A Professional Guide to Token Market Making for Web3 Founders

This article outlines whether the project requires market makers, the criteria for selecting market makers, and contract negotiations.

This article outlines whether the project requires market makers, the criteria for selecting market makers, and contract negotiations.Original Title: 《Founder's Field Guide to Token Market Making》

Author: Paperclip Partners

Compiled by: Block unicorn

The opacity and complexity of cryptocurrency market making can be daunting; nevertheless, ensuring liquidity is crucial for the growth and stability of token economies.

This report reveals the current state of cryptocurrency market making and provides founders with practical insights for collaborating with market makers (MMs). Key considerations include assessing whether your project needs market makers, criteria for selecting market makers, and contract negotiations.

Our research insights are supported by real project agreements and experts in quantitative finance and market making.

Introduction to Market Making

Market making involves an institution or trader simultaneously quoting buy (bid) and sell (ask) prices for a security or asset to provide market liquidity. The bid price represents the highest price a buyer is willing to pay for a security, while the ask price represents the lowest price a seller is willing to accept for the same security. The difference between the bid and ask prices is known as the spread, which represents the profit margin for market makers.

Market makers are typically motivated to maintain a narrow spread and provide liquidity to the market, as this attracts more buyers and sellers, leading to increased trading volume. In turn, higher trading volume increases the profits for market makers.

Liquidity refers to the ease with which an asset can be bought or sold without affecting its price. Markets with high liquidity have many buyers and sellers, so there is always someone willing to trade an asset. Conversely, markets with low liquidity have fewer buyers and sellers, which can lead to significant price fluctuations when someone wants to buy or sell a large amount of an asset.

Now that we know what market makers are, where is the problem?

The problem lies in the potential misalignment between the short-term profit motives of market makers and the long-term value creation goals of project teams. Our goal is to help founders form synergistic relationships with market makers and avoid creating transaction structures that allow market makers to profit at the expense of the project's long-term objectives.

Do You Need a Market Maker?

Founders should first consider two questions:

1. Does my project need a market maker at its current stage?

Market makers are typically needed during the early listing stages of a project, such as during the Initial Exchange Offering (IEO) phase, when initial trading volume is close to zero. Established digital assets usually have sufficient market-provided liquidity, making the benefits of market makers less significant.

2. What are the benefits of collaborating with a market maker for my project?

In other words: Does my protocol need liquidity? For a decentralized finance (DeFi) protocol designed for high trading volume, liquidity may be crucial. Conversely, for governance tokens designed for low-speed holding, liquidity may not be as critical.

In the latter case, a simple 50/50 Uniswap pool or other decentralized liquidity pools may suffice. Establishing a liquidity pool can be a straightforward self-service solution and requires less funding than hiring a market maker that charges recurring service fees. Once the protocol reaches a certain level of development (e.g., daily active users in the hundreds of thousands or millions), the project can transition to centralized exchanges like Binance, Huobi, or Crypto.com.

Evaluating the Pros and Cons

When conducting a cost-benefit analysis, founders should consider their specific circumstances, including financial status, project timeline, and token utility:

Advantages

Narrowing the Spread: A narrower bid-ask spread makes trading more attractive and reduces transaction costs for both buyers and sellers. A tight spread ensures minimal fees and slippage, providing a better trading experience.

Liquidity Creates More Liquidity: Initial liquidity fosters more liquidity, attracting more buyers and sellers into the market ("liquidity breeds liquidity"), creating a cycle that further amplifies trading volume and liquidity.

Price Discovery: Liquid markets facilitate accurate price discovery, representing the true value of an asset based on the decisions of numerous market participants.

Price Stability: High liquidity can reduce the volatility of prices due to large orders, enhancing investor confidence. Ideally, users should price tokens based on their intrinsic utility and value rather than purely viewing them as speculative assets (which may happen when prices are highly volatile).

Costs

- Participation Fees: Market makers may require setup fees, recurring fees, or token loans. For example, leading cryptocurrency market maker GSR charges a $100,000 setup fee, a $20,000 monthly fee, plus a $1 million loan in Bitcoin and Ethereum.

(Note from Block unicorn: Setup fees typically refer to the one-time payment required by market makers before they begin providing market-making services after signing a contract with founders or project teams. This may include costs for creating and configuring trading strategies and other preparatory work for market making.

