact the OKX Ventures team for reprints.

Introduction Primer

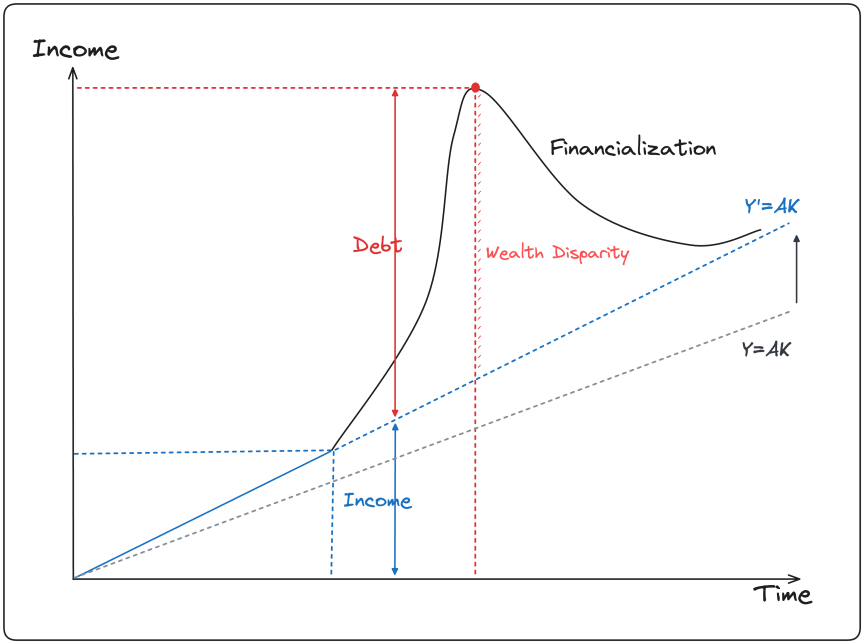

The impact of the pandemic, coupled with the Federal Reserve's consecutive interest rate cuts after Powell took over from Yellen, has led the market to reach the largest bubble phase in financial assets since World War II under conditions of high inflation and low real interest rates over the past few years. However, the fundamental basis of globalization that has existed for the past 40 years has begun to unravel due to the China-U.S. trade war, the Russia-Ukraine standoff, and the rise of populist forces in Europe. The financial wealth effect created by liquidity easing and high leverage since 2018 is now gone, and under the trend of inflation at the bottom of social wages and deflation at the top, the excess returns generated from valuation expansion due to declining interest rates seem to be irreversibly heading towards mean reversion.

Source: TS Lombard

Source: Bloomberg

Therefore, after a prolonged interest rate hike cycle, with U.S. Treasury yields maintaining a deep inversion of over 50 basis points, and the decline of purely virtual financial narratives such as Metaverse PFP NFTs due to a lack of intrinsic value support, DeFi, or the crypto economy, may be embracing real assets and TradFi from a virtual to a real perspective, which could be a natural response during a recession and deleveraging cycle.

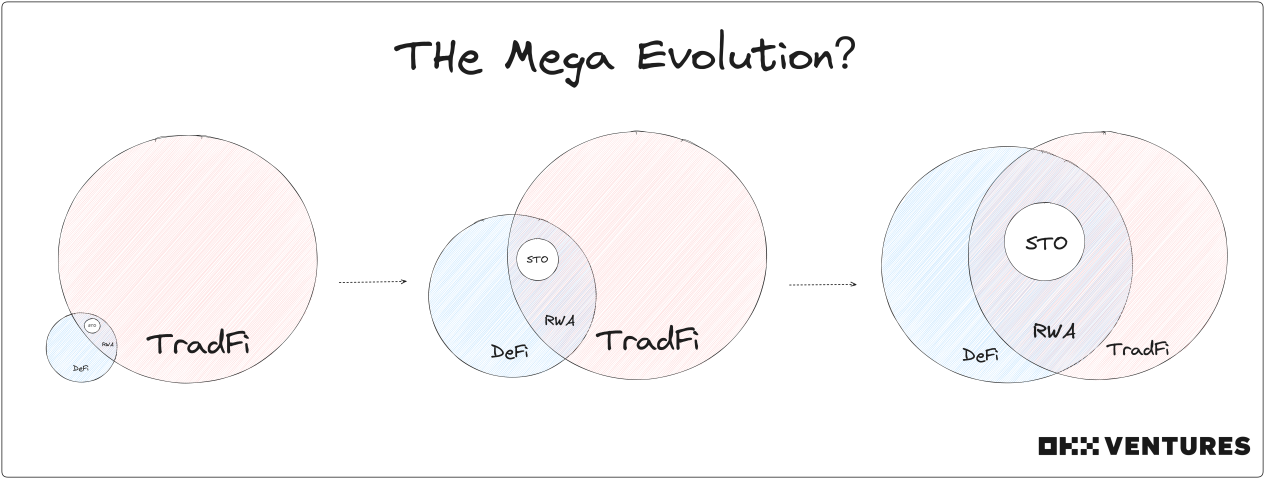

To further explore the trend of the integration and evolution of DeFi and TradFi, we have conducted a simple analysis of the increasingly discussed RWA (Real World Assets) sector below.

