DeFi New Strategy: Empowering Liquid Staking Derivatives

Since the Ethereum Shanghai upgrade, the market has shown a clear preference for liquid staking. In terms of the amount of ETH staked, Lido holds an absolute dominant position. The flow of funds in DeFi also indicates that stETH has become the preferred choice for asset staking.

Since the Ethereum Shanghai upgrade, the market has shown a clear preference for liquid staking. In terms of the amount of ETH staked, Lido holds an absolute dominant position. The flow of funds in DeFi also indicates that stETH has become the preferred choice for asset staking.Original Title: The Surge in Liquid Staking

Author: Alice Kohn, Glassnode

Compiled by: Annie, Daring Think Tank

Abstract

- In mid-April, Ethereum launched the staking withdrawals feature, further increasing market interest in liquid staking.

- Among numerous Ethereum liquid staking service providers, Lido has established an overwhelming advantage, possessing the highest supply and liquidity of LSDs (liquid staking derivatives) and enhancing its network effects through integration in DeFi, solidifying its leading position in the Ethereum staking market.

- With the application of LSDs in DeFi, a new trend has emerged—LSDs are being transferred into lending protocols for staking, while the TVL (Total Value Locked) of liquidity pools related to staking has decreased.

Ethereum Price Performance Relatively Stable

In recent weeks, the digital asset market has been influenced by BTC ETF applications, with BTC significantly outperforming other assets. Although BlackRock's BTC ETF application boosted ETH prices by 11.2%, by the end of the second quarter, it was only 6.4% higher than the opening price in April, showing unexpectedly stable prices.

Figure 1: Ethereum Price Performance Against USD

In comparison, many digital assets in 2023 have underperformed BTC, with the ETH/BTC ratio dropping to 0.060, nearly a 50-week low. However, this ratio has rebounded to 0.063, indicating a market recovery in early July.

Figure 2: Ethereum: Monthly Performance of ETH/BTC Ratio

Since the beginning of the year, the rise in ETH prices has not triggered fluctuations in on-chain activity. Gas fees, which represent demand for block space, have remained relatively low, especially in the week following the ETF application announcement. During the Shanghai upgrade in April, which preceded a similar rebound in the ETH market, gas fees increased by 78%, while this week's increase was 28%.

Figure 3: Ethereum Price vs Gas Fees

A New Wave of Staking

Although the Shanghai upgrade hard fork allowed validators to withdraw staked ETH, the upgrade did not trigger a wave of ETH withdrawals; instead, it sparked a new wave of staking.

Staking activity (number of transactions) peaked on June 2—over 13,595 new stakes (worth over 400,000 ETH). We can compare this with the ETH trading volume on exchanges, which remained around 30,000 during this period.

Figure 4: Exchange ETH Trading Volume vs Staking Activity Count

If we compare the staking volume of ETH on exchanges (blue) with the inflow of ETH (red), we can clearly see that the amount of newly staked ETH is rapidly increasing. Since the Shanghai upgrade, ETH staking activity has maintained high growth, matching the inflow on exchanges.

Figure 5: Exchange Inflow vs ETH Staking Activity Increment

We can further analyze the daily staking deposit volume by different service providers, revealing that the market is favorable to liquid staking service providers, especially Lido.

Figure 6: Daily Staking Deposit Volume by Service Provider

Lido's Advantage

The observations above reflect the market's demand for LSDs (liquid staking derivatives), which are essentially staking certificates for ETH deposited in staking pools.

Lido released its V.2 version update on May 15, allowing node operators to withdraw staked ETH, enabling Lido's stETH holders to convert it back to ETH. After the release, 400,000 stETH (approximately $721 million) were withdrawn, leading to a contraction in stETH supply. However, the massive increase in ETH staking deposits far outweighed the decline in stETH, bringing stETH to a new high of 7.49 million.

Compared to other liquid staking service providers, Lido's stETH supply is 16 times higher than that of the second place, firmly holding the leading position in the liquid staking market. However, since the beginning of this year, Rocketpool's liquid staking derivative (rETH) supply has been growing three times faster than Lido's supply.

