After the Shapella upgrade: Long-term impacts on yield, competition, and LSD-Fi

The level of staking rewards is a determining factor for whether ordinary users participate in staking. To explore the future development of ETH staking, we need to understand the composition of staking rewards and the future development trends.

The level of staking rewards is a determining factor for whether ordinary users participate in staking. To explore the future development of ETH staking, we need to understand the composition of staking rewards and the future development trends.Author: Mint Ventures

The Past and Present of ETH Staking

Before we begin, we need to briefly review ETH staking. Unlike most PoS public chains currently online, Ethereum's PoS does not support native delegation and limits the maximum staking amount for a single node (profitable) to 32 ETH. The advantages of this staking method are obvious, as it minimizes the possibility of a single entity influencing Ethereum's consensus by controlling a large node, thus maintaining the decentralization of the Ethereum network as much as possible. However, due to the operational complexity of node management, which is quite high for ordinary users, in practice, apart from solo staking where users stake by themselves, three other types of staking methods have gradually emerged: staking pools, liquid staking, and CEX staking. The characteristics of these four staking methods are as follows:

- Solo staking means that the staking user handles all staking processes and subsequent maintenance themselves, with the main drawback being the high requirements for equipment, funds, knowledge, and network.

- Staking pools alleviate the user's need for network and hardware to some extent. Staking users only need to pay a certain fee to hire professional staking service providers to stake their 32 ETH for returns. This method also ensures that the withdrawal private key is still controlled by the staker, maintaining a higher degree of control over funds. However, it still has high requirements for the staker's funds and knowledge. In some classifications, this staking method is also referred to as Staking as a Service.

- Liquid staking takes this a step further by outsourcing the specific operation of nodes to professional node operators, allowing staking pools to collectively pool users' ETH for staking operations, enabling users to stake any amount. Meanwhile, the staking pool issues a staking derivative called LSD (Liquid Staking Derivatives/Tokens, which we will refer to as LSD hereafter). LSD currently has a rich set of use cases in DeFi, which we will introduce in detail later. Of course, in essence, all staked funds belong to the contract of the staking pool, so stakers need to trust the staking pool. In some classifications, this staking method is also referred to as pooled staking.

- CEX staking is handled entirely by centralized exchanges (CEX), which also allows users to stake any amount and usually issues staking certificates (such as Coinbase's cbETH and Binance's bETH) to users.

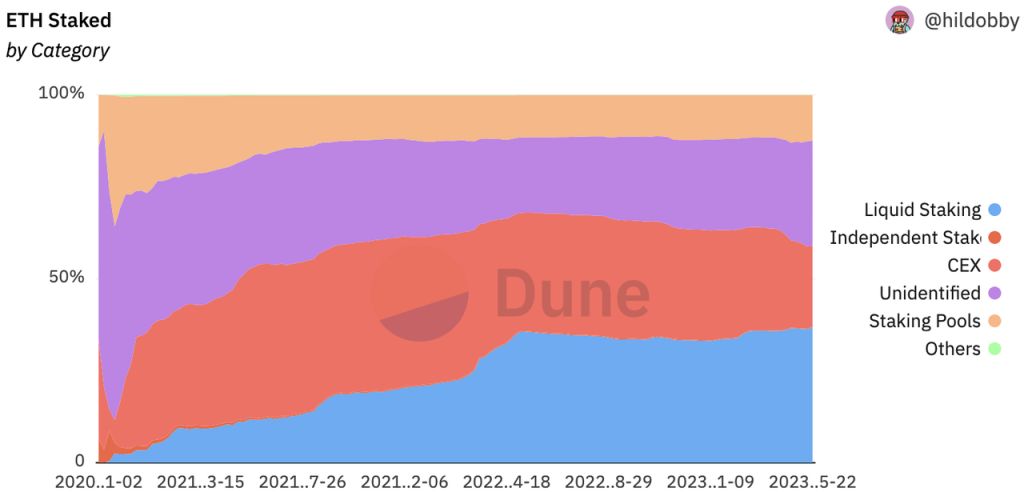

The following chart shows the historical changes in the relative share of ETH staking.

