zkSync Top Dex Showdown: Syncswap vs iZiswap

In the competition among head DEXs on zkSync, Syncswap's product mechanism is quite standard, lacking any impressive native innovations, while iZiswap's product has a relatively rich native exploration. However, whether this can translate into user and capital growth does not seem optimistic at the moment.

In the competition among head DEXs on zkSync, Syncswap's product mechanism is quite standard, lacking any impressive native innovations, while iZiswap's product has a relatively rich native exploration. However, whether this can translate into user and capital growth does not seem optimistic at the moment.***Author: ** Alex Xu, Mint Ventures Research Partner*

This issue's project overview focuses on the competition among leading DEXs in the emerging L2 ecosystem zkSync, attempting to answer the following questions:

-- Why is it necessary to pay attention to zkSync and its DEX track?

-- What is the current situation of trading projects on zkSync?

-- How do the various competing projects stack up, what advantages do they have, and who is more likely to win?

The following article reflects the author's views as of the time of publication, which may contain factual inaccuracies and biases, and is intended for discussion purposes only. Corrections from other research peers are also welcomed.

Why Pay Attention to zkSync and Its DEXs

zkSync: A Big Year for L2, A Strong Competitor Among Leading L2s

2023 is a big year for L2.

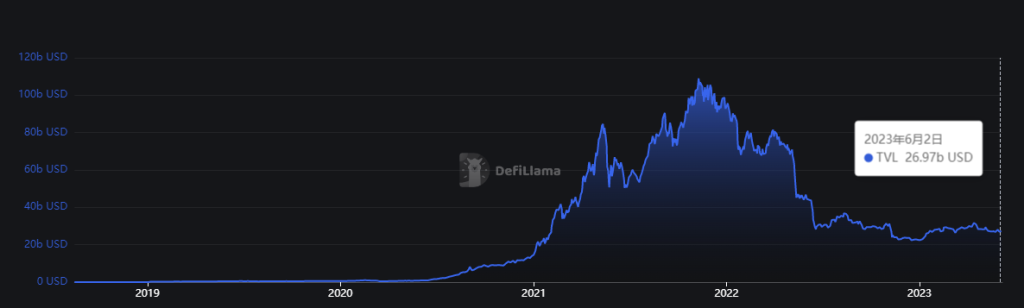

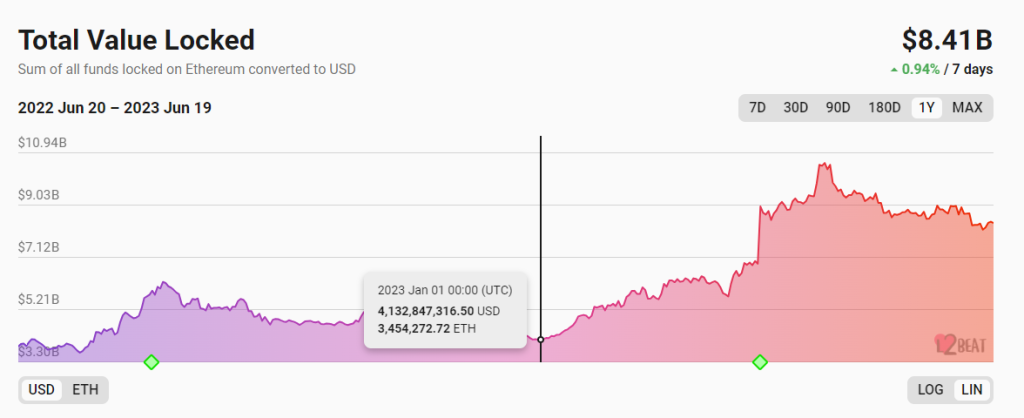

In terms of business data, while the TVL of various public chains represented by Ethereum remains low, the TVL of L2 has rapidly grown this year, breaking new highs.

Source: https://defillama.com/chain/Ethereum?tvl

Source: https://defillama.com/chain/Ethereum?tvl  Source: https://l2beat.com/scaling/tvl

Source: https://l2beat.com/scaling/tvl

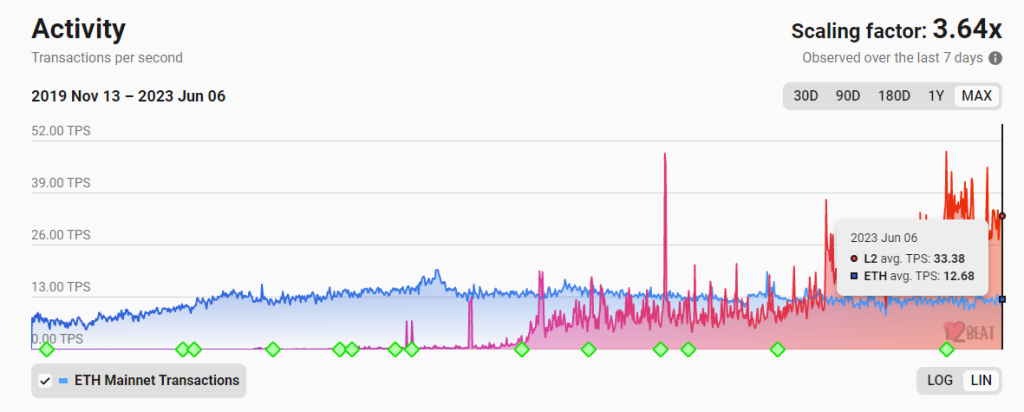

In addition to on-chain funds, active on-chain data also confirms this. Since the actual TPS of L2 exceeded that of Ethereum last October, this data has further risen rapidly this year. Currently, the actual TPS of L2 networks is about three times that of Ethereum, and this figure is expected to continue climbing in the future.

Below: Comparison of L2 Actual TPS with Ethereum

Source: https://l2beat.com/scaling/activity

Source: https://l2beat.com/scaling/activity

Beyond business data, the upcoming Cancun upgrade in October will significantly reduce costs for L2, further driving users and applications to migrate to L2.

