What should we pay attention to after the Shanghai upgrade era?

Once users are able to reselect the staking protocol, a new round of Ethereum staking will begin to reshuffle.

Once users are able to reselect the staking protocol, a new round of Ethereum staking will begin to reshuffle.Original Title: "What Should We Pay Attention to After the 'Shanghai Upgrade' Era?"

Original Source: Huobi Research

Abstract

Ethereum will complete the Shanghai upgrade in April, at which point the withdrawal feature for staked ETH on the Beacon Chain will be opened. The Shanghai upgrade is a hard fork of Ethereum's execution layer, expected to implement a total of 9 EIPs. As of March 14, 2023, approximately 17.5M ETH has been staked, accounting for 15.25% of the total ETH supply. Ethereum validators have averaged over 2 ETH in staking rewards, and after the Shanghai upgrade, over 1 million ETH will flow into the market.

The impact of the Shanghai upgrade on the Ethereum ecosystem is undoubtedly significant. This article mainly discusses the withdrawal design and related risks of Ethereum and LSD protocols after the Shanghai upgrade, as well as the effects on the price of ETH and the prices of derivative tokens related to LSD protocols.

I: Ethereum's Official Withdrawal Process

Withdrawals are implemented through upgrades to both the execution layer and the consensus layer, with two rules: "partial withdrawal" and "full withdrawal." Partial withdrawal only extracts the reward portion; full withdrawal exits the validator node, extracting both rewards and staked ETH. There is no priority difference between these two withdrawal methods; they will be executed automatically as long as the necessary conditions are met:

Necessary conditions: The validator possesses a 0x01 Credential (active validator deposit proof, currently 42% of validators have this proof).

Partial withdrawal conditions: The validator is in Active status, and the validator's balance is greater than 32 ETH.

Full withdrawal conditions: The validator is in Withdrawable status (this usually means the validator has exited the network).

The number of withdrawal requests executed by the Ethereum Beacon Chain within a fixed time is strictly limited, with a maximum of 16 withdrawal requests processed per block. Once validators meet the withdrawal conditions and submit applications, a withdrawal list is created to include all validators who have submitted withdrawal requests, detailing the withdrawal order, execution layer receiving address, and withdrawal amount. Withdrawal requests are initiated at the consensus layer and will not proceed independently or enter the transaction memory pool, so withdrawal actions do not require gas and will not increase Ethereum's gas.

II: Will There Be a Sell-off of Ethereum?

According to data from Beaconcha.in, as of March 14, 17,573,625 ETH has been staked on the Beacon Chain. The number of active validators is 549,181, with each validator currently averaging 33.98 ETH staked, and the total ETH on the Beacon Chain is 18,661,170.4 ETH.

Figure 1. The network history of Ethereum (Source: Beaconcha.in)

Based on the withdrawal conditions and processes, 512 validators can withdraw each Epoch (each Epoch has 32 slots, one slot per block), resulting in 115,200 validators being executed for withdrawal each day (12 seconds per block, 7,200 blocks per day). The total daily withdrawal limit is 3,686,400 ETH. If we disregard other factors, it is estimated that it would take approximately 5.06 days to completely withdraw all staked ETH based on the current amount. However, the execution of withdrawals takes time, and all exiting validators must wait at least 27.3 hours before they can begin to withdraw.

The staking of ETH began in November 2020, when the ETH price was between $500 and $600. These long-term stakers are likely to be eager to withdraw their ETH and rewards. Additionally, staking that began in February 2021 is currently at a loss compared to today's prices. Most withdrawal requests are expected to be "partial withdrawals." It is anticipated that after the withdrawal feature is opened, the selling pressure on ETH will not be too severe, primarily driven by early players' sell-off behavior.

Figure 2. ETH price curve (Source: coinmarketcap)

The withdrawal process is not always smooth, and there are some cases where the withdrawal conditions are not met, especially for those with only a 0x00 Credential deposit proof, who will need to convert their proof to a 0x01 Credential after the Shanghai upgrade. This conversion is also limited to 16 requests per block. Validators with 0x00 credentials tend to be older and have accumulated more staking rewards, which will gradually increase the total amount of ETH withdrawn per block. In extreme cases, a complete exit of validator nodes is unlikely, as various staking protocols need to meet outflow limit functions, which somewhat reduces selling pressure. Based on the above analysis, it can be predicted that there will be significant selling pressure on days 3-4 after the Shanghai upgrade.

Additionally, according to data from Glassnode, there are approximately 920 nodes with intentions to exit as validators. At the same time, due to regulatory reasons, most ETH tokens staked through centralized institutions will be unlocked, and in extreme cases, a complete exit may be required. This may include Kraken (6.52%) and Binance (4.92%), which account for over 2 million ETH. Due to the validator outflow limit function, it will also take about a month to complete all withdrawals. However, these staked ETH will not fully circulate in the market and are likely to continue being deposited into other staking protocols.

Figure 3. Statistics on the number of voluntarily exiting validator nodes (Source: Glassnode)

LST tokens now account for about 65% of the total staked amount. These staked derivative tokens have experienced significant discounts in the past two years. Currently, due to the approaching Shanghai upgrade, LSTs have good overall liquidity. The opening of withdrawals is a positive factor for LST price recovery, but it also tests the risk management capabilities and withdrawal process designs of various LSD projects.

III: Current Status and Withdrawal Design of Various LSD Protocols

3.1 Performance of Liquid Staking Tokens (LST)

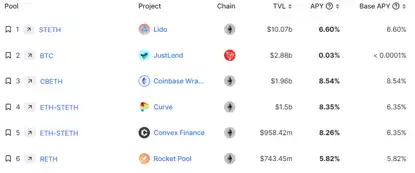

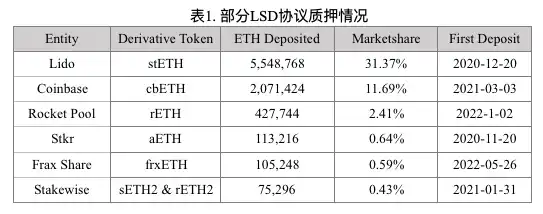

Currently, the total staked ETH of various LSD protocols accounts for 42.97% of all staked amounts, with Lido protocol alone accounting for over 30%. The derivative tokens of these protocols, LST, have already circulated in the secondary market ahead of the Shanghai upgrade, and they currently show good performance in DeFi protocols.

Figure 4. DeFi yields ranking (Source: Defillama)

LST tokens now account for about 65% of the total staked amount. These staked derivative tokens have experienced significant discounts in the past two years. Currently, due to the approaching Shanghai upgrade, LSTs have good overall liquidity. The opening of withdrawals is a positive factor for LST price recovery, but it also tests the risk management capabilities and withdrawal process designs of various LSD projects.

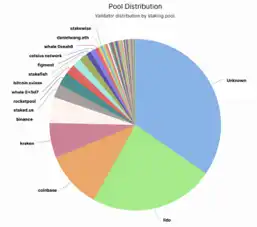

Figure 5. Ethereum staking proportion

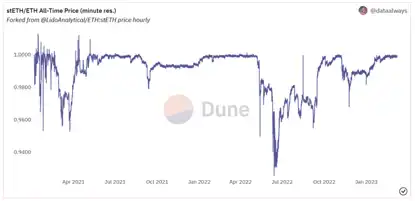

stETH is currently the most liquid LSD token. The stETH/ETH price curve below shows that the stETH/ETH price experienced significant discounts during March 2021 and June 2022, corresponding to the 3AC and FTX events, respectively. This was mainly due to insufficient liquidity. The sell-off in 2021 coincided with the market peak, and most of the sellers were stakers from the end of 2020, who made considerable profits upon exit.

Figure 6. stETH/ETH price curve

Coinbase's LST token cbETH had previously been in a discounted state, primarily traded on Uniswap, with a current TVL of approximately $7.5M and low daily trading volume, which may lead to liquidity issues. However, it has recently shown strong performance. As the Shanghai upgrade approaches, arbitrageurs may profit by purchasing discounted cbETH.

Figure 7. cbETH TVL (Source: Uniswap)

Rocket Pool holds the third-largest market share among LSD protocols, with its derivative token rETH having a market cap of $391M and a circulation of 210,000. After the Shanghai upgrade, users can return rETH to the protocol to redeem staked ETH and corresponding rewards, so the price of rETH in the secondary market has consistently been higher than ETH.

Figure 8. rETH/WETH price curve

3.2 Comparison of Withdrawal Processes of Various LSD Protocols

The withdrawal scheme designs of various LSD protocols carry uncertain risks. The Ethereum Shanghai upgrade is an improvement to the PoS mechanism and a challenge to LSD protocols. Protocols need to balance user experience, operational speed, and security. Overall, the Ethereum PoS withdrawal process is very complex, especially since the time allocation varies across different withdrawal protocols. After the Shanghai upgrade, various LSD protocols may face attacks due to design flaws. Most withdrawal designs will address the following two issues:

Avoiding attacks and arbitrage behaviors: This mainly concerns the protocol exchange between LST tokens and ETH and potential price fluctuations in the secondary market that could lead to arbitrage, thereby reducing the protocol APR. Ensuring the protocol has enough ETH for user redemptions is also crucial.

Setting withdrawal thresholds while enhancing user experience, especially regarding user wait times.

3.2.1 Lido

The Lido v2 version has been approved through community voting. Lido's withdrawal design has two modes: Turbo and Bunker. Lido has established a withdrawal buffer, mainly composed of execution layer rewards, withdrawal ETH, and user-staked ETH. After the Shanghai upgrade, Lido will have 200,000 ETH available for immediate withdrawal (without going through the validator exit process), which can be used to establish the buffer.

Turbo mode: Once there is enough ETH, the protocol will fulfill withdrawal requests. The request time varies from 1 hour to 3/4 days, depending on whether the buffer has enough ETH, with wait times being uncertain (requiring validator nodes to exit).

Bunker mode: If Lido validator nodes experience widespread penalties, triggering this mode, users will need to wait until the penalized nodes exit to predict losses, which will then be shared among users. Additionally, it must ensure that the stETH:ETH redemption calculation can be accurately performed. In this mode, withdrawals may take over 36 days.

Once a user's withdrawal request enters the queue, they will receive an NFT representing their position in the withdrawal request queue. This NFT can be traded in the secondary market, allowing users willing to bid to purchase positions closer to the front of the queue. If ETH prices fluctuate significantly in April, this secondary market could have many strategies. If penalties occur during the request period, users in the queue will also have to share the penalty proportion. However, stETH withdrawal requests in the queue do not earn rewards, which is also to prevent malicious arbitrage attacks.

In addition to the above designs, to avoid attacks and arbitrage, Lido has other requirements for withdrawals, such as withdrawal requests cannot be canceled, and the redemption rate requested cannot be better than the redemption rate at the time of request creation.

3.2.2 Rocket Pool

Rocket Pool introduces minipools, lowering the capital requirements for validators, allowing them to operate a minipool with just 17.6 ETH. When withdrawing from the pool, the validator's funds will first incur losses, providing rETH holders with 110% insurance.

For withdrawal requirements, Rocket Pool has designed a deposit pool, where rETH redemptions can be provided from the deposit pool and partial withdrawals. rETH can also be exchanged for ETH at a low price in the secondary market, creating an arbitrage opportunity for minipool operators, as they can purchase discounted rETH from the secondary market and use Rocket Pool's burn mechanism to exit minipools, ensuring rETH:ETH = 1:1 exchange rate. Thus, minipool operators can choose whether to exit or withdraw rewards, entirely determined by market behavior.

For Rocket Pool, the withdrawal process is not complicated; operators only need to withdraw minipools. However, it is crucial to enhance the liquidity of the protocol's deposit pool to ensure smooth redemption of rETH. During the Ethereum merge, the Rocket Pool protocol handled the merge well, while one of Lido's node operators experienced downtime. Therefore, in dealing with the withdrawal process after the Shanghai upgrade, Rocket Pool is expected to perform better. The Atlas upgrade launched by Rocket Pool will lower the threshold for becoming a validator, further promoting rETH liquidity and RPL token prices.

3.2.3 Frax Finance

Users stake ETH with Frax, and frxETH does not accumulate staking rewards but can be redeemed for ETH at a 1:1 ratio within the protocol. To earn staking rewards, users need to deposit frxETH back into the protocol to receive sfrxETH. Therefore, Frax's redemption will not be affected by the Shanghai upgrade; the more critical consideration is whether the protocol can provide enough ETH for redemption. Especially when Frax can no longer attract users based on higher yields, there may be a large number of redemptions.

Figure 9. frxETH APY & TVL (Source: Defillama)

3.2.4 StakeWise

StakeWise offers liquid staking services similar to Lido, but the new upgraded V3 version is designed to address the risks of centralized validators, although this version has not yet been launched. StakeWise has two staking mechanisms: Pool and Solo. The Pool mechanism is a staking pool for any ETH holder, while the Solo mechanism provides non-custodial staking services for users with 32 ETH.

In terms of exit mechanisms, users in the Pool mechanism will need to wait until after the Shanghai upgrade to destroy sETH2 and rETH2 within the protocol and receive ETH in a 1:1 ratio as a reward. Before the Shanghai upgrade, there is a secondary market where sETH2 and rETH2 can be traded. Solo users can choose to exit voluntarily before the Shanghai upgrade, but their balance will be inaccessible and cannot re-enter staking. After the Shanghai upgrade, those who choose to exit voluntarily will continue to incur fees until fully exited, which takes several days.

IV: Conclusion and Thoughts

The impact of the Shanghai upgrade on LSD protocols mainly has three aspects:

Token prices, including ETH, various LSD protocol tokens, and protocol derivative token prices;

Withdrawal design tests the technology of various LSD protocols, as users begin to reallocate;

More DeFi protocols derived from Ethereum staking or LSD protocols.

Once users can reselect staking protocols, a new round of Ethereum staking reshuffling will begin. Moreover, new LSD protocols or staking-based mechanisms will be launched, such as applications based on DVT technology and the re-staking concept of EigenLayer, which may offer better yields. For most ETH stakers, after the Shanghai upgrade, they can change their initial staking methods and targets, leading to a redistribution of the entire Ethereum staking market share.

In terms of withdrawal design fluidity, staking yields, permissionlessness, and security, users will consider more liquid staking protocols. Besides Lido, Rocket Pool may be the fastest-growing LSD protocol, and attention should be paid to the number of minipools established after the Shanghai upgrade and its token price trends. Especially with its Atlas upgrade, which addresses withdrawal design, reward systems, and scalability.

Index tokens based on LSD have already emerged. For example, Gitcoin has collaborated with Index Coop to launch the new Ethereum staking index token gtcETH, aimed at providing users with a place to obtain mixed yields from various liquid staking services. This also helps promote multiple LSDs, further decentralizing Ethereum. In addition, more DeFi applications will emerge:

Utilizing LST to mint new derivatives;

Futures products anchored to ETH yields;

Stablecoin projects based on staked ETH. The unlocking of Ethereum staking may also bring incremental benefits to lending protocols, as many articles have analyzed the potential high yields from re-staking.