Recurring fees usually refer to the fees that market makers need to pay regularly (e.g., monthly or annually) while providing market-making services for a project. This may include costs for maintaining and managing trading strategies and providing ongoing market-making services. These fees are usually fixed and not related to the actual volume or amount traded by the market maker.)

Imbalanced Trades: Due to their low trading volume (which results in smaller profits for market makers), founders or token issuers often find themselves in a weaker negotiating position. In such cases, market makers can exploit this to impose more skewed trades.

Bad Actors: The lack of regulation in the crypto industry may attract fraudulent market makers engaging in deceptive practices, such as wash trading or abusing token loans. The risks of misconduct or default by market makers should be considered.

Criteria for Choosing a Market Maker for Tokens

Currently, there are over 50 major market makers in the cryptocurrency/web3 space. When selecting a market maker, we recommend considering the following five key criteria:

Fees: Including setup fees, recurring fees, performance-based fees, and the total of options.

Capability (Trading Volume and Spread): The quoted trading volume or spread initially provided by the market maker. Some market makers may only guarantee quotes during certain hours of the day, while others can trade around the clock.

Reputation: Established firms with substantial balance sheets, a good track record (e.g., partnerships with reputable projects, traditional finance experience), and experience in delta-neutral market making.

Accessibility: The criteria set by market makers themselves when selecting trading markets (e.g., market makers with minimum trading volume thresholds for assets).

Relationships: Reliable connections with major exchanges (Binance, Huobi, Crypto.com), which may assist with exchange listings, must be considered cautiously and conservatively.

Contract Terms with Market Makers

The final step is to negotiate and finalize a contract outlining the terms of the market-making agreement, also known as a Liquidity Consulting Agreement (LCA).

By analyzing public and private market-making agreements, we have identified key factors in any project founder's agreement to focus on :

Compensation

We view compensation as any form of financial incentive designed to reward market makers for positive behavior. We have identified three main forms of compensation from various market-making transactions: 1) service fees, 2) options, and 3) performance-based fees tied to key performance indicators (KPIs).

Service Fees

Fixed fees paid to market makers can represent a significant amount of fiat currency for early-stage projects. There are several pricing structures:

Setup Fee: A one-time large payment made to the market maker at the start of the service contract.

Retainer Fee: A fee paid regularly to the market maker (e.g., monthly, bi-weekly, quarterly) — this is usually a specified fixed rate.

Both Setup and Retainer Fees (for retained market-making services).

No Fees: In a bull market, market makers may choose not to charge any form of fees, especially for popular tokens. Supply and demand dynamics determine the overall cost of market making, and the profits from hyped tokens may be sufficient for market makers without further charges.

Founders should be cautious as market makers typically have negotiating advantages due to:

Abundant Market Choices: Market makers can trade across numerous different markets, so losing a project to trade has limited impact on their business.

Limited Profit Margins for Early Projects: For early projects with limited existing trading volume or liquidity in their native tokens, the profit opportunities and potential risks seen by market makers when providing services are quite limited. Market makers utilize high-frequency algorithmic trading to profit, so when trading volume is limited (due to lack of liquidity), this opportunity becomes less attractive for market makers.

Options

Options are common in market maker agreements, providing financial returns based on token price performance. Typically, this grants market makers the option to purchase tokens at a pre-negotiated price after the loan matures.

Thus, market makers are incentivized to keep prices above a specific threshold (the option's strike price), as this allows them to exercise the option to purchase a certain number of tokens at the pre-specified strike price and immediately sell them at a higher current market price, yielding substantial profits.

Market makers leverage options to persuade founders to sign agreements, indicating that using options can align their interests with the success of the token (i.e., the token price increase). This is particularly common in bull markets, where early project tokens have the potential to grow 100 times, prompting market makers to aggressively pursue option trades (and they often succeed).

However, these options become worthless after expiration, making this alignment short-term for market makers.