In terms of competitive landscape, L2 is similar to L1, with a strong network effect built by users, developers, and funds, second only to stablecoins in the Web3 world, and the first-mover advantage is very evident.

In the OP Rollup space, the duopoly of Arbitrum and OP has been established, and the only potential new player that could still compete in the future might be Coinbase's L2 Base built on the OP stack, but there likely won't be many new players joining the table in the short term.

The battle in the ZK Rollup space has just begun. As a long-term direction supported by the Ethereum Foundation and Vitalik, ZK will undoubtedly occupy a place in the increasingly fierce L2 wars in the future. Following this year's Arbitrum airdrop, zkSync has become the next highly anticipated L2 airdrop project, with its TVL and user activity numbers continuing to rise. In less than three months since its launch, it has already become the L2 with the TVL second only to Arbitrum and Optimism, and it is currently the largest ZK Rollup project in terms of TVL and user count. The types of on-chain projects are also gradually diversifying, with both DeFi infrastructure and meme projects like Cheems emerging.

Overall, zkSync has already gained a first-mover advantage in the ZK L2 competition.

DEXs: Infrastructure for Gathering Users and Funds

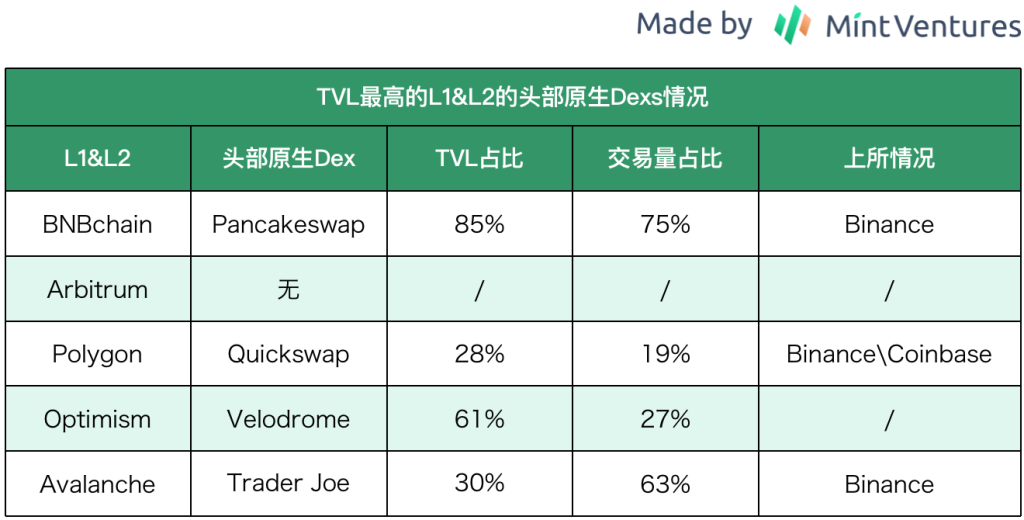

DEXs, lending, and stablecoins are the three fundamental financial components of L1 & L2. However, looking at the development of past L1 and L2, it is easy to find that each chain's leading "native DEX" often has only one. The author defines "leading" by two criteria, at least one of which must be met:

- Business data such as TVL and trading volume far exceed competitors, with at least one market share exceeding 50%

- The token has been listed on top-tier exchanges like Binance

Data Source: Defillama Date: 2023.6.7 Table created by: Mint Ventures

Data Source: Defillama Date: 2023.6.7 Table created by: Mint Ventures

As the leading DEX on its chain, it enjoys more advantages compared to other competitors, such as:

- Mental positioning: It is easier to become the preferred platform for user trading and market-making activities, with higher trust.

- Business advantages: It is easier to gain favor from other partners, becoming the first stop for liquidity deployment or a cooperative launchpad.

- Traffic convenience: Leading DEXs are more likely to be mentioned and cited in various business rankings, news, and research reports, gaining more free exposure and organic traffic.

- Cross-border network effect advantages formed by leading liquidity and trading volume.

- Tokens are more likely to be listed on top CEXs, gaining liquidity premiums and more token holders.

As a relatively new L2 ecosystem, zkSync is in the early stages of growth for users, funds, and developers, and the market landscape for various tracks has not yet solidified. Brand projects from other chains have not completed cross-chain deployments (such as Uniswap V3 and Aave), and native projects still have time to compete for and consolidate their positions.

However, the future DEX landscape on zkSync will likely mirror that of other L1 & L2s, where there is only one leading native DEX (or it may be occupied by Uniswap V3).

So the question is, who will become the leading native DEX on zkSync?