TL; DR

Logic:

- TradFi Perspective: Reduce transaction costs, improve transaction transparency and capital circulation efficiency; enhance the composability of financial primitives, provide more hedging tools; activate potential funds from speculators and institutions.

- DeFi Perspective: Support and amplify DeFi speculative loops; introduce massive liquidity, expand the DeFi user base; the stablecoin market has already been validated.

- Development Drivers: Macroeconomic cycles prompt funds to flow back to U.S. dollar-denominated assets, increasing interest from traditional institutions, and the crypto market needs to attract new users.

- Development Resistance: Uncertain regulatory environment, limited traction, and a scarcity of high-quality underlying assets.

- Evaluation Dimensions: Product fundamentals, risk control capabilities, protocol mechanisms, and partners.

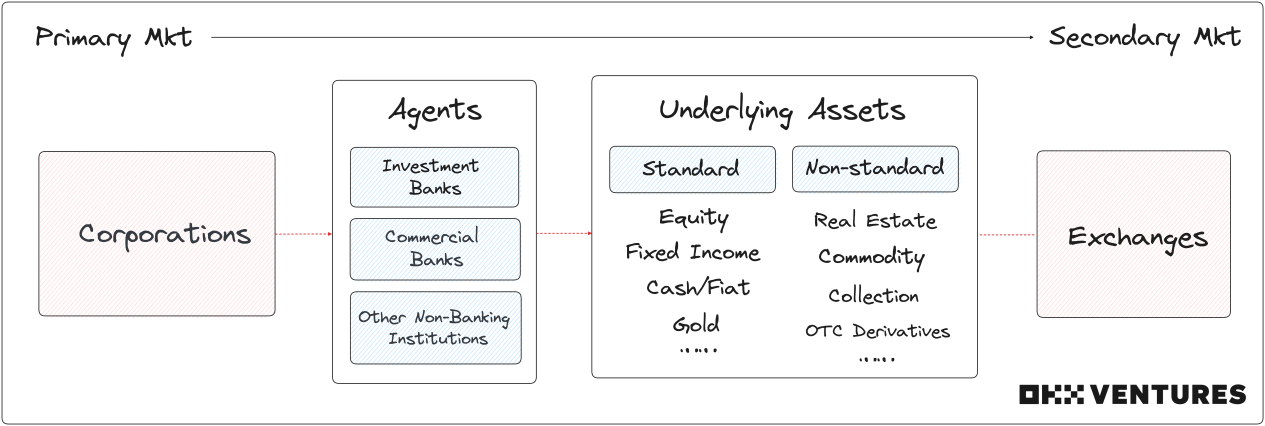

Classification:

- By Asset Form: Standardized, Non-standardized.

- By Asset Category: Fiat currency, Fixed income (bonds, credit), Equity, Alternative (real estate, collectibles, commodities).

- Mentioned 46 Projects: Centrifuge, ONDO, Maple, OpenEden, BondbloX, FortunaFi, CredeFi, Goldfinch, TrueFi, Defactor, Credix, Clearpool, Bru Finance, Resource Finance, Backed Finance, Sologenic, Swam, AcquireFi, Horizon Protocol, Hamilton Lane, RealT, Parcl, LABS Group, Propy, Atlant, ELYSIA, Tangible, Blocksquare, Milo, Figure, LandShare, Lingo, HOME Coin, Theopetra, EktaChain, Robinland, Homebase, 4K, Arkive, mattereum, Codex Protocol, PAX Gold, Tether Gold, Cache Gold, Agrotoken, LandX.

Views:

- Currently, most RWA products struggle to find PMF: In the short term, it is more about narrative FOMO rather than genuine breakthrough innovation or strong growth momentum; closely monitor the dynamics of compliance policies in the U.S., Hong Kong, and Singapore to minimize policy risks.

- Alternative assets & non-standard RWA protocols are emerging: Non-standard assets can be tokenized on-chain using erc721/1155, and erc20 may not become mainstream in the future, as there is significant imagination space for note NFTs, RETIs NFTs, and collectibles NFTs.

- Government bond RWA will remain mainstream, while equity RWA is gaining attention: U.S. Treasury bonds have gained consensus recognition from the crypto community; the demand for equity-like RWA is real, but faces numerous compliance hurdles.

- Recognition from the crypto community is key, and collaboration with native communities is harder to achieve: The challenge for fixed income RWA lies in connecting the loan side; DeFi DAO members have significant differences in their understanding of off-chain assets, and overly complex off-chain assets are difficult for the community to comprehend.

- Points worth discussing and further researching: On-chain Ponzi schemes like RWA Fi, RWA options trading, etc.; verification of on-chain middleware, SaaS companies, compliant issuers, and intermediaries facilitating lending and borrowing like IX Swap, Stima, Castle, Curio, etc.

Basic Concepts

- RWA------ Tokenization of real assets on-chain.

- STO------ Corporate bond financing.

Difference: RWA asset categories are richer, spanning both primary and secondary markets, and the yield gradient can be more extensible.