Source: https://dune.com/hildobby/eth2-staking (Note: Due to the complexity of statistics, the proportion of solo staking is difficult to quantify. In most staking classification statistics, there is a category called "Unidentified" (shown in the chart above). According to a recent analysis by Rated, currently, 6.5% of the total staking amount is provided by solo stakers.)

From the chart above, we can clearly see that, except for the first two months after the Beacon Chain went live, until April 2022, CEX staking quickly became the leader in staking due to the large amount of ETH naturally held by users on CEX as a means of earning. This situation was not what the Ethereum Foundation and community members wanted to see. However, with institutions like Paradigm investing in Lido and the gradual establishment of good liquidity and composability for stETH, Lido rapidly developed, subsequently driving the growth of the entire liquid staking category. To this day, liquid staking continues to hold a leading position in the field.

After the successful launch of Shapella, the share of CEX staking has seen a significant decline, with a considerable portion of users who originally staked ETH on CEX beginning to transition to liquid staking and solo staking (Unidentified).

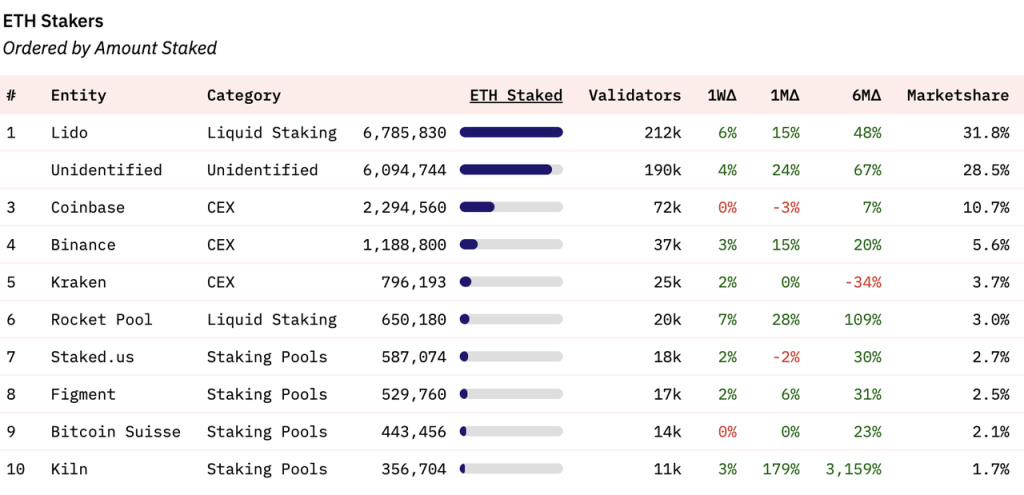

Looking at specific staking entities, Lido currently occupies 31.8% of the total staking market share, while the 3rd to 5th positions are held by three centralized exchanges, the 6th position is another liquid staking service provider, Rocket Pool, and the 7th to 10th positions are all staking pools.

Source: https://dune.com/hildobby/eth2-staking

Future Yield of ETH Staking

The level of staking rewards is a decisive factor for ordinary users considering participation in staking. To explore the future development of ETH staking, we need to understand the composition of staking rewards and future trends. We know that after the Merge, staking Ethereum can earn rewards from both the consensus layer and the execution layer. Currently, the total APR from these two parts is 5.4%.

Source: https://ethereum.org/en/staking/

The rewards from the consensus layer are ETH issued by the Ethereum network, and the release of these rewards increases with the total amount staked. However, the APR for staking decreases as the total amount of staked ETH increases. Currently, the APR for consensus layer rewards is 3.4%. The market generally estimates that by the end of this year, the ETH staking rate will be around 25-30%. When the staking rate reaches 30%, the APR for consensus layer rewards will be approximately 2.4%. This reward is much lower than that of most PoS chains and reflects the Ethereum Foundation's principle of "minimizing ETH issuance."

The rewards from the execution layer of Ethereum staking consist of two parts: 1) the network's priority fee (the portion of gas paid by users that is not burned), and 2) MEV. Both of these components share the characteristic that their earnings do not increase with the amount of staked ETH. This part is the main variable of ETH staking rewards, and we need to study it further.

