PawnFi: Exploring the Protocol Mechanism and Token Value of the NFT Liquidity Engine

PawnFi is not just built for "NFT lending," but for a larger NFT financial ecosystem.

PawnFi is not just built for "NFT lending," but for a larger NFT financial ecosystem.Author: PawnFi

Growth of the NFT Financial Sector

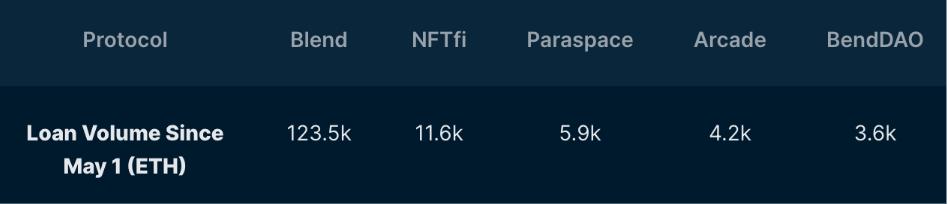

According to previous data from Nansen, after Blur launched the NFT perpetual lending protocol Blend, the protocol has facilitated over 15,800 loans for 1.2 million independent borrowers and 1.6 million lenders, totaling 123,500 ETH (approximately $224.4 million).

Shortly after, Binance also announced the launch of NFT lending services, indicating that there is still demand and market potential for NFTs in the financial sector.

At the same time, PawnFi, an NFT financial project backed by top institutions such as DCG and Coinbase Ventures, has recently seized the market opportunity to launch an Early Access event. However, unlike Blend and Binance, PawnFi is not just building "NFT lending," but a larger NFT financial ecosystem.

To fully understand PawnFi, we must start with the core mechanism of the entire protocol: "P-Token."

P-Token Releases NFT Liquidity

P-Token is a new mechanism in the NFT space that can "standardize and split" NFTs, converting non-fungible tokens (non-standard assets) into ERC20 tokens (standard assets), thereby providing liquidity to NFTs while addressing their functional issues in financial applications.

Replacement Process

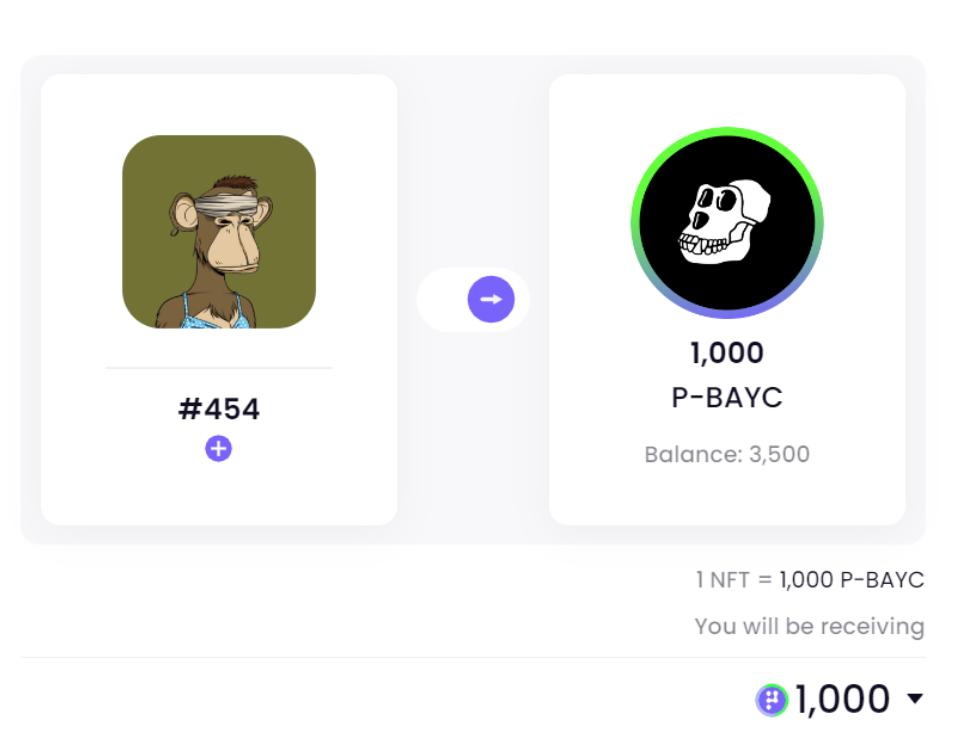

NFT holders can use Flashtrade to exchange an NFT (e.g., BAYC) for 1,000 P-Tokens (P-BAYC) representing ownership of the BAYC NFT. The following is a schematic diagram:

It is important to emphasize that for the protocol, NFTs do not have value differences based on rarity; therefore, all NFT exchanges are fixed at 1,000. For example: any BAYC = 1,000 P-BAYC, any MAYC = 1,000 P-MAYC, any Azuki = 1,000 P-AZUKI, and so on.