Market Data

- The latest data shows that RWA has climbed into the top 10 in the DeFi TVL rankings, with a year-to-date growth of 257%.

Source: Defillama

Source: Defillama

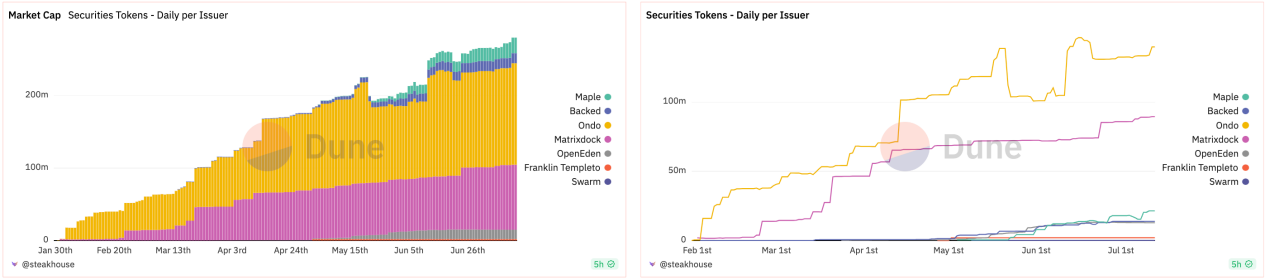

- Since January this year, the overall market capitalization and daily issuance of government bond RWA tokens have steadily increased, with the total market capitalization of the leading seven projects nearing $300M.

Source: Dune

Source: Dune

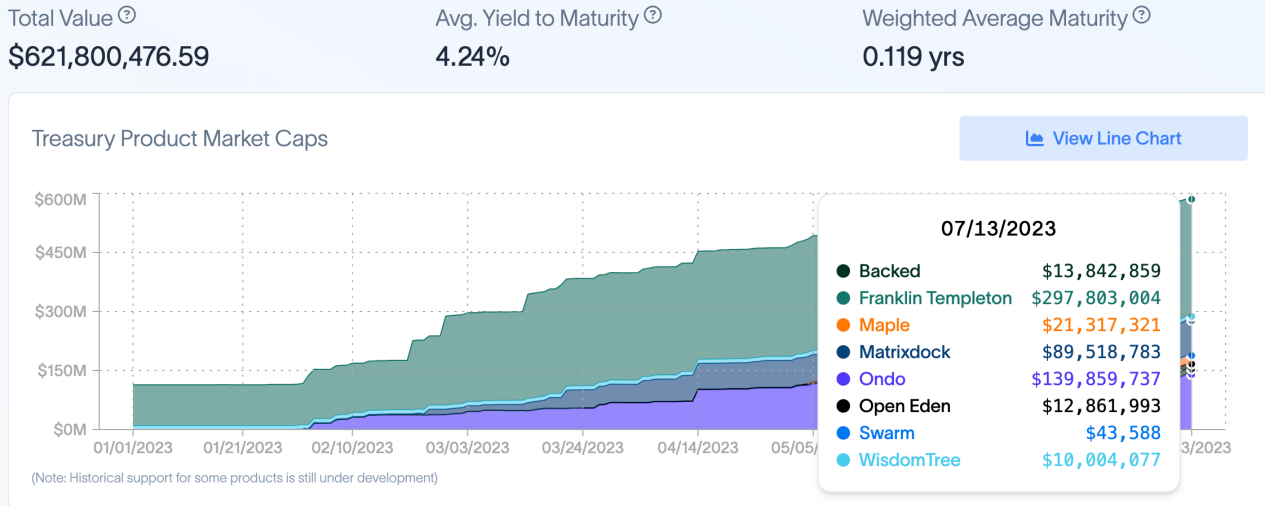

- The total value of U.S. Treasury RWA tokens has exceeded $600M, and the number of RWA token holders has surged from 28k to 40k, an increase of nearly 43%. Among them, nearly 20k users have held for over 12 months.

