Analysis of the Landscape of Decentralized Contract Exchanges: dYdX, GMX, Gains, Kwenta, and Level

A comparative analysis will be conducted on the trading volume, transaction fees, and native token valuation of decentralized perpetual contract representative products.

A comparative analysis will be conducted on the trading volume, transaction fees, and native token valuation of decentralized perpetual contract representative products.Author: ThorHartvigsen

Compiled by: Shenchao TechFlow

Since the collapse of FTX, an increasing number of traders have turned to on-chain perpetual DEXs, and their market size continues to expand.

While centralized exchanges like Binance remain the primary venues for derivatives trading, as decentralized technology matures, it is expected that more funds will flow into the decentralized perpetual contract market in the future.

This article will compare and analyze the trading volume, fees, and native token valuations of several representative decentralized perpetual contract exchanges, and discuss the challenges they may face and their future development directions.

Overview of the Decentralized Perpetual Contract Market

In the first quarter of 2023, the total trading volume of on-chain perpetual contract exchanges was $164.2 billion.

Although this represents a significant increase compared to before, Binance alone generated $4.5 trillion in derivatives trading volume in the first quarter.

Since the collapse of FTX, more and more traders have turned on-chain, and several new protocols have emerged. As the market matures, I have no doubt that the cumulative trading volume of on-chain perpetual contracts will grow to trillions of dollars each quarter.

