Research on the Survival Status of NFT Trading Platforms (1): The Competition Among Leaders in the Era of Post-Royalty Wars

Under the downturn of the overall environment, NFT Marketplace is struggling, and the related trading platform tokens are also in a continuous decline.

Under the downturn of the overall environment, NFT Marketplace is struggling, and the related trading platform tokens are also in a continuous decline.Author: nobody, Wu Shuo

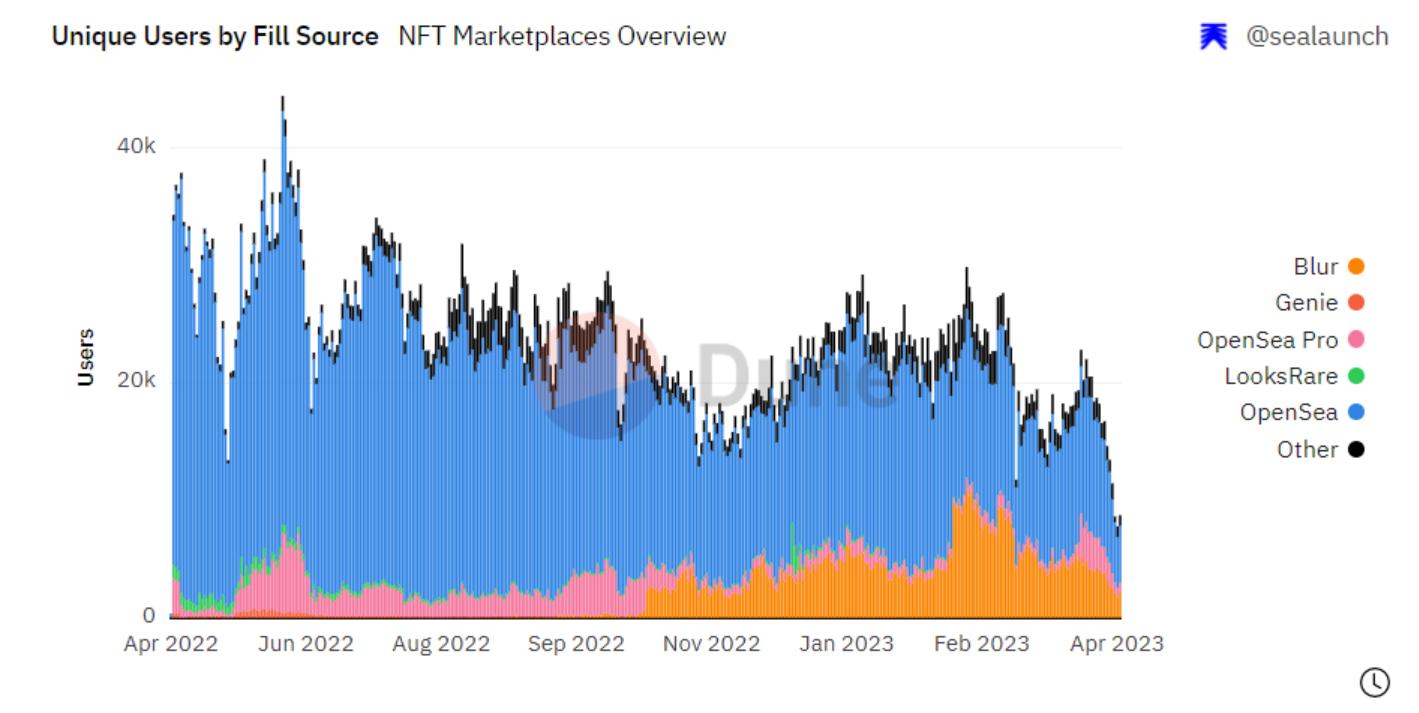

The NFT market continues to languish, with three key indicators—trading volume, number of transactions, and number of trading users—at their lowest levels in over a year. According to @SeaLaunch_ data panel, on April 19, both the number of trading users and transactions in the entire NFT market hit new lows for the past year, indicating a decline in trading interest among both ordinary users and NFT traders. Additionally, blue-chip floor prices for collections like BAYC and Azuki have been on a prolonged decline, with BendDAO blue-chip liquidations occurring almost every few days, and even former NFT whale Franklin has surrendered in this poor market environment. Amidst this overall gloom, NFT marketplaces are struggling, and related trading platform tokens are also in decline. However, as of now, no mainstream platform has declared defeat; most are still developing according to their own strategies, with occasional highlights. This article is the first in a study on the survival status of NFT trading platforms, focusing on Blur and OpenSea in the post-royalty era.

