Foresight Ventures: The Productization Journey of Perpetual DEX's LP

DeFi products have gradually transformed from a single product form aimed at interactive users to a dual product form targeting both LPs and interactive users.

DeFi products have gradually transformed from a single product form aimed at interactive users to a dual product form targeting both LPs and interactive users.Original Author: Kylo, Foresight Ventures

Tips:

The AMM mechanism of Uniswap and the liquidity mining of Compound are the ancestors of LP productization.

DeFi native products should cater to both LPs and interactive users.

Order book systems as a narrative of Web 2.5 should not be too constrained by Web 3.

Perpetual Protocol's development has been hindered due to issues with LP productization.

The most successful aspect of P2P pool Perpetual DEX is the realization of LP productization.

P2P pool Perpetual DEX LPs will give rise to a large number of derivative products.

Overview

The main narrative of this article focuses on the productization of LPs, which is the process of transforming the liquidity of DeFi protocols into a standardized product. In people's initial understanding, a good product should serve users as a whole.

Taking DyDx and 0x protocol as examples, both integrate market makers into their products and package them into a trading platform through good UI design, providing traders with smooth trading services and capturing trading fees. This is a typical product thinking aimed at a single user.

The emergence of Uniswap's AMM model and Compound's liquidity mining should be regarded as the ancestors of LP productization: the AMM model allows LPs and traders to interact and influence each other; Compound's liquidity mining stimulates users' deposits and loans, blurring the identity boundaries between borrowers (interactors) and depositors (LPs), allowing LPs to earn returns without loss.

The two scenarios mentioned above actually reflect the characteristics of LP productization:

LPs can obtain standardized returns under controllable risks.

After providing liquidity, corresponding LP notes will be issued to lay the foundation for subsequent LP leverage.

The productization model of LPs has been proven to be a feasible solution in spot AMM DEXs and lending protocols. Currently, the idea of LP productization is also gradually emerging in the development of Perpetual DEXs. The mechanism of Perpetual DEX has undergone three major changes from 2017 to now: from DyDx's order book mechanism to Perpetual Protocol's vAMM, and now to the P2P pool trading model.

These changes in trading models actually reflect the aesthetic and morphological changes of on-chain Perpetual DEXs: DeFi products are gradually transforming from a single product form aimed at interactive users to a dual product form aimed at both LPs and interactive users. This model also answers the question of what constitutes a good DeFi product, namely:

The smoothness of the interactor's experience, i.e., the launch of interactive products.

The separability of LP risks and the simplicity of market making, i.e., the launch of LP products.

Currently, both order book systems and P2P pool models have the opportunity to achieve LP productization, while the vAMM model is temporarily unable to do so. The reason vAMM cannot be realized is that there is currently no effective LP management method.

That is, there is no effective way to separate LP risks and returns; the order book system, assisted by some on-chain financing protocols and Advisor Protocols, can achieve the democratization of LP's income rights, but the management rights of LPs are still limited; in the P2P pool model, GMX's GLP pool and gTrade's gDAI pool are typical LP products.

This means that for GMX and gTrade, Perpetual Trading is the trading product they offer to traders, while GLP and gDAI are yield products provided for ordinary retail investors. These two products complement each other, creating a logically coherent system.

In the subsequent structure of this article, we will interpret the mechanisms of the three types of Perpetual DEXs and elaborate on their possibilities and methods for achieving LP productization. Finally, we will explain why LP productization is of great importance to the development of DeFi from the perspective of the historical development of DeFi.

1. Order Book Trading Model

The order book system is currently the most widely used and robust trading model. It is inherited from TradFi, providing functions for price discovery, liquidity provision, and trading of Perpetuals. Currently, mainstream Perpetual trading products, such as WOO Network, Orderly Network, DyDx, etc., all adopt the order book trading model.

Since the trading model of traditional markets is mostly order book-based, the migration cost for traders interacting with order book products on the blockchain is very low. Additionally, for market makers, a series of risk control tools already exist for order book systems. Under controllable risks, market makers can stably earn trading fees and customer loss profits.