How to Exchange Back to NFT?

When it comes to exchanging P-Tokens back to NFTs, most people might think of the term "redemption," but this is actually incorrect because NFT holders are not collateralizing NFTs to borrow P-Tokens; instead, they are exchanging NFTs for P-Tokens.

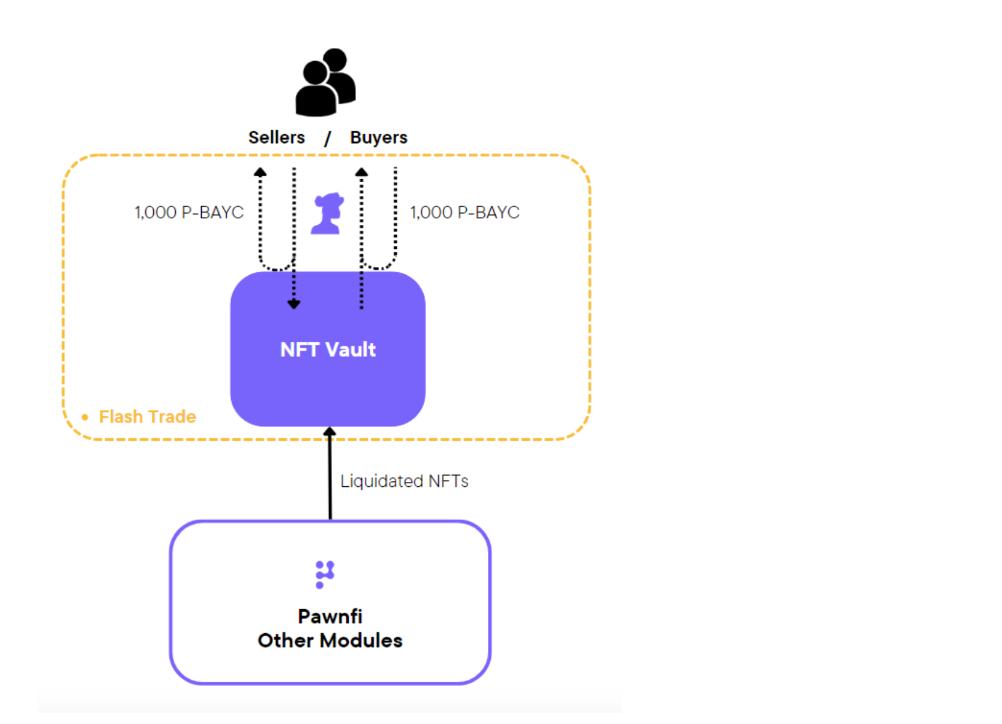

After executing the exchange steps, it is equivalent to relinquishing ownership of the original NFT, and the NFT will be held in the protocol's treasury. When users want to exchange back for the NFT, they can execute one of the following two options through Flashtrade:

- Random Exchange: Pay 1,005 P-BAYC (0.5% fee) to randomly exchange for a BAYC.

- Specified Exchange: Pay 1,015 P-BAYC (0.5% fee + 1% specification fee) to specify an exchange for a BAYC (if the original NFT is still in the protocol's treasury, it can be retrieved).

It is important to note that exchanging NFTs is not an exclusive right of P-Token creators; anyone holding sufficient P-Tokens can exchange NFTs. This helps to promote market arbitrage and maintain the fair value of P-Tokens.

Where Does P-Token Value Come From?

P-Tokens are essentially ERC20 tokens, which means P-Tokens can be traded on any AMM protocol, with the official liquidity pool created on Uniswap (e.g., P-Token/ETH), available for P-Token holders to redeem value at any time (anyone can provide liquidity to earn trading fees and additional mining rewards). Since P-Tokens are exchanged for NFTs at a fixed ratio, when P-Tokens deviate from their intrinsic value, market arbitrageurs will intervene to pull the market price of P-Tokens back to their intrinsic value.