zkSync DEX Track Landscape

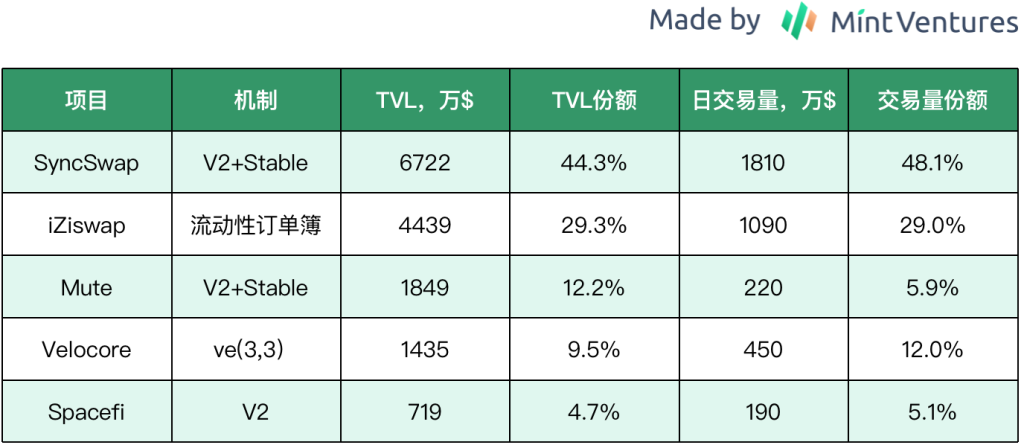

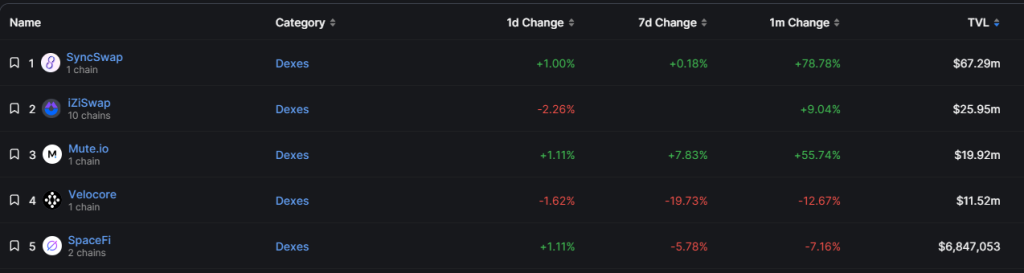

Currently, there are many DEX projects on zkSync, each adopting different mechanisms. However, from the business data, a trend of market share concentration has already emerged.

Data Source: Defillama and official project data Date: 2023.6.6 Table created by: Mint Ventures

Data Source: Defillama and official project data Date: 2023.6.6 Table created by: Mint Ventures

PS: Here, the "share" is calculated based on the total business volume of the top five DEXs.

In terms of business mechanisms, among the top 5 DEXs, 3 (SyncSwap, Mute, and Velocore) have adopted the V2 dynamic pool + stable pool model, with Velocore also using an economic model similar to Velodrome's ve(3,3) mechanism, while also engaging in liquidity market business.

However, from the two core business data points of TVL and trading volume, the current top-tier DEXs on zkSync are SyncSwap and iZiswap, with the future leading DEX likely to emerge from these two.

Syncswap vs iZiswap

Next, the author will outline and compare the basic situations of these two leading DEXs in the zkSync ecosystem, mainly covering project mechanism design, business indicators, economic models, and team situations.

Syncswap

Mechanism Design

Pool Types

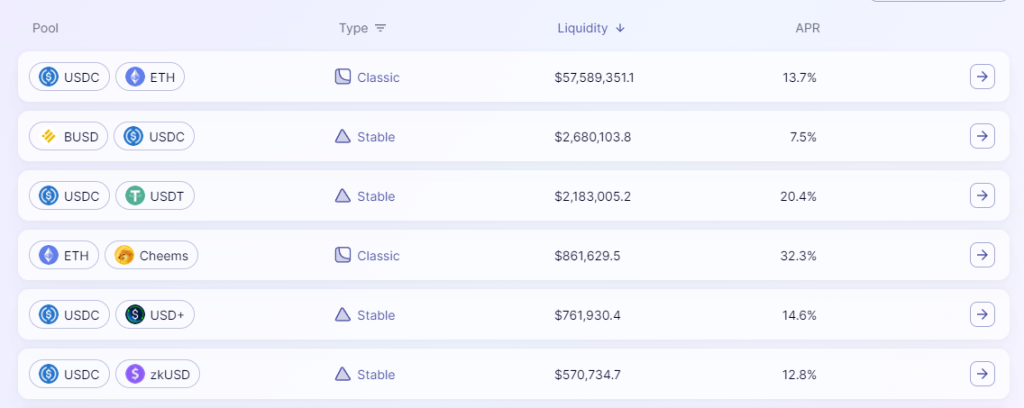

Overall, Syncswap does not have much innovation in its DEX product mechanism. It adopts a multi-pool mechanism commonly used by ve(3,3) projects, currently mainly based on Uniswap v2's Classic Pool (suitable for trading pairs with significant exchange rate fluctuations) and Curve's Stable Pool (suitable for trading pairs with stable exchange rates).

Below: Syncswap's Pool List

Source: https://syncswap.xyz/pools

Source: https://syncswap.xyz/pools

Trading Fees

Syncswap refers to its fee mechanism as "Dynamic Fees," but in reality, it is not the dynamic fee mechanism we understand (where the fee rate increases with asset price volatility to compensate LPs for impermanent loss). A more accurate expression might be "customizable fees."

Specifically, Syncswap's fees include the following features:

- Adjustable fees: Different pools can set different fee rates, with a maximum of 10%.

- Directional fee rates: Different rates are set based on the trading direction (buy/sell), for example, buy 0.1%, sell 0.5%.

- Fee discounts: Based on token staking, users can receive reductions in trading fees.

- Fee distribution agency: Fees from the pool can be directly distributed to external addresses.

It can be seen that Syncswap's Dynamic Fees are actually unrelated to "dynamics," but rather provide richer customization permissions.

Business Performance

We analyze Syncswap's business situation from four perspectives: trading volume, user count, liquidity, and trading fees (LP fees and protocol revenue).