Source: rwa.xyz

Source: rwa.xyz

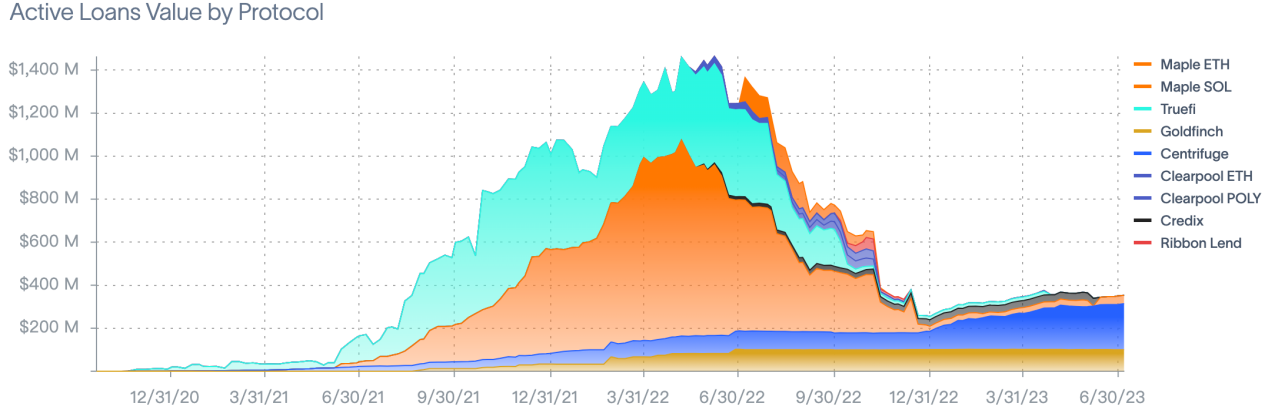

- Private credit RWA protocols currently have about 1553 loans, with a total active loan amount of $500M and a total locked amount of approximately $4B, showing significant growth potential compared to last year's peak loan total of $1500M.

Source: rwa.xyz

Source: rwa.xyz

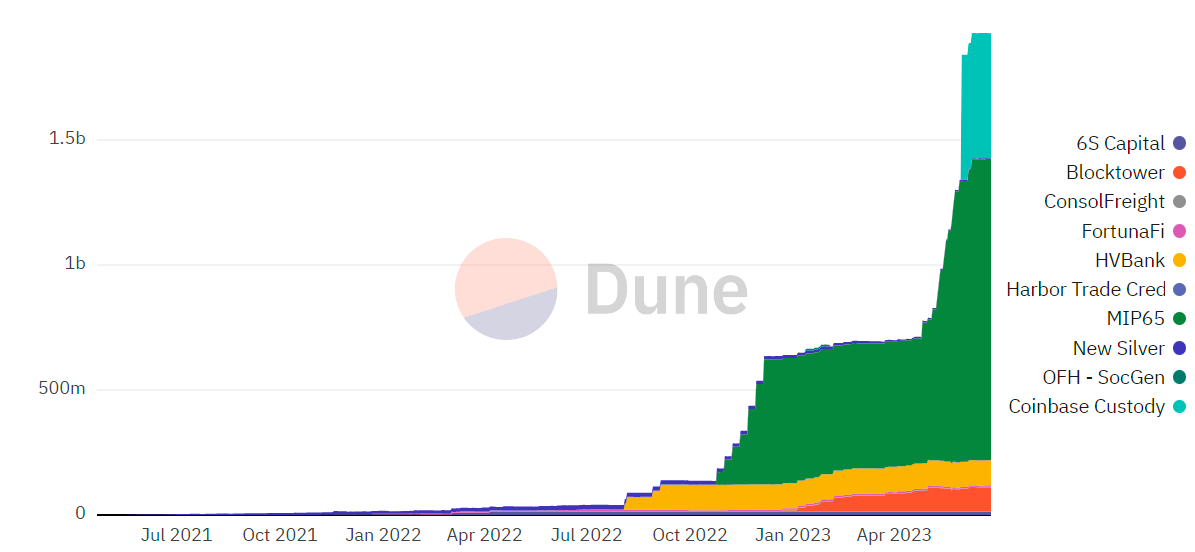

- Statistics released by MakerDAO in June show that RWAs continue to account for the vast majority of its stable fees. In May, RWAs accounted for 7% of all stable fees generated by the protocol, up 7% from April.

Source: MakerDAO

Source: MakerDAO

Sector Logic

TradFi-wise

Reduce transaction costs and intermediaries, improve transaction transparency and capital circulation efficiency.

- Non-liquid assets like real estate and art can be tokenized to disperse ownership and enable quick turnover, trading, collateralization, and financing in secondary markets.

- Heavy investments like infrastructure, railways, and electrical works can issue tokens to quickly recover costs, while SMEs can crowdfund globally through tokens.

On-chain alternative assets & synthetic structures enhance the composability of financial primitives, providing more hedging tools.

- Deriving various combination paradigms, extending the asset class spectrum vertically, diversifying and spreading investment portfolio risk exposure.

- Within a single mixed fund or structured product, on-chain assets can serve as hedges against traditional assets and currency fluctuations in different jurisdictions.

Activate the funds of restricted foreign potential speculators and institutions.

- The narrative of inclusive finance means a larger TAM, which translates to higher profit extraction potential.

- Funds that escape banks are effectively flowing back into TradFi in another form.

- This further activates global liquidity of funds, benefiting some local institutional investors, with the potential outcome being a rapid exacerbation of regional wealth and liquidity issues, leading to more severe social stratification.

DeFi-wise

Support and amplify DeFi speculative loops.

- DeFi has created a token speculation market, where the value capture of tokens mainly comes from the protocol's ability to generate revenue from speculative activities.

- RWA can shorten this token speculation loop, and the underlying assets possess liquidity, debt, collateral, etc., supporting swaps, effectively creating a foundational layer supported by traditional assets beneath DeFi.

Introduce massive liquidity and expand the DeFi user base.

- Simply put, the rules of the TradFi game are more easily recognized and accepted by the mainstream, which helps lower the learning and entry barriers for DeFi to some extent.

- The scale and density of institutional funds, the audience range and the size of their risk exposure, sales channel windows, market participant ratios, and the degree of specialization in TradFi far exceed those in DeFi.

