LSD hides "sevenfold benefits," the endgame of APR-War is a 10X growth in TVL

The curse of APR and TVL being mutually exclusive will be broken.

The curse of APR and TVL being mutually exclusive will be broken.Author: shutong, SevenUp DAO

LSD hides "sevenfold returns," and the upcoming APR-War will drive a 10X growth in DeFi TVL, breaking the curse of Ethereum mainnet staking APR and TVL being mutually exclusive.

This article mainly discusses three parts: the first part defines ETH-Staking and four staking methods, the second part explores how the story of high returns from LSD staking continues through seven avenues, and the third part covers some side notes and potential tracks.

1. Definition, Pain Points, and Four Methods of ETH-Staking

1.1 Definition of Staking Mining:

In simple terms, it is mining, but in the context of 2.0, "stakers" replace "miners" in the verification work and earn the right to profits; the biggest barrier is that the fixed cost has shifted from the previous mining machine expenditure to a minimum deposit of 32 ETH.

1.2 Pain Points:

High Costs: There is a minimum investment threshold, and the capital efficiency of staking is low, with long lock-up periods and no withdrawals; additionally, users verifying nodes individually need to maintain good node performance to avoid costs from being offline.

Low Returns: 4% - 6% and in a declining state; although hardware costs are low, they cannot be ignored.

1.3 Four Staking Methods:

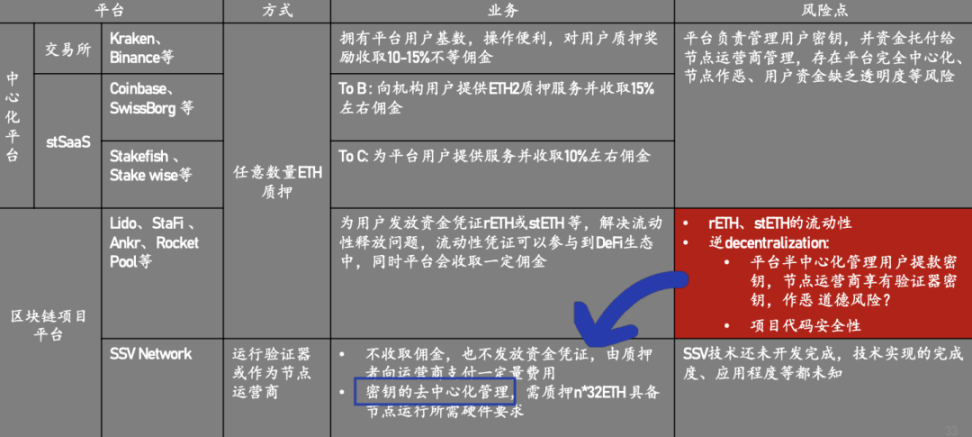

In terms of classification, users will receive two private keys after staking assets on the ETH mainnet— the validation private key (responsible for the verification signature during mainnet node operation) and the withdrawal private key (responsible for the permission to deposit and withdraw from Ethereum staking mainnet). Based on the different ownership of these two private keys, four Staking solutions emerge:

Solo (direct staking), Sass (having 32 ETH for a node to run), Pool (similar to LDO's joint staking solution), CEX (compliant solutions from exchanges like Coinbase).

Image source: Robert. Hu SSV China Ambassador @RobertHuWeb3

From top to bottom, the security and decentralization levels gradually decrease. In the solo method, users have control over both private keys, freely managing profits and node verification status. In the Sass solution, users only have the withdrawal private key, ensuring the safety of funds, while Pool and CEX fall under the category of custodial solutions, where both private keys are handed over. Comparatively, CEX has a higher degree of opacity; at least Pool is relatively "decentralized custody."

Each of the four solutions has its pros and cons, and users mainly consider several dimensions such as fund security, convenience, cost, and yield. Undoubtedly, the Pool solution is a compromise and the most attractive to market attention, as it guarantees returns while lowering the entry barrier for users into LSD, and in a "seemingly decentralized custody" manner, the psychological safety of stakers is compensated.

The current market heavily criticizes the CEX solution, which employs a centralized staking method, often accompanied by inflated or misleading yields, with protocols not disclosing details. Users, lacking the right to know, can easily be "free riders," and unclear rules are often a means for platforms to attract assets. However, as the most direct entry point for staking, the convenience or compliance needs may be the biggest competitors to relatively decentralized staking protocols; otherwise, it wouldn't hold a 30% market share.