Trading Volume and User Count

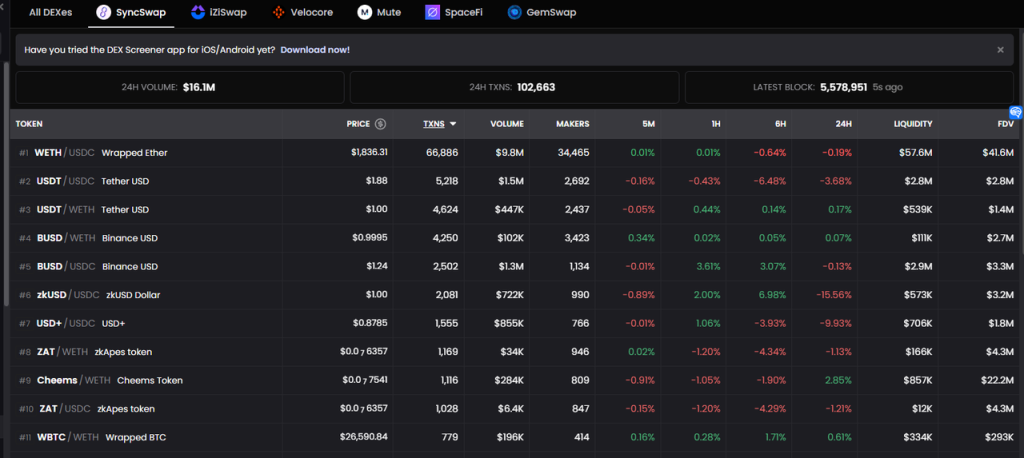

Syncswap itself does not provide a complete trading volume data dashboard. Based on on-chain data, the trading volume for Syncswap over the past 7 days and 30 days has been calculated, with a trading volume of $431,351,415 for the last 30 days (2023.5.8-6.7), corresponding to an average daily trading volume of $14,378,380; and a trading volume of $103,743,812 for the last 7 days (2023.6.1-6.7), corresponding to an average daily trading volume of $14,820,544.

The above trading data roughly matches the 24-hour trading volume statistics from Dexscreener and the official 24-hour trading volume statistics for each pool.

Below: Syncswap 24-hour Trading Volume

Source: https://dexscreener.com/zksync/syncswap

Source: https://dexscreener.com/zksync/syncswap

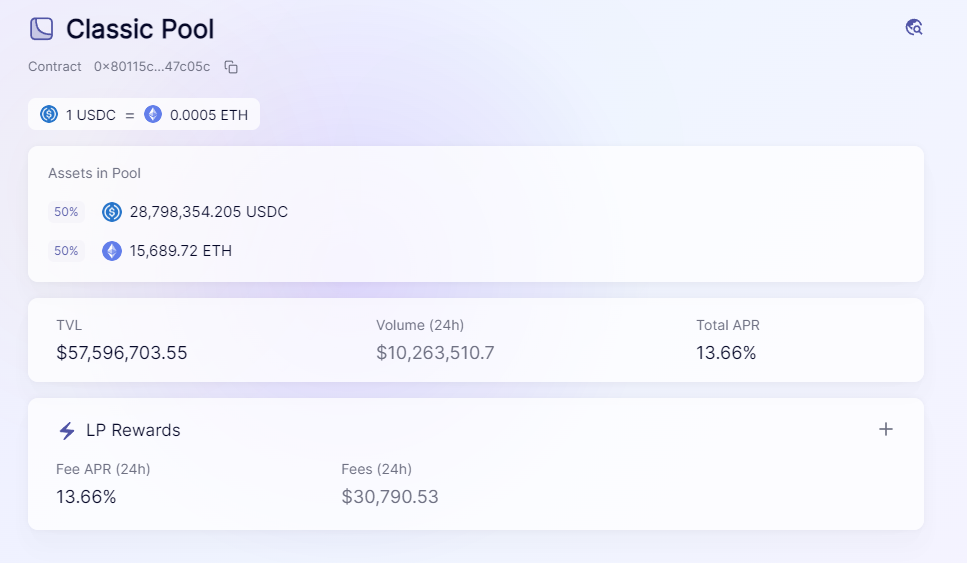

Below: Business data for Syncswap's largest trading pool, with a daily trading volume of about $10 million.

Source: https://syncswap.xyz/pool

Source: https://syncswap.xyz/pool

In the composition of trading volume, the ETH-USDC pool accounts for a significant share at 60.8%, followed by stablecoins, while the trading volume of true zkSync native assets accounts for less than 5%.

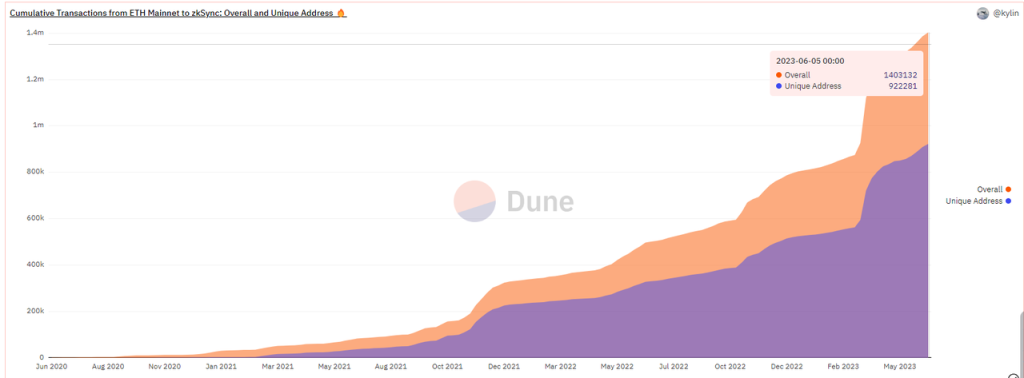

Also based on on-chain data, from 2023.5.8-6.7, Syncswap's monthly active address count was 843,692, and the weekly active address count from 6.1-6.7 was 247,814. As of 6.5, the number of unique addresses on zkSync was 922,000, which means that nearly 91.4% of addresses interacted with Syncswap within a month.