Using Options as Compensation for Market Makers is Complex and Risky for the Following Reasons:

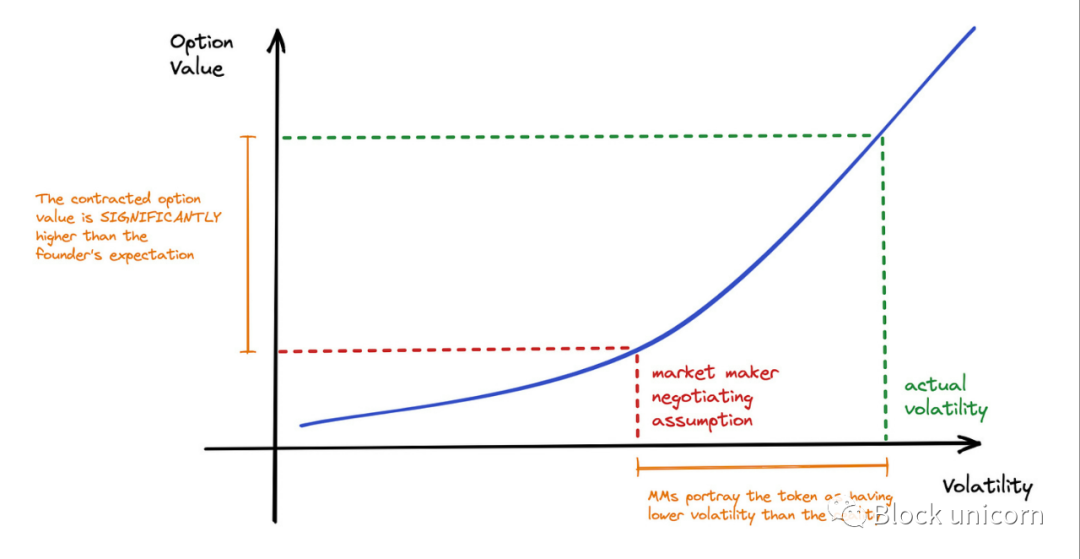

Pricing Challenges: Determining a reasonable strike price, option duration, or volatility for new assets is very difficult and prone to significant inaccuracies. In a bull market, market makers aim to negotiate large option packages at lower prices, seeking returns from token price increases in a manner similar to venture capital.

Manipulation Risks: Founders with limited financial/statistical knowledge may become victims of manipulation of key parameters affecting option value. They may not even realize that the options they provide have additional pricing/implied value — akin to the difficulties in valuing equity in a startup.

------ Unethical market makers can underestimate the actual value of options by using unrealistic assumptions in their calculations, causing founders to inadvertently relinquish more value. This can be achieved by using unreasonable assumptions (e.g., that the token's volatility will equal Bitcoin's volatility), meaning the option's value in the contract is actually significantly lower than reality.

Special Reminder: While token founders do not need to learn complex statistics and option pricing theories, there are tools available for roughly estimating the value of token options in contracts. It is challenging to accurately determine the value of your option trades, but founders should understand the value being offered to engage in more transparent and informed discussions with market makers.

There are tools and methods available for estimating option value, such as calculators or simulators based on option pricing models. Founders can use these tools to generate a rough valuation range to better understand the value of options. However, it is important to note that these valuations are for reference only, and the actual option value may be influenced by various factors, including market conditions, project development status, and the interests of market makers.

Founders should strive to understand the value of option trades and have a more transparent and informed position when discussing with market makers. This can better protect the long-term interests of the project and ensure that transactions with market makers result in relatively fair and profitable agreements.

We have created a basic tool to assist in estimating and valuing option contracts: Paperclip Option Pricing Tool.

There may be risks of price manipulation:

If option prices are too high, this may encourage market makers to drive up prices.

If option prices are too low, market makers (if the loan repayment model is based on token quantity) can maximize profits by shorting tokens, ultimately only needing to repay part of the principal.

One available form of option pricing is to use "tranches," where the token issuer offers several option choices with different strike prices or expiration dates. For example, GenesysGo, which signed a contract with Alameda, provided three tranches priced at $1.88/$1.95/$2.05 for the option strike prices.

Interestingly, tranches have little substantive impact on the actual services provided. Nevertheless, they exist for two reasons: a) market makers want to complicate trades to appear more "legitimate." b) market makers may wish to offer slightly better trading conditions compared to competitors.

Performance-Based Fees

Key performance indicators (KPIs) can be used to create performance-based fees that reward market makers for achieving the project's desired objectives. Below are some performance indicators (along with our assessments of them):

- Trading Volume

Trading volume as a metric carries significant risks, as it may incentivize wash trading. This practice is illegal in most markets and can mislead market data, artificially inflating trading volume figures.

- Price

As a metric, it is not ideal, as it may lead market makers to inflate token prices, which could subsequently pose a risk of collapse to the ecosystem when prices fall.

- Spread

a. The spread or bid-ask spread refers to the difference between the quoted price for selling and the quoted price for buying a stock immediately. In other words, it is the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept.

b. Generally, this is a relatively reliable key performance indicator, although it needs to be supplemented with some metrics capturing market depth (otherwise, a small spread may still be easily swayed by price movements).