For example: if the floor price of BAYC is 46 ETH, the intrinsic value of 1,005 P-BAYC is equivalent to 46 ETH. When P-Tokens are below their intrinsic value, arbitrageurs will buy P-Tokens, exchange them back for BAYC, and sell them, earning the price difference while pulling the market price of P-Tokens back, and vice versa.

Achieving Comprehensive Financial Applications for NFTs with P-Tokens

Once the liquidity of P-Tokens is established, it essentially means that the financial capabilities of NFTs have been fully released. Currently, existing DeFi applications can be applied to NFTs. The financial applications planned by PawnFi include: NFT leverage, NFT full-collateral lending, NFT consignment, and more.

NFT Leverage

Although Flashtrade has released liquidity for NFTs and allowed for diverse financial applications, it is undeniable that some NFT holders may be unwilling to risk losing their NFTs to obtain liquidity. For this type of user, "NFT leverage" would be a better choice.

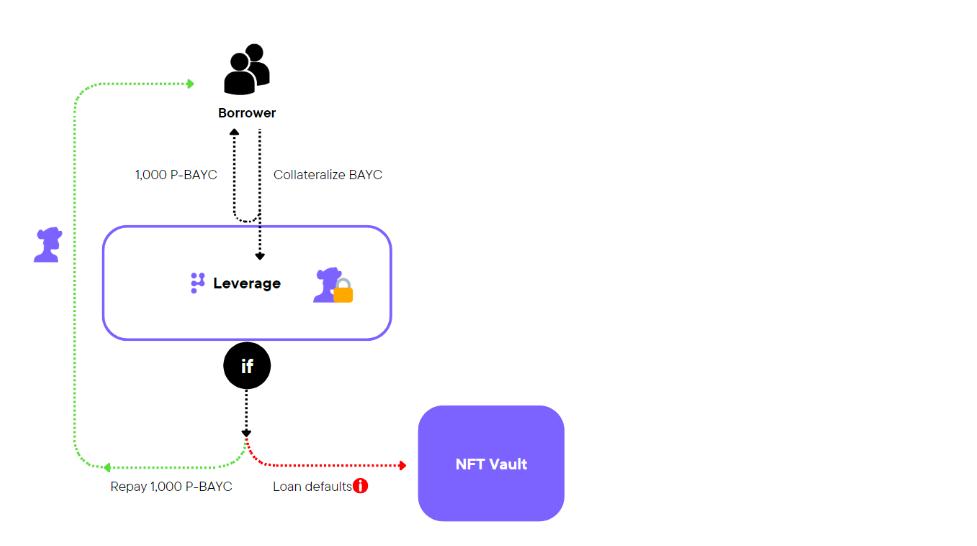

PawnFi's NFT leverage is a "peer-to-peer" lending model structure, but the counterparty of the lender is not the user but the protocol itself.

Specifically, NFT holders can use their NFTs as collateral to borrow corresponding P-Tokens from the protocol. The loan-to-value (LTV) ratio is close to 100%, but the actual amount of P-Tokens that can be borrowed still depends on the "leverage days (N)" and the "protocol margin rate" (according to official documentation, the initial margin rate is 10%), calculated as: "1,000 x (1 - 10% x N / 365)." The borrower only needs to repay the loan within the term to redeem the original NFT. For example:

If a BAYC holder wants to borrow P-BAYC for 30 days, the amount borrowed would be:

1,000 x (1 - 10% x 30 / 365), which is 991.78 P-BAYC.

When repaying, they must repay the borrowed amount plus additional interest (interest is calculated based on the actual borrowing days). According to official documentation, the annualized interest rate for leverage is 10%. For example:

If a BAYC holder repays P-BAYC on the 20th day, the amount to be repaid would be:

991.78 + 1,000 x (10% x 20 / 365), which is 997.259 P-BAYC.

Additionally, the biggest advantage of PawnFi's NFT leverage is that it significantly reduces the risk of collateral and borrowed assets. Since the leveraged assets are P-Tokens, regardless of how the price of the collateral (NFT) fluctuates, the lender will not face liquidation risk. However, if the borrower does not repay the loan within the term, the NFT collateral will still be liquidated and moved to the exchange pool for others to exchange.