Figure 7: Circulating Supply of LSDs

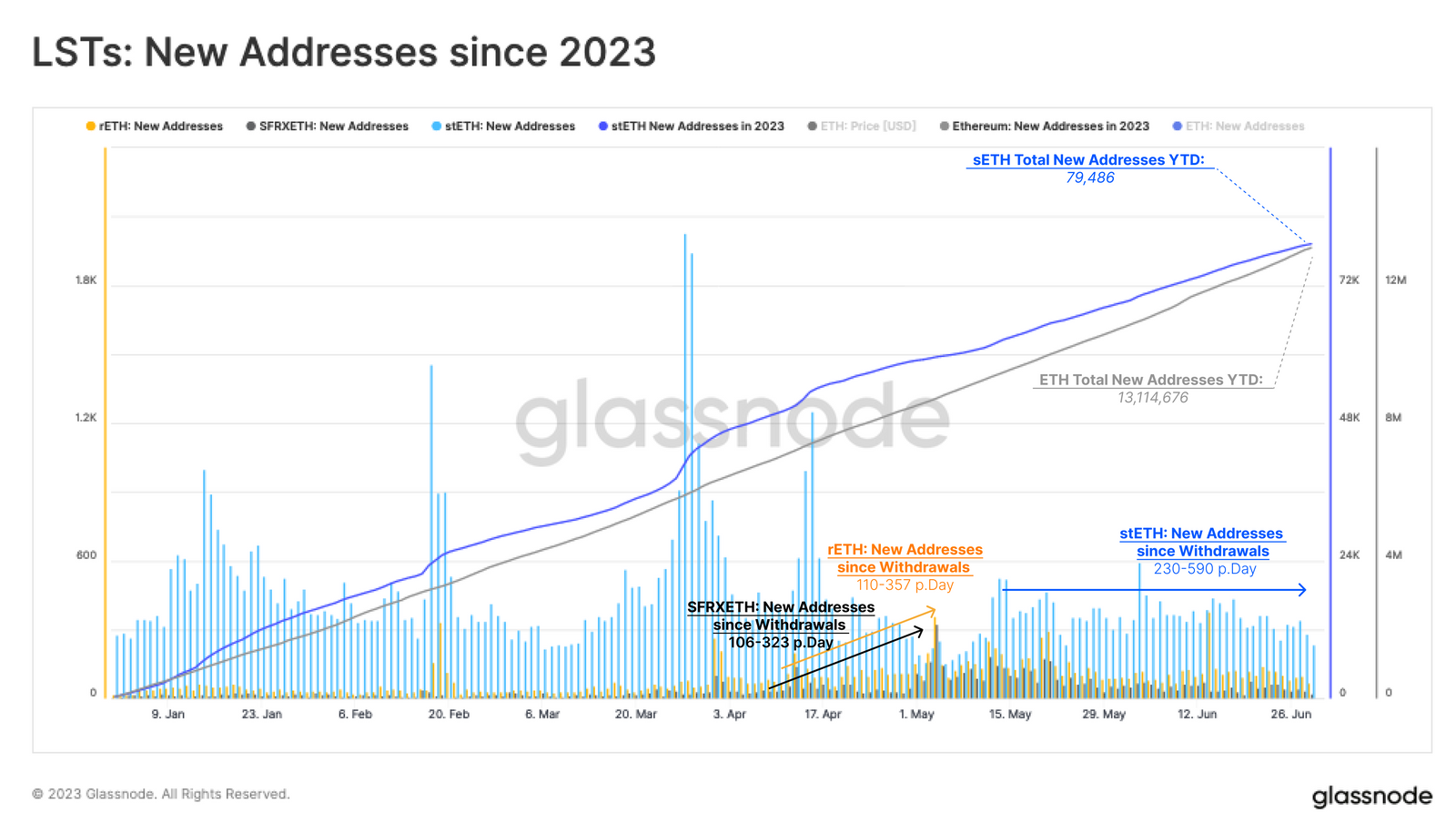

Interestingly, the increase in demand for Lido's stETH has not been reflected in the growth of new holders of stETH. We observed that the number of liquid staking users for Rocketpool and FRAX has increased since the Shanghai upgrade, but there has been no significant growth in new users for Lido.

The daily increase in addresses holding stETH has fluctuated between 230 and 590, showing no significant changes since the beginning of the year. Thus, we can conclude that the new staking deposits for Lido are actually driven by existing stETH holders increasing their staking deposits.