- Minimum Buy and Sell Sizes (in USD)

a. Minimum buy and sell sizes refer to the value that market makers are willing to buy and sell in USD (the value of the project token).

b. This is an important key performance indicator that ensures there is a reasonable buffer when large orders cause significant price fluctuations, preventing prices from easily skyrocketing or crashing.

Comparing Different Forms of Compensation

Deciding which form of compensation to choose for a project is ultimately highly personalized and depends on the founder's available funding, goals for decentralization and governance, and the project's stage.

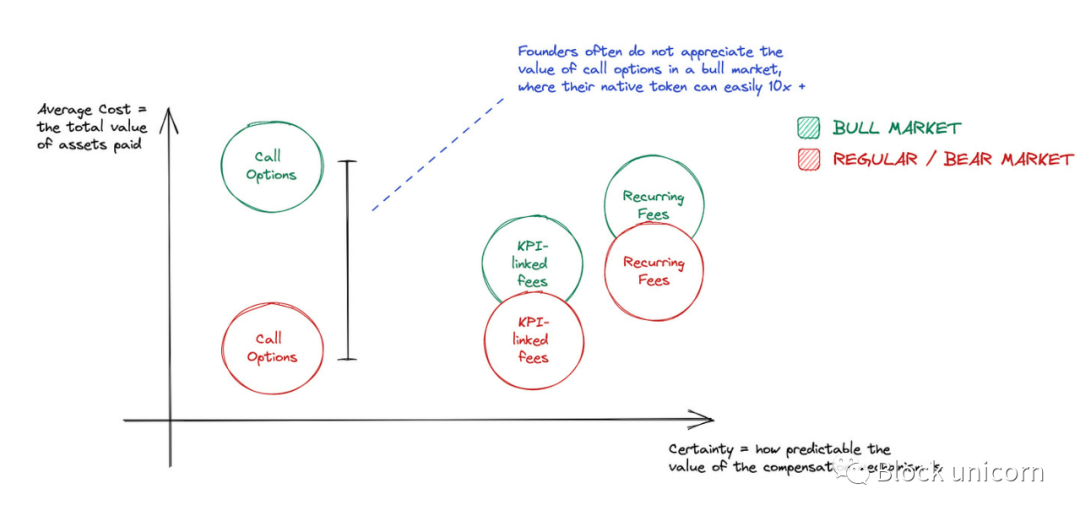

Visualization of Compensation Mechanisms: Measured by "certainty" or "average cost" metrics, fees generally have higher certainty (in USD value) compared to options, but they may significantly increase based on market conditions. However, in a bull market, if the underlying token price skyrockets, subscription options can easily inflate to extremely high values.

Service fees (including setup fees and monthly recurring fees) represent a balanced arrangement but may require high initial costs to increase liquidity support from well-known market makers (MMs) for the project. However, it is not ideal to set vague targets for these fees. Combining performance-based fees with specific targets, such as spread percentage, can better align market makers' behavior with project goals. However, care should be taken during negotiations to avoid using easily manipulable KPIs, such as trading volume.

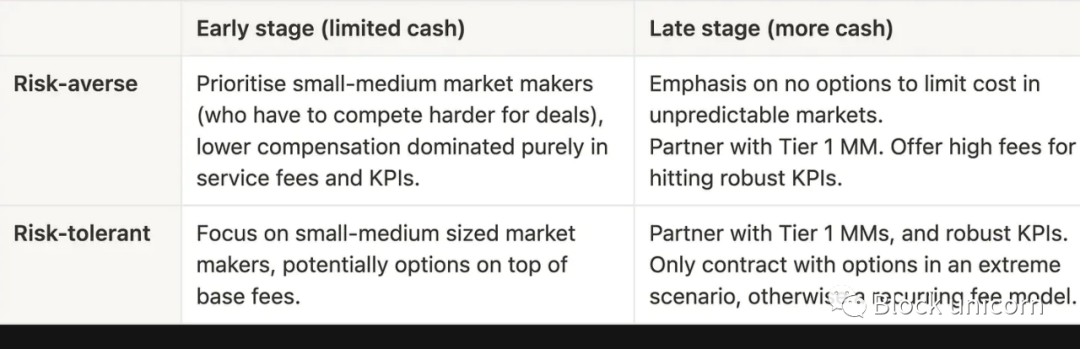

------ We recommend that risk-averse teams combine service fees with KPI-based bonuses. Cash-strapped projects should seek proven trustworthy small to medium-sized market makers, while well-funded projects should contract with large top-tier market makers and negotiate primarily on fixed terms.