Source: https://dune.com/dev_1hermn/zksync-era

Source: https://dune.com/dev_1hermn/zksync-era

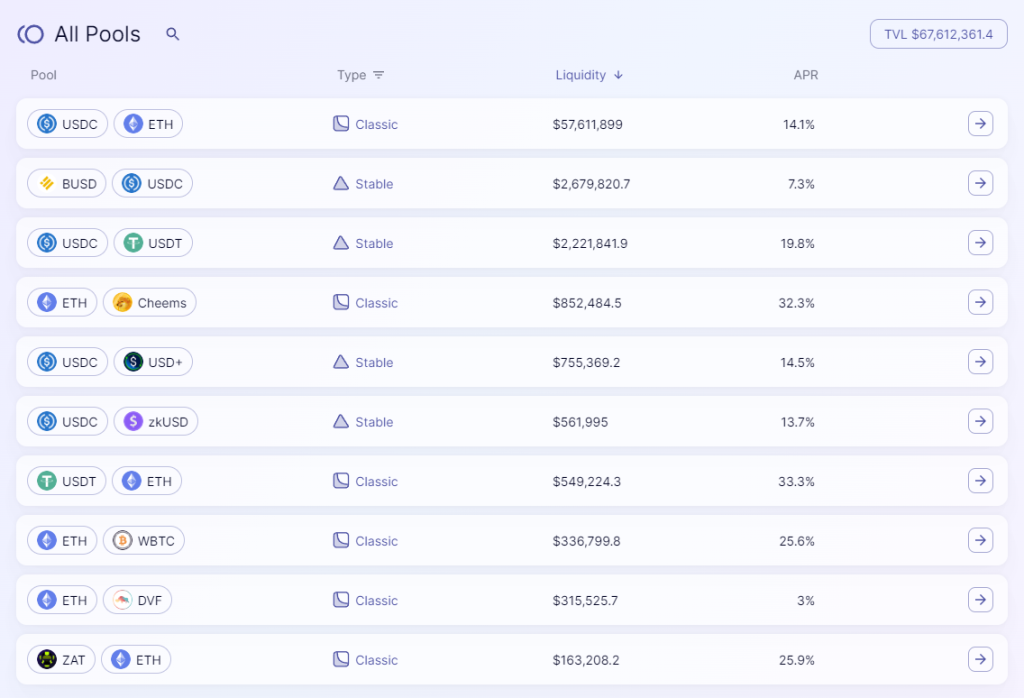

Liquidity

Syncswap's total liquidity is $67.61 million, with the ETH-USDC pool accounting for $57.61 million, or 84.5%.

Source: https://syncswap.xyz/pools

Source: https://syncswap.xyz/pools

Among the top 10 pools by liquidity, zkSync native non-stablecoin assets are Cheems (meme) and ZAT (NFT), accounting for only 1.5%.

Trading Fees and Protocol Revenue

The author has compiled the protocol revenue from the top 10 trading pools on Syncswap as of June 9, as follows:

Data Source: Syncswap Official Date: 2023.6.9 Table created by: Mint Ventures

Data Source: Syncswap Official Date: 2023.6.9 Table created by: Mint Ventures

According to the table, the protocol revenue from ETH trading pairs accounts for 90.6%, making it the bulk of fees and revenue. Additionally, Syncswap's fee-sharing ratios for Cheems and USD+ (Tangible's stablecoin) are only 10% and 20%, respectively, indicating a clear intention to attract liquidity from this segment by offering most of the revenue to LPs.

Notably, Syncswap has not yet issued a token or initiated liquidity or trading subsidies, making it a relatively rare DeFi project that can achieve positive returns. Of course, this is also related to the fact that neither zkSync nor Syncswap has issued tokens yet, and there are many airdrop hunters interacting with the platform.

Economic Model

Although Syncswap has not officially issued tokens, it has already disclosed some information about its token, which is called SYNC, with a total supply of 100 million.

In terms of token rules, Syncswap partially references Curve's ve model. Token holders need to convert SYNC into veSYNC to gain token utility, including:

- Voting governance

- Protocol fee dividends

- Trading fee discounts

However, the specific unlocking mechanism differs from Curve. After choosing to unlock, veSYNC has a linear unlocking period of 6 months, during which 50% of the tokens can be obtained on the 20th day after unlocking, while the remaining 50% continues to unlock linearly.

Despite this, the disclosure of Syncswap's token economic model is still incomplete, as it does not mention the token distribution ratios, release speeds, or whether the ve model will be used to guide token pool emissions. However, based on the overall mechanism of the project, Syncswap resembles a ve(3,3) DEX project.

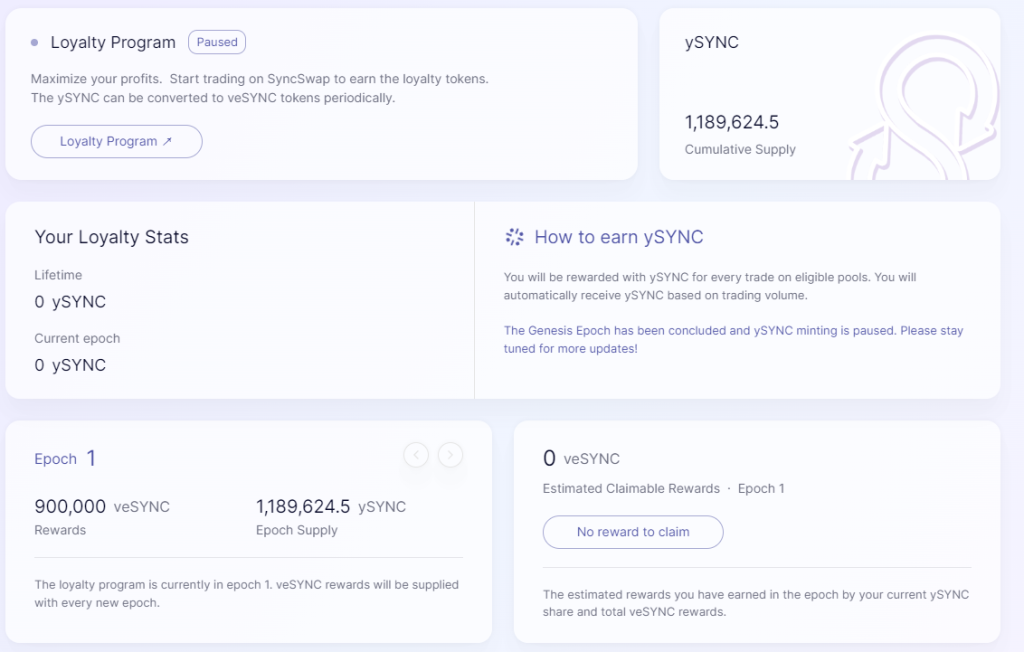

Additionally, although the SYNC token has not been listed, Syncswap has launched a token incentive program called "Loyalty Program." This program incentivizes fees generated from specific trading pairs, similar to "trading mining."