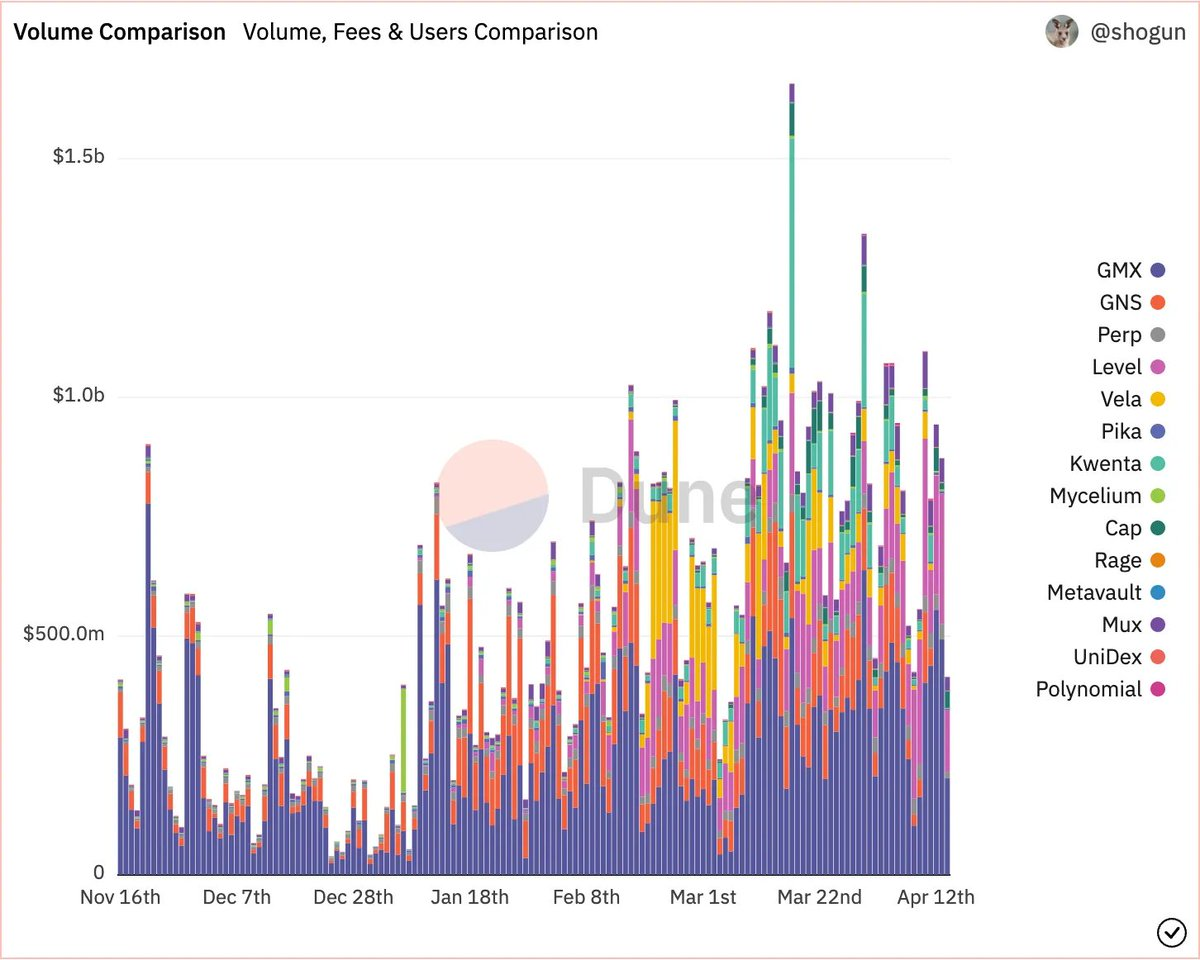

The table below shows the total trading volume and generated fees of leading on-chain perpetual contract exchanges. Two things stand out:

• dYdX continues to attract a large trading volume;

• Despite a significant decrease in trading volume, GMX's fees are almost equivalent to dYdX.

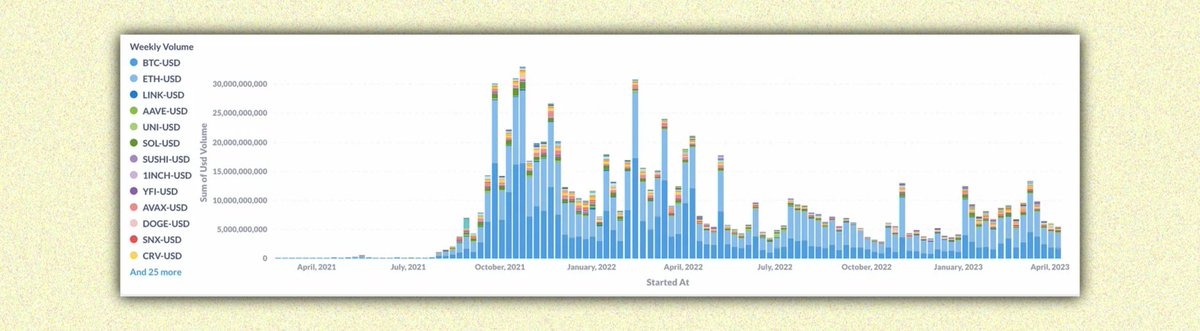

dYdX

Total trading volume: $913 billion;

14-day trading volume: $12.15 billion;

14-day fees: $3.24 million.