The order book trading model is already a very mature trading model in the TradFi industry, but due to the significant differences between blockchain characteristics and TradFi, order book systems may face adaptation issues in the blockchain ecosystem, including:

Due to the limitations of on-chain TPS, the order matching process is implemented off-chain, with only the final transaction settlement occurring on-chain.

The liquidity provided by market makers, while highly capital-efficient, cannot be leveraged.

Liquidity is monopolized by market makers, and on-chain users cannot share in the profits of market makers.

In fact, the so-called adaptation issues mentioned above do not fundamentally affect the order book model; rather, they arise from the clash between the two different ideologies of TradFi and DeFi Native. Therefore, regarding the future development direction of order book DEXs, Web 3 is divided into two perspectives: one is the Web 3 Native perspective, and the other is the pragmatic perspective.

From the Web 3 Native perspective, order book data should be on-chain; (currently, chains like Sui Network claim to have the opportunity to achieve complete on-chain order books, but this can only be realized in testnet environments; DyDx's V4 version also claims to utilize a mempool-like model to achieve decentralization of order books.) The liquidity of the order book system should seek ways to achieve leverage.

However, from the pragmatic perspective, a fully on-chain order book system still faces two main issues:

Professional traders have privacy trading needs, and the existence of a fully on-chain order book may disrupt the environment for private trading.

Decentralization and high performance are somewhat contradictory; putting all order book data on-chain is essentially a compromise towards centralization in the blockchain. Compared to centralizing at the level of matching, centralization at the entire blockchain level may be more unacceptable.

Moreover, the issues of LP income democratization and LP leverage also face inefficiencies and high costs. First, the democratization of LP income relies on Advisor Protocols and some on-chain fund protocols, meaning that order book market makers finance on-chain and use the borrowed funds to participate in the order book system's market making, but the management rights of that LP are still monopolized by the market makers themselves.

Secondly, LP leverage relies on the democratization of funding sources. After market makers raise funds on-chain, they generally issue a note to the users providing funds, representing that user's ownership of part of the market maker's funds. Since this note has ownership of the market maker's funds and partial income rights, it also possesses the fundamentals to participate in other DeFi ecosystems. Throughout this process, the order book needs to incur three levels of additional costs to achieve so-called LP productization:

Financing costs

Integration costs for the issued LP notes to participate in other DeFi ecosystems

Costs for maintaining LP exit liquidity

Excessive costs imply a poor business model. Therefore, while the LP productization model has the potential to be realized on-chain, it may not be the optimal choice.

So, from a pragmatic perspective, what will be the future development trend of order books? As an import from TradFi, the positioning of order books should be at the Web 2.5 stage. This means it should leverage the advantages of both TradFi and DeFi to serve Web 3 users: the advantage of TradFi lies in the market maker system and the mature order book model; the advantage of DeFi lies in the transparency brought by on-chain settlement of assets and the asset attributes of tokens.

Rationally utilizing the asset attributes of tokens to incentivize liquidity and combining marketing is the best gift that DeFi brings to TradFi.

2. vAMM Trading Model

The vAMM mechanism was first proposed by Perpetual Protocol, currently having V1 and V2 versions. The V1 version provides a trading method with infinite liquidity, where trading does not require long and short counterparties. In the V1 version, there is no real liquidity for ETH - USDC, but we can understand it as a virtual AMM pool, with the k value manually adjusted by the official team.

When a trader conducts a trade, assuming they go long on ETH with 5x leverage, Perpetual Protocol will generate 5x virtual USDC and exchange that 5x USDC for an equivalent amount of 5x ETH in the virtual pool. This 5x ETH is equivalent to the trader's 5x leveraged long position on ETH. Since there is no real liquidity in the V1 version, the aforementioned swap process does not actually occur; we can simply understand it as an accounting process.

The core of the entire mechanism is the setting of the k value, which directly relates to the impact of each trade on the contract price. If the k value is set too high, the contract price becomes insensitive to the opening volume, affecting the trader's experience; if the k value is set too low, the opening volume has too great an impact on the contract price, which can directly cause losses for traders. The reasonable choice of k value lies in real-time adjustments based on CEX liquidity.