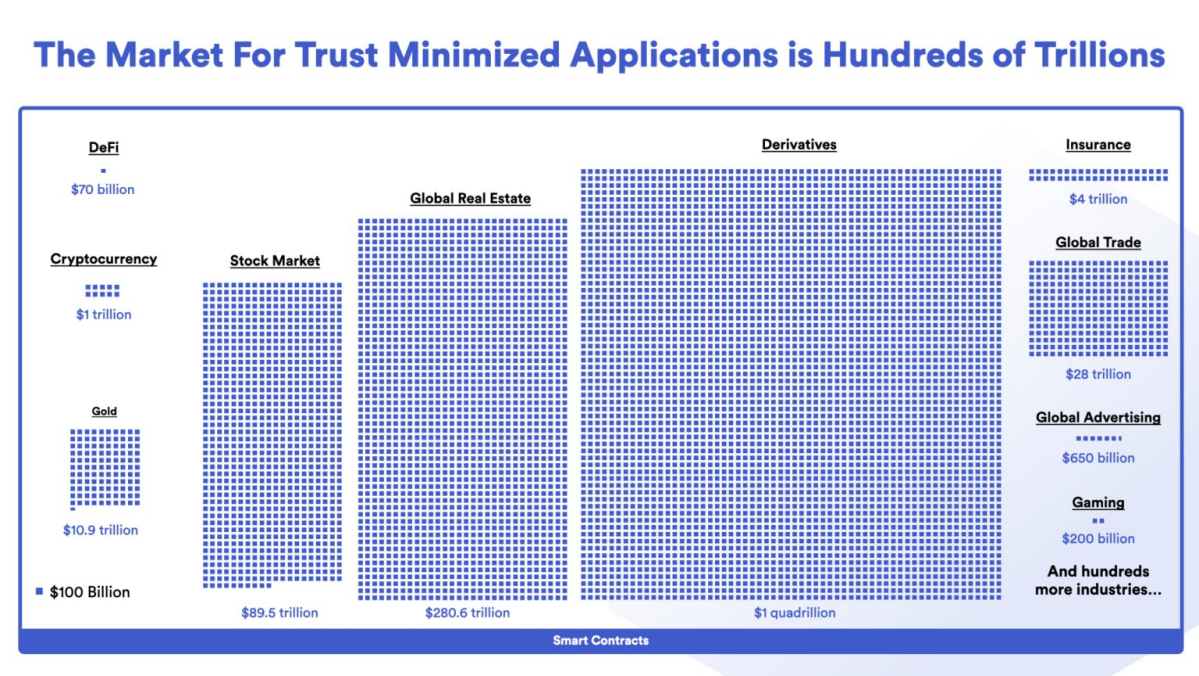

- BCG & ADDX research suggests that the tokenized market could reach a scale of $16 trillion in 2023 (including a $3 trillion real estate market, $4 trillion in listed/unlisted assets, $1 trillion in bonds and fund markets, $3 trillion in alternative asset markets, and $5 trillion in other tokenized markets).

- Citigroup estimates that, based on the most basic points, the combined scale of digital securities and blockchain trade finance could reach $5-6 trillion by 2030.

Source: Chainlink

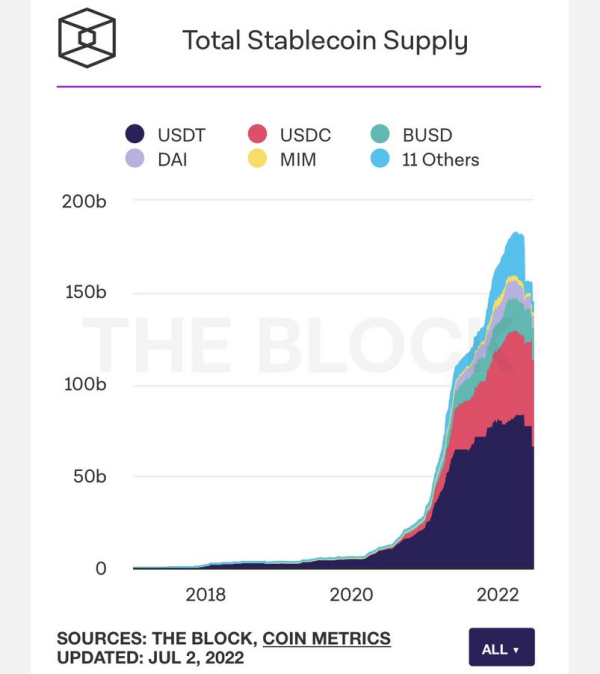

The stablecoin market has already been validated.

- USDC and USDT are essentially RWA backed by fiat currency.

- The stablecoin market reached a peak market capitalization of $180B in 2022.

Source: The Block

Momentum

Macroeconomic cycles prompt funds to flow back to U.S. dollar-denominated assets.

- Regulatory tightening and improved compliance laws.

- Traditional U.S. dollar-denominated funds are yielding more, with sustained interest rate hikes raising short-term Treasury yields to 4% (the latest 2-year yield is 64%, slightly narrowing but remaining high).

