How should the native benchmark interest rate of the crypto world be defined?

By considering the "risk-free rate," we can understand what types of economic activities in the crypto market may achieve a balance between risk and return.

By considering the "risk-free rate," we can understand what types of economic activities in the crypto market may achieve a balance between risk and return.Author: Mint Ventures

The narrative of the "bond market" in the blockchain industry has gradually gained attention from the market and various investors after DeFi Summer, including discussions on the development model of "interest rate markets" by firms like Multicoin Capital, which invested in related assets during that period. However, even with expectations of "institutional investors entering" and "rapid development of DAOs" at that time, the on-chain bond market did not experience an explosion, and relevant metrics such as TVL remained low. We did not see the flourishing development of the "bond market" in this cycle.

So, does an on-chain bond market actually exist? What kind of development model might a crypto native bond market have? To answer these questions, thinking about the crypto native risk-free rate is an important entry point, as it is the cornerstone that determines the direction of the bond market's development, being a crucial component of the discount factor for crypto native assets. Only by contemplating the "risk-free rate" can we understand what kind of economic activities in the crypto market might achieve a balance between risk and return.

1. The Narrative of Public Chains

How to view public chains has long been an important topic for many investment institutions and researchers. Joel Monegro from USV proposed the concept of "Fat Protocols" in 2016, which has resonated deeply and is still regarded by many investors as an important starting point for the public chain narrative.

In 2021, Tascha introduced the logic of "National Valuation" for public chains, questioning the mainstream approach of valuing public chains using stock valuation models, and suggesting that currency exchange rate models are more useful for valuing public chains. In 2022, Jake Brukhman also proposed that blockchain technology represents a new way of human collaboration, more like a "public good," but with the potential for profit.

Public chains provide a series of foundational services, and any project based on a public chain cannot exist independently. From this perspective, I personally tend to elevate the narrative of public chains from "companies" to "nations." Since we view public chains as nations, it naturally leads to a discussion of the risk-free rate of a "nation," which is the pricing cornerstone of "national" assets.

When we start from a "nation" narrative, the next step is to define currency. A nation's currency is, of course, issued by its "authoritative institution." Mapped onto the blockchain world, the public chain token of a public chain should be considered the currency of that chain. For example, ETH for Ethereum, SOL for Solana, FTM for Fantom, etc.

2. Potential Risk-Free Rates

The risk-free rate excludes credit risk, term risk, etc., and is generally considered to be the short-term government bond rate or the benchmark interest rate set by central banks in the traditional world.

If we break down the nominal risk-free rate, we can see that part of it is price expectations (inflation), and another part is the growth expectations of the economy itself (real interest rate). The well-known Taylor rule for central bank benchmark interest rate pricing indicates that these two factors influence the risk-free rate. Of course, this rate still has some underlying assumptions, such as relative stability of the country and the integrity of regulatory institutions. Therefore, beneath the risk-free rate, there is not absolutely no risk.

Now let's take a look at the main interest rates in the crypto market.

2.1. Stablecoin Lending Rates

Some investors in the market consider the lending rates of stablecoins as the risk-free rate of the crypto market, such as the lending rates of USDC and USDT in Aave and Compound.

However, if we believe that USDC/USDT, which are directly pegged to the US dollar, are not the public chain tokens of the public chain, then from this perspective, they cannot be considered the risk-free rate of the public chain itself.

The price relationship between stablecoins like USDC and the public chain's public chain tokens is more akin to foreign exchange rates, and the interest rates of these two types of currencies resemble the different interest rate levels between offshore dollars and other national currencies.

2.2. Native Token Lending Rates

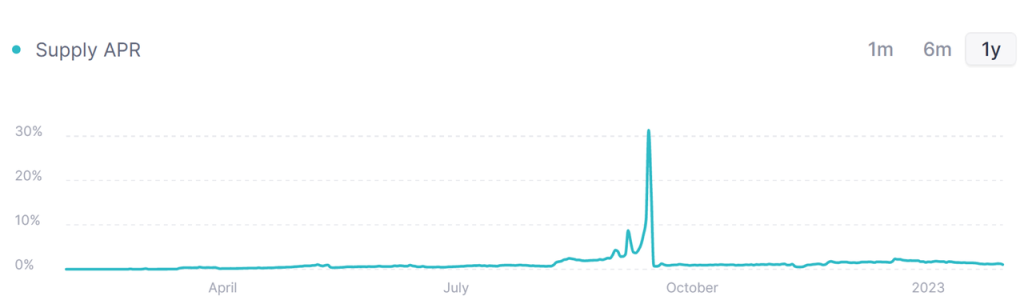

Tokens like ETH and SOL also have corresponding lending pools in lending protocols, and their lending rates are very low most of the time. Taking ETH in Aave as an example, the interest rate level of ETH is generally low.

Source The high rates in the chart occurred during the successful upgrade of ETH2.0.

However, lending public chain tokens carries default risk and liquidity risk. The former is due to issues with the counterparty in the lending transaction (counterparty risk), while the latter is related to overall market risk (market risk), and these risks do not fall under the "risk-free rate." Therefore, these lending rates cannot serve as a benchmark for the "risk-free rate."