Source: https://transparency.flashbots.net/

Source: https://dune.com/LidoAnalytical/lido-execution-layer-reward (where CLAPR represents consensus layer earnings; ELAPR represents execution layer earnings)

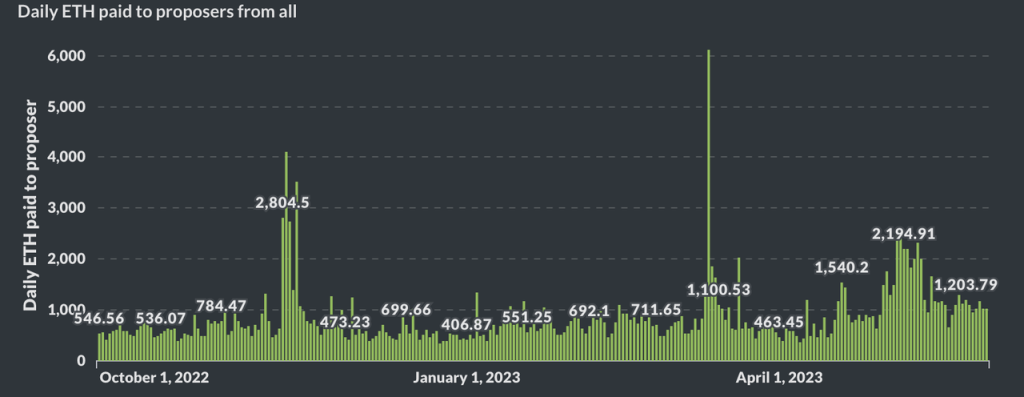

Flashbots has compiled the total income of proposers (i.e., validators) since the Merge. Lido has also tracked the APR of Lido's consensus layer and execution layer earnings since the Merge, showing consistent trends. Lido has also compared the earnings from the consensus layer and execution layer, and we will analyze this in detail using Lido's charts.

We can see that after the Merge, the APR from the consensus layer has been slowly decreasing as the total amount staked increases, while the APR from the execution layer fluctuates significantly, averaging around 1.5%, allowing staking returns to reach 5%. During periods of high on-chain activity (such as the meme season in May), the APR from the execution layer can even exceed that of the consensus layer, bringing the yield for staking Ethereum close to 10%. Staking rewards serve as the "risk-free rate" of the Ethereum network (see Mint Clips|How Should the Native Benchmark Interest Rate in the Crypto World Be Defined?), making it highly attractive for ETH holders.

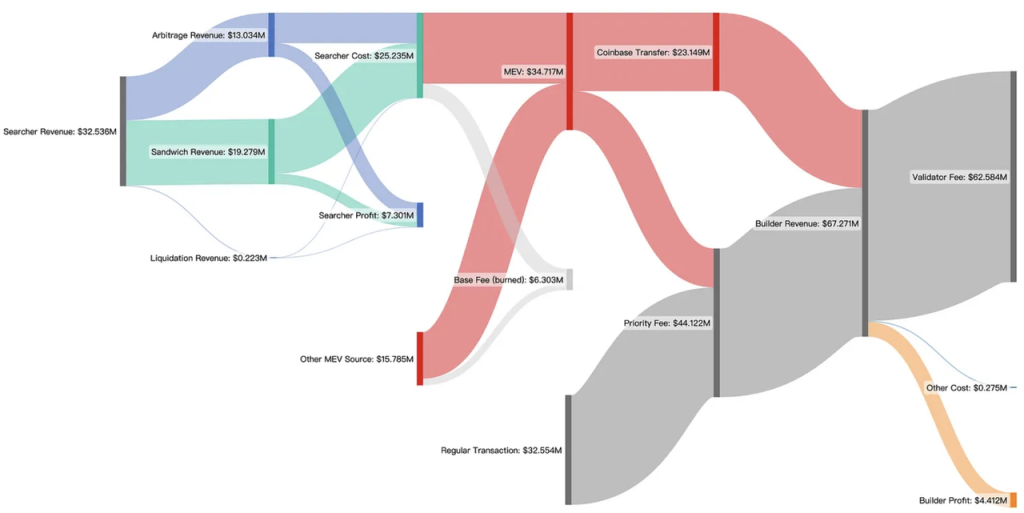

So how will execution layer earnings evolve in the future? We first need to understand the proportion of priority fees and MEV in the execution layer earnings of stakers. We can refer to a detailed analysis by the MEV data provider Eigenphi on the income data of various roles in the Ethereum execution layer from January to February 2023:

Source: https://eigenphi.substack.com/p/value-allocation-in-mev-supply-chain

We can see that over the two months, priority fees and MEV constituted the Ethereum staking earnings (Validator fee) at a ratio of approximately 55%:45% (44.12 million:34.72 million).

Next, we will explore the future trends of priority fees and MEV.

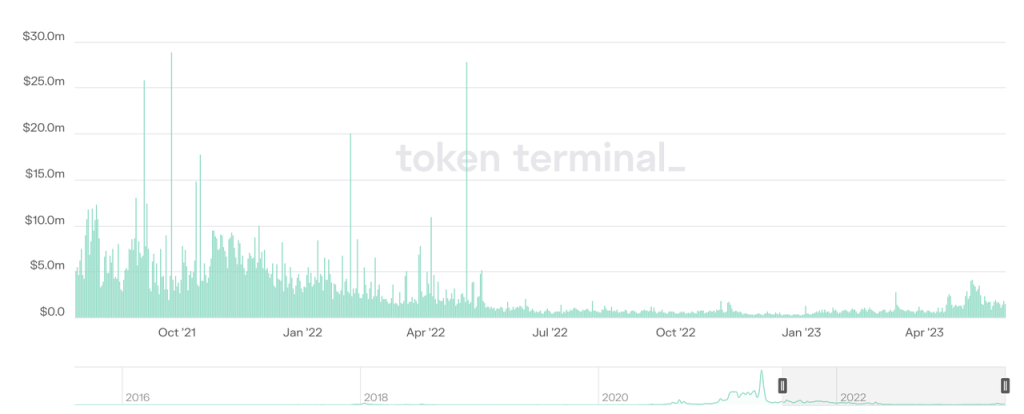

Ethereum Network Priority Fees Source: https://tokenterminal.com/terminal/projects/ethereum

Regarding priority fees, since the launch of EIP-1559, the market has gone through a cycle of bull and bear. We can see that priority fees are closely related to market activity. During the bull market in 2021, the daily average priority fee could approach 10 million USD, while during the bear market in 2022, the daily average priority fee was around 800,000 USD. In May of this year, during the Meme Season, the daily average priority fee reached about 3 million USD. In the future, priority fees will continue to fluctuate with market conditions, and this income is ETH-denominated, meaning it will continue to fluctuate with market conditions.

The situation with MEV is more complex. In addition to the MEV that cannot be fully analyzed on-chain, its composition mainly includes arbitrage, sandwich attacks, and liquidations. We currently do not have the latest trend data on MEV since the Merge. However, the Ethereum Foundation has had a generally negative attitude towards MEV for a long time. A year ago, they proposed the PBS (Proposer-Builder Separation) plan, one of the goals of which is to eliminate the impact of MEV on small stakers' earnings. Recently, Justin Drake from the Ethereum Foundation Research Institute proposed a plan called MEV burn, which aims to eliminate MEV entirely in the next 3-5 years, serving as another force for Ethereum's deflation. Although this plan is still in the planning stage and involves many interest trade-offs, Ethereum has demonstrated the ability to "persuade" key stakeholders within the ecosystem to forgo their interests in order to realize Ethereum's roadmap, as evidenced by its successful transition from PoW to PoS.

Therefore, the MEV, which currently accounts for about 20% of total staking earnings, is likely to be reduced or even disappear in the medium to long term due to its misalignment with the values of the Ethereum Foundation.

Another marginal factor worth noting is L2. Driven by the rollup-centric Ethereum roadmap, an increasing number of transactions will inevitably shift from Ethereum L1 to L2, thereby reducing the MEV and priority fees on the Ethereum mainnet. Currently, the MEV/priority fees on L2 are handled independently by L2 and are unrelated to the stakers on the Ethereum mainnet. Especially after the Cancun upgrade further reduces ETH L2 fees, this may drive further growth of L2, potentially leading to a further decrease in the overall fees + MEV that L1 can obtain.