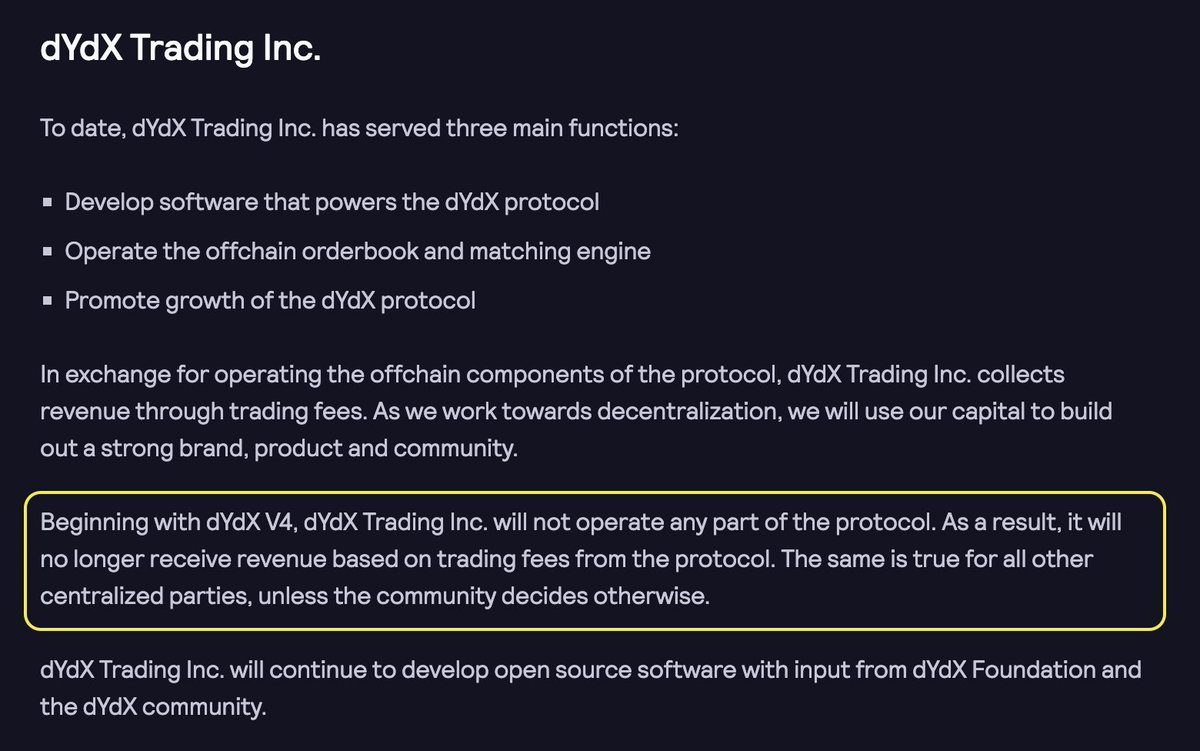

dYdX currently operates on a custom zk-rollup designed by Starkware but will transition to an application chain in the Cosmos ecosystem later this year (dYdX V4).

In V4, dYdX validators will operate a decentralized order book and matching engine on-chain. Current tests have achieved a throughput of over 500 TPS. After launch, all fee income will not be allocated to centralized entities.

GMX

Total trading volume: $100.5 billion;

14-day trading volume: $4.93 billion;

Total fees: $148.2 million;

14-day fees: $7.43 million.

Last year, GMX sparked the narrative of on-chain perpetual contracts. Despite many new entrants in recent months, GMX's daily trading volume, user count, and fees have continued to grow.

GMX V2 will introduce trading features for synthetic assets (not just cryptocurrencies).

• Using Chainlink low-latency oracles for better real-time market data;

• Each trading pair will have separate liquidity to isolate risk;

• Gradual phasing out of GLP tokens after V2.

Expected to launch in the second or third quarter.

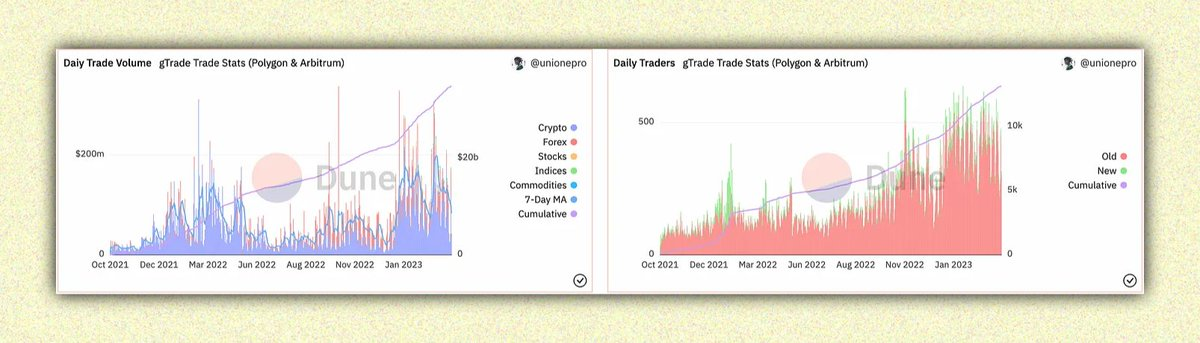

GainsNetwork

Total trading volume: $35 billion;

14-day trading volume: $1.8 billion;

Total fees: $25.4 million;

14-day fees: $1.6 million.

gTrade saw a significant increase in daily trading volume after its deployment on Arbitrum in January.