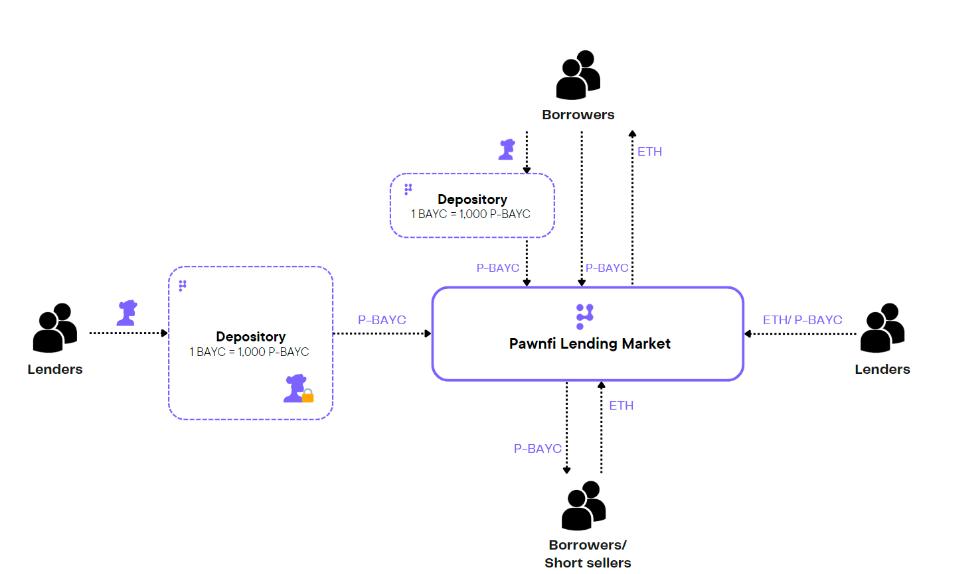

NFT Lending

PawnFi's NFT lending follows a "pool-to-pool" lending model structure, similar to DeFi protocols like Compound and Aave, allowing all users to deposit tokens for lending or use a basket of deposited assets as collateral for borrowing. This approach ensures that even in volatile markets, it is not easy to reach the liquidation line.

However, unlike traditional DeFi protocols, PawnFi's NFT lending protocol allows for the use of ERC20 tokens for lending or borrowing, as well as the simultaneous use of NFTs as collateral, making it more versatile compared to traditional DeFi lending protocols and typical NFT lending protocols.

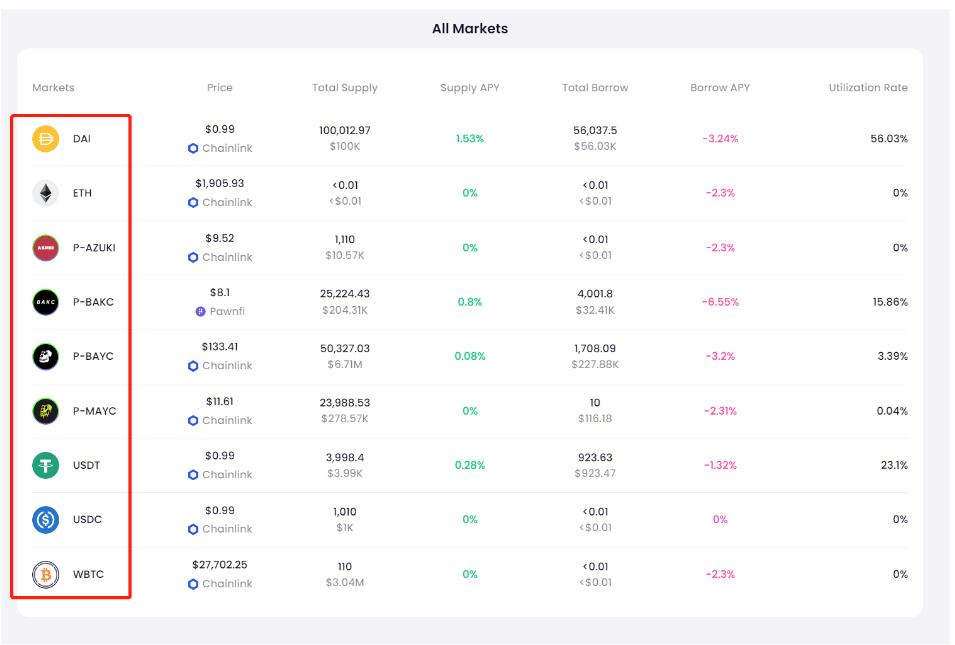

In the early stages of protocol deployment, the number of supported tokens by PawnFi is limited. Currently, the supported P-Tokens can be referenced in this document, and the supported lending can be checked here, but over time, the number of supported tokens and NFTs will continue to increase.