In summary, considering the impacts of MEV burn and L2 on the composition of ETH staking earnings, when the ETH staking ratio reaches 30%, the earnings from ETH staking are likely to drop to around 3% (including 2.4% from the consensus layer and 0.6% from the execution layer). This yield will significantly affect users' enthusiasm for participating in staking.

Liquid Staking Will Remain the Mainstream Staking Method, with Potential for Increased Centralization

The Shapella upgrade activated the withdrawal function for ETH, granting liquidity to ETH staked through solo staking and staking pools. The core reason for the rapid development of liquid staking from 2021 to 2022 is that liquid staking protocols can provide liquidity for LSD, effectively enabling withdrawal from staking. Therefore, the Shapella upgrade has clearly diminished the advantages of liquid staking. Although solo staking still has a considerable operational threshold, tools serving solo stakers are increasingly available, gradually lowering the barrier for solo staking. Additionally, solo staking maintains the legitimacy of decentralizing the Ethereum network and has strong support from the Ethereum Foundation.

Why do we still believe that liquid staking will maintain its advantageous position in the staking arena, and even see further increases in concentration?

The main reason lies in composability. LSD possesses good composability, which means the potential for higher returns and greater capital efficiency. Users participating in staking are naturally sensitive to returns and tend to choose staking methods that offer higher yields. The high composability of LSD effectively provides staking users with higher returns.

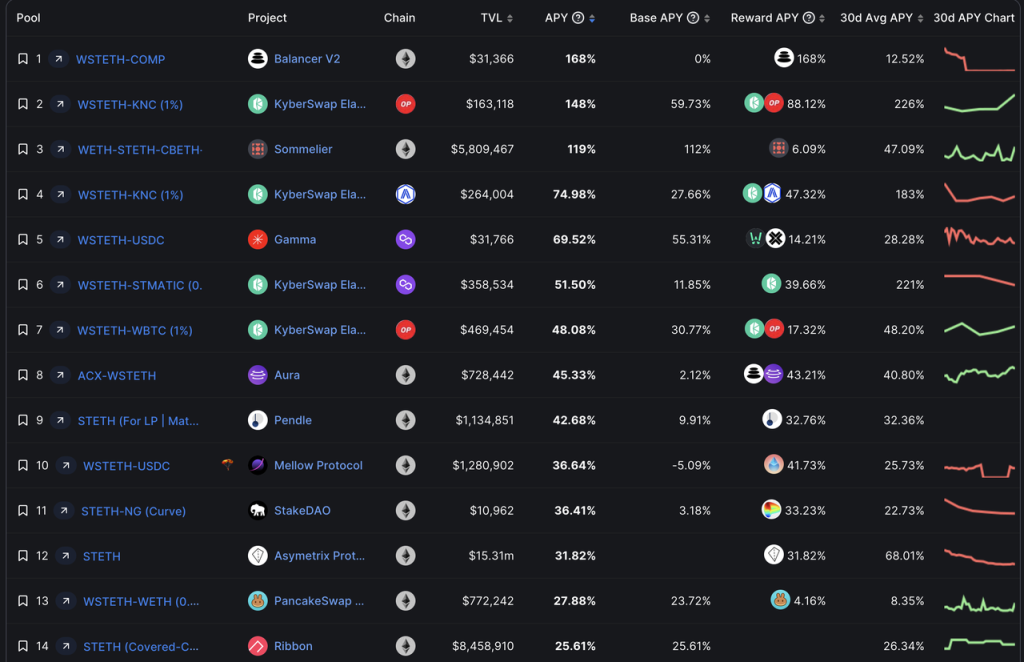

Currently, with the base yield for staking at 5.6%, LSD can easily achieve an APR of 10%. Taking Lido's stETH as an example:

Source: h ttps://defillama.com/yields?token=STETH

We can see that stETH LP can easily achieve an APR of over 50%. Considering the capital occupation of paired assets, the total APR can exceed 25%. Meanwhile, stETH can also achieve an APR of over 25% in Asymetrix (LSD's pool together) and Ribbon (options protocol) (though it may face some risks). When combined with stETH's own 5.6% APR, the total yield for users staking through Lido can reach 30%.