When the pools managed by Perpetual Protocol are few, manually adjusting the k value is a relatively reasonable choice; however, as the number of pools continues to increase, manual adjustments may struggle to keep pace with market changes. Therefore, considering the issue of market-based pricing for the k value, Perpetual Protocol proposed the V2 version.

Perpetual Protocol V2 constructs actual "virtual liquidity" using Uniswap V3. "Actual" means that there are indeed real LPs in V2, while "virtual liquidity" indicates that the liquidity within Perpetual Protocol V2 is not the common AMM LP liquidity but rather virtually generated non-real value AMM LP.

When LPs provide liquidity in V2, they need to deposit USDC. For example, if an LP wants to provide liquidity with 1000 USDC, the system will generate up to 10000 vUSDC for them. This LP can then exchange this 10000 vUSDC for an equivalent amount of vUSDC - vETH trading pair based on the current vETH - vUSDC exchange rate, and after setting a reasonable price range, deposit this LP into Uniswap V3 to provide liquidity for Perpetual V2.

(Of course, this LP can also retain some vUSDC, such as only providing liquidity equivalent to 8000 vUSDC, while the remaining 2000 vUSDC can be used for trading.) When the liquidity of vETH - vUSDC is abundant, the k value of the LP is naturally determined by the market.

The price of vETH in the vETH - vUSDC LP pool calculated by the vAMM model is the pricing for ETH perp by Perpetual Protocol V2. To anchor the perp price to the spot price, Perpetual Protocol introduces funding rates to balance longs and shorts.

In fact, we can provide a more concrete description of the abstract concept of Perpetual Protocol V2's actual "virtual liquidity." The vUSDC generated when LPs deposit USDC exists in the form of ERC-20, and the constructed vETH - vUSDC LP also truly exists in Uniswap V3.

The liquidity provided by LPs essentially provides liquidity for vETH - vUSDC, and the perp trades conducted by traders are essentially transformed into spot trades of vETH - vUSDC, with the price of vETH being the current pricing for that perp. Since the pricing of vETH is independent of the pricing of ETH, to anchor these two prices as closely as possible, the funding rate tool is naturally introduced into Perpetual Protocol.

From the mechanisms described above, it can be seen that the boundaries between LPs and traders are quite blurred, mainly reflected in three points:

LPs can open positions in their trading accounts using unused vUSDC after providing liquidity.

When there is an imbalance between longs and shorts, LPs need to act as counterparties to bet against traders.

LPs also provide leveraged liquidity when providing liquidity.

The second and third points are the main risks faced by LPs, and this part of the risk is caused by the mechanism of vAMM itself, which cannot be hedged by other means. The risk of LPs acting as counterparties to traders is that some of their LP positions automatically become trading positions.

Since LPs automatically choose to provide leveraged liquidity when market making, this means that these trading positions are also leveraged positions, and LPs need to pay funding rates and may face liquidation.

The Perpetual Protocol team has also recognized these issues and is trying to reduce the risks faced by LPs as much as possible through subsidies and an Insurance Fund mechanism. The subsidy mainly comes into play when LPs face impermanent loss and losses incurred from betting against traders; Perpetual Protocol will subsidize LPs with a certain amount of $Perp. The purpose of the Insurance Fund is to act as a counterparty to traders when there is an imbalance between longs and shorts in Perpetual Protocol, thereby reducing the direct market participation risks that LPs may face.

These two remedies may seem effective, but in reality, they are a form of disguised transfer payments. The $Perp subsidy mainly eliminates the losses faced by LPs through bubbles in the secondary market, which is essentially unsustainable; the funding source for the Insurance Fund comes from part of the liquidation fees and 20% of the taker opening and closing fees, which essentially comes from protocol fees and LP earnings.

This effectively forces a portion of the earnings that should be obtained by LPs to be redistributed to the Insurance Fund, reducing the overall earnings of LPs and correspondingly lowering overall risks.

Overall, the vAMM model of Perpetual Protocol currently appears to be a crypto-native perp pricing model. This mechanism cleverly leverages the advantages of Uniswap V3's trading mechanism but also inherits the significant impermanent loss drawbacks of Uniswap V3.