Currently, about 80% of the total trading volume occurs on Arbitrum. Since the introduction of the gDAI vault, there has also been a substantial influx of liquidity. This vault tokenizes users' liquidity shares in the vault and allows them to deposit into AMMs, lending protocols, etc.

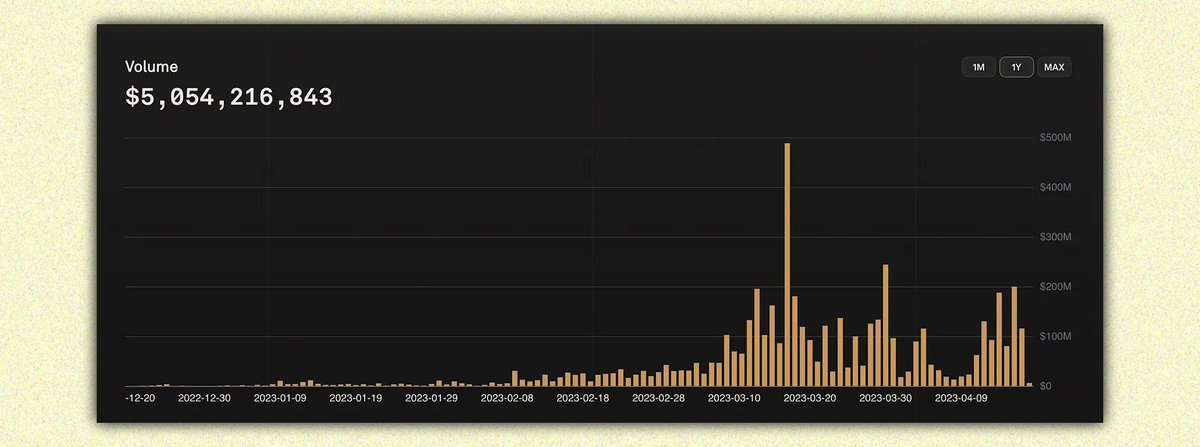

Kwenta

Total trading volume: $6.4 billion;

14-day trading volume: $500 million;

Total fees: $12.6 million;

14-day fees: $800,000.

Kwenta launched its V2 version in February, adding a large number of new tradable assets, and trading volume has significantly increased since then.

Kwenta utilizes Synthetix as the liquidity layer for perpetual derivatives trading. With the launch of Synthetix V3 introducing more collateral assets as backing for sUSD, we may see deeper liquidity on Kwenta.