Source: https://syncswap.xyz/rewards

Source: https://syncswap.xyz/rewards

The token mining rules for the Loyalty Program are as follows:

- The more trading fees generated by users trading on designated trading pairs, the more activity reward tokens (ySYNC) they receive, where the number of ySYNC obtained = user-contributed trading fees.

- A program cycle is referred to as an epoch, with the first epoch (epoch 1) lasting one month, while subsequent epochs last one day.

- Users can redeem rewards based on ySYNC, but rewards are distributed in veSYNC, and if users wish to sell, they must first unlock veSYNC.

The genesis epoch of the Loyalty Program ran from April 10 to May 10 this year, with a total reward of 900,000 veSYNC. The final number of ySYNC obtained by participating users was 1,189,624.5, indicating that during the event, users paid a total of $1,189,624.5 in trading fees on designated trading pairs, corresponding to a cost of approximately $1.32 per 1 veSYNC obtained.

However, the Loyalty Program is currently paused, having only conducted one round.

Team and Financing

The Syncswap team is anonymous, with unclear team size and personnel, and no financing news has been disclosed.

iZiswap

Mechanism Design

iZiswap is one of the products of iZUMi Finance, which is a DeFi project providing multi-chain liquidity services (Liquidity as a Service, LaaS). iZiswap is its DEX product for liquidity services, and other products currently launched include:

- LiquidBox: A liquidity incentive service based on concentrated liquidity (Uni V3 and its derivative models), which helps project parties customize liquidity incentives based on price ranges.

- Bond financing service: Provides project parties with a financing method similar to convertible bonds in traditional finance.

This article mainly focuses on the competition among leading DEXs in the zkSync ecosystem, so it will primarily look at iZiswap's situation on the zkSync network.

The main innovation of iZiswap lies in the proposal and implementation of DL-AMM.

DL stands for Discretized Concentrated Liquidity. DL-AMM does not use a constant product formula but instead places liquidity at discrete different price points, with each price point following a constant sum formula L = X * √P + Y / √P.

Countless discrete price points are connected to form a complete AMM price curve similar to Uniswap, as shown on the left in the diagram.

Source: https://assets.iZUMi.finance/paper/dswap.pdf

Source: https://assets.iZUMi.finance/paper/dswap.pdf

In DL-AMM, liquidity is divided into two categories: LP liquidity and limit order liquidity. The two are combined and distributed in different price areas, as shown on the right in the diagram.

The former is dual-token liquidity, while the latter is single-token liquidity, aiming to exchange one token for another at a specific price. Once the target price is reached, it will be exchanged and will not be swapped back (Uni V3 can also achieve limit order logic through one-sided liquidity in a small range, but when the price returns, it will be swapped back to the original token), and it will remain in the contract until the user withdraws it.

Additionally, based on the point distribution characteristics of iZiswap's liquidity, it also provides an order book trading interface version (iZiswap Pro), offering users a trading experience similar to CEXs.

Source: https://iZUMi.finance/trade

Source: https://iZUMi.finance/trade

Speaking of liquidity order books, it is easy to think of the more well-known DEX project Trader Joe, which launched the Liquidity Book (LB) in November 2022, also distributing liquidity points, with specific price points using a constant sum formula rather than a constant product.

For more details on Trader Joe, you can read the author's research report “Borrowing Arbitrum for a Second Spring? A Comprehensive Analysis of Trader Joe's Business Status, Token Model, and Valuation Level”.

In fact, the liquidity order book concept of Trader Joe likely originated from the DL-AMM proposed by iZUMi. The paper on DL-AMM titled “iZiSwap: Building Decentralized Exchange with Discretized Concentrated Liquidity and Limit Order” was published in November 2021, while iZiswap launched in May 2022 (initially on BNBchain), well before Trader Joe's LB feature went live. Trader Joe also acknowledged and referenced iZUMi in its V2 white paper.

In addition to DL-AMM, iZUMi has also designed a liquidity incentive service based on concentrated liquidity called LiquidBox. The liquidity mining incentives based on V2 are straightforward: users stake LP certificates to receive token rewards, which incentivizes liquidity across all price ranges. However, the incentive designs for V3, DL-AMM, and BL-type concentrated liquidity are much more complex.

Assuming a token priced at $100, one LP provides liquidity with $1,000 in the $95-$105 range, while another LP provides liquidity with $1,000 in the $10-$20 range (one-sided order). The liquidity utilization efficiency of the former is much higher than that of the latter. If we refer to the V2 model and provide the same rewards based on liquidity value, it is clearly unreasonable.

For users, LiquidBox is where they deposit liquidity and receive incentives, while for the incentivizers (usually token project parties and iZUMi), it allows for differentiated range allocation of the obtained liquidity to achieve the liquidity goals desired by the project parties.