- Most idle funds have avoided risk since March due to the SVB incident, primarily accumulating in stable assets like U.S. Treasuries.

Source: Alliance Bernstein

Increasing interest from traditional institutions.

- The push for BTC ETF issuance also indicates that traditional market alpha opportunities are fading, with the mainstream relying on beta passive returns (not actively seeking to outperform the market, just aiming for average market returns).

- TradFi is facing bottlenecks in its own development, seeking industry transformation, as seen in past internet + finance, embracing AI, and fintech pearls like Aladdin.

- Old money believes that the crypto native lacks a complete understanding of TradFi and cannot penetrate the market deeply; the RWA sector is more suitable for traditional players to explore and lay out.

The crypto market needs to attract new users.

- A series of explosive events (LUNA, FTX) have severely eroded market confidence.

- On-chain liquidity has dried up, and NFTs have plummeted.

- The on-chain infrastructure of crypto is inverted between primary and secondary markets, and protocol Lego innovation is dull.

Resistance

Uncertain regulatory climate.

- Taxation, asset definitions, licensing, recovery processes, and other systemic elements depend on the local financial policy environment.

- The regulation of digital assets varies across different jurisdictions globally, and a unified classification standard does not yet exist.

- The attitudes of central banks, banks, and securities regulators essentially determine the lifespan of protocols, with a high probability of explosive failures.

Limited traction.

- Contrary to crypto-native beliefs, PMF cannot be found.

- Early crypto-native users are extremely resistant to centralized regulation and banking systems, seeking independent on-chain DeFi ecosystem development.

- Most DeFi participants dislike KYC/AML (even though zk-proof solutions can provide privacy protection) and prefer completely permissionless interactions.

- High-risk tolerant DeFi users do not value RWA yields; even when discussing equity RWA, the yield comparison may not be as attractive as creating a pool on Uniswap (especially now that v4 has introduced hooks, further liberating playability and freedom).

- The base of low-risk tolerant DeFi users is itself small, and they can easily choose to stake mainstream coins or buy ETFs for passive income.

- Traditional institutions are not in a hurry to enter the market and are still weighing their options.

- On-chain liquidity remains small compared to traditional finance, and the current market depth is insufficient to create significant wealth effects; it is likely that hot money from traditional financial players will flow back to on-chain rather than the other way around.

- Based on this logic, how much effort traditional institutions are willing to invest for a metaphysical alpha arbitrage space and what percentage of their balance sheets they are willing to allocate to explore the unknown remains to be seen. Currently, it seems unlikely that they will allocate more than 0.1%, which is negligible compared to other businesses.

- After communicating with traditional secondary fund managers, most indicated that they do not consider trading on-chain assets or synthetic assets in the short term: first, there are sufficient alternatives and hedging methods in the traditional stock market; second, due to the background attributes and risk preferences of LPs, it is impossible to allocate too much crypto assets without interfering with their existing investment systems.

Limited high-quality underlying assets.

- High-quality underlying asset categories like U.S. Treasuries are limited; niche assets like New Zealand stocks lack sufficient liquidity and do not have T+0 settlement methods, while other small-cap stocks and altcoins are not closely related to the macro economy, making it difficult to formulate speculative strategies, rendering tokenization unnecessary and unlikely.

- Tokenizing similar underlying assets means that the competitive barriers for protocols will not be very high, leading to a trend of homogenization.

- The sector is inevitably heading towards a Matthew effect similar to LSD in the later stages.

Evaluation Dimensions

Product Fundamentals

- The variety of RWA products offered and the range of yields have differentiation and competitiveness in the market, including the scope of services (what assets are currently being handled, where are these services provided? Are they qualified to provide this service long-term?).

- TAM stickiness, user retention, asset pool depth and liquidity, funding discount rates.

- Protocol revenue and net profit, token value and circulation efficiency.

Risk Control Capabilities

- Team: Does the team have experience in traditional investment banks, commercial banks, or securities firms? Do they maintain good relationships with local legal systems? Do they have any illegal records or bad reputations in the crypto industry?

- Compliance: Is the company subject to local securities laws and regulations (what is the local policy environment and tolerance for crypto? Are regulatory documents clearly defining asset attributes or prohibiting such assets?), KYC/AML, default settlement, compliance costs, credit assessment.

Protocol Mechanisms

- Tokens representing real assets need to interact with multiple blockchain ecosystems, requiring interoperability in the protocol's architecture across different chains.

- Is the on-chain method decentralized? What kind of trust-minimization mechanisms are followed? Are off-chain cash flows and related collateral debt information disclosed regularly? What oracle network data operation mechanisms are used, and how are nodes selected?

- The protocol's security mechanisms, whether they can effectively prevent information leakage of interacting account addresses, oracle manipulation, hacker attacks, etc.

Partners

- Have they established partnerships with mainstream DeFi crypto communities like MakerDAO and Aave, or have stable on-chain lending supporters?

- Have they chosen experienced and trusted third-party custodians for on-chain assets (e.g., off-chain collateral SPV controlling disposal rights)?