2. Can the Narrative of High Returns from ETH Staking Continue?

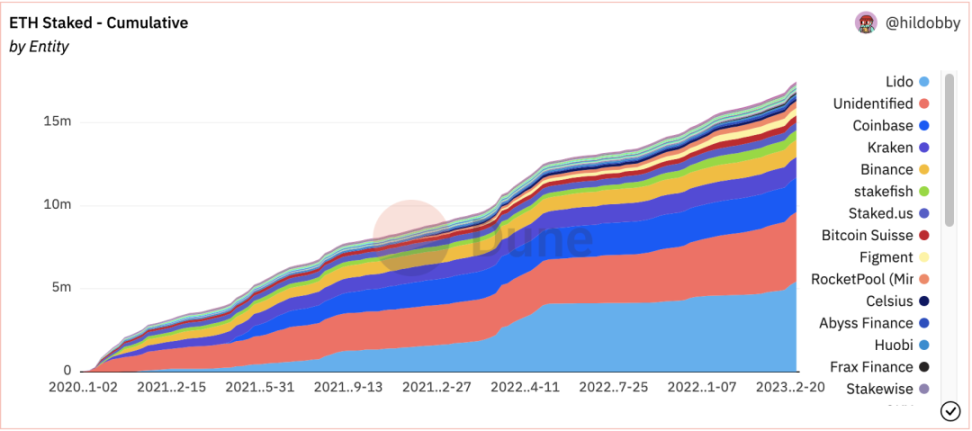

The staking yield of the Ethereum mainnet and the overall locked amount are in a mutually exclusive state. The current staking rate is about 14.6%, and the yield will decrease as the total staking amount increases, leading many in the market to expect a significant drop in yield after the Shanghai upgrade. As a fixed-income product, its competitiveness cannot match that of U.S. Treasury bonds at the same time, suggesting that the LSD market may not have such a large imagination space. Below, we will explain how the yield in the LSD track can be expanded in multiple dimensions based on time and space.

2.1 Time Dimension:

The staking rates of mainstream public chains are generally at 60%+, with Solana at 70% and Bnb at 90%. The ETH Beacon Chain was launched in December 2020, initiating POS staking deposits. After a year of validating nodes working together, the staking rate has only risen to less than 15%. Therefore, the increase in validating nodes and staking rates is not instantaneous; it requires a game between the market and miners.

According to the current rules of the staking mainnet, approximately 50,000 new Ethereum can enter contracts daily, and without large withdrawals, it would take a year to increase the share by 15%. Thus, LSD yields will not plummet suddenly but will maintain a certain level over a longer period.

During this interim period, various leveraged tools derived from LSD will boost yields, and even subsidies from external tracks will flow into LSD, thus offsetting the decline in yields due to the increase in mainnet staking rates.

2.2 Space Dimension: The Initial Signs of LSD APR-War

Ⅰ. Circular Lending and Staking

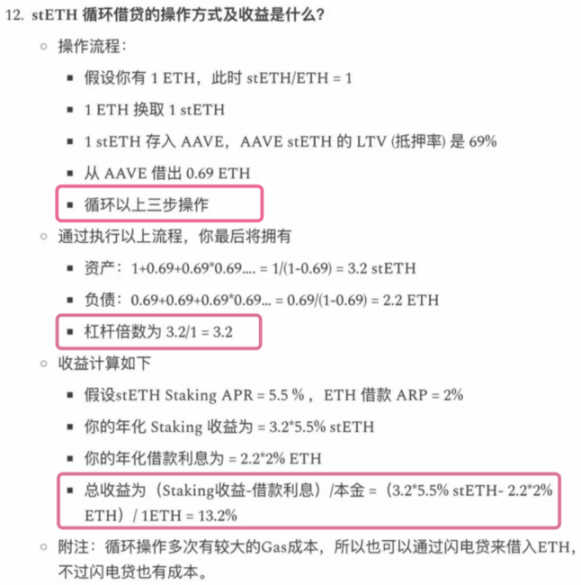

The current methods for expanding returns in the LSD track mainly focus on two approaches: one is to leverage stETH through circular lending, which can yield a 3X leverage and a 13% return if borrowing costs are not considered. This has a significant premium over Treasury yields, and the time needed to smooth out the interest rate spread must also be considered;

Additionally, through Aave V3's efficient model, circular staking can leverage up to 10x, and yields will also expand accordingly. However, it is worth noting that, on one hand, this incurs high borrowing costs, and on the other hand, excessive leverage can hinder exits. The false liquidity in the circular lending market, where $100 million in liquidity may only be backed by assets worth $2,000, makes the process of leveraging easy, but a rush to de-leverage can quickly deplete liquidity.