In Uniswap V3, the price range set by LPs is equivalent to the price range at which LPs are willing to act as counterparties to traders. Within this price range, if the buying and selling sides of traders are not well balanced, then LPs will engage in a game against traders as counterparties. Similarly, in Perpetual Protocol V2, if the longs and shorts are not balanced, LPs will act as counterparties to traders, bearing various gains and losses.

In CEXs, market makers and traders have various mature risk management strategies for their games, such as limiting delta positions. However, since the trading model of Perpetual V2 is automated and mandatory, LPs cannot reasonably manage their position risks. When prices fluctuate sharply, LPs will be exposed to significant risks due to impermanent losses and the existence of trader PnL.

The V2 model of Perpetual Protocol can also be considered a P2P pool trading model, where LPs will also bet against traders under certain conditions. However, the risk tolerance of LPs under the vAMM model is far lower than that of LPs under the P2P pool model, mainly because LPs under vAMM bear their own risks, while LPs under the P2P pool model share all risks collectively, and individual risk tolerance is far lower than that of the collective.

For P2P pools, losses caused by extreme market conditions will be averaged among all LPs; but for the vAMM model, some LP positions may be directly liquidated.

Since the income earned by LPs and the risks they bear in vAMM are closely related to their own risk management capabilities, and there is currently a lack of risk management tools for Uni V3, this results in higher market-making risks on Perpetual V2, while returns are relatively low, making it impossible for LPs to participate in the liquidity provision of Perpetual Protocol in a standardized manner.

Providing subsidies to LPs is also a form of disguised transfer payments that cannot solve the actual problems. Therefore, for Perpetual Protocol, its LPs are difficult to present in a productized form, and its subsequent development will be constrained.

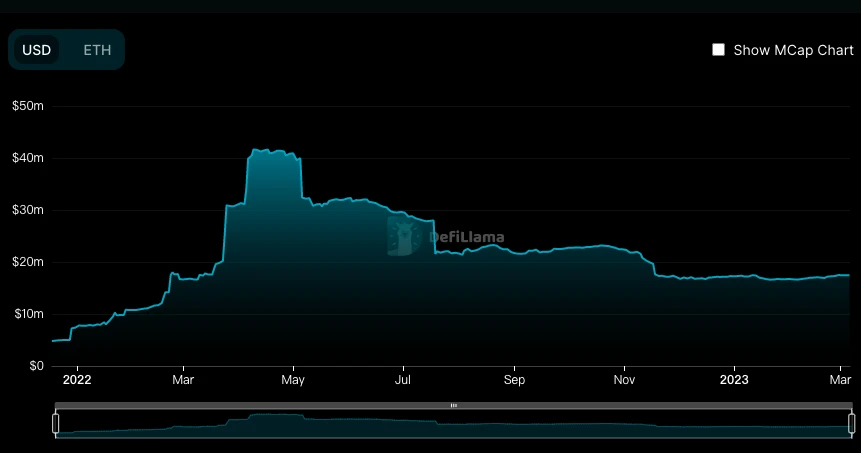

From the data perspective, the TVL data of Perpetual Protocol does not look good, and the root of the problem lies in the LP productization aspect.

3. P2P Pool Trading Model

For Perpetual Protocol V2, the vAMM design is indeed an innovation in the trading paradigm of the blockchain industry, enabling on-chain price discovery for Perpetuals. However, the cost of this price discovery function is that LPs bear excessive risks, which are difficult to hedge, meaning that under certain returns, risks are uncontrollable.

In a situation where the experiences of trader users and LPs are inconsistent, it is difficult for the product to grow into a universal protocol. The P2P pool model of GMX emerged on the historical stage against this backdrop. The P2P pool Perpetual Trading model did not originate with GMX but was greatly developed within GMX.

Its main advantage lies in the modularity of the trading module, which can be split into LPs, trading users, pricing systems, settlement systems, etc., with each part able to operate independently, while the risks for LPs can also be split.