Data source: https://dune.com/sealaunch/NFT?undefined=\&Select+Timeframe_ef4aff=365+days

As the strongest challenger to OpenSea, Blur has had a very clear strategic approach since its inception. As a trading aggregator, it aggregates others but does not allow others to aggregate, trading time for action space. With a points system spanning three airdrop phases, the first phase rewards historical users—capturing competitors' users and leveraging the aggregator's advantages to convert them into its own users; the second phase incentivizes listings—stimulating seller liquidity on its platform, attracting user retention, gaining platform reputation, and standing out in the royalty war; the third phase offers bidding rewards—after achieving good seller liquidity, it stimulates buyer liquidity in return, innovatively launching the Bid Pool, moving from peer-to-peer trading to more efficient pool trading, and continuing to expand brand influence, leading the royalty war. The transition from the second to the third airdrop, from incentivizing sellers to incentivizing buyers, from participating in the war to leading the war, reflects Blur's changing market position at different stages. Of course, an excellent UI/UX and a smooth experience for professional traders are prerequisites and guarantees for Blur's strategic actions. In my view, Blur should have already planned the specific path for the three airdrops since its establishment, with Pro trading being a very prescient strategic point.

Regarding the royalty war, Blur has at least two significant milestone events:

During the second phase of listing incentives, from late October to early November, as a new generation zero-royalty platform, Blur did not fall behind OpenSea in the competition for Art Gobblers, which had potential new blue-chip attributes. From the first day of this NFT's launch, Blur faced off against OpenSea directly and did not fall behind, generating nearly 10,000 ETH in trading volume in the first three hours before launch, with OpenSea accounting for 52% and Blur for 43%. From November 2 onwards, Blur's trading volume for Art Gobblers surpassed OpenSea, and with the support of Art Gobblers, Blur's total trading volume defeated OpenSea for several consecutive days, a sight not seen for a long time. Although Art Gobblers eventually fell, Blur firmly established itself on the historical stage in this small-scale battle, validating the success of its second-phase incentive plan. In November, nearly half of OpenSea's foundational blue-chip liquidity and trading volume was captured by the zero-royalty platform, a significant portion of which flowed into Blur.

