U.S. regulators are challenging leading platforms, is the landscape of the Ethereum LSD track changing?

The fixed currency market may integrate into blue chips like Tether and USDC, or another possibility is the rise of decentralized stablecoins like DAI.

The fixed currency market may integrate into blue chips like Tether and USDC, or another possibility is the rise of decentralized stablecoins like DAI.Author: Terry, Plain Language Blockchain

On February 9, Coinbase co-founder and CEO Brian Armstrong tweeted, "We are hearing rumors that the SEC wants to eliminate crypto asset staking services for retail customers in the U.S. I hope this is not the case, as I believe allowing this to happen would be a terrible path for the U.S."

The next day, Kraken announced the termination of its crypto asset staking services for U.S. users and agreed to pay $30 million to settle SEC charges regarding the offering of unregistered securities. This has sparked significant interest in the increasingly important crypto sector of ETH liquid staking.

01 Dominance of Lido, Lagging Centralized Institutions

As of the time of writing, the total amount of staked Ethereum on the Beacon Chain has surpassed 16.5 million ETH, accounting for nearly 14% of the total ETH supply.

Source: dune

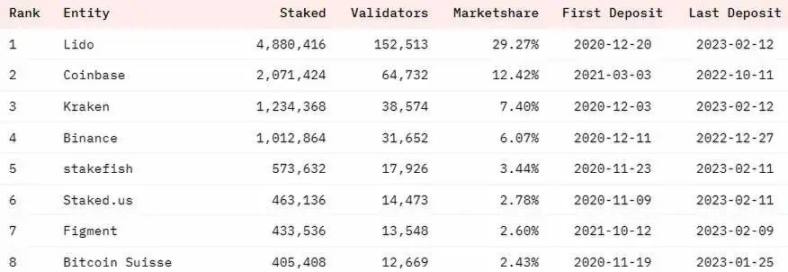

Meanwhile, among the staked ETH, the top eight ETH staking service providers hold 66% of the market share, indicating a clear head effect.

Lido Finance stands out with approximately 4.88 million ETH staked, capturing nearly 30% (29.27%) of the market share, which is equivalent to the combined total of the second to fifth places.

Source: dune

The second to fifth places include centralized exchanges like Coinbase, Kraken, and Binance, as well as stakefish, all of which are centralized staking service providers. Their advantage lies in one-click, user-friendly staking without the need for at least 32 ETH, while also providing liquidity through centralized guarantees.

However, even Coinbase, which follows closely behind, holds only 12.42% of the market share, less than half of Lido's. Notably, data shows that Coinbase seems to have temporarily suspended its ETH staking service since October of last year.

Previously, Coinbase's Q3 2022 revenue report indicated that its staking revenue reached $62.8 million, accounting for about 11% of its net revenue ($580 million), a continuous increase from 8.5% in Q2.

This highlights the importance of staking services for centralized exchanges in terms of business: in the context of a sluggish market, staking has become one of the more stable sources of revenue.

Currently, Kraken has staked approximately 1.2337 million ETH, accounting for 7.42% of the total staked ETH, ranking just behind Lido and Coinbase. However, like other centralized institutions such as Binance and stakefish, its market share is still significantly lower than Lido Finance's 29%.

Due to the SEC's strong actions, it is foreseeable that with the suspension of Kraken's staking services, ETH will continue to flow towards Lido Finance among centralized institutions.

Overall, decentralized ETH staking protocols represented by Lido Finance not only hold an absolute advantage over centralized institutions in the current landscape but are also expected to see an accelerated outflow of staked ETH from some centralized institutions due to the SEC's regulatory impact in the short term.

02 Extremely Uneven Decentralized Liquid Staking

So within decentralized liquid staking protocols, besides Lido Finance's dominance, are there any other noteworthy new trends or projects?

Almost none.

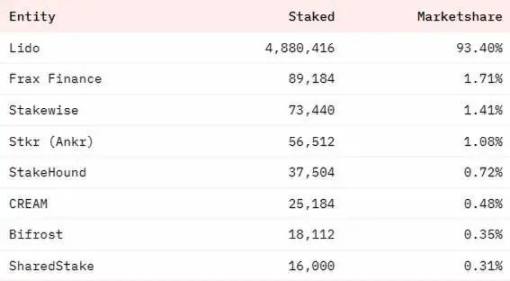

If we isolate the data for decentralized ETH liquid staking (RocketPool has nearly 400,000 ETH), Lido Finance alone occupies 93.4% of the market share.

Frax Finance and others hold less than Lido's fractional share. More critically, Lido's stETH has already weathered multiple panics and sell-offs, including the Three Arrows Capital incident last year, giving it a clear first-mover advantage in the ETH/stETH LP pool on Curve and L2 expansions.

However, it is worth noting that Frax Finance's newly launched Ethereum liquid staking product, frxETH, has seen rapid growth—since its launch on October 21, 2022, frxETH has grown from 0 to approximately 90,000 ETH, quickly rising in prominence.

This remarkable growth is driven by its average staking yield of 8% over the past two months, which even peaked above 16% (while Lido's was around 5% during the same period):

This is mainly due to Frax being the largest holder of CVX, allowing it to leverage substantial exchange rate impacts to influence Curve's reward distribution, thus achieving high yields in the frxETH/ETH liquidity pool on Curve.

This has been key to Frax's miraculous performance over the past four months. Whether frxETH can become an outlier in the Ethereum liquid staking space and whether other decentralized ETH liquid staking services can capitalize on the constraints faced by centralized institutions remains to be seen.

03 What is the Impact on Ethereum Staking?

It is still unclear whether the SEC will impose a complete ban on crypto asset staking services by centralized institutions, which also raises the question of whether the SEC has the authority to enforce such a ban—Is ETH a security?

If not, then the SEC does not have sufficient jurisdiction to act unilaterally (the SEC has also been quite busy lately), and the pace of legislative and regulatory progress will not be swift. Other relevant regulatory bodies, such as the CFTC, have also been seeking to gain enforcement authority over the crypto market.

Coinbase's Chief Legal Officer Paul Grewal stated that according to the Securities Act and the Howey test, Coinbase's staking services are not securities, and the SEC's enforcement action against Kraken could severely damage the development of the U.S. crypto industry.

Indeed, under Gary Gensler's leadership, the SEC has been quite active in the field of crypto regulation in recent years. However, based on historical experience, once a project is targeted by the SEC, even if it involves securities attributes, it is not without resolution:

On September 23, 2019, the SEC reached a settlement with Block.one (the company behind EOS), where Block.one agreed to pay a $24 million civil penalty to resolve SEC charges regarding its unregistered token offering, while also granting it significant exemptions for future business.

This also provides a perspective for many projects facing similar accusations—maintain a proactive attitude and accept penalties to move forward.

As the Shanghai upgrade, scheduled for March 2023 (which may change), approaches, if the upgrade successfully initiates the process for Ethereum stakers to withdraw their staked ETH, it would be a long-term positive for the entire industry.

On this basis, if in the future the SEC and other regulatory bodies truly impose strict limitations on centralized institutions' liquid staking services, it would only allow decentralized staking protocols to gain a larger share of staked assets:

After all, companies as entities are easier to regulate, while protocols are not so straightforward. Lido Finance is unlikely to comply with securities regulations like a centralized entity registered in the U.S. such as Coinbase, allowing it to seize opportunities from Kraken and others in the market. A significant portion of future staking increases may likely shift towards liquid staking protocols like Lido.