2.3. Public Chain POS/POW Yields

Whether through POS or POW mechanisms, a certain reward must be provided to miners/validators to maintain the normal operation of the chain. This yield includes the new issuance of public chain tokens (incentives), which is the inflation of the "national currency," and also relates to the level of activity on the chain.

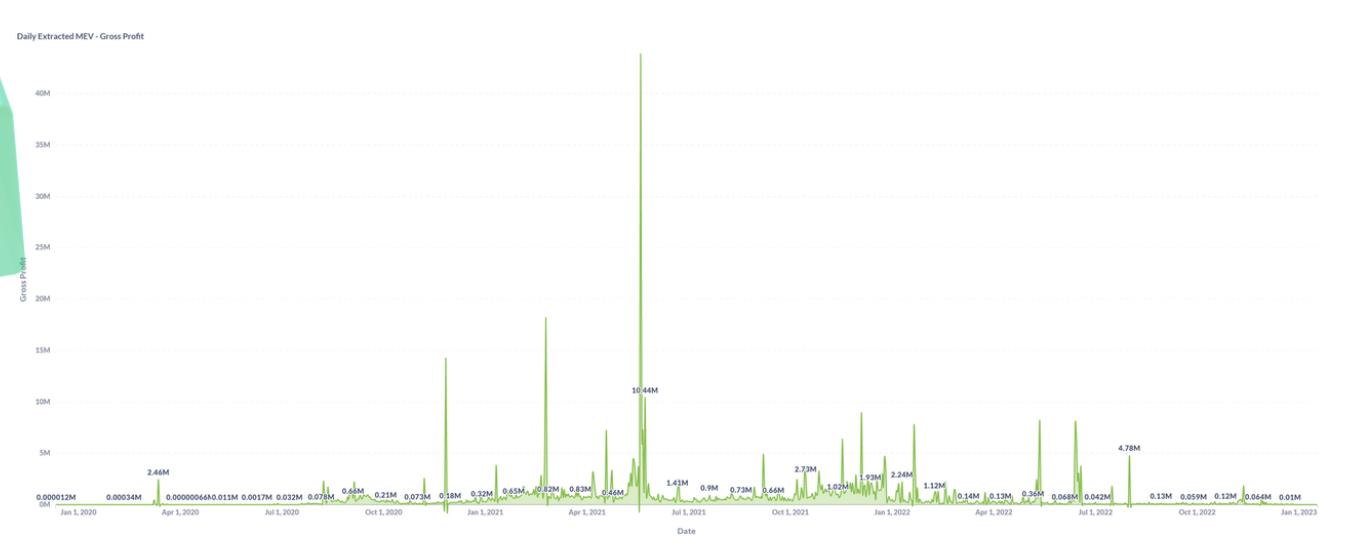

For example, in a POS mechanism, the main sources of MEV are: arbitrage, liquidation, and sandwich attacks, all of which are closely related to the intensity of on-chain activities. From the daily profits of Ethereum MEV, we can also see that MEV is more abundant in bull markets, while it decreases significantly in bear markets.