- Do they have long-term collaborations with top banks, trusts, and other TradFi intermediaries in terms of reputation, scale, and service scope?

Underlying Asset Classification

By Asset Form Classification

Standardized (S)

- Semi-fungible/fungible, easily tradable, with financial and monetary value.

- Public + on-market circulation.

- Generally regulated by the SEC.

Non-standardized (N)

- Non-liquid, non-homogeneous, difficult to price and trade assets.

- Typically circulate in private + over-the-counter markets.

- More likely to be regulated by the CFTC.

A brief overview of U.S. regulatory agencies and their subjects is as follows:

By Asset Category Classification

- The funding attributes determine the behavior of traders, and the trading behavior within major asset categories determines the available options.

- The potential users' tolerance for risk and uncertainty determines their allocation ratios across different major asset categories.

1. Fiat Currency RWA

Common: USD, EUR, JPY, GBP, CNY, etc.

Focus sequence: AUD, CAD, KRW, CHF, ZAR, MXN, etc.

Key tools: Collateralized stablecoins.

Projects: Circle, Tether, Frax, MakerDAO, etc.

- The initial RWA was stablecoin projects backed by fiat currency (mainly USD), such as Circle's USDC and Tether's USDT.

- Transaction costs, channels, and available categories are currently quite limited.

- If more fiat currencies can be issued as on-chain assets in the future, fiat stablecoins from countries with weak correlations like Russia and Malaysia, and negatively correlated currencies like Canada, Australia, and South Korea may become good hedging tools (not discussing depth issues for now).

2. Fixed Income RWA

2.1 Bonds

Common: Government bonds (sovereign rate bonds: U.S., Europe, Japan, Australia, China), central bank notes, government debt, corporate bonds, foreign debt, credit bonds, convertible bonds, etc.

Key tools: ETFs, bond derivatives.

Projects: Centrifuge, ONDO, Maple, OpenEden, BondbloX, FortunaFi, CredeFi, etc.

- Government bonds/Government bond ETFs currently account for the largest share of RWA, as they are considered low-risk and are typically viewed as safe-haven assets in the fixed income category.

- Despite unsatisfactory yields, leading DeFi communities are still willing to balance their risk exposure through RWA of government and corporate bonds; for example, 500 million DAI was invested by MakerDAO in the first phase of U.S. Treasury RWA purchases at the beginning of the year.

- There is still some exploration space for RWA in notes, corporate bonds, credit bonds, etc., and project teams can seek differentiated routes based on their resources and background advantages.

2.2 Credit

Common: Personal loans, corporate loans, structured financing tools, personal housing mortgages, auto loans, etc.

Projects: Centrifuge, Maple, Goldfinch, TrueFi, Defactor, Credix, Clearpool, Bru Finance, Resource Finance, etc.

- It can connect global credit, providing institutional investors and retail investors with more opportunities for stable returns.

- Corporate loans significantly alleviate the financing pressure on SMEs, making it easier to gain social and government support.

3. Equity RWA

Main markets: U.S., Europe, Japan, China, Hong Kong, Australia.

Focus sequence: Some emerging markets in BRICS.

Key tools: ETFs, index derivatives, leading stocks in key industries.

Common: Equity, primary shares (private placements), secondary shares (public markets), etc.

Projects: Backed Finance, Sologenic, Swam, AcquireFi, Horizon Protocol, Hamilton Lane, etc.

- Individual stocks do not require excessive attention to macro cycles, focusing more on the operational status of individual listed companies.

- There is genuine trading demand for this type of asset, but it is greatly limited by legal issues. Projects like BackedFi that enable 24-hour trading of U.S. stocks may become a paradise for arbitrageurs.

- The route of combining with crypto assets to create "synthetic assets" seems more attractive.

4. Alternative RWA

4.1 Real Estate

Common: Residential, commercial properties, etc.

Key tools: REITs.

Projects: RealT, Parcl, LABS Group, Propy, Atlant, ELYSIA, Tangible, Blocksquare, Milo, Figure, LandShare, Lingo, HOME Coin, Theopetra, EktaChain, Robinland, Homebase, etc.

- Real estate tokenization and NFTization provide a convenient borrowing form backed by physical properties, and on-chain property fragmentation facilitates retail investment and trading.

- The on-chain packaging of real estate into REITs is already quite mature, but overall cost control (personnel transportation, property management and maintenance, property distribution, housing types) still depends on the capabilities of the project team.

- The diversification of underlying assets & the degree of global operation have a trade-off with project costs & scalability.

4.2 Collectibles

Common: Art, jewelry, coins, etc.

Projects: 4K, Arkive, mattereum, Codex Protocol, etc.

- Individual assets are of high value but have low standardization.

- There is potential to enter niche and non-standard trading sectors, creating new trading roles, such as on-chain trading of luxury watches, cars, and bags.

- The idea of making dealers into traders has good imaginative space.

4.3 Commodities

Common: Precious metals (gold, silver, platinum, palladium), base metals (copper, aluminum, cobalt, lithium, zinc), energy (crude oil, BRENT, WTI).

Focus sequence: Iron ore, coal, dairy products, agricultural products, etc.

Projects: PAX Gold, Tether Gold, Cache Gold, Agrotoken, LandX, etc.

- The degree of non-standardization is high, and the processes of sourcing, securing, pricing, and verifying assets on-chain are usually complex; the lengthy process of asset sourcing and packaging may lead to significant cost consumption, making rapid growth and expansion difficult.

- The TAM is relatively limited, and niche assets need to consider depth dimensions, making them suitable only for professional commodity investors.

- Agricultural products tend to follow a pure commodity investment framework, and investors lacking traditional commodity investment experience may struggle to assess the production cycles, storage and transportation processes, regional market environments, and climate temperature changes affecting economic crops.

- Crude oil is generally viewed as an interest rate impact observation, highly correlated with interest rates; traditional investors can directly purchase mainstream interest rate products, seeing little on-chain demand.

- On-chain gold purchases can achieve instant settlement and redemption advantages. However, gold can be considered based on bond logic (interest rates + inflation expectations), and large positions of investors can still prioritize mainstream U.S. Treasuries and other RWAs.

POV

Long-term layout, small steps, wait for the wind.

- RWA is likely a "necessary evil" for DeFi to expand to the next hundred billion user scale, but in the short term, it is more about sellers calling orders and narrative FOMO, rather than genuine breakthrough innovation or strong growth momentum. For small and medium investors, asset allocation should still align with their own needs.

- It is recommended that institutions focus on long-term layouts of 1-2 leading projects with innovative designs, while closely monitoring the dynamics of compliance policies in the U.S., Hong Kong, and Singapore; only with the cooperation of TradFi financial institutions can the overall sector's policy risks be minimized.

A clear trend is that alternative assets & non-standard RWA protocols are emerging.

- Is it necessary to standardize underlying assets? Not necessarily; non-standard assets can be directly tokenized on-chain using non-standard protocols like erc721/1155, and structured products can even use the latest 6551 directly; there is no need to strictly use 20, which is unlikely to become mainstream in the long run.

- Centrifuge, FortunaFi, etc., have already provided collateralized lending by packaging future income notes as NFTs; emerging protocols creating RETIs and collectibles with RWA narratives, like 4K, have significant imaginative space, and after gaining community trust through early operations, they may lead the next wave of trends.

Government bonds/U.S. Treasury RWA will remain mainstream, while equity RWA is gaining attention.

- The on-chain mechanism for U.S. Treasury bonds is mature, and the asset structure is robust, having gained consensus recognition from the crypto community; however, most have already issued tokens on platforms, leading to competition in the existing market, which is large but lacks novelty.

- Products that enhance equity-like RWA provide opportunities for on-chain traders to speculate on traditional stocks, with real demand, but face numerous compliance hurdles due to the influx of overly dispersed and untraceable funds on-chain, which may disrupt the normal operation of internal financial systems in various countries.

- Currently, most equity RWA still only target high-net-worth and ultra-high-net-worth institutional users, failing to lower the speculative threshold for retail investors, leaving significant room for sector development.

Recognition from the crypto community is key, and collaboration with on-chain crypto-native communities is harder to achieve than off-chain cooperation.

- For fixed income RWA, it is not difficult to promote cooperation with off-chain partners due to the ability to bear lower borrowing costs; the challenge lies in connecting the loan side.

- DeFi DAOs hold a large amount of lendable assets, but DAO members have significant differences in their understanding of off-chain collateral; the project team needs to provide transparent solutions for specific auditing, underwriting, and off-chain asset tracing processes.

- The compliance processes for off-chain TradFi lending may cause friction with DAO governance mechanisms; overly complex off-chain assets are difficult for the crypto DAO community to understand, and if community members do not understand or do not want to understand, proposals may be long-term shelved or rejected, making cooperation impossible. Theoretically, it is challenging for projects with purely TradFi backgrounds to gain the community's trust.

Points worth discussing and further researching:

- On-chain Ponzi schemes based on RWA assets may be more suitable for exploration by crypto natives, such as RWA Fi, RWA options trading, etc.

- Middleware for verifying asset tokenization, SaaS companies, compliant issuers, and intermediaries facilitating lending and borrowing on-chain, like IX Swap, Stima, Castle, Curio, etc., are worth paying attention to, as monopolistic players may emerge in the future.

- How regulated RWA DeFi and unregulated native DeFi will be segmented and coexist, and what competitive landscape will emerge with CeFi remains uncertain.

Conclusion

The enthusiasm of European and American asset management institutions to enter emerging national bond markets through various means and private wealth management services has never faded. As crypto infrastructure gradually improves and massive asset managers like Blackrock view BTC as digital gold, it is clear that the traditionally fragmented financial market is actively seeking better funding utilization scenarios and liquidity efficiency improvement solutions. Regulatory tightening actually signifies the beginning of serious scrutiny and governance assessment of crypto. As the vision of the world economy shifting from Keynesianism to Austrian economics gradually becomes a reality, the reach of crypto into traditional stock, bond, and currency markets will accelerate.

In the chorus of "models will eventually rule the world," DeFi whispers of devouring all markets.

TradFi may embrace crypto faster than you expect :)