In addition to high yields, stETH is also widely integrated into blue-chip DeFi protocols: Maker, Aave, and Compound all support stETH (wstETH) as collateral, with collateral parameters not significantly different from ETH. In Curve, the stETH-ETH pool still has over 1.1 billion USD in liquidity, making it much easier for stETH holders to obtain liquidity through direct swaps or collateralized lending.

These advantages are not available through solo staking or staking pools. Especially if the ETH staking yield, as mentioned earlier, drops to only 3%, considering the equipment, knowledge, time, and effort expended by solo stakers and pool stakers for a 3% yield, people are likely to choose simpler and higher-yielding options.

Ethereum community users are willing to maintain the decentralization of Ethereum, but they also need to consider opportunity costs. "Maintaining Ethereum's decentralization is important and cool, but I still prefer to choose 30%."

LSD and LSD-Fi

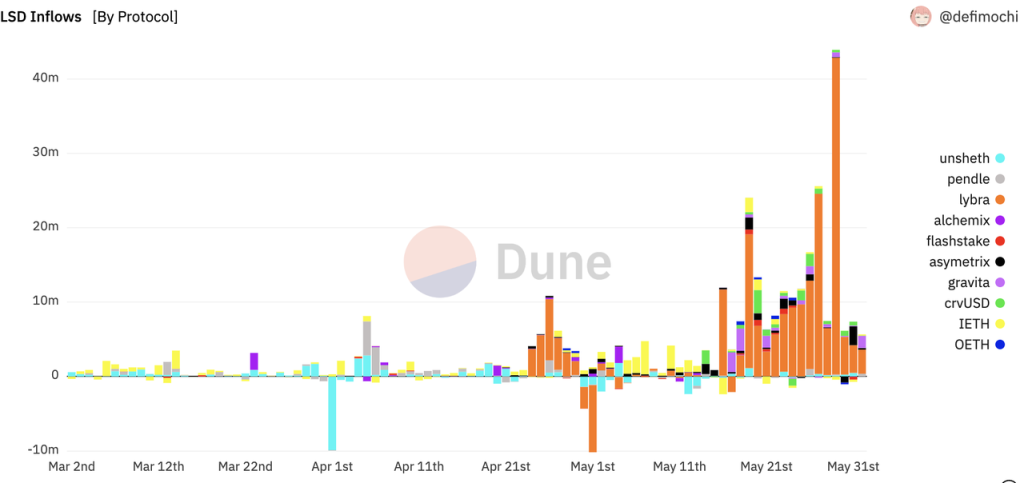

After the Shapella upgrade, many LSDfi projects have emerged in the market, characterized by attracting users' LSD deposits for various financial applications. Many believe we are about to experience an LSDfi summer.

Source: https://dune.com/defimochi/lsdfi-summer

In this article, we will not discuss the pros and cons of specific LSDfi projects, as I believe LSDfi has not created a new business category but merely allows LSD to serve as collateral for many businesses. Essentially, the services provided by these protocols still revolve around stablecoins, yield aggregation, DEX, and interest rate services. The success of their businesses will still depend on their understanding of the stablecoin, yield aggregation, DEX, and interest rate service markets. Among the LSDfi projects that have already launched products, we have not yet seen any that can break free from forking and simple yield farming games. Of course, there are still many high-quality LSDfi projects that have not yet launched, and we look forward to more innovations based on LSD in the future.

What we want to discuss is the impact of LSDfi on the entire staking industry.

Holders of LSD must possess two characteristics: they hold ETH on-chain and have some understanding of DeFi; they are sensitive to yields (which is why they stake). These two characteristics make them target users for any DeFi entrepreneur on the Ethereum network: they hold ETH on-chain, so they can perform on-chain operations and may understand their business; they are yield-sensitive, so incentives can influence their behavior. In fact, even at this relatively mature stage of DeFi development, many ETH holders still only hold ETH on centralized exchanges.