It is worth mentioning that in PawnFi's NFT lending protocol, using NFTs as collateral is equivalent to depositing 1,000 P-Tokens in the protocol. In other words, the collateral itself can provide additional interest income to the holder (in the form of P-Tokens).

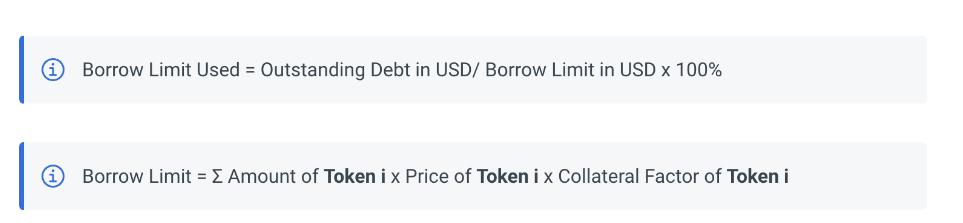

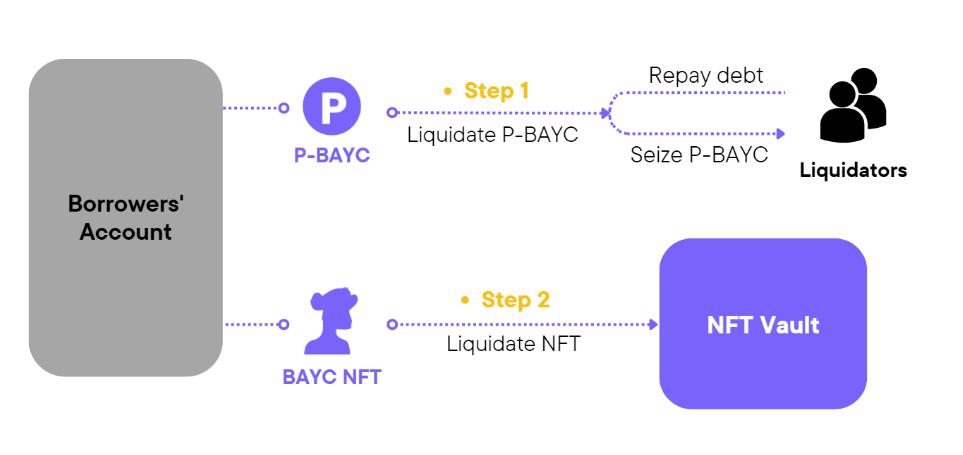

Regarding the liquidation mechanism, when the used lending limit exceeds 100%, liquidation will be triggered, and the actual calculation formula is as follows.

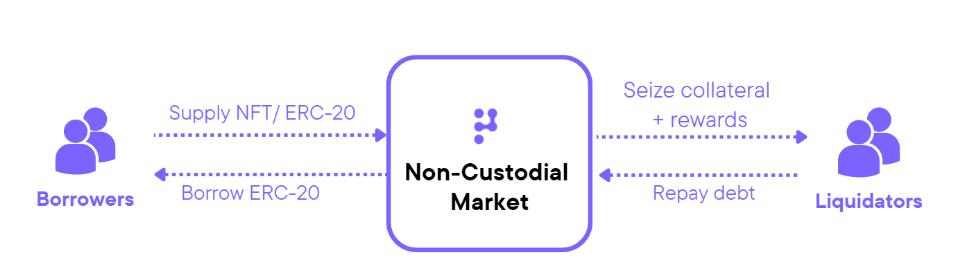

Similar to many traditional lending protocols, the liquidation work is handled by liquidators. When liquidation is triggered, anyone can act as a liquidator, assisting in repaying the debt and receiving collateral slightly above the debt value as a reward. During this process, the protocol will charge a 2.8% penalty on the collateral value as a liquidation fee, which will be deposited into the protocol's treasury.

Additionally, to avoid the full liquidation of the lender's position, the team has limited the amount that can be liquidated in a single transaction to 50% of the debt.

When a user's collateral is an NFT, the NFT is actually deposited in the form of P-Tokens (without affecting the user's NFT). For example, when using a BAYC as collateral, the BAYC will be held in the contract, while the protocol will simultaneously help the user deposit 1,000 P-BAYC into the pool.