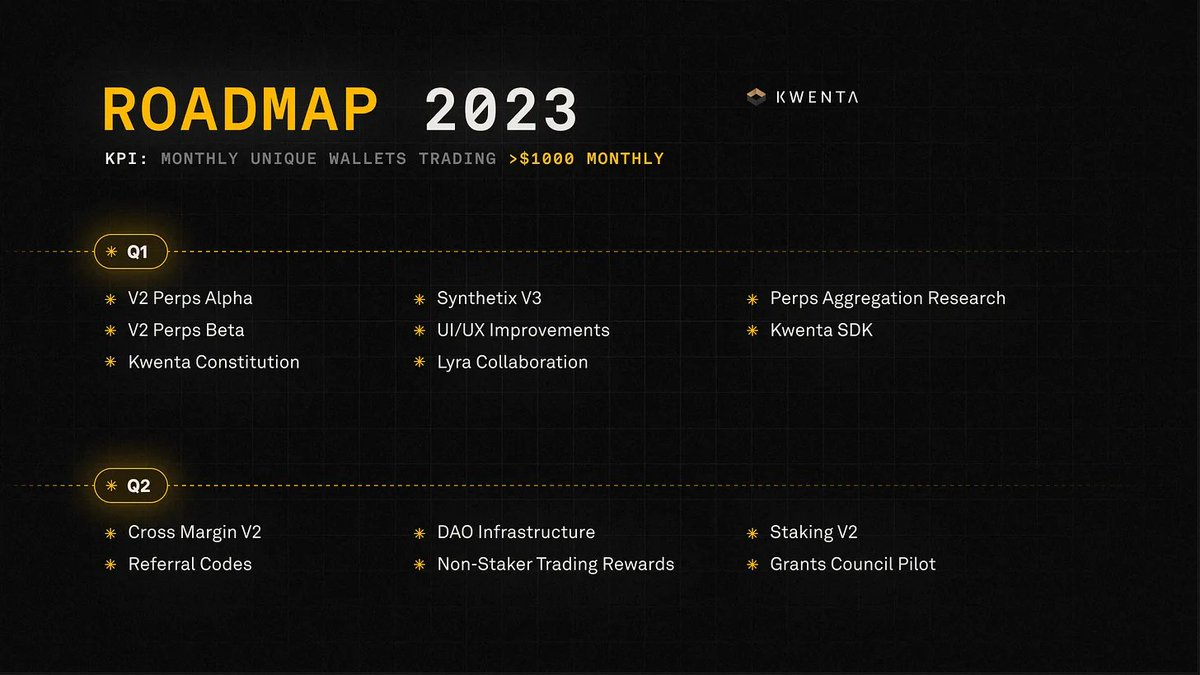

Current Kwenta roadmap:

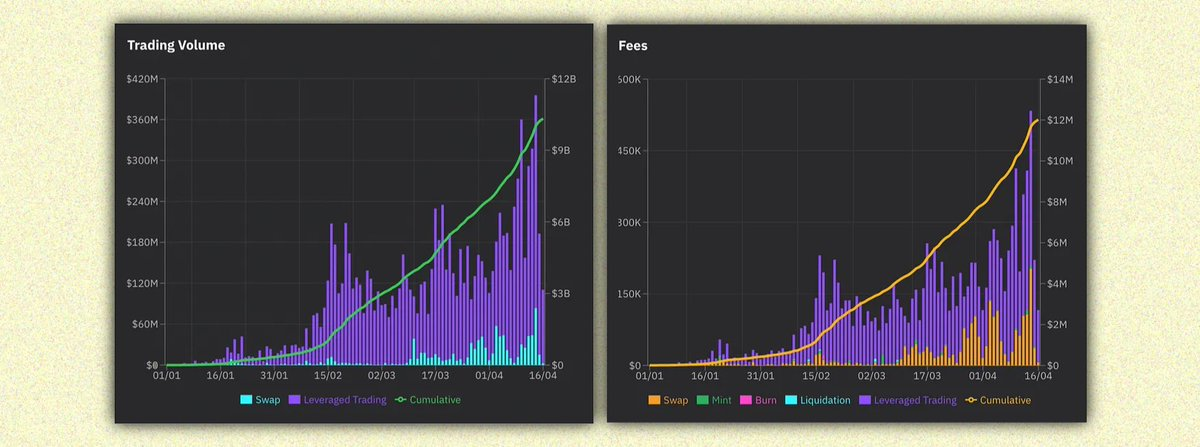

Level

Total trading volume: $10.3 billion;

14-day trading volume: $3.2 billion;

Total fees: $12 million;

14-day fees: $3.9 million.

