OPNX bond trading has become a gimmick, questioned for "fake trading." Can Su Zhu's wish to establish an exchange to repay debts be realized?

After doing the math, based on OPNX's current daily trading volume of 50 million USD, it would take approximately 213 years for Su Zhu and others to repay the 3.5 billion USD debt of Three Arrows Capital.

After doing the math, based on OPNX's current daily trading volume of 50 million USD, it would take approximately 213 years for Su Zhu and others to repay the 3.5 billion USD debt of Three Arrows Capital.Author: Grapefruit, ChainCatcher

Recently, the crypto credit trading platform OPNX (Open Exchange), founded by Three Arrows Capital's Su Zhu and others, has seen a surge in trading volume and a skyrocketing price of its platform token OX, successfully attracting the attention of the crypto community.

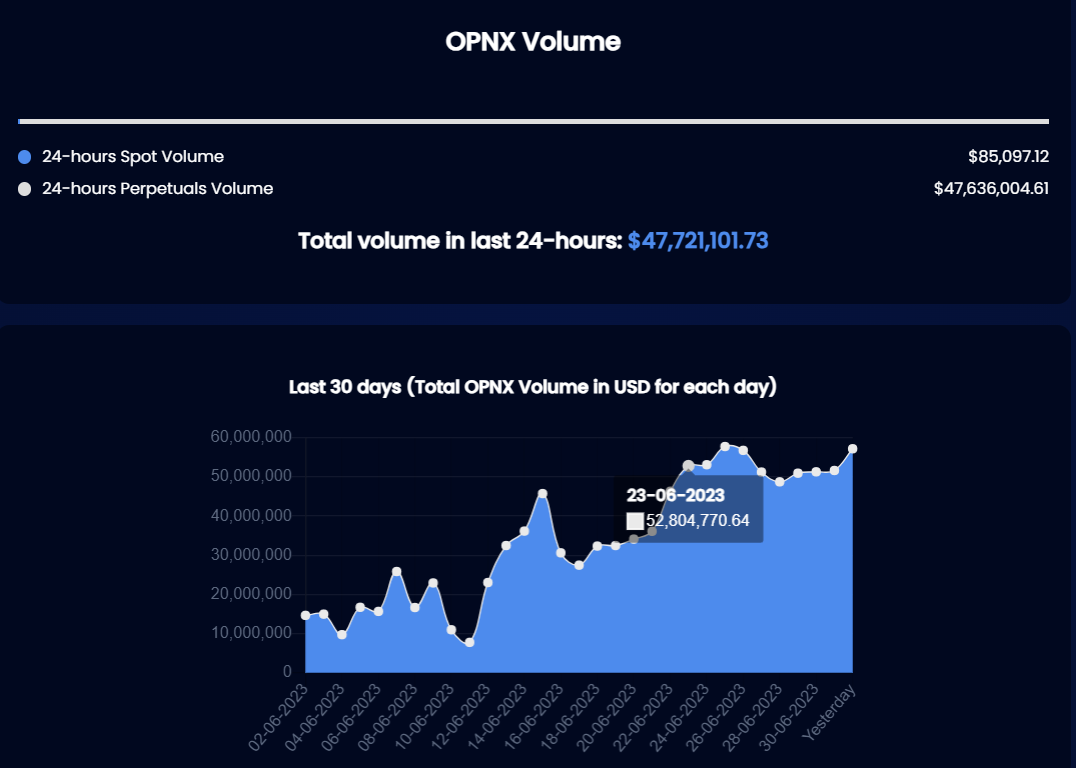

On June 26, OPNX tweeted that its daily trading volume had surpassed $50 million, with an average daily trading volume of $41 million. Since its launch on June 1, the platform token OX has risen from $0.011 to a peak of $0.044, marking a maximum increase of 300%. The price has now retreated to $0.036, with a total market capitalization of approximately $119 million, ranking 233rd among crypto assets.

From the trading data on the OPNX platform, this new crypto trading platform, which has been online for only three months, has trading volumes comparable to established platforms like Crypto.com (with a 24-hour trading volume of $79.63 million) and Bitfinex (with a 24-hour trading volume of $68 million).

It seems that all these indicators suggest OPNX is developing in the direction set by its founders, but due to the unique nature of the founding team, users remain skeptical about the platform.