Figure 8: Average Balance of stETH Holders Since 2023

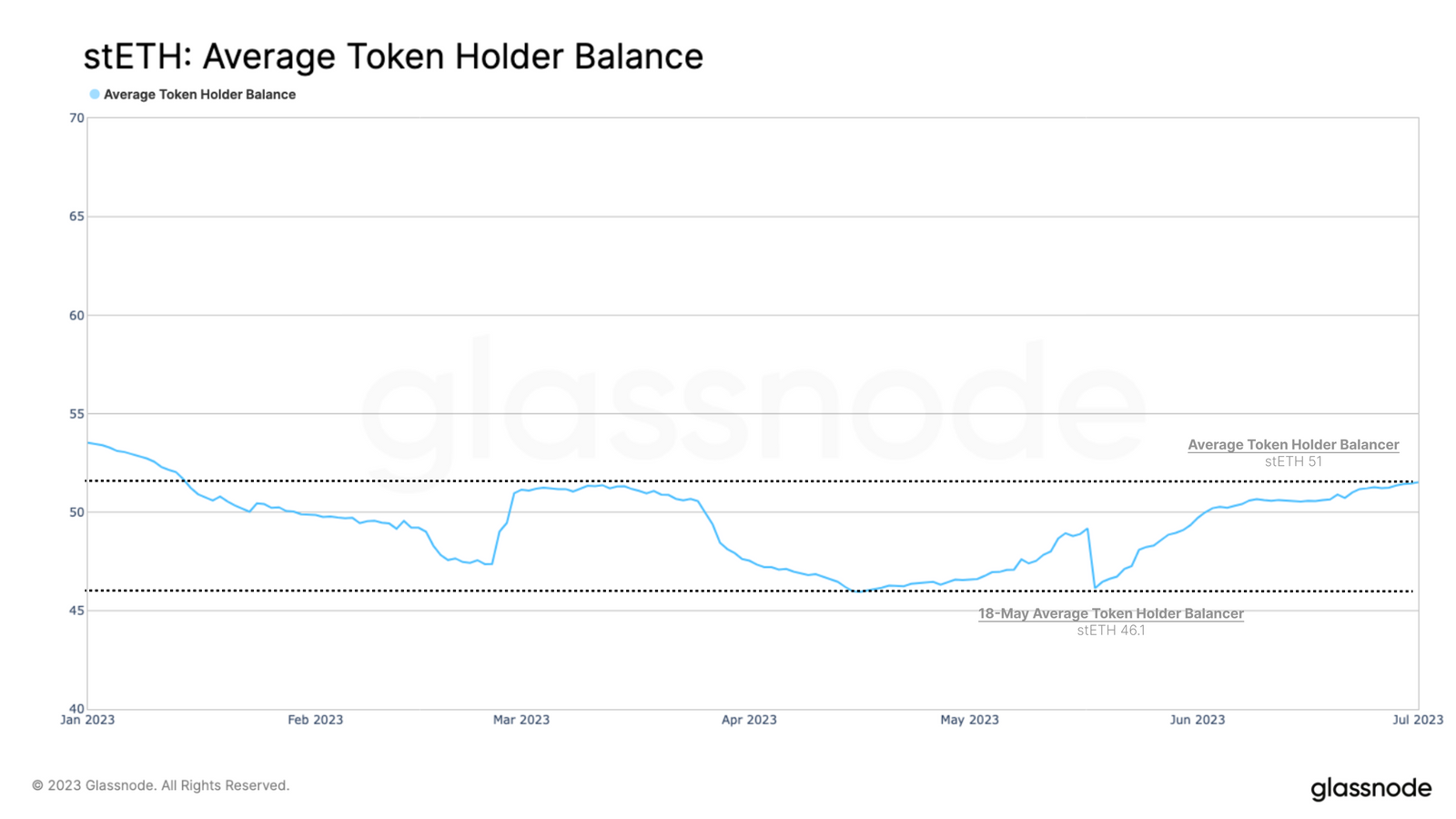

By analyzing the average balance of stETH holders, we can estimate the distribution of newly issued stETH. After Lido enabled the withdrawal feature, the average balance of stETH holders dropped to 46.1 stETH ($83,000).

Since the Shanghai upgrade, the average balance of stETH has increased to 51.0 stETH ($100,000), indicating that existing holders are indeed increasing their share of ETH staked in stETH; this also suggests that there has been no significant growth in new users for Lido's liquid staking.