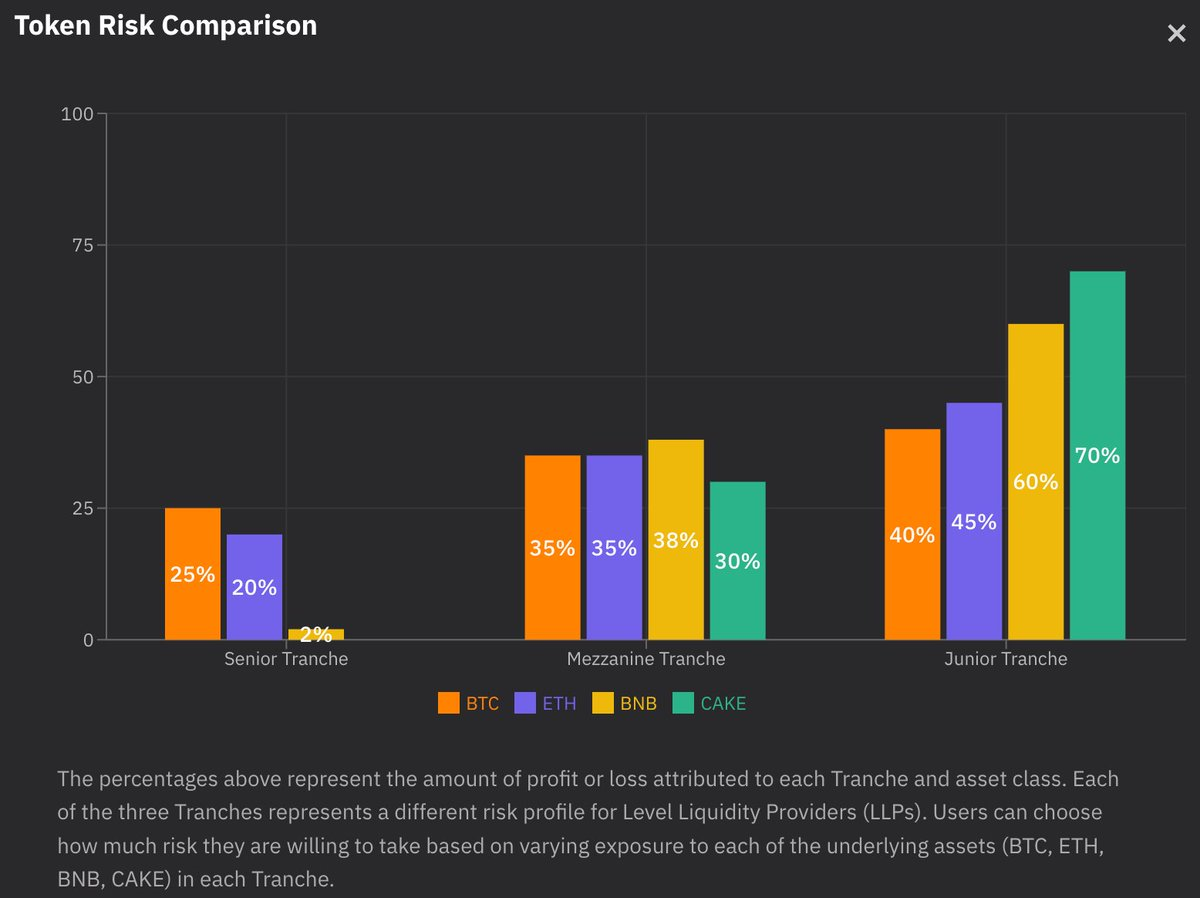

Level is the largest perpetual contract exchange on the BNB chain, offering trading pairs for ETH, BTC, BNB, and CAKE.

Tranches are used to provide liquidity for traders with higher risk appetites, with riskier tranches receiving a larger share of trading fees. Level also plans to expand to new chains and upgrade its current liquidity structure in 2023.

Comparative Analysis

The table below shows recent trading volumes, fees, and native token valuations.

The lower the ratios of FDV/trading volume and FDV/fees, the better the valuation. Note that there is a significant difference in calculating these values based on market capitalization and FDV.

Based on these numbers, GNS and GMX have the best valuations (also because their FDVs are closer to market cap). Based on market cap calculations, DYDX is the best-valued token. However, it is important to note the future token unlock situations.

It is also worth noting that both Kwenta and Level incentivize traders through native token issuance. Will they continue to grow in the face of reduced token issuance?

Personally, I am very focused on $DYDX and $GMX, as they will see catalyst events later this year (such as version updates, new products, etc.).

In summary, I firmly believe that there will be a significant influx of liquidity into the market in the future. If trading volume grows 10-20 times in the future, many of these tokens could see significant increases from their current prices due to this additional growth.