LiquidBox offers three plans, which are jointly decided by the liquidity incentivizers (usually token project parties and iZUMi):

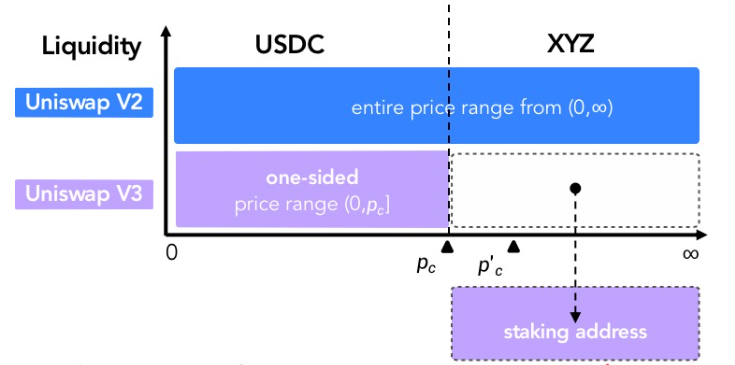

- One-sided mode: The project tokens deposited by users will not be placed in the pool but will be staked separately to reduce the number of project tokens in the pool, lowering resistance during price increases; the other half (value tokens such as ETH or stablecoins) will be allocated to the left side of the current market price to strengthen buying pressure during price declines. For project parties, this effectively achieves the goal of "increasing token buy pressure and reducing token sell pressure." For users, if the project token price rises, there will be no impermanent loss caused by "selling while the price rises." However, if the token price declines, the failure to sell the project token at a high price will amplify the impermanent loss caused by the decline. Thus, this can be understood as a mechanism encouraging users to stake tokens without selling, a joint (3,3) market-making mechanism.

Below: Comparison of One-sided Mode with V2

Source: iZUMi Documentation

Source: iZUMi Documentation

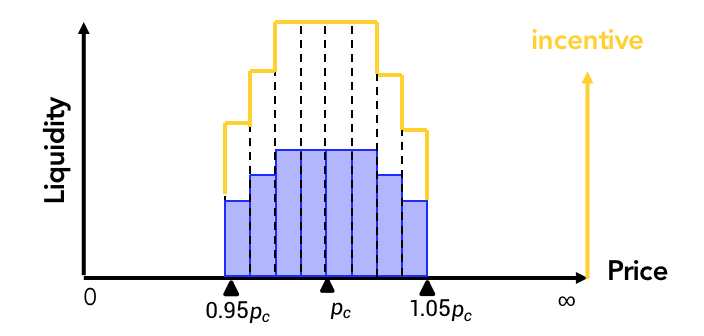

Fixed range mode: This is relatively easy to understand, as it incentivizes liquidity within a fixed price range, which is more suitable for stablecoins and wrapped assets.

Incentives for Fixed Range, Source: iZUMi Documentation

Incentives for Fixed Range, Source: iZUMi DocumentationDynamic mode: Users participate in liquidity mining by providing liquidity within the range of (0.25Pc, 4Pc) around the current price (Pc). The width of the price range can also be set by the project party, such as (0.5Pc, 2Pc). The benefit is that there will be better liquidity around the market price range, but if the token price fluctuates significantly beyond the user's initial market-making range, users will face impermanent loss and will need to frequently withdraw LP and re-stake, leading to higher operational costs.

In practice, most active LiquidBox pools currently choose the dynamic mode.

Additionally, LiquidBox supports LPs from Uniswap V3 and iZiswap to participate in staking incentives, with most of the opened incentive pools on the zkSync network.

Business Performance

Trading Volume and User Count

The author also uses on-chain data to compare iZiswap's data with Syncswap's data during the same period. Its trading volume for the last 30 days (2023.5.8-6.7) was $195,025,494, corresponding to an average daily trading volume of $6,500,849; and a trading volume of $60,007,769 for the last 7 days (2023.6.1-6.7), corresponding to an average daily trading volume of $8,572,538.

The above trading data roughly matches the 24-hour trading volume statistics from Dexscreener and the official 24-hour trading volume statistics for each pool.

Source: https://dexscreener.com/zksync/iziswap

Source: https://dexscreener.com/zksync/iziswap  Source: https://analytics.iZUMi.finance/Dashboard

Source: https://analytics.iZUMi.finance/Dashboard

Similar to Syncswap, iZiswap's ETH-USDC trading volume is even more extreme, with the two pools accounting for 85.8% of the total daily trading volume, followed by stablecoins and its own token IZI.

Also based on on-chain data, from 2023.5.8-6.7, iZiswap's monthly active address count was 301,993, and the weekly active address count from 6.1-6.7 was 102,938, which is about 35-40% of Syncswap's active addresses.

Liquidity

In terms of liquidity statistics, there is a significant discrepancy between the data provided by iZiswap and that provided by Defillama. The official dashboard shows current liquidity at $44.78 million, while Defillama's data shows $25.95 million.

iZiswap Officially Disclosed Liquidity Data

iZiswap Officially Disclosed Liquidity Data  Defillama's zkSync DEX TVL Ranking

Defillama's zkSync DEX TVL Ranking

The reason for this discrepancy is that the official liquidity statistics include a significant amount of self-issued stablecoins and wrapped assets by iZUMi, such as iUSD (debt financing stablecoin) and slstETH, slUSDT (wrapped assets issued cross-chain based on Ethereum collateral), as shown below.

However, in the current market environment, promoting self-issued stablecoins and wrapped assets is quite challenging, as there are third-party single-point risks associated with asset redemption. Most users and mainstream DeFi do not readily accept third-party issued wrapped assets. Additionally, according to iZUMi's feedback, wrapped assets represented by slstETH are still in the preparation phase and have not officially started operations. Therefore, we will rely on Defillama's statistics for TVL observation, as they are more reliable.

After accounting for the aforementioned wrapped and self-issued stablecoin TVL, iZiswap's TVL is similar to Syncswap's, with the ETH pool accounting for 86.8%.

Regarding liquidity incentives, iZiswap has launched a considerable number of LiquidBox mining pools on zkSync, all adopting a dual incentive model of project party tokens + IZI tokens.

Source: https://iZUMi.finance/farm/iZi/dynamic

Source: https://iZUMi.finance/farm/iZi/dynamic

The author has calculated the current dual mining token rewards and found that the majority of the total rewards for liquidity incentives are funded more by the project party, although there are a few pools where the project party token has declined, making the IZI token more valuable.

Currently (as of 2023.6.14), the total amount of IZI tokens for the 8 LiquidBox liquidity incentive tokens on zkSync is 60,180 per day, valued at approximately $1,208.