The modular design should be one of the most important product thinking brought to the blockchain industry by the ETH 2.0 upgrade. The GMX-style product design is philosophically consistent with ETH 2.0. In the future planning of ETH 2.0, PBS (proposer-builder separation) is one of the important steps in the Ethereum upgrade.

Its main function is to separate the two steps of block construction and block proposal, as the block builder needs to construct all blocks, including beacon chain blocks, within the time of a slot, which requires high computational power.

However, for public chains, high computational loads and decentralization are contradictory; the existence of high computational loads severely undermines the decentralization characteristics of the blockchain. The existence of PBS combines high computational loads with decentralization, specifically by transferring high computational loads off-chain and returning only the computation results after completion.

The implementation logic of PBS can answer the pricing issues of on-chain Perpetual Trading. The pricing of derivatives requires high computational loads and effectiveness. If the computations related to derivative price discovery are forcibly placed on-chain, the delays and errors in computation results caused by insufficient computational loads will ultimately be borne by traders and LPs.

However, if the computations related to derivative pricing are placed off-chain, and the results are transmitted to the chain via oracles after completion, traders and LPs will not face losses caused by the price discovery mechanism.

Therefore, the design of P2P pool Perpetual DEX essentially hands the complex pricing issues of derivatives over to CEX for quoting, and then utilizes a CFD model for on-chain trading, with the final results settled on-chain. Completing the settlement requires a liquidity pool, which is essentially the pool in the P2P pool.

Currently, classic projects in P2P pool Perpetual DEX include GMX and gTrade, but the fundamental mechanisms of the two differ significantly. Overall, GMX is more risk-seeking and has a more aggressive style compared to gTrade; additionally, due to the complexity of GLP's composition and risk, the derivative products related to GLP are more numerous compared to gTrade.

3.1 GMX Trading Mechanism

A transaction on GMX requires several steps:

GMX obtains various contract price data from CEXs through oracles.

Based on the pricing and the weights of various CEXs, GMX calculates the contract price for opening positions.

Based on the opening leverage, a portion of assets is borrowed from the GLP pool for final asset settlement.

Depending on the duration of the position, borrow fees and corresponding opening and closing fees are paid.

GMX's invocation of CEX contract prices incurs no slippage, which is indeed an advantage that attracts traders to GMX. However, often the strengths of a product can also be its weaknesses. Since slippage is a cost of liquidity, no slippage means a third party bears this cost.

In the GMX scenario, the GLP pool ultimately bears the losses caused by slippage. (On GMX's AVAX mainnet, there have been instances of arbitrage due to insufficient AVAX liquidity. Currently, quantitative funds often engage in arbitrage activities between GMX and CEX based on CEX liquidity.) Therefore, the no-slippage trading model essentially subsidizes traders through the GLP pool to attract them to trade.

However, the arbitrage behavior related to slippage has not become a serious issue for GMX, mainly because the high yield sharing of the GLP pool masks the losses incurred from arbitrage activities.

When GMX traders conduct trades, they need to borrow assets and pay borrow fees. This portion of borrow fees is one of the sources of GLP's income. However, the purpose of borrowing assets differs from the principles of leverage platforms like Gearbox. The funds borrowed by GMX are to prepare sufficient spot assets for each position for final settlement; while Gearbox is similar to margin trading, where the borrowed assets represent the actual leverage obtained.

Another source of income for GLP comes from trader PnL, i.e., the losses incurred by traders during trading. Since there are no funding rates in GMX to balance longs and shorts, GLP holders face naked short positions, meaning LPs directly bet against traders. However, from a long-term perspective, this may not be an issue, as traders generally have a win rate of less than 50%. In such cases, GLP holders often end up in a profitable state, although short-term yields may face significant volatility.

There has been intense discussion within the community regarding the sustainability of GMX's model. Arguments against GMX's sustainability mainly focus on the imbalance of GMX positions due to the absence of funding rates. In a bull market with one-sided trends, the GLP pool may face significant risks from naked short positions, with the potential for large losses.

However, this issue is similar to addressing how CEXs avoid naked short positions during bull markets. The currencies supported in the GLP pool are only a few highly liquid blue-chip assets, so there will not be a one-sided trend similar to Luna.