Ⅱ. External Subsidies from Established DeFi Protocols

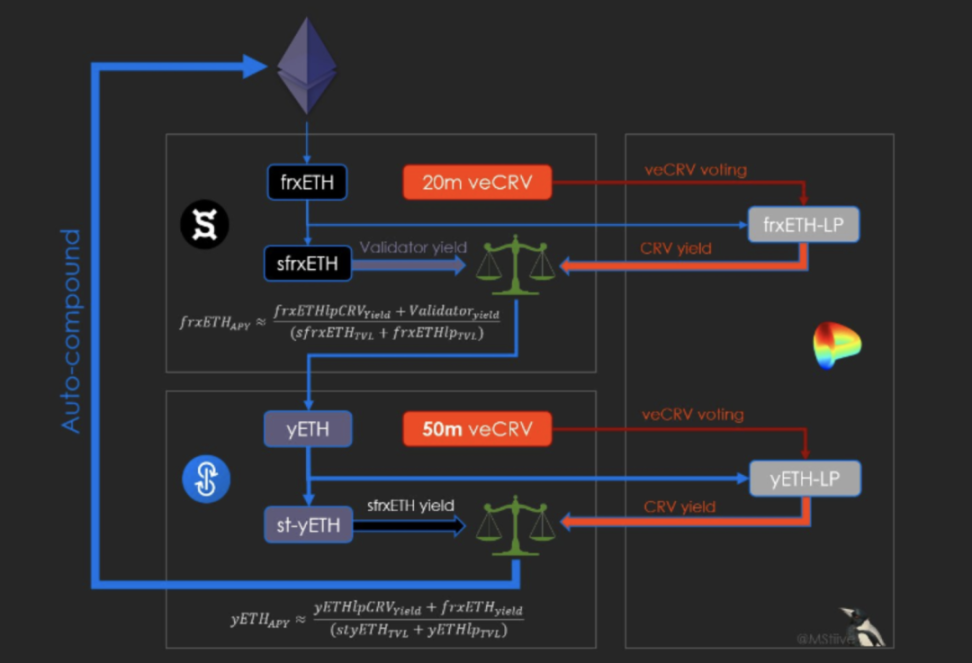

Without leveraging, there are also established DeFi protocols like FXS and YFI that hold a large amount of veCRV votes, manipulating the voting process to change the intensity of curve LP emission yields. Essentially, this subsidizes the returns of LSD stakers through external subsidies, and serves as a core means to enter the LSD track.

In fact, it is a very wise move for these established protocols to enter the LSD track from DeFi protocols. On one hand, the resources accumulated in early DeFi can be repurposed, and entering the LSD track is akin to starting with a good hand.

On the other hand, established DeFi protocols are facing growth bottlenecks; YFI has been in a continuous outflow state since November 2021, dropping from a peak of $5 billion to around $400 million currently. Recently, FXS has positioned LSD as a new outlet for accommodating funds, with TVL rapidly increasing from $1.2 billion to $1.5 billion.

After LDO became the largest locked protocol, it can be expected that established DeFi protocols will find ways to enter the LSD track to share the pie, and in a situation where protocol token distribution has been exhausted, they can only attract external subsidies to draw in funds and push TVL back up.

However, the subsequent returns may also be substantial. For example, FXS's stablecoin strategy, after absorbing a large amount of ETH to mint frxETH, may develop into an lsdETH-USD stablecoin strategy, adding a layer of asset creation. This will become a key focus for various DeFi protocols, transitioning from simply stacking lsd-TVL to the process of APR War and nested leverage.

Ⅲ. New Protocol Token Mining Rewards

For new LSD protocols, their unexploited economic models are their greatest advantage, directly attracting funds through token incentives to initiate a "vampire attack" on established protocols. Who knows, we might see an LSD mining Summer? Similar to Aura Finance backed by Balancer's liquidity support, it may also become a dark horse.