On June 22, a community user raised concerns about the inconsistency in the trading volume and price fluctuations of BTC pairs on OPNX, suggesting the possibility of "wash trading," which sparked widespread discussion in the crypto community. Additionally, the platform, initially positioned as a crypto credit trading platform, has seen its credit tokens become more of a gimmick, with the real business being contract trading.

The phrase "dishonest founders + failed platform" continues to linger around OPNX, difficult to shake off.

OPNX $10 million trading volume questioned for "wash trading," yet less than two dollars on the first day of launch

Since entering June, OPNX has been releasing a continuous stream of positive news. On June 26, OPNX tweeted that its daily trading volume had surpassed $50 million, with an average daily trading volume of $41 million; on June 25, it announced the launch of its first Launchpad project, the unsecured credit market Raiser (RZR), where all OX stakers will share 10% of the RZR supply allocation; on June 24, OPNX announced the launch of the credit currency oUSD, which can be exchanged 1:1 with USDT; and on June 1, it announced the launch of the new governance token OX and the governance platform The Herd, allowing users to trade for free through staking and supporting the conversion of OX using FLEX, among other features.

OPNX (Open Exchange) is a crypto credit trading platform co-founded by Three Arrows Capital's Su Zhu and Kyle Davies, along with the bankrupt exchange CoinFLEX. It tokenizes the credit assets of bankrupt crypto projects for users to trade or use as collateral to release the liquidity of trapped crypto assets. The platform made its debut in February this year and announced in early March that it had acquired all assets of the exchange CoinFLEX, including personnel, technology, and tokens, continuing to use FLEX as the platform token, which was restructured and renamed Open Exchange.

Since the launch of the OPNX platform, its trading volume has garnered significant attention from users. According to FLEX Statistics, since June 23, the 24-hour trading volume on the OPNX platform has exceeded $50 million, peaking at $57 million, with the current 24-hour trading volume at $47.72 million.

However, the authenticity of the trading data on the OPNX platform has been called into question. On June 22, crypto trader @Loris tweeted that by analyzing the daily trading volume data of OPNX's BTC perpetual contracts and comparing it with leading trading platforms, it was found that OPNX might be engaging in "wash trading."

Loris pointed out that the normal volume-price data displayed by leading trading platforms shows consistent fluctuations in volume and price (e.g., higher trading volumes should accompany significant price fluctuations) and features a stable baseline. In contrast, OPNX's volume-price data shows that the price fluctuations corresponding to its increased trading volume are minimal, while price fluctuations are significant during periods of decreased trading volume.

Additionally, OPNX's daily trading volume exhibits an independent and distinct pattern relative to price fluctuations, leading to the conclusion that OPNX may be engaging in "wash trading."

Subsequently, another crypto user commented that the wash trading volume on OPNX is quite evident.

From the BTC contract price chart data on OPNX's official website, it aligns with Loris's claims. Since entering June, trading volumes have periodically (generally at 8:00, 12:00, 4:00 daily) surged dramatically, with the peaks in the trading volume bars mostly within similar ranges, showing huge trading volumes during low price fluctuation periods and extremely low trading volumes during periods of significant price fluctuations. In contrast, the BTC price chart data and trends on the OKX platform during the same period conform more closely to volume-price rules.

BTC/USDT contract chart on OPNX

BTC/USDT contract chart on OKX

OPNX responded that these trading volumes are attributed to its market maker program. However, OPNX's market maker incentive program was announced as early as April 8. Currently, @Loris's tweet has also been deleted.

The reason why trading volume has garnered so much attention is that OPNX was reported to have a trading volume of less than $2 on the day it launched on April 4. According to CoinDesk, within 24 hours of OPNX's launch, only two trades were executed, totaling $1.26. Later, OPNX clarified that CoinDesk's $1.26 trading data only came from contracts and did not include spot trading; in fact, the total trading volume that day was $13.64.

In just three months, OPNX's daily trading volume has surged from around $10 to $50 million. The official explanation for this change in data can be attributed to multiple factors, such as the market maker program, the platform token OX, and the new Launchpad projects, but this does not alleviate users' concerns.

OPNX Credit trading has become a gimmick, contracts are now the mainstay

Aside from the authenticity of the trading volume data, the credit trading that OPNX initially promoted has also become a gimmick, with the trading volume of claims-related assets (also known as credit tokens) being nearly zero for many days.