Moreover, major CEXs also have sufficient liquidity, and GMX can hedge risks through CEXs or other on-chain DEXs or directly implement position limits. Overall, GMX has many available risk-hedging methods during bull markets.

In fact, GMX's team has also recognized potential flaws and risks in its model design. In version X4, they mentioned several possible improvement plans for the future, but essentially they remain compromises:

Introduce new assets to the GLP pool, but the assets that can be opened for positions are still limited to the assets that make up GLP.

Introduce funding rates to balance the issue of excessive naked short positions during extreme market conditions, which means that traders may need to pay both borrow fees and funding fees when trading on GMX.

Adjust the ratio of non-stablecoins to stablecoins in the GLP pool during extreme market conditions to increase the capacity for opening positions.

These improvement plans have not yet been finalized and are still under discussion. Discussions related to GMX may continue indefinitely.

In summary, GMX's characteristics include:

No slippage in trading, with this cost borne by GLP.

No funding rates, so GLP may face significant naked short positions.

Traders need to pay borrow fees to GLP.

Limited by GLP, only certain currencies can be traded on GMX, lacking scalability.

From the design of the GLP model, it can be observed that the LPs attracted by GMX are mostly high-risk tolerant. Whether it is the no-slippage trading model or the existence of naked short positions, both imply that GLP holders bear more risks and obtain risk returns. In contrast, the model design of gTrade is more conservative and LP-friendly.

3.2 Gains Network (gTrade) Trading Mechanism

gTrade (GNS) was originally a Perp Trading product on Polygon, later migrated to Arbitrum, and its overall design differs significantly from GMX. The specific differences include:

When pricing through oracles, the slippage and opening fees for contracts are calculated based on CEX liquidity and position size.

The mechanism introduces funding rates to balance longs and shorts, reducing the risks of the gDAI pool.

The settlement pool (gDAI) only holds DAI stablecoins.

Traders do not need to pay borrow fees when opening positions but must pay extension fees.

Each address has a limit on unilateral positions, which can be increased by holding NFTs.

Supports trading of various currencies, commodities, and foreign exchange, with strong scalability.

The internal settlement pool of gTrade only contains DAI, and its capital scale is far smaller than gTrade's daily trading volume. In the absence of slippage in the protocol, arbitrageurs can easily cause losses in the settlement pool through slippage arbitrage; the introduction of funding rates aims to ensure that the settlement pool does not have excessive naked short positions, thereby reducing the risks of the settlement pool; extension fees exist to mitigate time risks, aiming to avoid significant one-time losses in the settlement pool due to prolonged holding of profitable positions; unilateral position limits are also designed to prevent significant losses in the settlement pool.

Therefore, from the mechanism design of gTrader, it can be seen that its style is risk-averse compared to GMX. Various risk control mechanisms are in place to ensure the safety of funds in the gDAI pool.

3.3 LP Products under P2P Pool Mechanism

Returning to the main narrative of LP productization, GMX's GLP pool and gTrade's gDAI pool are typical LP products. This means that for GMX and gTrade, Perpetual Trading is the trading product they offer to traders, while GLP and gDAI are yield products provided for ordinary retail investors.

These two products complement each other, creating a logically coherent system. GLP carries higher risks and yields but does not guarantee capital; gDAI has lower risks, but gTrade has set up a series of buffer mechanisms to prevent gDAI users from incurring losses as much as possible.

GLP and gDAI are already relatively mature LP products, but for GLP, since GMX does not use funding rates to balance longs and shorts, the GLP pool often has significant naked short positions, effectively forcing the GLP pool to act as a counterparty against traders.

Additionally, the composition of GLP includes BTC, ETH, Link, Uni, and stablecoins, meaning that the value of GLP will fluctuate with the changes in the spot value of its components, indicating that currency prices are also an important factor affecting GLP's gains and losses. Thus, overall, the risks of GLP can be simply split into two unrelated risks: Delta risk and Trader PnL risk.