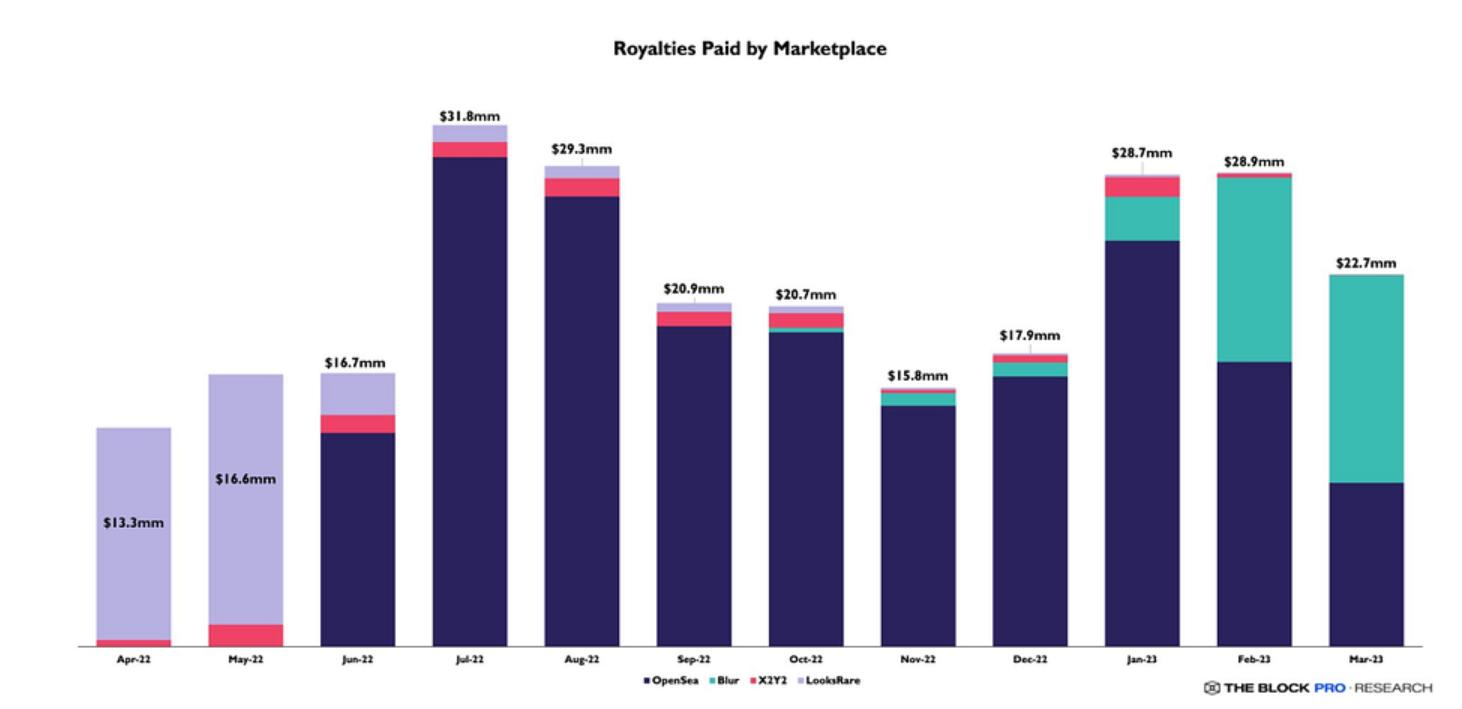

(Continuing to advance bidding rewards around Bid Pool) After the airdrop was released, Blur officially declared war on OpenSea. At that time, Blur had already achieved an outstanding position in the NFT market through bidding blind box airdrop incentives and Bid Pool innovations, and users were no longer surprised that Blur's trading volume exceeded OpenSea's. Users' sentiments were somewhat aligned with Blur at this point. The day after the BLUR airdrop was claimed, Blur published a blog post targeting NFT creators, explaining the differences in royalty payment options between it and OpenSea, and since creators could not earn royalties on both Blur and OpenSea simultaneously, Blur suggested that creators disable OpenSea and would enforce full royalties on any NFT projects not using OpenSea. Initially, it was thought that OpenSea would resist, but within two days, OpenSea announced it would reduce platform fees to 0% and shift to a 0.5% creator revenue model. OpenSea's changes essentially replicated Blur's fee structure, resulting in its complete defeat in the royalty war, with Blur almost declaring itself the victor and king of this battle through a form of dimensionality reduction. The Block Pro data shows that in March, Blur paid creators more in royalties than OpenSea, reaching $12.6 million, a 12.5% increase month-over-month; in contrast, OpenSea's royalties dropped from $17.3 million to $9.9 million, indicating that Blur provided NFT project parties or creators with stronger profitability than OpenSea.

Data source: https://twitter.com/TheBlockPro__/status/1645792435237429250?s=20

Of course, the royalty war has many exciting details, such as Blur using OpenSea's Seaport to bypass its trading blacklist of Yuga series NFTs, and it is not limited to just Blur and OpenSea. To some extent, Blur's ultimate victory can also be attributed to X2Y2. When SudoSwap opened the door to zero royalties, there was hardly any discussion, while later entrant X2Y2 bore much of the NFT community's public opinion fire regarding zero royalties, which ultimately made the burden lighter for Blur, but one cannot help but marvel at the subtle timing of Blur's entry. [Note: For the origin and progress of the royalty war, you can refer to the article I wrote last year: https://mp.weixin.qq.com/s/Ebee0XxplmAXdUZe6nN_JQ]