Currently, over 99% of the trading volume on the OPNX platform is actually contributed by perpetual contracts. For instance, on July 3, OPNX's 24-hour trading volume was $68.12 million, of which contract trading volume was $67.99 million, while spot trading volume was only $137,000, and the trading volume of credit tokens is negligible as it is included in the spot trading volume.

This seems to contradict its initial positioning. At the platform's inception, OPNX was characterized as a credit trading platform and planned to support claims trading for several bankrupt companies, including Celsius, FTX, Genesis, BlockFi, Voyager, and Three Arrows Capital.

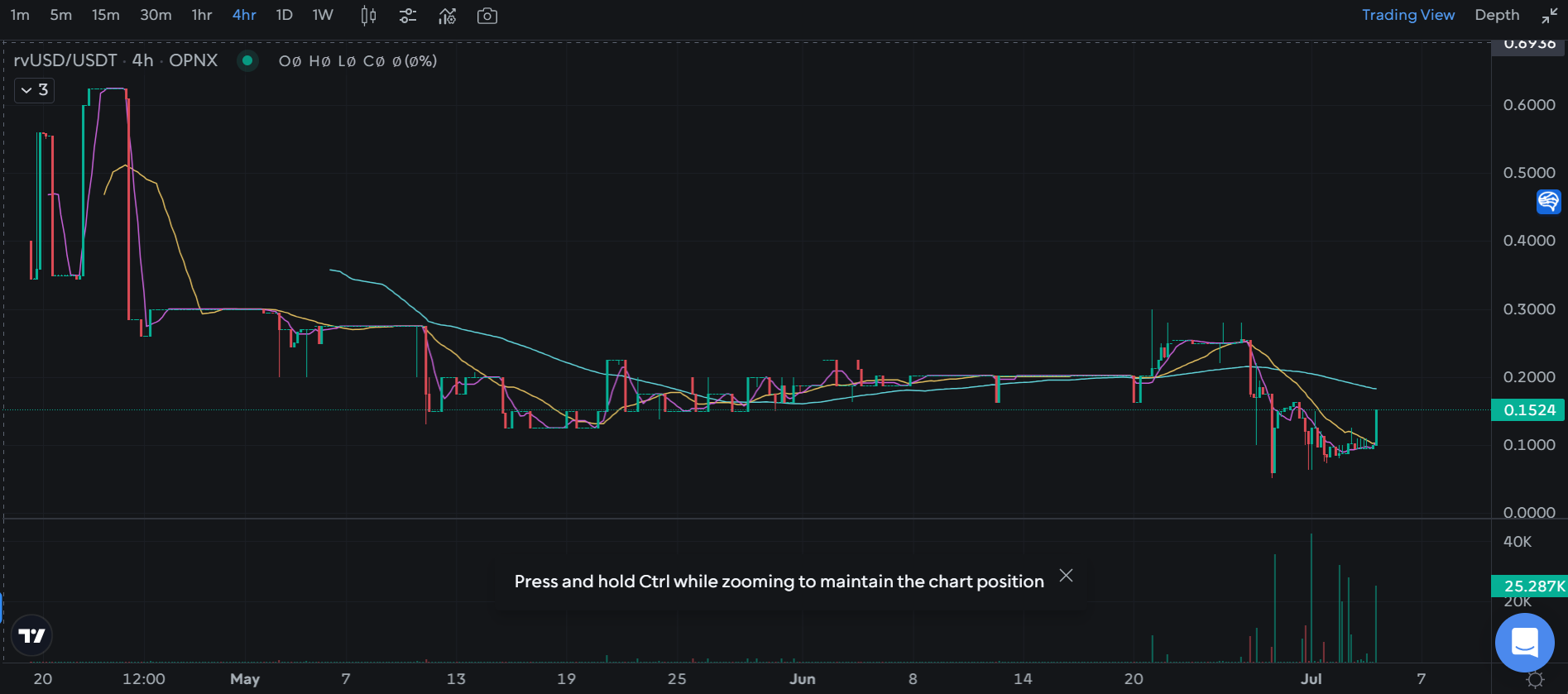

The first credit token launched was rvUSD (Recovery Value USD Tokens), issued by CoinFLEX, representing Roger Ver's $84 million personal debt owed to CoinFLEX. After CoinFLEX was acquired by OPNX, CoinFLEX users' KYC information and account balances could be seamlessly migrated to OPNX as its first customers, and the credit token rvUSD was subsequently launched on OPNX.