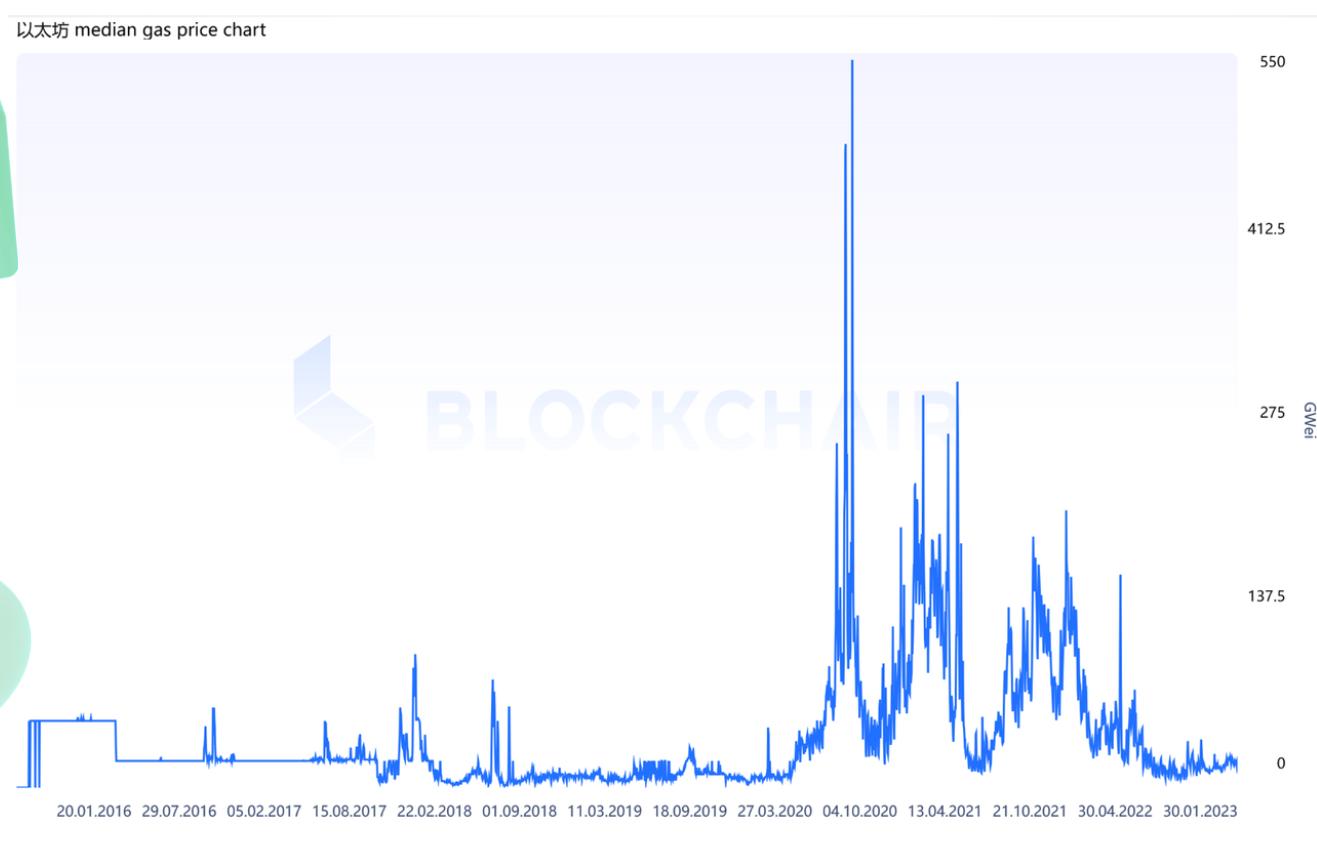

Another relevant metric—the on-chain gas fee—also shows corresponding characteristics.

However, from a risk perspective, is the POS yield completely risk-free? Not necessarily.

To obtain this yield, one must bear hardware, software (client), and network risks, but these risks are necessary to ensure the smooth operation of the public chain. Moreover, the POS yield also includes potential slashing penalties, which remain unavoidable risks in the operation of public chains.

Overall, the yield obtained by miners/validators includes both the inflation of public chain tokens and the yield from on-chain activity levels. Compared to the previous two types of interest rates, the POS yield is more aligned with the "risk-free rate" under the "nation" narrative.

2.4. Understanding Interest Rates of Other Currencies

Some friends may have the question: "I perform many operations on-chain using stablecoins like USDC; why can't I use the stablecoin interest rate as the risk-free rate?"

First, the interest rate of USDC arises from user borrowing behavior, which includes potential default risk and term risk. These risks primarily stem from users' on-chain activities, including possible credit issues with counterparties, which do not align with the "risk-free rate" that only reflects the basic situation of money supply and economic growth.

Secondly, under the "nation" narrative, public chain tokens serve as the local currency of the public chain, while other currencies should be viewed as "foreign exchange." Unlike traditional nations, where a country typically can only conduct daily production and business activities using its own currency with the support of coercive institutions, in the cryptocurrency market, there are no coercive institutions or mechanisms that enforce the exclusive use of public chain tokens for any activities. Thus, public chains appear more like an extremely open "nation," accepting any currency as a payment tool. Therefore, stablecoins and other non-public chain currencies can be seen as "foreign exchange."

3. Basic Use of POS Yields

The risk-free rate provides a perspective for observing the overall status of the "public chain nation," while the real interest rate can assist in judging the maturity of the ecosystem and has certain guiding significance for investment strategies.

Now let's take a look at some POS yields of public chains. Here, we select public chain projects with a TVL of over $100 million, that have POS yields and ongoing inflation. Overall, it presents a situation very similar to the real world: the more mature the economy, the lower the interest rate level provided by the economy.

Next, let's observe the real interest rate levels. The real interest rate level of an economy is mainly related to the potential growth rate, population structure, and asset return differentiation of the economy. Healthy economies generally exhibit positive real interest rates. When mapped to the public chain domain, the "population" can correspond to the number of addresses and active addresses, while "potential growth" can correspond to transaction volume, transaction fees, and the growth rate of deployed contracts.

StakingRewards provides adjusted reward yields, calculated by adjusting for the inflation of network supply. The adjusted reward can represent the real interest rate. From the chart below, we can see that most public chain projects are still in a growth phase.

By simply observing the rankings of POS yields and TVL, it is beneficial to deploy different public chain investment strategies: for conservative investors, they should look for public chain projects with low POS yields and positive actual POS yields as a target pool; for aggressive investors, perhaps projects with a larger risk-reward ratio in public chains with high POS yields and negative actual POS yields.

After discussing the risk-free rate of public chains, it naturally leads us to think about applying the risk-free rate in market pricing. The lending market is well-known, but the bond market has remained lukewarm. In the next article, we will discuss the current state of the bond market and explore the future development direction of the market.

4. References

Exploring the Opportunity for DeFi Interest Rate Markets, Multicoin Capital

Fat Protocols, USV

Price layer 1 blockchain tokens like countries, Tascha Labs

Crypto Networks Are Monetizable Public Goods, Jake Brukhman

Determinants of the real interest rate, European Central Bank