Trading Fees and Protocol Revenue

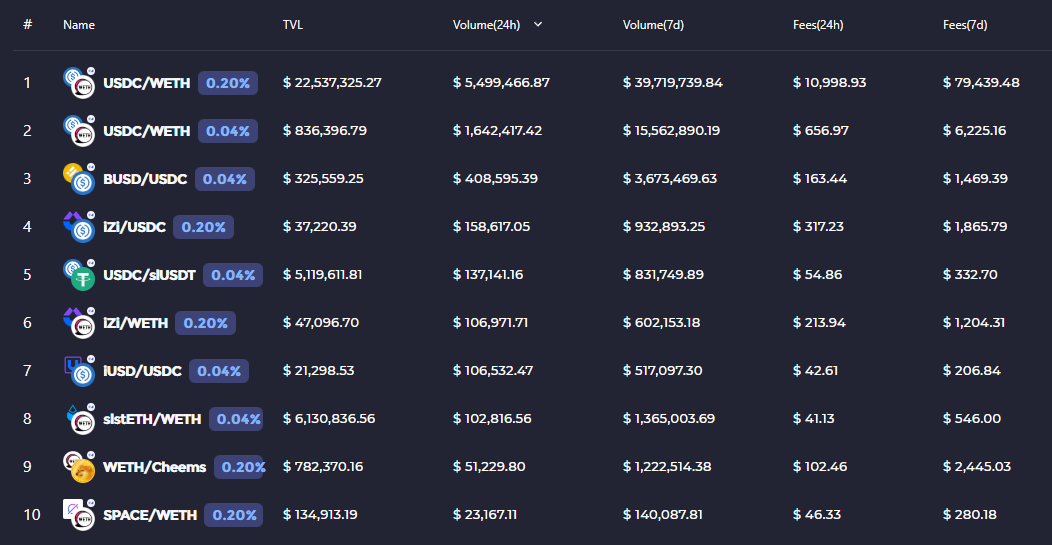

iZiswap's data dashboard displays the fee situation generated by each pool, with the following being the ranking of the top 10 pools by weekly fees.

Data Source: iZiswap Official Date: 2023.6.14 Table created by: Mint Ventures

Data Source: iZiswap Official Date: 2023.6.14 Table created by: Mint Ventures

PS: Protocol distribution revenue refers to the income allocated to IZI token users, which is 25% of the fees.

Compared to Syncswap's daily protocol revenue of $11,631.4, iZiswap's daily protocol revenue is $6,312.5. However, according to the token design, 50% of this revenue will be used to repurchase iUSD and serve as market funds, meaning that only 25% of the fees are distributed to IZI token users.

Economic Model

iZiswap is a product module of iZUMi and is currently the main module generating revenue. In terms of business scale and development prospects, zkSync is currently iZiswap's most important battlefield.

Total Supply, Distribution, and Supply Rate

iZUMi's project token is IZI, with a total supply of 2 billion, distributed across Ethereum, BNBchain, Polygon, Arbitrum, and zkSync.

Its token distribution and release speed are as follows:

Source: https://docs.iZUMi.finance/tokens/tokenomics

Source: https://docs.iZUMi.finance/tokens/tokenomics

According to CMC data, the total amount of unlocked tokens is 787,400,000, but 276,091,843.3 IZI are currently staked in ve.

Token Use Cases

The planned uses for the IZI token are threefold:

Governance voting: Used for voting on the direction of token emissions (not yet launched).

Staking dividends: Staking can earn a distribution of 25% of iZiswap's fees used for repurchasing IZI.

Yield acceleration: Staking can accelerate mining in LiquidBox by up to 2.5 times, similar to Curve's boost mechanism.

The intrinsic value of ve model DEX tokens primarily comes from two sources: 1. The governance value of directing liquidity, which is determined by the liquidity price of the corresponding DEX and is influenced by the liquidity procurement needs of other project parties on the chain; 2. The cash flow discount from fee dividends.

Currently, iZiswap's ve voting function has not yet been launched, and the distribution of trading fees is split by the bond repurchase module, suppressing the intrinsic value of the token.

Team and Financing

According to information disclosed by Rootdata, the founder of iZUMi Finance is Jimmy Yin, a graduate of Tsinghua University, and the current team size is over 20.

According to data disclosed by Rootdata, iZUMi has conducted a total of 4 rounds of financing:

- 2021.11: Seed round, $2.1 million, corresponding to a valuation of $14 million.

- 2021.12: Series A, $3.5 million, corresponding to a valuation of $35 million.

- 2022.5: Raised $30 million through Solv via convertible bond financing for liquidity operations.

- 2023.4: Raised $22 million through Solv in a fund format for liquidity operations.

Notably, in the last two rounds of financing, iZUMi did not use direct token sales but opted for bonds or fund-raising methods, with the financing purpose not only for project expenses and team recruitment but also for liquidity operations (market-making), with operational profits used for team income and financing returns.

Conclusion

In the competition among leading DEXs on zkSync, Syncswap's product mechanism is conventional, lacking any impressive native innovations, while iZiswap's product has a richer native exploration. However, whether this can translate into user and fund growth currently looks pessimistic. From specific business data, Syncswap clearly leads in both TVL and trading volume, and its unallocated token and expectations for project airdrops strongly attract user funds and trading behavior, enjoying lower operational costs (in contrast, iZiswap still incurs daily expenses for token incentives).

However, both currently face the common issue that zkSync, having been established for a short time, lacks a sufficient number of viable native projects, with most of the liquidity and trading volume of the two DEXs being related to ETH.

In the future, more native projects will emerge on zkSync. Which platform will these projects choose to deploy their initial liquidity on? The more advanced zkSync or the more richly mechanized iZiswap? This also leaves some suspense for future competition. Additionally, Uniswap had already voted in October 2022 to deploy V3 on zkSync, which could enter this new market at any time, bringing greater competitive pressure.

We look forward to the subsequent developments.