However, since rvUSD's launch on OPNX in April, its price has continuously declined from a peak of $0.62 to the current $0.15, with trading volume being zero for many days, indicating almost no liquidity.

rvUSD price chart

rvUSD price chart

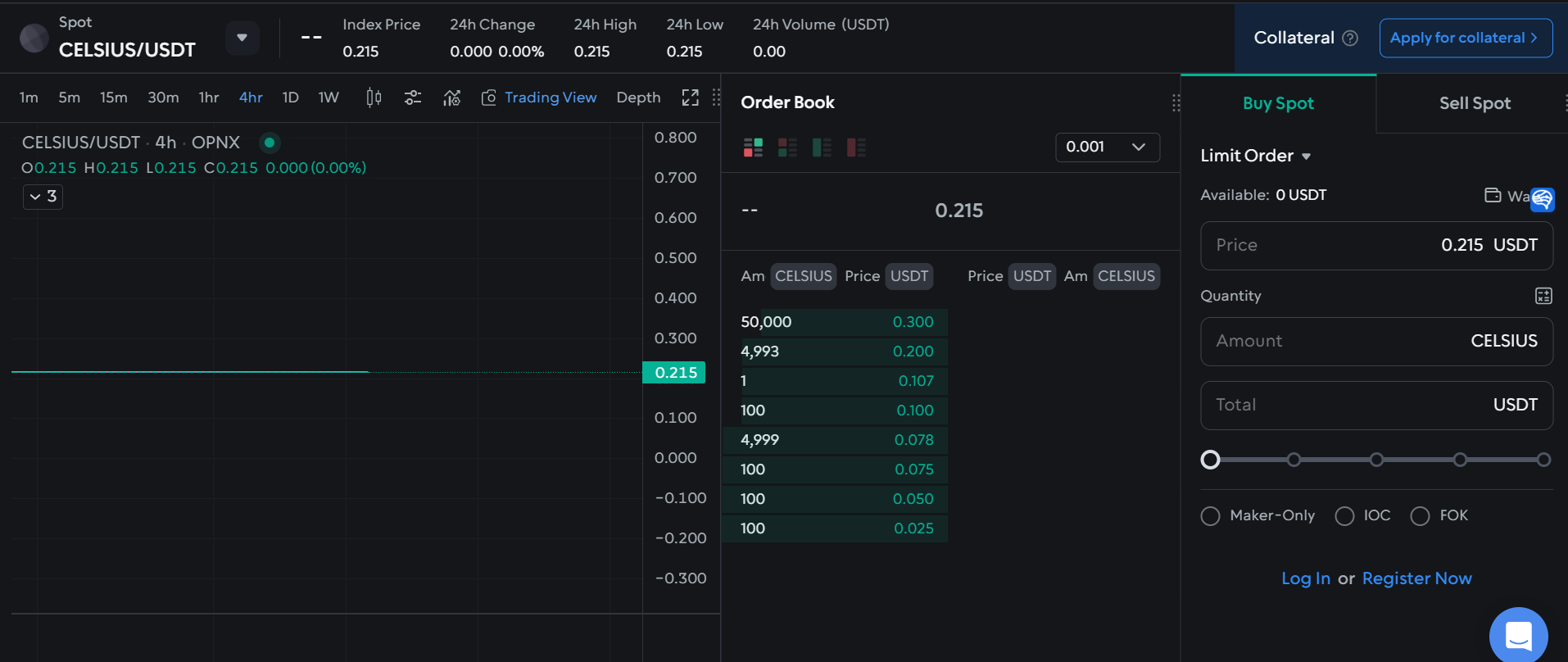

The Celsius credit token CELSIUS, launched on June 1, allows Celsius creditors to tokenize their claims to release liquidity for their trapped funds. However, as of July 4, there have been no trades on the CELSIUS/USDT trading pair since its launch, with trading volume consistently showing zero, and the token price remains a straight line with only eight sell orders on the order book.