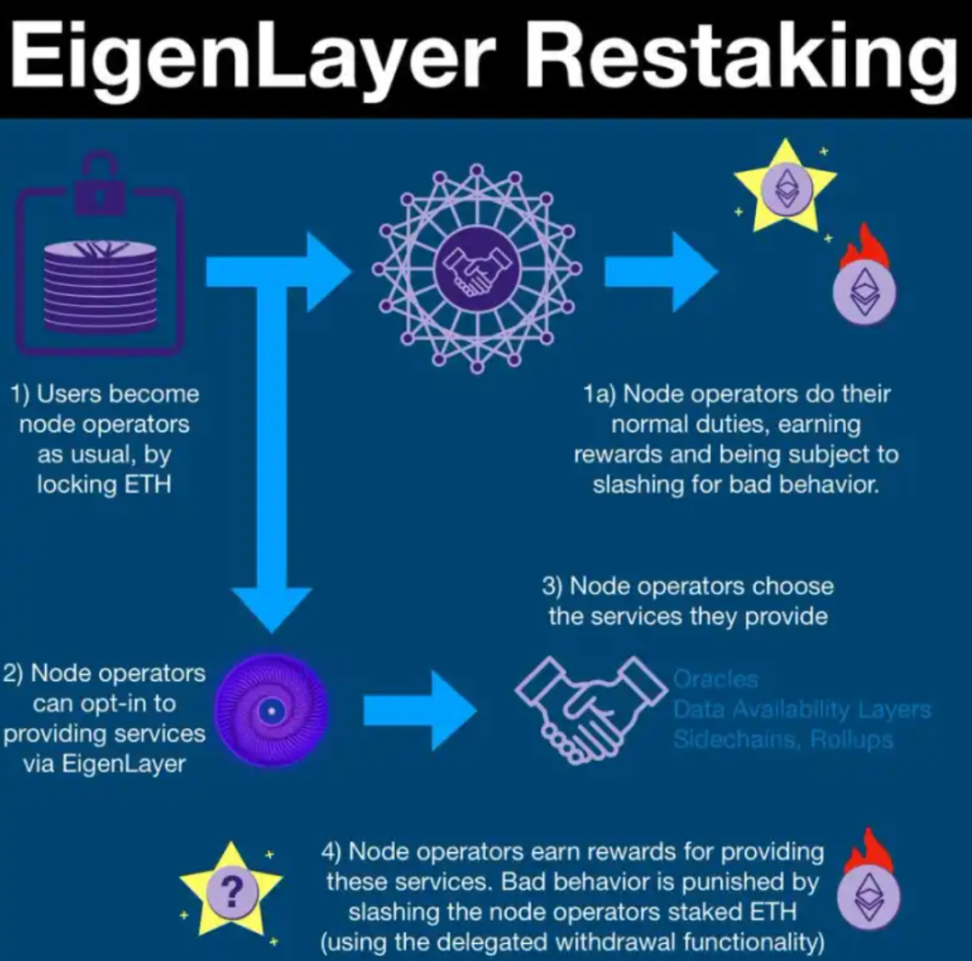

Ⅳ. The Real Returns of Re-staking Solutions

In the future, Eigenlayer will serve as an expansion solution for the ETH consensus layer. Through the re-staking solution proposed by Eigenlayer, LSD liquidity tokens can earn returns not only from ETH itself but also from nodes in other cross-chain bridges and oracles. If LP staking for lsdETH is launched subsequently, it can achieve a threefold return.

① Staking Ethereum Returns

② Token rewards for nodes built and verified by partner projects

③ Liquidity Token staking rewards from DeFi LPs

Ⅴ. Introducing Liquidity Income from lsdETH Trading Pairs on Dex

Currently, most trading pairs on DEX are primarily ETH and USDX. In the future, as the staking rate of ETH on the mainnet increases, the amount of ETH in the market will decrease, and its liquidity will inevitably decline. In its place, the share of lsdETH will expand on DEX, thus, under the premise of ETH trading pairs gradually weakening, more assets will be incentivized to use lsdETH as an anchor asset, providing LSD users with an additional layer of trading pair and liquidity income.

Ⅵ. "Fixed Income +" Financial Product Yields Will Rise Further

ETH-Staking yields will represent the "risk-free rate" of the crypto ecosystem, much like the position of Treasury yields in traditional financial markets.

Fixed income products such as deposits and Treasury bonds are the largest scale in the traditional financial market, and the derived "Fixed Income +" products also have a scale of several billion dollars. "Fixed Income +" is an investment strategy that increases the return rate while ensuring capital preservation. In the crypto world, this means depositing user principal into stable fixed income, i.e., POS staking, while allocating a small portion of funds (the part that can be compensated by yields) into high-risk assets such as synthetic assets, cryptocurrencies, index funds, and quantitative strategies to seek higher returns.

Summary

Therefore, there is no need to be pessimistic about the overall yield level of the future LSD track; the yield models are diversified and have "partially combinable characteristics."

The first part provides a guaranteed "fixed income" from mainnet staking, the second part expands yields through circular lending in DeFi, the third part offers liquidity income from lsdETH/ETH LP on DEX, the fourth part anticipates the incentive yields from the "hundred regiments war" of LSD protocols (established DeFi protocols manipulating votes to increase incentive caps, while new protocols mine governance token emissions, similar to the early LDO), the fifth part grants additional rewards from third-party project validation nodes through re-staking protocols represented by Eigenlayer, the sixth part comes from liquidity incentive income introduced by DEX trading pairs (lsdETH/some token), and the seventh part involves yield aggregators reinvesting mining rewards into high-yield financial products, creating a "Fixed Income +" market.