However, the royalty war is just one process in the development of NFT marketplaces, which may be insignificant in the long historical view, and there may be another royalty war in the future. Does Blur's victory in this royalty war mean it has succeeded? Clearly, the answer is no. In Blur's various incentive plans, since they are all post-event incentives, the general methods for identifying wash trading in transaction mining do not apply to Blur, leading to a mistaken belief that many of Blur's trading activities are organic. This has misled many users and data analysts in the first quarter of this year; in fact, Blur's organic trading volume may be much lower than imagined. The consequences of false prosperity have also been exposed in a worse market environment—due to a lack of actual trading demand and the relatively small market value of NFTs, the Blur Bid Pool has gradually become a powerful tool for large players to manipulate the market, especially as Season 2's double points continue to this day. Large players, in order to gain points and obtain liquidity from a narrow profit margin, rely on stronger financial power than retail investors to set up moving false Bid Walls to toy with retail investors in NFT buying and selling, earning meager profits from it, but due to thin margins and substantial subsidies from future airdrops based on points, large players are happy to do so. The end result is that large players control NFT market prices, leading to falling and volatile floor prices.

Additionally, Blur's roadmap is also worth mentioning. When I first saw Blur's IDEA MAP, it felt reminiscent of BAYC. As we all know, BAYC has excellent storytelling capabilities, and its roadmap is presented in a comic, but it neither shows the starting point nor the endpoint, nor does it indicate where it will go next. The roadmap only tells you the possible destinations; regarding when and how to get there, the official team buries these clues in tweets and videos, guiding the community to speculate and explore in certain directions. Returning to Blur, I also felt that the team behind it was adopting similar behaviors, hoping that Blur will launch more powerful tools in the future.

The above discussion is centered around Blur's perspective; now let's talk about OpenSea. As the market's elder brother, OpenSea had already endured for over two years before the NFT boom in 2021, and even now, it is much better than in 2020 and earlier, so OpenSea should be the most composed in the current poor environment. OpenSea's historical past is likely familiar; the vast majority of users purchased their first NFT on OpenSea, and there is no need to elaborate further. OpenSea's advantages lie in its first-mover advantage, scalable brand effect, and long-tested trustworthiness. Unlike Blur, which has clear short-term motives to defeat OpenSea and capture its users, OpenSea's expansion effect not only brings new user growth but also manifests in its partnerships with the traditional art market/auction houses. Sotheby's and Christie's collaboration with OpenSea has brought digital art into the real world.

Despite bowing its head in the royalty war and losing some market share, OpenSea's strong first-mover advantage has still prevented Blur from making significant inroads, maintaining at least a 2x lead in daily active users. To address the growing professional trading demands of NFT traders and the community's calls for airdrops, OpenSea has upgraded Gem, which it acquired in April last year and had been idle for a long time, into OpenSea Pro. As a professional trading platform, OpenSea Pro largely borrows from Blur's approach, adopting a zero-fee model, acting as a trading aggregator, and featuring an Offer Wall (Bid Wall). Additionally, after the successful brand upgrade, OpenSea Pro also airdropped NFTs for free to Gem's historical users, responding to the long-standing calls for airdrops from the OpenSea community, although this is fundamentally different from the anticipated OpenSea Token.

The launch of OpenSea Pro also provided the OpenSea team with another line of thought. As a potential compliant entity, OpenSea may find it difficult to reach a conclusion between going public and issuing a token in the short term. The launch of OpenSea Pro can significantly shift community attention away from OpenSea Token. Furthermore, the official documentation of OpenSea Pro emphasizes that it will reward the community with more NFTs in the future. A brand new continuous NFT airdrop reward route is indeed a good narrative to divert the community's attention from OpenSea Token. The performance of the first NFT airdrop from OpenSea Pro, the commemorative Gemesis NFT, is also noteworthy, as it could initially be sold for over a hundred dollars, and currently has a floor price of over $60. Moreover, this NFT airdrop, backed by a large brand, provides a new way for project parties to issue NFTs, which can be termed Airdrop as NFT Drop, meaning airdrop issuance. Utilizing this method to issue NFTs rewards historical users; for the platform, it generates trading volume, especially the FOMO trading volume during the initial launch; for project parties, although they give discounts to users during the minting phase, they gain platform support, attention, and traffic, and pay more attention to later community maintenance. Of course, other project parties may not be able to compare with the deep binding relationship between Gem and OpenSea, but this does not prevent it from potentially becoming OpenSea's future issuance strategy for quality new NFTs.