Figure 9: Average Balance of stETH Holders

Figure 9: Average Balance of stETH Holders

New Uses of LSD in DeFi

One of the key values of LSDs is their integration with DeFi protocols. LSD holders can easily trade LSDs on decentralized exchanges or use them as collateral to earn through lending protocols.

Since their emergence, LSDs have seen increasing activity across various DeFi protocols, with Lido's stETH being the most active. The widespread use of stETH in DeFi is another factor contributing to Lido's dominance in the liquid staking space. However, several interesting trends are occurring among the DeFi protocols accepting LSDs.

Since the Shanghai upgrade, the stETH-ETH Curve pool, which is Lido's largest liquidity pool for liquid staking services, has lost 39% of its total locked value (TVL). It is now approaching levels seen during the deleveraging period following the Terra-Luna collapse in May 2022.

Figure 10: Total Locked Value of Curve Pool

Analyzing the Balancer's wstETH-ETH Pool, we can see this trend more clearly. Since April 15, the TVL of this pool has decreased by 71%, from $351.2 million to $101.4 million.

Figure 11: Total Locked Value of Balancer's wstETH-ETH Pool

By studying the annual percentage rates (APR) of the two liquidity pools, we can see a consistent downward trend in 2023. We use April 15 as a reference point, as it was when the new wave of staking began, and liquidity on related DEXs started to decline.

The APR of the Curve stETH-ETH Pool has dropped from 3.47% on April 15 to the current 2.27%. On the other hand, the Balancer Pool reached a low of 1.69% in April, then slightly rose to 2.10%.

Note: The APR of liquidity pools consists of different reward structures paid in various types of tokens. Lido rewards Curve liquidity providers with LDO, and this reward program will end on June 1. Given the starkly different APR trends on these two platforms, this changing reward structure itself is unlikely to cause the decline in liquidity.

It is possible that since the withdrawal feature was opened, the APR has become somewhat irrelevant for LSD pools. Before the Shanghai upgrade, liquidity pools were the only source of liquidity for stakers; however, now the trading requirements between stETH and ETH on DEXs have been reduced, allowing users to mint or redeem directly on the platform.

This may indicate that market makers are seeing reduced rewards as DeFi liquidity providers. Additionally, due to increased scrutiny from U.S. regulators, the retreat of some leading market makers may further exacerbate this trend.

Figure 12: Annual Percentage Rates of stETH and wstETH Liquidity Pools

Since we see that the reduction in liquidity is a continuous trend rather than a sudden withdrawal caused by a few players leaving, we tentatively conclude that these reductions in liquidity are more likely due to structural changes.

Another explanation could be that new sources of income from other DeFi protocols have increased the potential opportunity cost for liquidity providers. Lending pools like Aave or Compound allow LSDs to be used as collateral and leverage them against ETH.

Aave's total locked value has seen significant growth, particularly in the V3 lending pool for wstETH. Since its launch in late January 2023, the wstETH Pool's value has ballooned to over $734.9 million, while the stETH Pool hovers around $1.79 billion.

Figure 13: Total Locked Value of stETH and wstETH in Aave

Figure 13: Total Locked Value of stETH and wstETH in Aave

The Compound V3 wstETH Pool has also seen significant growth since its launch earlier this year, now holding over $42.2 million in stETH. It has increased by 817% since May 9. Compared to ETH and even stablecoins, yield-bearing liquid staking derivatives (LSDs) seem to be becoming a more attractive collateral option.

Figure 14: Total Locked Value of Compound V3 wstETH Pool

Figure 14: Total Locked Value of Compound V3 wstETH Pool

Conclusion

The Ethereum Shanghai upgrade was completed in mid-April, allowing participants to withdraw staked ETH. Rather than triggering a wave of withdrawals, it further accelerated staking deposit activities, with the market showing a clear preference for liquid staking derivatives (LSDs).

Among them, Lido holds the largest market share to date, accounting for 7.5 million ETH staked. Lido's stETH also plays an important role in DeFi—being the preferred collateral. Since the Shanghai upgrade, there has been a noticeable change in the distribution of stETH in DeFi, with a contraction in DEX liquidity pools and an increase in collateral usage in lending protocols.

This indicates that investors may be employing a strategy to maximize staking yields by establishing stETH exposure through lending leverage to amplify their returns.

Risk warning Risk warning

Risk warning Risk warning