Arkstream Capital: The Cliff Racing between Blur and OpenSea

The traffic jam between Blur and OpenSea is just the first chapter of the infinite war of NFTfi.

The traffic jam between Blur and OpenSea is just the first chapter of the infinite war of NFTfi.Original source: MoKe, “Arkstream Capital: The Cliff Race between Blur and OpenSea”

Current State of the NFT Market

The second half of 2022 marked the winter of NFTs. With the release of Otherdeed for Otherside draining the last bit of liquidity from the market, the NFT market announced the collapse of the speculative boom.

OpenSea monthly trading volume (dune)

As an excellent NFT marketplace, Blur's token issuance expectations brought some incremental value to the market. After Blur issued the $BLUR token, the massive airdrop rewards brought even more increments to the market.

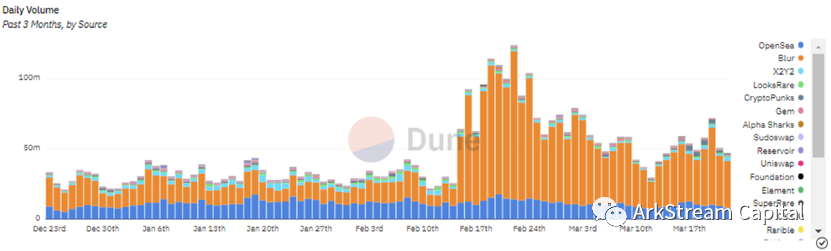

NFT Marketplace daily trading volume (dune)

From the trading data of NFT marketplaces, we can clearly draw several conclusions.

Art-focused NFT marketplaces have fallen significantly behind comprehensive NFT marketplaces (which are essentially PFPs).

Blur's trading volume had already surpassed OpenSea before the airdrop on February 15.

After experiencing the hype and disillusionment of 2022, the NFT market has returned to a healthy state in the first quarter of 2023.

Arkstream has consistently focused on NFTfi, and we believe that NFTs, as certificates of ownership, have long-term value that will not be tarnished by the overall downturn of the NFT market.

Before we officially begin our article, we would like to engage in some casual discussions about the value of NFTs.

Discussion on the Value of NFTs

Consistency and Inconsistency of NFTs

As the name suggests, NFT stands for Non-Fungible Token, referring to non-homogeneous tokens. Compared to the simple consistency of FT (Fungible Token), NFTs encompass both consistency and inconsistency attributes.

Given the current trading activity in the market, NFTs mainly fall into two categories: NFT artworks and NFT PFPs. As humanity becomes increasingly intertwined with the internet, PFPs are more suitable as avatars for online identities. This explains why PFPs are more important than NFT artworks in the NFT space.

NFT artworks possess only inconsistency. In contrast, NFT PFPs are typically composed of series, containing both consistency and inconsistency. NFT PFPs are the Web3 expression of pop art, and the underlying logic is repeated subjects + random variables.

Repetition in industry creates commonality, which fosters community, representing consistency. The scarcity of variables artificially creates inequality, marking social status. For humans, who inherently pursue "inequality," the hierarchy of class disdain is a fundamental need of human nature. The author believes that consistency takes precedence over inconsistency in sequence; only consistency can create a fertile ground for the value of NFT PFPs, allowing the growth of social discrimination value based on inconsistency. The value of PFPs is proportional to community energy.

The blend of consistency and inconsistency in NFTs becomes the biggest challenge that every NFTfi must face. This leads to a split in handling liquidity into P2P (CLOB) and P2Pool (AMM) directions. Each of these two directions excels at addressing one type of contradiction, which becomes an underlying barrier to the development of NFTfi.

NFT Royalties

The frequently debated issue of royalties in the industry becomes clearer when interpreted within the framework of consistency and inconsistency.

NFT artworks carry the artistic value of the artist and their unique expression; they do not require high turnover but rather focus on collectible value. Over the lifecycle of an NFT artwork, it appreciates over time. Van Gogh lived a life of poverty and died unmarried, only to enjoy posthumous fame. High royalties for NFTs can prevent such tragedies from recurring, allowing the time value of NFT artworks to return to artists sooner. Therefore, high royalties align well with the characteristics of NFT artworks.

Initially, NFT PFPs adopted the high royalties of NFT artworks. The author believes that this industry inertia poses significant problems. As previously discussed, since the consistency of PFPs precedes their inconsistency, and the value of PFPs heavily relies on community energy, high liquidity is more beneficial for the value growth of PFPs. PFPs need to capture greater community value through better liquidity and lower friction. The author initially thought that royalties for PFPs would be determined through competition among PFPs. However, it turned out that the liquidity war between Blur and OpenSea inadvertently resolved this issue.

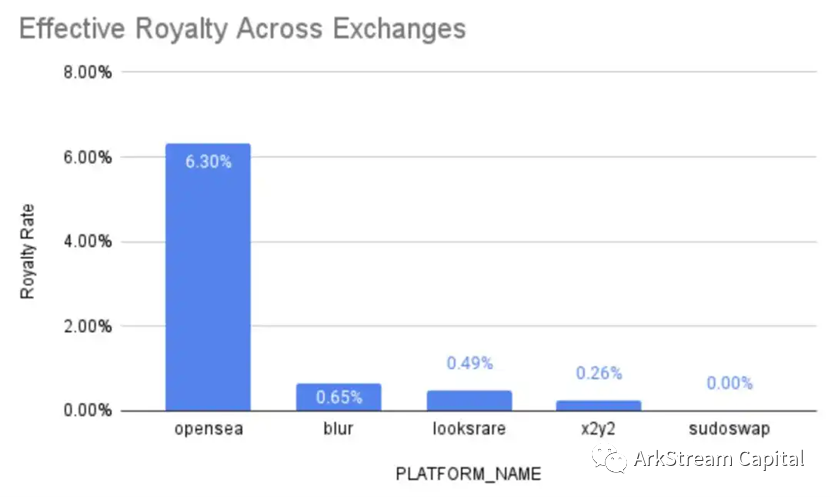

According to data from Proof's research director NFTstatistics.eth, Blur's overall average royalty rate is only 0.65%, which has led to a decline in overall NFT market royalties.

Many NFT project teams have voiced their grievances about this. The author wants to say that these project teams have no right to take the profits from the market's golden period for granted. Taking the project Phantabear, which the author is familiar with, as an example, it has accumulated sales of 35,735 ETH, with a royalty of 7.5%, resulting in total royalty income of 2,680 ETH, equivalent to about $4.5 million at ETH = $1,700. These funds have not been reinvested into the project's development but have been largely divided among the founders. Not to mention the minting fees. Phantabear is just one of many NFT projects that do little.

By: Phantabear is a money-making project created by founders Mark and Will using Jay Chou's fame. Later, Jay Chou, due to personal reputation issues, expressed a willingness to take over Phantabear. However, the two founders have been unable to clarify the division of rights and responsibilities, leading to the project's practical failure.

The fact that NFT projects can only struggle to make money through community management is the greatest respect users can show for a healthy NFT market.

Competitive Landscape of NFT Marketplaces

Strictly speaking, NFT marketplaces can be further divided into three categories: CLOB Marketplace/AMM Protocol/Aggregator.

The earliest players in the Aggregator space were Gem and Genie, both of which were acquired by OpenSea and Uniswap, respectively. Rather than being true aggregators, they served more as batch operation tools for OpenSea.

The Aggregator concept originated with Genie, and Gem entered the market with a more user-friendly and convenient product after Genie opened the market. It also had better customer friendliness and superior promotional and capital support, which allowed Gem to achieve initial success in the NFT aggregation platform competition. However, Gem did not enjoy its success for long; as challengers to OpenSea gradually emerged, a stronger aggregator, Blur, appeared, which seemed more focused on driving traffic to its own marketplace. An aggregator that does not want to be a marketplace is not a good aggregator.

By: X2Y2 also has aggregator functionality, but X2Y2's aggregator is more of a side feature that provides batch trading capabilities for LooksRare and OpenSea.

Currently, strictly speaking, only Reservoir resembles a dedicated aggregator, but under the pressure of the two giants, Blur and OpenSea, it appears relatively lonely. The aggregator space may only find its opportunity when the market is in a more chaotic state.

Trading Experience and Liquidity War

One dimension of competition among NFT marketplaces lies in the convenience of trading. From the trading interface, it is clear that Blur's trading experience caters to professional traders and wholesale markets, while OpenSea's trading experience is geared towards ordinary users and retail markets. Most other marketplaces have designed their interfaces based on OpenSea.

Blur trading interface

OpenSea trading interface

Blur's outstanding trading experience is why it has attracted some early users. It also explains why so many airdrop hunters were willing to invest resources and time in Blur before the token was issued.

However, regarding the discussion of CLOB marketplaces, the author wants to focus this topic on liquidity. As a market, the greatest value lies in providing the best liquidity to users. In DeFi, Uni's early LP design and GMX's zero slippage betting and GLP design on Arbitrum have all made efforts to enhance liquidity.

As the earliest NFT marketplace, OpenSea provided an offer buying function in addition to listing NFT sell orders. However, the convenience and batch processing of the offer buying function are not very good, limiting the liquidity of buy orders. When the author holds a large number of NFTs from a single series, selling them becomes a headache. The author has previously questioned whether OpenSea intentionally did this to maintain the overall price performance of the NFT market. Because a better order book function is theoretically not difficult to implement.

When LooksRare launched, we discussed its token economic model. It initially adopted a trading mining logic. The history of trading mining can be traced back to 2018, and it was only after the DeFi craze that liquidity mining became widely adopted.

In our analysis of the liquidity mining initiated by Compound in 2020, we noted its differences from the Dapp craze of 2019 and earlier trading mining models like Fcoin and DragonEx.

The problem with trading mining is that it can lead to wash trading, resulting in garbage transactions driven by token incentives. These garbage transactions do not generate lasting value and do not contribute to liquidity growth. For players who lack the technical means to mine at low costs and can only engage in market orders to mine, their trades are transient and lack "inertia." When token incentives begin to halve, liquidity will quickly diminish. This indicates high costs and low efficiency of mining subsidies.

In contrast, the advantages of liquidity mining are that first, it provides real liquidity, and LPs bear the risk. Second, it has inertia; the vast majority of LPs do not frequently switch their LPs. In DeFi, we even see some defunct projects with hundreds of thousands of US dollars in farm funds remaining. Additionally, LPs receive trading fee dividends in addition to mining rewards, further increasing their retention.

In Arkstream's thoughts on token economics, we believe that good token economic design must meet the following criteria:

1. Project teams must deeply understand that token incentives are a form of debt and design emissions cautiously.

2. Token incentives must encourage behaviors that positively drive the long-term value of the protocol.

3. Token incentives must be applied to protocols with network effects.

None of these three can be omitted.

The subsequent performance of LooksRare's token price and trading volume proved the failure of trading mining.

Looks token price (Coinmarketcap)

LooksRare trading volume ranking (LooksRare official website)

Afterward, LooksRare added listing rewards. X2Y2, on the other hand, included listing rewards from the very beginning. After updating its token economy to version 2.0 on March 30, 2022, and switching to trading mining, this was actually a regression.

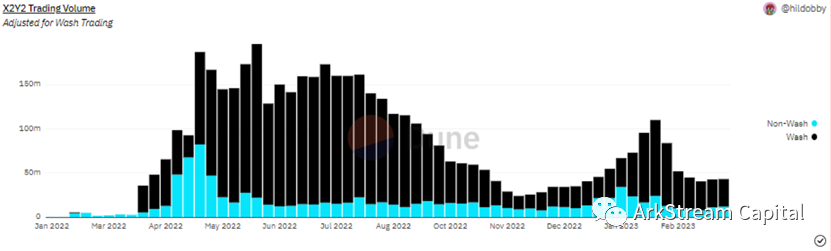

X2Y2 wash trading (dune)

Liquidity is bidirectional, and for the NFT market, the biggest issue is not the lack of sellers listing but rather the insufficient counterparties to absorb the selling pressure when trying to offload NFTs. Therefore, in terms of liquidity, Blur has considered more than LooksRare and X2Y2.

In Airdrop 2, Blur adopted listing mining, and then in Airdrop 3, it introduced BID mining, corresponding to both ends of liquidity.

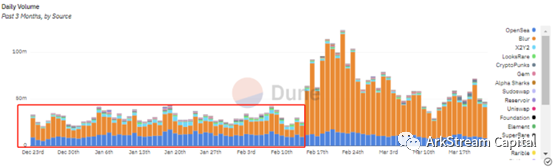

NFT Marketplace daily trading volume (dune)

Before the official issuance of $BLUR, such a bidirectional liquidity scheme had already generated a significant positive stimulus for Blur's trading volume. This is clearly a successful airdrop plan.

This is also why the author has given significant attention to Blur; Blur is the first player in the NFT marketplace to adopt a proactive strategy (including BID product design and token incentives) to address NFT liquidity.

Defects in Blur's Liquidity Scheme

However, the author believes that Blur's liquidity scheme is still not the best solution. Compared to Uniswap's LP liquidity design, Blur's BID appears to lack sufficient inertia.

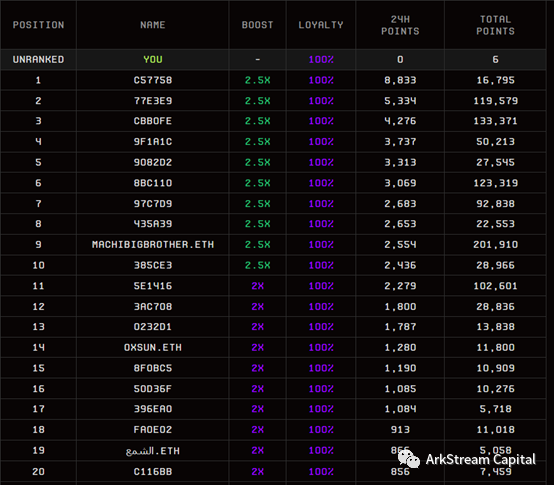

Currently, in the BID rankings, more than half of the top 20 are Chinese individuals with names, including large holders/scientists/studios that the author has heard of several times. The vast majority of funds in the BID are not loyal.

Blur BID points ranking

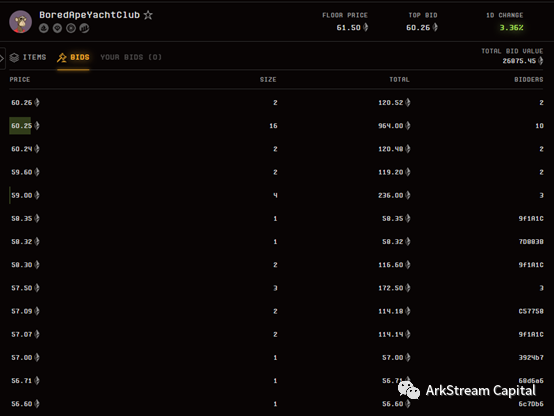

The BID walls for BAYC and MAYC illustrate this point well.

BAYC BID wall

MAYC BID wall

Due to MACHI's substantial holdings in BAYC, many fear MACHI's potential sell-off, leading to a lack of large funds bidding on the 1/2/3 tiers.

In contrast, there is significant funding in the 2/3 tiers for MAYC. These obvious buy walls are primarily for accumulating BID points; aside from these clear buy walls, there are not many genuine liquidity market makers.

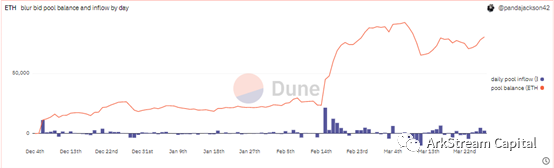

The total amount of ETH in Blur's BID pool saw many withdrawals on the day of the Silicon Valley Bank crisis. On that day, the market plummeted, and NFT prices were also significantly pressured, causing the BID funds for most collections to drop from 30,000 ETH to 10,000 ETH.

Blur BID pool balance (dune)

Moreover, because Blur currently operates on a zero-fee mechanism, aside from the token incentives themselves, it cannot provide incentives to LPs through fees like Uni. A healthy system is one where, even without token incentives, there are still incentives for LP providers to offer liquidity. When $BLUR launched on Uniswap, many players were eager to become LPs to earn trading fees, with some friends recouping 50% of their costs on the first day.

Once Blur's liquidity incentives are removed, it is easy to imagine that these BID walls will collapse immediately.

The Massive Collapse of NFTs Due to Liquidity

When discussing the liquidity mining of Blur and its impact on the NFT market, we also face the issue that Blur has accelerated the collapse of the NFT market. Previously, due to liquidity issues, large holders could not quickly cash out. However, with Blur's BID walls, whales can now offload their assets freely.

Many small NFT projects will use Blur's mechanism for dumping. In the early stages of Blur's imperfect mechanism, these project teams would first inflate trading volume on OpenSea, and once a floor price was established there, they would gradually raise BID orders on Blur to earn points. In this process, some project teams choose to list part of their NFTs, so even if their BID is successful, the sold NFTs can still recoup some funds. Others hold a majority of the NFTs in the collection, allowing them to raise prices freely to accumulate points while not selling to others.

If there are no competitors for BID, project teams may be content with just accumulating Blur points. However, if retail investors or bots also participate in BID, once they accumulate sufficient BID depth, they will quickly withdraw their bids and sell their NFTs to these bidding retail investors and bots.

In this frenzy, NFT project teams and whales gain valuable liquidity, while liquidity market makers obtain "valuable" $BLUR.

Thus, the author believes that Blur's token economy needs an upgrade to increase the costs for these arbitrageurs. Arbitrageurs pose a threat to the system.

Although this liquidity has become a double-edged sword for the NFT market in the short term, in the long run, liquidity remains a positive factor. If we acknowledge the long-term value of NFTs, then the collapse under rich liquidity merely aids in the rapid discovery of prices.

Future Outlook

The author believes that since Blur's current token economic design does not consider the inconsistency of NFTs, it could completely adopt Uni's LP pairing method for mining to enhance the inertia and durability of liquidity market makers.

This essentially represents an AMM approach, further aggregating rare and floor-priced transactions through front-end methods. Blur has previously attempted a similar approach when it bypassed OpenSea's restrictions using front-end methods.

In addition, the competitive direction of CLOB marketplaces should move towards increasing specialization, as demonstrated by Tensor.Trade.

Tensor trading interface

Tensor includes Tensor Trade (Aggregator) and Tensor Swap (AMM Protocol). In terms of user experience, its direction is similar to Blur's, aiming to provide richer information (NFT floor price candlesticks) and additional trading experiences (more diverse order functionalities) for users.

The author also looks forward to seeing the BID functionality on Blur become more robust, such as incorporating take-profit and stop-loss features, as well as batch order management for offers.

The Cliff Race between Blur and OpenSea

Under the competitive pressure from Blur, OpenSea launched a zero-fee model on February 22 to counter Blur, but this did not significantly increase OpenSea's trading volume; it felt more like a passive defensive strategy.

OpenSea's traffic over the past three months (Similarweb)

Blur's traffic over the past three months (Similarweb)

In terms of traffic, OpenSea has been severely impacted by Blur's token issuance.

On the other hand, Blur is also under significant pressure. After layoffs in 2022, OpenSea reportedly has around 230 employees and raised $300 million in its last funding round, giving it a relatively strong financial position. In contrast, Blur has disclosed only $14 million in funding; while its operational costs are lower, it also has fewer resources. The zero-fee model of Blur, both legally (under SEC regulation) and in the market, cannot generate income through transaction fees, nor can it empower $BLUR in any way. It can be said that Blur has pulled itself and OpenSea into a cliff race, engaging in a game where death is the endpoint.

This war is bound to end with one side outlasting the other; however, in the process, secondary NFT marketplaces like X2Y2 and LooksRare are facing greater pressure and may collapse even faster.

Current State of AMM Protocols

In the AMM direction, there are not only Sudoswap but also early projects like NFT20/Unicly, which typically added fragmentation or ERC20 conversion.

This process has not significantly helped the liquidity of NFTs themselves. The author believes that Sudoswap's approach is relatively more straightforward.

Standard AMMs can only handle the consistency of NFTs. Sudoswap addresses inconsistency through a multi-pool model, allowing users to adjust to different rarity levels and match them with different pricing pools. It then integrates these through the front end. This design has some cleverness, but in practice, this stratification is insufficient to address complex rarity issues and does not effectively solve the problem.

The author had high hopes for Sudoswap early on and closely followed its airdrop process. In the face of strong competitors like OpenSea, the competitive landscape of NFTfi does not resemble that of DeFi in its early days. Uniswap's growth benefited significantly from the bear market of 2018-2019, allowing it time to accumulate users.

However, time is not on Sudoswap's side; lack of incentives equals death. Web3, to some extent, is an enhanced version of Web2, especially regarding the Matthew effect, with Web3 carrying a turbocharged version of this effect. Long-term observers of DeFi will notice that since 2022, DEXs on the ETH chain have primarily captured long-tail tokens, with Uni dominating this space. Aside from 1inch and Curve, other DEXs have faced significant pressure in terms of both market capitalization and trading volume.

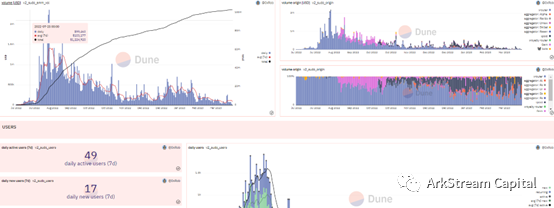

However, Sudoswap's airdrop plan has left both yield farmers and players in pools 1 and 2 disheartened. The author even suspects that the project team did not intend to manage this project well; Sudoswap's airdrop seems entirely aimed at benefiting Xmon holders or the project team itself, as most Xmon is held by the project team, without considering long-term positive incentives for Sudoswap.

Sudoswap data dashboard (dune)

In stark contrast to Blur, Sudoswap's airdrop has effectively hindered its progress. After the airdrop, there was no coherent token incentive plan to support liquidity for its AMM.

However, as mentioned earlier, we still believe that AMMs have significant potential in handling floor prices within the current CLOB marketplace logic. Given the contradictions between the consistency and inconsistency of NFTs, neither the P2P (CLOB) nor the P2Pool (AMM) models can effectively solve the liquidity issue of NFTs. Therefore, the author believes that a fusion of the two, with one as the primary focus, may be a promising direction.

Conclusion

Despite the many flaws in Blur and the $BLUR token price remaining sluggish since its launch, with the community criticizing the empowerment issues of $BLUR, the author believes that Blur's commitment to enhancing liquidity in the NFT market places it in a crucial ecological position at this time. Only with sufficient liquidity can the second chapter of NFTfi emerge. Just as the growth of T1 DeFi projects like Uniswap and AAVE paved the way for the growth of T2 DeFi projects like YFI and 1inch.

The cliff race between Blur and OpenSea is merely the first chapter in the infinite war of NFTfi; let us continue to pay attention to NFTfi.

Risk warning

Risk warning Risk warning

Risk warning