Credit token CELSIUS price chart

Credit token CELSIUS price chart

This indicates that OPNX has not developed into the intended credit trading platform; its business has now shifted to resemble that of a traditional crypto exchange, with contracts becoming the mainstay.

In fact, there were early signs of this shift. On April 4, the platform known for credit claims trading officially launched its first feature, which was to support cryptocurrency spot and derivatives trading services, rather than the trading of tokenized claims. This has been described by community users as "using the guise of supporting crypto claims trading, while the real business is actually a contract casino." This also indicates that OPNX's business focus is on crypto asset trading rather than credit trading, as the types of claim trading assets and user groups are limited.

Additionally, on April 18, the Dubai Virtual Assets Regulatory Authority issued a written reprimand to the founders of OPNX and its CEO, stating that they were operating and promoting their digital asset trading platform OPNX without the necessary local licenses. This exposes compliance issues within OPNX.

The shadow of failure lingers, can the plan to open an exchange to repay debts be realized?

OPNX has attracted user attention through a temporary surge in trading volume and a brief spike in the platform token OX, but the shadow of the founders' dishonesty and CoinFLEX's suspension of user withdrawals remains ever-present.

On June 27, the liquidators of Three Arrows Capital were still attempting to recover $1.3 billion from its founders Su Zhu and Kyle Davies. According to a previous report by the business management company Teneo, Three Arrows Capital currently owes about $3.5 billion in claims to 27 companies. Meanwhile, the trading platform CoinFLEX has suspended all user withdrawals due to funding shortfalls, forcing its creditors and investors to become shareholders in the company.

The combination of "dishonest founders + failed platform" makes it difficult for users to fully trust OPNX, which faced significant opposition from the outset. When Su Zhu first announced the launch of the crypto credit trading platform on Twitter, one community user commented, "You should focus on talking to your lawyer instead of launching new scams." Additionally, Wintermute's CEO Evgeny Gaevoy stated that he would not invest in this new exchange established by the founders of Three Arrows Capital; crypto venture capital partner Nic Carter subsequently remarked that it sounded reasonable for disreputable fraudsters to collaborate with other disreputable fraudsters to trade the claims of a defunct fraudulent exchange.

After OPNX's launch in April, it tweeted its main investors, including AppWorks, Susquehanna (SIG), DRW, MIAX Group, China Merchant Bank International, Token Bay Capital, Nascent, and Tuwaiq Limited, stating that these institutions not only provided funding but also offered significant advice and assistance regarding its vision, token economics, legal framework, and the decision to relocate to Hong Kong.

However, the list of investors disclosed by OPNX was quickly contradicted, as DRW, Nascent, MIAX, and Susquehanna (SIG) all issued statements denying their investment in OPNX. Among them, Nascent and DRW stated that they did not participate in OPNX's financing and only invested in FLEX tokens in early 2021.

Subsequently, OPNX representatives stated that Su Zhu and Kyle Davies were no longer involved in the daily operations of OPNX. However, both still have @OPNX in their Twitter bios and share data and updates related to the OPNX platform daily. Just yesterday, Kyle Davies stated in a Twitter Space that the two founders of Three Arrows Capital would donate the "future profits" of the OPNX platform to creditors who suffered losses due to the fund's bankruptcy last year.

This aligns with users' speculation that "OPNX is an important plan for Su Zhu and others to open an exchange to repay debts." Exchanges are often considered cash cows and good businesses in the crypto industry. It has been suggested that if a trading platform has a daily trading volume of 500 BTC, it could generate a net income of half to one Bitcoin per day. So, can the wish to repay debts through the OPNX platform be realized?

Calculating the numbers, based on OPNX's daily trading volume of $50 million, with the current maker fee of 0.02% and taker fee of 0.07%, OPNX's daily fee income would be $45,000. With Three Arrows Capital currently owing about $3.5 billion in claims, it would take approximately 77,777 days, or about 213 years, to repay the debts. If we factor in the potential rise of the platform token OX, increased trading volume, and future listing fees, the repayment speed might accelerate.

However, it is worth noting that the current official Telegram group of OPNX has only 2,060 users, while the Chinese Telegram group has 2,690 members (Su Zhu's Twitter name has also been changed to the Chinese "朱溯"). This starkly contrasts with the 568,000 and 517,000 followers of Su Zhu and Kyle Davies, respectively.