When liquidation occurs, the protocol will liquidate part of the P-Tokens to repay the debt. As long as the user's remaining P-Token position is above a certain threshold, the user can always replenish the corresponding P-Tokens and retrieve their original NFT. This design is intended to prevent users from immediately losing their NFT collateral during liquidation, providing a higher level of protection for NFTs compared to other NFT lending protocols.

For example, when a user uses a BAYC as collateral, it is equivalent to depositing 1,000 P-BAYC. When liquidation occurs, as long as the user's remaining position after liquidation is > 300 P-BAYC, they can always replenish 700 P-BAYC and redeem their original BAYC. However, if the user does not replenish and a second liquidation occurs, the deposited BAYC will be forcibly liquidated and transferred to the exchange pool for others to exchange.

Additionally, to avoid malicious manipulation of P-Tokens due to insufficient liquidity at the initial launch of NFT lending, all price data involving P-Tokens will primarily rely on decentralized oracle Chainlink to fetch floor price data for NFTs from platforms like OpenSea and Looksrare. However, over time, the weight of the TWAP oracle price feed for P-Tokens on Uniswap will increase.

NFT Consignment

General NFT sellers can only release corresponding liquidity after the NFT is sold. To meet the needs of some sellers who are eager to obtain liquidity, PawnFi combines "lending" and "listing" to introduce a new application called "NFT Consignment."

Specifically, when users consign NFTs on PawnFi, they can receive an advance payment from the protocol in the form of P-Tokens. The calculation formula for the advance payment is: 1,000 x (1 - 10% custody fee x consignment days / 365). For example, when a user wants to consign a BAYC for 2,000 P-BAYC over 30 days, they will receive an advance payment of 1,000 x (1 - 10% x 30 / 365), which is 991.78 P-BAYC.

After successfully listing for consignment, three possible scenarios may occur:

- Successfully Sold

Assuming the user's BAYC is bought on the 20th day for 2,000 P-BAYC, the platform will charge a 1% fee from the price difference and send the remaining funds after deducting the advance payment and unused custody fees to the user. Therefore, the actual P-BAYC received by the user = 2,000 - 1% fee - 20 days of custody fee, which is 1,984.52 P-BAYC.

- Change of Mind Not to Sell

If the user changes their mind after N days and decides not to sell, they must repay the advance payment plus N days of custody fees to redeem the NFT.

- Expired Unsold

If the NFT is not sold by the expiration date, the user must repay 1,000 P-BAYC to redeem the NFT; otherwise, the NFT will directly flow into the exchange pool for others to exchange.

PawnFi Token

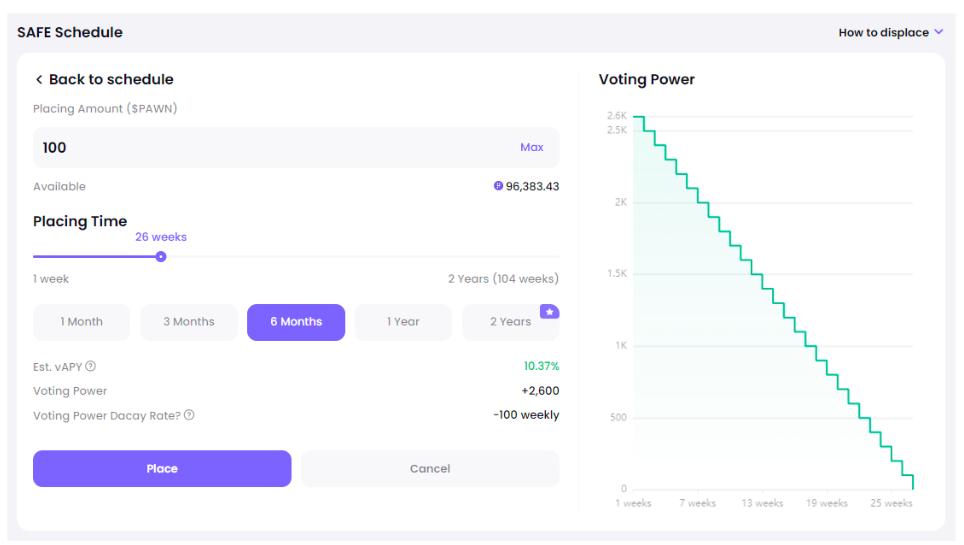

According to official documentation, PawnFi will soon issue a governance token, PAWN, which has governance functions for the protocol. The governance module design references the typical ve (Vote escrow) model, where holders need to lock PAWN tokens in the SAFE contract and receive corresponding governance rights based on the chosen lock-up period.