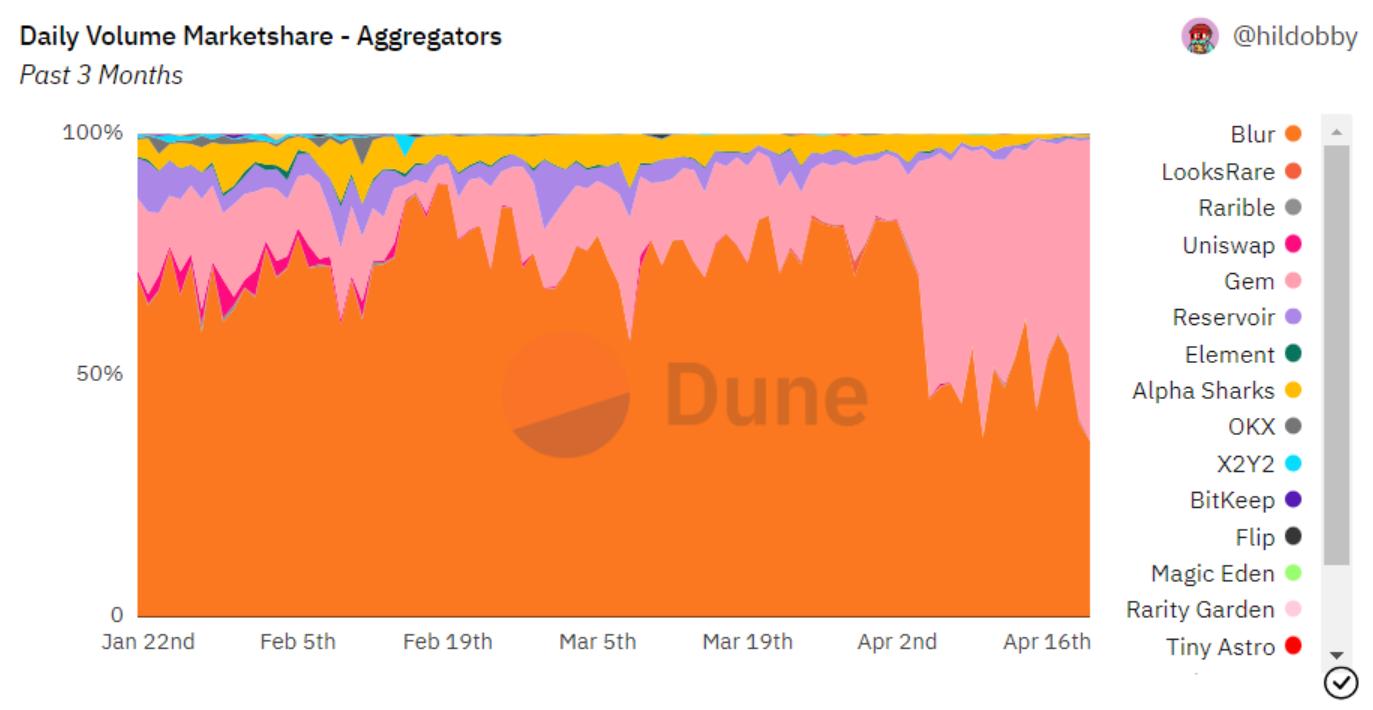

Returning to OpenSea Pro itself, as OpenSea's counterattack, it has also achieved good performance after brand reshaping and has become one of the highlights in the post-royalty era. According to @hildobby_ data panel, since the launch of OpenSea Pro, its aggregated trading volume and users as a trading aggregator have recently been roughly on par with Blur, although OpenSea Pro's aggregated trading volume mainly comes from Blur and OpenSea, and visually, Blur may still occupy a larger share. However, even the unadjusted trading volume of OpenSea + OpenSea Pro has not yet reached 50% of Blur's, indicating that OpenSea Pro still has significant room for growth.

Data source: https://dune.com/hildobby/nft-aggregators

In the post-royalty era, the overall market environment has worsened, and as two leading NFT marketplaces, OpenSea and Blur have both fallen into a phase of developmental bottleneck—OpenSea's daily active users have nearly returned to July 2021 levels, and the Blur Bid Pool has become a tool for large players to manipulate the market, with the delayed halving of rewards being criticized by the community. However, on the other hand, there is also the possibility of mutual learning between the two to survive the winter; OpenSea has borrowed from Blur's professional trading interface to complete the brand upgrade of OpenSea Pro, while Blur has learned from OpenSea regarding its complementarity with the art market, etc.