Compensation through options may lead to overpayment for market maker services and increase risks. Another negative outcome involves governance: if founders issue a large number of options to market makers at low strike prices, market makers may accumulate a significant amount of circulating supply. This can undermine the decentralization of the protocol, especially since market makers often vote with a profit-maximizing orientation rather than aligning with the project's vision.

------ For teams that are cash-strapped but have a higher risk tolerance, it may be worth considering using a certain number of options in the reward scheme, but attention should be paid to the present value of the options. However, if the project has substantial cash reserves and a loyal user base, using options is generally not recommended, and thorough scenario testing is needed to avoid overpayment.

Here is a summary of the above content:

A framework for understanding the risks of market maker transactions is: as a founder, consider what market makers will gain or lose if the project token price increases 1000 times or drops to zero.

Assuming market makers always act with the goal of maximizing profits and returns, the team should be able to understand the motivations of market makers in driving prices. Ideally, market makers should maintain a neutral stance on price direction, as their goal is merely to provide liquidity.

Loan Terms

In market-making agreements, a common arrangement is for the asset issuer or the party requesting liquidity services to provide loans to market makers for trading and providing liquidity for tokens. Several elements of the loan terms are significant:

Loan Duration: The length of the loan term is important as it determines how long the project must wait before the market maker repays the loan capital. This should be negotiated on a case-by-case basis according to the project's roadmap and the core team's financial needs.

Interest Rate: This token loan is based on a 0% interest rate, as market makers receive variable returns when trading; if they also have to pay fixed interest, it becomes unattractive.

Amount and Value of Token Loans: If the tokens used in the loan are consistent with the ecosystem's native tokens, the incentive alignment will be stronger. However, it is important to note that loans based on token quantity can create adverse incentives for market makers; if token prices decline, they benefit because the value of the repayment amount decreases. This contract term resembles "embedded options," as it provides market makers with significant potential gains from substantial price declines before expiration.

Repayment Issues: The project team should clearly specify the contractual obligations that arise if the market maker fails to repay the tokens; the contract terms typically also include payment of the unpaid amount in BTC/ETH or stablecoins.

Termination Rights

1. Notice Period

Typically, both parties can terminate the agreement with written notice within a specified advance period. As with many commercial agreements, the notice period for termination usually ranges from 14 to 30 days. However, each issuer should assess the ease of obtaining additional market makers based on their individual circumstances and adjust the notice period accordingly. Other conditions under which both parties can terminate the agreement.

2. Asset Issuer

a. Has the right to terminate the agreement in the event of a material breach of its obligations.

- Market Makers: Market makers have more significant termination rights as they determine the conditions under which they will no longer provide liquidity. We outline four possible termination conditions and comment on key considerations for the core team (if applicable).

Breach of Payment Terms: The issuer should ensure that safeguards are in place, including grace periods, to provide the team with buffer time in case of poor financial conditions.

Breach of Other Terms (e.g., confidentiality agreements).

Conflicts with the terms and conditions of exchanges providing liquidity.

Legal Regulations: Due to the constantly changing regulatory environment in the cryptocurrency space, market makers need to protect themselves in case their obligations suddenly become criminal offenses. One source for potential legal due diligence is understanding the laws governing market making in traditional asset markets, which can set precedents for future Web3 regulatory approaches.

Liability

In most liquidity agreements with market makers, market makers are typically exempt from any liability related to token price fluctuations. This is to be expected, as cryptocurrencies are speculative in nature, and it should be noted that there are countless factors beyond the control of market makers that can determine token prices; thus, holding market makers financially accountable for such price fluctuations is fundamentally unreasonable.

Conclusion

In summary, market making plays a crucial role in ensuring liquidity and stability in cryptocurrency markets. This report aims to unveil the complexities of cryptocurrency market making and provide actionable insights for founders considering collaboration with market makers. Through the analysis of real contracts and insights from industry experts, this report emphasizes the necessity of considering market makers, selecting the right firms, and negotiating terms effectively.

We hope this report serves as a valuable resource for founders and other stakeholders in the cryptocurrency ecosystem, helping them make informed decisions in market making and driving the growth and stability of token economies.