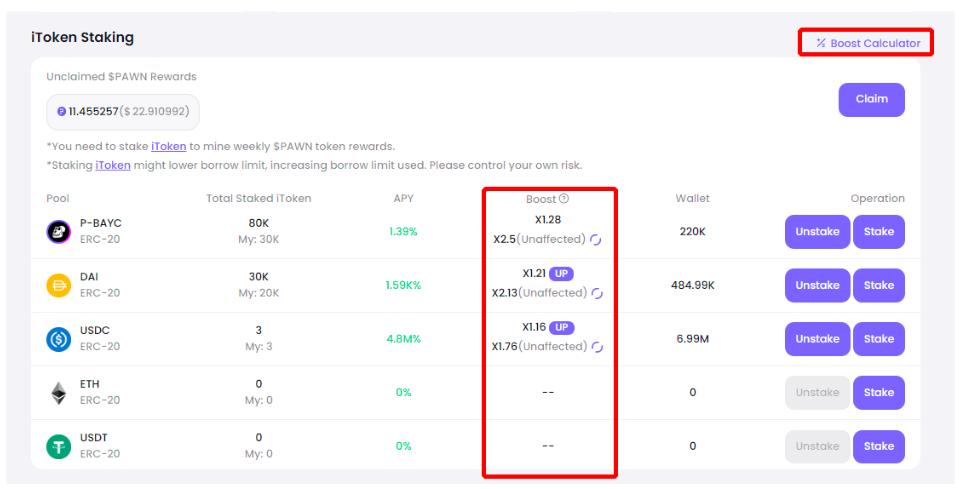

At the same time, users can earn PAWN tokens through liquidity mining rewards by providing liquidity for P-Tokens or in the NFT lending pool.

Combining governance and liquidity mining incentives, the PAWN token can derive diverse value capture capabilities, including:

Enhancing Personal Mining Returns

When users lock PAWN in the SAFE contract to participate in governance, they can simultaneously boost their liquidity mining rewards. Depending on the locked share and chosen lock-up period, the boost can be up to 2.5 times.

Sharing Protocol Revenue

PawnFi's lending module will distribute 50% of the platform's fee revenue weekly to users who lock PAWN in the SAFE contract proportionally. These revenues come in various forms, including ETH, USDT, DAI, and P-Tokens, providing additional incentives for governance participants.

Initiating "PawnFi War"

Similar to DeFi protocols like Curve Finance, the governance rights of PAWN can determine the distribution of liquidity mining rewards. For example, PawnFi's lending pool supports P-BAYC and P-PUNK, and to enhance their respective earning capabilities, the community will compete by voting for their own pools to maximize earning potential.

For instance, the BAYC community may choose to "use the DAO treasury to buy PAWN tokens to vote for their own pool," "provide APE token rewards for those who vote for themselves," or "offer additional APE token rewards for liquidity providers," bringing the typical "bribery model" from the DeFi ecosystem into the NFT market and enhancing the value of PAWN as a governance token.

Conclusion

Overall, due to the team's background primarily in traditional finance, PawnFi's design covers almost all financial application scenarios related to NFTs, and the scale of the entire ecosystem is quite large, with significant potential for development.

However, there are certainly some aspects of PawnFi's design that are worth noting. For example, P-Tokens are the core of the entire protocol, which means the liquidity of P-Tokens will be key to success or failure. However, the volatility of NFTs themselves does not seem to be as significant as that of tokens, which may result in relatively low fee income for LP pools. Whether the additional liquidity mining rewards can provide sufficient incentives for participants to enter the pool is something to watch.

Nonetheless, if PawnFi can gain the favor of NFT project teams, encouraging them to actively collaborate and provide liquidity for their NFTs in PawnFi's pools, or even join the "PawnFi War" to compete for reward shares, the growth rate of the protocol will exceed expectations.

Currently, PawnFi is conducting an Early Access event, and participants are said to have the opportunity to receive potential token airdrops. Interested individuals can keep an eye on the official website, follow the official Twitter, and join the Discord community for more related information.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles