Outlook for the Cryptocurrency Market in the Second Half of the Year: Expecting Innovation, Not Narratives

Perhaps we can look forward to the performance of the cryptocurrency market in the second half of the year and even for the whole year, especially the performance of Bitcoin.

Perhaps we can look forward to the performance of the cryptocurrency market in the second half of the year and even for the whole year, especially the performance of Bitcoin.Author: Nakamoto Huixiang, Nebula Capital

01 Introduction

In May, I mentioned in the monthly report that from a medium to long-term technical perspective, Bitcoin is likely to recover from its downtrend around the arrival of the third quarter and has a high probability of rising to $33,000.

From May to mid-June, Bitcoin completed a pullback and consolidation, restarting its upward momentum on June 15, and within the following week, it completed the recovery and set a new high for the year at $31,432.

Entering July, Bitcoin peaked at $31,500, and since then, it has been hovering in the $29,500-$31,500 range for 20 days.

Currently, we are in a historical phase of anticipated economic recession and severe monetary tightening; however, the U.S. stock market and Bitcoin are irrationally surging, especially the U.S. stock market, which, in the recently concluded first half of the year, ignored deteriorating earnings expectations, with the S&P 500 index rising by 15% and the Nasdaq Composite index rising by 31%, seemingly stirring up confidence for continued momentum.

Although, starting from the third week of June, the three major stock indices and leading tech stocks experienced a relatively deep correction, they all rebounded after several economic data releases at the end of the month, and after entering July, they all reached new highs again.

After Bitcoin returned to $31,000 and set a new high for the year, the market has almost reached a consensus on two potential scenarios for future developments—either rising to $34,000-$40,000 and forming a double top structure, leading to a deep correction; or officially opening the curtain for a Bitcoin bull market, boldly breaking into historical highs.

In the first two quarters of 2023, we experienced an equal duration of bull and bear markets. At this time, we are still in a narrative vacuum, lacking absolute hotspots, with overall liquidity not decreasing but stopping its inflow into the market. Occasional market fluctuations are driven by events. After Bitcoin broke the $31,000 barrier, we all began to look forward to the directional choices the market must face in July, with the decisive factor still being accurately positioning the macro cycle.

Defense or offense must be based on fundamentals (probability of economic recession, scale of liquidity) and the expectations triggered by fundamentals (market confidence anchor point). We will make a comprehensive judgment on both after the conclusion of this article.

02 Global Real Liquidity

The urgent question regarding liquidity now is: how much has the liquidity in risk markets decreased due to the interest rate hikes and balance sheet reductions by global central banks, especially the Federal Reserve?

The Federal Reserve began raising interest rates in March 2022 and started reducing its balance sheet in June, marking the first time in history that the Fed has simultaneously raised interest rates and reduced its balance sheet. So far, it has cumulatively raised rates by 500 basis points, with the U.S. federal funds rate maintained in the range of 5.00%-5.25%, while the balance sheet has shrunk by over $570 billion since the start of the reduction.

Comparing the Fed's asset scale of up to $8 trillion, and the U.S. Treasury may issue over $1 trillion in government bonds in the second half of the year, this reduction is indeed a drop in the bucket, hardly significant.

The reduction in the balance sheet has been loud but with little impact; what about the liquidity scale recovered from interest rate hikes?

Both interest rate hikes and balance sheet reductions are means to regulate the money supply; however, it is important to distinguish that balance sheet reduction is the central bank's way of reducing the base money supplied to banks, while interest rate hikes suppress commercial banks' lending activities, reducing the issuance of derived money. The total money supply in society, apart from the base money provided by the central bank to commercial banks, comes more from the continuous deposit generation through a series of credit asset expansion activities by commercial banks on the liability side.

We can understand that as the total deposits of commercial banks continue to increase, the total money supply in society will also continue to grow.

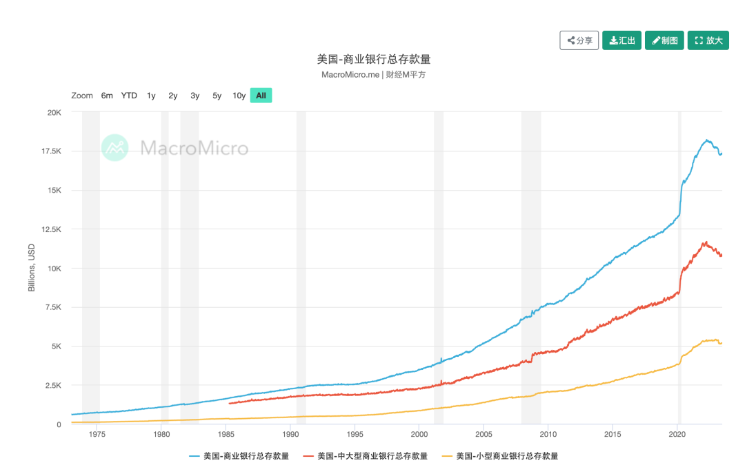

So, how much did the total deposits decrease after 15 months of interest rate hikes?

On March 16, 2022, the Federal Open Market Committee (FOMC) announced the first interest rate hike after its meeting, raising the federal funds rate range by 25 basis points to 0.25%-0.50%. At that time, the total deposits of U.S. commercial banks were $18.1 trillion, and on April 13, 2022, the total deposits peaked at $18.2 trillion.

As of June 28, 2023, the current total deposits of U.S. commercial banks are $17.3 trillion. In other words, after 15 months of frequent and significant interest rate hikes, the total money supply in the U.S. has only decreased by $800 billion, which, when reflected in a line chart, shows no significant fluctuations or declines.

The Eurozone began its first interest rate hike in July 2022, and according to CEIC data, the total deposits in the EU reached a minimum in September 2022, after which they began to rise rapidly, significantly surpassing the deposit levels before the interest rate hikes began. By April 2023, the total deposits of commercial banks in the Eurozone had gradually returned to their highest levels in the past decade.

The target of the benchmark interest rate increase is liquidity preference and the money multiplier, while the money multiplier reflects the desire of enterprises and residents to use money; in other words, it reflects confidence in economic growth.

The domestic money multiplier in the U.S. has hardly changed, partly due to the limited reduction in base money and total deposits of commercial banks, and partly because the reserve requirement ratio for deposits in the U.S. remains at zero, theoretically allowing U.S. commercial banks to maintain unlimited credit creation capacity.

Focusing on whether the Fed will raise interest rates has, in fact, temporarily lost its significance, as the fluctuations in risk markets have become almost desensitized to the Fed's interest rate decisions.

What we should really pay close attention to is the actual extent of credit contraction in the U.S., the changes in the broad money supply, which is the total deposits of commercial banks.

When liquidity is abundant and the greatest divergence and volatility factor lies in confidence, we will see a dual bull market for risk assets and safe-haven assets; whoever creates confidence will win liquidity. At the same time, we can conclude that people are losing confidence in the U.S. government, as the U.S. risk-free yield continues to soar, with both long-term and medium-short-term bond prices continuously declining.

03 When Will the Fed Stop Raising Interest Rates

So, when will the Fed stop raising interest rates?

Or let's rephrase the question: why hasn't the Fed started cutting rates yet?

Looking back at the market's bets on the Fed's interest rate hike process over the past few months, it has almost always shifted from extreme optimism (stopping rate hikes or even cutting rates) to a realization of reality (the rate hike cycle will continue).

Since the Fed began raising interest rates, market attention has been entirely focused on the regulation of money supply and the pace of rate hikes, while neglecting the issue that was widely mentioned at the beginning of the Fed's quantitative tightening policy—attracting global funds back to the U.S.

Reflecting on the Fed's aggressive interest rate hikes over 15 months, the anti-inflation effects were not apparent before June; although the CPI year-on-year growth rate of 4% announced in mid-June is still a relatively high absolute value, it has significantly cooled down. However, Powell made hawkish remarks at the central bank forum held by the European Central Bank on June 28, stating that "the possibility of consecutive rate hikes in July and September cannot be ruled out."

We can see that regardless of whether inflation is sticky, the Fed will persist in its rate hike policy; fighting inflation may just be a nominal goal, while the Fed's real concern is "attracting capital."

Since the Fed began raising rates in 2022, the total market capitalization of U.S. stocks has evaporated by about $10 trillion, returning to the levels at the beginning of the pandemic sell-off, which also marks the level before the panic sell-off was repaired and the significant rally was officially initiated.

As of now, the total market capitalization of U.S. stocks has increased by about $8 trillion from the lowest point in 2022, gradually approaching the scale before the rate hike began.

Undeniably, the U.S. economy is indeed expanding at a moderate pace. The economic growth rate, inflation rate, and unemployment rate that the Fed loves to monitor will not worsen due to rate hikes; instead, they may become uncontrollable due to capital outflows resulting from "stopping rate hikes."

Historically, the Fed has decided to stop raising interest rates mainly in two scenarios: one is when sustained high interest rates alleviate inflationary pressures, economic fundamentals weaken, unemployment rises, and the economy significantly declines; the other is when a sudden risk event leads to an emergency end of the rate hike cycle.

In this round of rate hike cycle, the rate hike cycle will only truly end when domestic capital in the U.S. is insufficient to support its economic expansion (global liquidity is exhausted, or certain factors lead to capital outflows from the U.S.), resulting in a substantial recession.

04 The Final Judgment Day

When will the final judgment day occur?

The current situation bears many similarities to the interest rate and debt cycle of 2006.

In 2006, the Fed gradually raised interest rates, increasing the rate from 1% in 2004 to just above 5%. However, at that time, the rate hikes were insufficient to slow down the asset appreciation supported by debt financing. Over three years, the S&P 500 index returned 35% (this year's Nasdaq return is 31%, and S&P 500 is 15%); meanwhile, foreign capital flooded in, and total loans increased. In 2007, the stock market and economy still performed well, with the stock market reaching new highs and a strong job market boosting consumer confidence.

For a long time before the financial crisis erupted, debt issues and tightening conditions did not affect the real economy.

It wasn't until August 2007 that the crisis erupted in the interbank market, with BNP Paribas suffering significant losses, interbank lending in Europe becoming tense, and the largest mortgage issuer in the U.S. facing bankruptcy. Within days, the stock market plummeted, and central banks in Europe and the U.S. urgently provided liquidity to banks, ending the stock market crash and beginning a recovery.

The most critical similarity with the banking crisis that erupted in March this year is that most decision-makers and investors believed that the debt risk issues exacerbated by tightening policies could be controlled, and the Fed and the government’s rescue of the banking system even resulted in GDP not declining but increasing.

Investors continued to increase their risk exposure, with debt bubbles concentrated in one or a few market sectors, leading to high volatility and significant rebounds in the U.S. stock market, approaching historical highs.

The complete detonation of the last debt crisis occurred at the end of 2007, about a year and a half after the interest rate reached the terminal rate of 5.25%, with the largest decline occurring on the day the Fed announced a rate cut.

In early 2008, U.S. economic data deteriorated across the board, and several major banking groups announced losses. People finally began to believe that the U.S. was entering a deep and prolonged economic recession. The Fed's emergency rate cut to 3.5% failed to save the collapsing credit and economic situation.

After large-scale easing policies boosted the economy, small rebounds occurred in April and July, but the self-reinforcing nature of economic depression continued and spread globally. Note that Lehman Brothers announced bankruptcy in September 2008, by which time the stock market had already fallen 20% from its peak, and individual stocks like Lehman Brothers had dropped by as much as 80%. By November, the U.S. stock market fell over 20% in that month alone.

The avalanche continued until March 2009, when the U.S. stock market hit bottom, and investors were extremely bearish. Suddenly, it surged 6.4%, and a week later, the Fed announced a $1 trillion stimulus plan.

Thus, whether we are trying to find a needle in a haystack or following a map, we seem to be able to judge the current situation and the next steps.

History does not repeat itself, but it does rhyme.

The banking crisis in March made people begin to prepare for a recession, but recently, this has gradually been drowned out by optimistic economic data and high investment sentiment. Liquidity remains abundant, optimism has not yet peaked, debt accumulation continues, and financial deleveraging has not yet reached its climax—the final judgment day will come much later than we expect, at least around 18 months after the interest rate reaches the terminal rate, when the economy truly experiences a significant downturn, and the Fed urgently loosens monetary policy.

05 How to Distinguish Bull from Bear

Perhaps we can look forward to the performance of the cryptocurrency market in the second half of the year and even the entire year, especially Bitcoin.

First, the current total liquidity in the cryptocurrency market is far higher than the liquidity level during the same price period of Bitcoin in 2020; second, the cryptocurrency market always benefits from the liquidity transfer and overflow from the U.S. stock market; furthermore, Bitcoin can be considered a high-quality asset in various attributes, especially favored amidst the regulatory pressures.

I want to reiterate that when liquidity is abundant, the most important factor determining asset prices is confidence.

Of course, returning to the beginning of the article, the two scenarios that the market has written for Bitcoin—either a pullback after reaching $34,000-$40,000 or a new historical high.

The panic sell-off of Bitcoin that began in June 2022 lasted for six months, followed by three months of massive long green candles and three months of low-volume pullbacks. The signals we need to pay attention to are not only that Bitcoin took six months to climb from $15,500 to $31,500, but also that the oscillation of Bitcoin in the high range is accompanied by decreasing trading volume and continuously rising support, with relatively low selling pressure in the market, and indeed, there are many long-term holders willing to buy in the $25,000-$29,000 range, indicating that accumulation is still developing.

Combining the overall liquidity situation and the search for macro cycles, Bitcoin may not necessarily break through its historical highs, but it will certainly approach them; $40,000 may be a rather conservative estimate.

Note that I do not believe the bull market will last forever; I believe the bull market has not yet begun and I am betting on its arrival.

06 Expect Innovation, Not Narratives

Since there is ample liquidity in the market and additional liquidity can be introduced from outside, how can we restore market confidence?

I realize that imagination fills the cryptocurrency market, and everyone is tirelessly digging for narratives for the industry, even fabricating them.

However, many times, these stories become limitations, constraining imagination, causing many industry builders and participants to be confined to a box, unable to think about how the industry should present itself beyond the narratives described.

What I mean is that whether for institutional investors or retail investors, FOMO means repeatedly telling the same stories and clinging to outdated narratives. Everyone should be adept at discovering, embracing, and supporting truly new things, as well as those inventions and innovations that are making breakthroughs and progress, even if they are not yet fully formed or sufficient to constitute a narrative.

The most critical factor driving the arrival of a bull market is always new inventions, new developments, and exciting new products.

A bull market relies on solid reasons for pushing asset prices up, and this reason must be compelling enough for people to believe that the world will be changed, and the companies creating it will have a bright future.

Focus on innovations and progress within the industry, and do not pay attention to things that are merely repackaged or transformed; the belief in "emerging things" and "this time is different" is the eternal characteristic of a bull market.

As for whether there are new products in the industry that align with the bull market's ignition or which emerging new things have made significant progress, please like, follow, and subscribe for the next thematic breakdown.