Although the above seven types of yields cannot be completely stacked, they can expand yields through "partial stacking combinations."

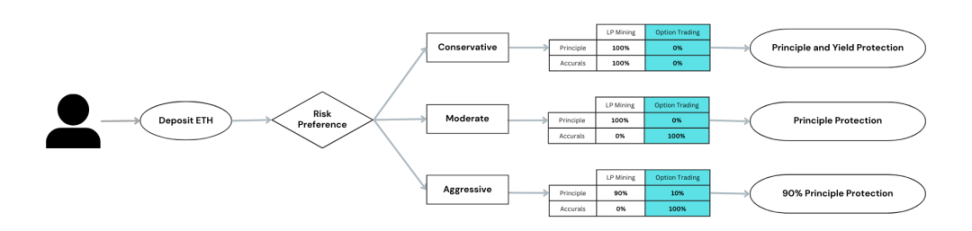

For example, one of the strategies employed by the LSD yield aggregator protocol Shield is for stakers to deposit half of their ETH into LDO, earning mainnet **① node validation rewards while receiving liquid staking tokens stETH, then using the remaining half of ETH to form an stETH/ETH LP deposited in Curve to earn **② platform liquidity rewards and **③ Curve incentive rewards. This can increase the pure staking yield by 20-30%; additionally, if users want to achieve higher yields, Shield will use part of the returns **④ to purchase options that anchor ETH prices to gain price appreciation, making it a "Fixed Income +" product in the crypto world.

In conclusion, from a temporal perspective, the rate of POS staking will delay the possibility of a sharp drop in yields. The time window formed during this period will provide more innovative gameplay for the LSD track, increasing locked amounts while expanding the yield and liquidity of staking assets, and the combined financial attributes will break the curse of TVL and APR being mutually exclusive in the LSD track.

The following will discuss the direction of Alpha, without involving specific targets.

3. Some Side Notes

Ⅰ. Is there still a necessity for the lsdETH protocol after the Shanghai upgrade?

We can return to the user's purpose for conducting liquid staking on Ethereum, which is primarily threefold: threshold, liquidity, and financial attributes.

The Shanghai upgrade mainly optimizes the process for withdrawals and staking reward extractions, addressing liquidity needs. The potential for higher yields is more focused on large holders, while lowering staking thresholds and convenience is more valued by retail investors. Increasing the financial attributes and leverage scale of lsdETH is what the protocol parties focus on.

Therefore, the lsdETH protocol will not only exist but will also face fierce competition. If lsdETH becomes more commonly used and circulated compared to native ETH in the future, it would not be surprising.

Ⅱ. Which LSD tracks can be focused on in the future?

The value discovery of a certain track generally follows a process of gradual diffusion from midstream to upstream and downstream. For example, decentralized staking protocols like LDO focus more on the midstream track, but the midstream track is also the first to be discovered for value, and the current valuation level (P/F≈10X) can already match UNI.

Additionally, the midstream of LSD currently has limited yield stock (with a daily production cap of 1,500), and it is a red ocean track, with numerous new and established DeFi protocols competing for the market with external subsidies and token incentives, while exchanges and compliant tracks are also eyeing it.

Therefore, future deeper value discovery in the midstream will rely on the increase in TVL staking rates after the Shanghai upgrade and related protocols such as Re-Staking, DVT, and DeFi protocols building on Lego, using leverage to compensate for insufficient yields.

The upstream track of LSD is most directly related to DVT-related technology protocols.

- Narrative Aspect: DVT technology is an essential part of ETH ecosystem security, originating from the technical debt formed after the Merge to POS, and DVT was proposed by the Ethereum Foundation, just separated out for individual focus. DVT and ETH can be said to be interdependent, and B2B business has greater market barriers and technological accumulation.

- Ecological Aspect: Short-term specialized competitive solutions, long-term development into industry standards. After sufficient market education (SEC, Kraken, Coinbase, etc.), the importance of anti-regulation and anti-censorship will gradually be recognized. Many DVT protocols have not yet launched on the mainnet, which remains an advantage.

The downstream track mainly consists of some yield aggregators and re-staking protocols that have not yet launched.

Yield aggregators are the most direct entry point for LSD staking, and high yields are the most straightforward way to capture user attention. As mentioned earlier, there will definitely be an APR War in the LSD track, which is also the opportunity for yield aggregators.

Most importantly, the projects that lead the industry to its shining moments are often those that the market did not anticipate. New gameplay combined with the Shanghai upgrade will add a touch of brilliance to LSD.