The separability of risks implies the possibility of developing derivatives for GLP. Currently, many protocols are attempting to hedge the Delta risk faced by GLP, such as GMD Protocol, Umami Finance, and Rage Trade. However, the Trader PnL risk may be difficult to hedge from a derivatives perspective, and feasible solutions lie in improving GMX's internal mechanisms or attempting to hedge on other DEXs or CEXs.

4. Why is LP Productization Important for the Development of DeFi?

After sorting through the entire history of DeFi development, we can derive a simple three-layer architecture:

The first layer consists of core currencies, such as ETH, BTC, and other blue-chip core assets.

The second layer consists of DEXs, lending, and stablecoins.

The third layer consists of so-called DeFi 2.0 protocols.

The connection logic between these three layers is also straightforward. The connection logic between the first and second layers is to leverage core currencies; the connection logic between the second and third layers lies in the composability of DeFi protocols.

Leveraging core currencies is a stage that all public chains must go through when building their DeFi ecosystems, as it allows for the construction of an endogenous DeFi ecosystem based on leverage. It is worth noting that the connection between the second and third layers, i.e., the composability between protocols, relies on the real yields generated by the second-layer protocols. In other words, the composability between protocols actually reflects the flow of real yields across different protocols.

Currently, there are not many scenarios on-chain that can generate real yields, including:

Financial service fees, such as trading fees, lending fees, etc.

Bribery fees.

Staking yields.

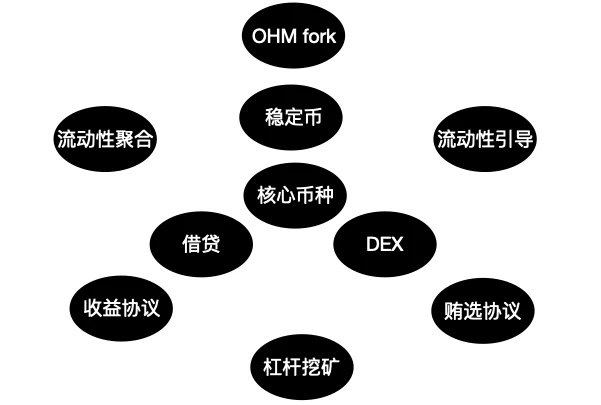

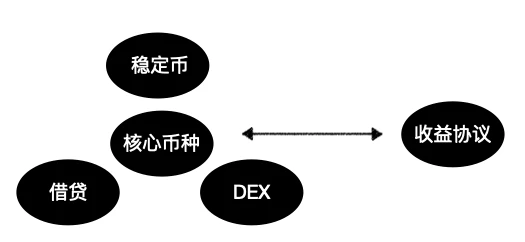

These scenarios with real yields form the basis for the development of DeFi-related products. From the narratives proven in the last DeFi cycle, the core engine driving the initial development of DeFi protocols can be summarized in the following diagram:

The yield protocols here include Yearn Finance and others, whose most important function is LP productization. In the early stages of DeFi development, there were not many users who knew how to fill liquidity in DeFi protocols, and liquidity mining was still a relatively new narrative.

The emergence of Yearn Finance provided LPs with a scenario to earn yields, strategizing ways to earn yields in DeFi so that LPs could passively earn returns based on Yearn Finance's strategies without needing to understand the specific operations.

Although the strategies provided by Yearn Finance may seem overly simplistic in hindsight, they greatly promoted the development of DeFi. After LP productization, the increase in TVL of DeFi protocols entered the fast lane, and the increase in TVL also enhanced the interactive users' experience with DeFi products. Furthermore, LP productization also allows for the possibility of leveraging LPs, laying the foundation for the development and integration of subsequent derivative products and building DeFi legos.

Therefore, for Perpetual DEX, the path of LP productization is essentially replicating the logic of the initial development of DeFi protocols. So what is the takeaway? An underappreciated narrative actually exists in past stories; it is just that this story has been forgotten in the corner after changing its cover. When people suddenly remember that this story can be told in a different way, it becomes fresh again, but if traced back, the core of this story has always existed in the river of time that has passed.

Reference

https://defillama.com/protocol/perpetual-protocol