Source: https://etherscan.io/accounts

Based on this wave of LSDfi enthusiasm, more and more LSD projects will begin to launch, each with new tokens, which means they will have new market budgets. What happened with unshETH, Agility, and Lybra may be repeated in the next 3-6 months in the LSDfi space. LSD will continue to offer APRs far exceeding the on-chain yields of ETH, potentially creating a self-reinforcing flywheel effect between LSD and LSDfi: the more LSDfi there is, the higher the yields offered, and the more motivated ETH holders will be to convert their ETH into LSD; the more LSD there is, the more DeFi protocols will target these users, attracting them with high yields to help the protocols through their cold start phases.

Ultimately, all DeFi protocols may be broadly referred to as LSDfi, as they all support LSDfi to some extent (in fact, currently, apart from a few stablecoin protocols, the vast majority of DeFi protocols are already associated with LSD). Clearly, LSD can capture the beta of LSDfi. The popularity of LSDfi will further promote the share of liquid staking in the overall staking arena.

The Ethereum Foundation's Attitude

Regarding issues related to staking, the Ethereum Foundation has expressed the following attitudes:

- They do not wish to see too much ETH entering staking, as an excessive amount of ETH in staking would increase the release of consensus layer ETH rewards, contradicting Ethereum's long-standing principle of "minimizing the feasible issuance amount." Additionally, it would reduce Ethereum's economic bandwidth (economic bandwidth, a concept proposed by Bankless, refers to the liquid market capitalization of Layer 1, which underpins the operation of all DApps).

- They have a negative view of MEV. For every Ethereum staker, MEV is a potentially massive reward that can drop from the sky at low probabilities. Without intervention, it can easily lead to forced centralization (as seen in BTC and ETH in PoW mining pools), establishing new alliances on top of Ethereum's consensus (such as the current MEV-boost), resulting in unnecessary and potentially unsafe complexities at the consensus layer. In the medium to long term, the Ethereum Foundation will promote the burning of MEV, transforming it from a privilege of a few validators into a shared reward for all ETH holders.

- They do not want to see an overly powerful LSD that could "replace" ETH on the Ethereum mainnet. This would also bring more unnecessary security risks to ETH.

The underlying theme of Ethereum's thinking is to maintain a decentralized consensus layer while preserving ETH's characteristics as the primary collateral asset of the Ethereum network, and to prevent the consensus layer from being influenced by protocols built on Ethereum.

Source: https://ultrasound.money/

stETH is currently the largest non-native, non-stablecoin asset on the Ethereum network. USDT and USDC, which rank higher than stETH, have very broad use cases, but they fundamentally rely on the credit of Tether and Circle. If they encounter issues, it could significantly impact Ethereum, but it would not consume Ethereum's credit.

However, the uniqueness of stETH lies in its near-universal integration as collateral similar to ETH across all DeFi protocols. Let’s consider a thought experiment: if the Lido Finance contract were attacked and all withdrawal private keys for Lido on the Beacon Chain were controlled by hackers, would Ethereum need to undergo a hard fork like the DAO incident?

No one wants to see that, which helps us understand why the Ethereum Foundation needs to support solo staking vigorously, why the Ethereum community discusses whether to limit Lido's scale, and why Lido has made decentralization its primary task going forward. But the issue is that the emergence of a large liquid staking service provider is not a deliberate act of an evil centralized organization, but a natural result of market competition. Even if the Ethereum Foundation/core community could control Lido's scale in some way, Mido or Nido would emerge as the new focal point for staking.

We face two worlds:

- One is what the Ethereum Foundation initially hoped to see: a low proportion of ETH staked, sufficient to maintain security, with most ETH still serving as collateral on the mainnet to support various DApps, and the main stakers being solo stakers.

- The other is what we are likely to see in reality: due to the presence of one (or several) powerful LSDs, more ETH has entered liquid staking, and this (or these) LSDs have become collateral for various DApps, to a large extent, this (or these) LSDs "have become" ETH.

Currently, the probability of the latter scenario occurring is much higher.

Risk warning

Risk warning Risk warning

Risk warning