Dragonfly Capital researcher: NFT trading is becoming homogenized, and the road to efficiency is still long

Even though NFTs themselves are non-fungible assets, NFT transactions are becoming more homogeneous than ever.

Even though NFTs themselves are non-fungible assets, NFT transactions are becoming more homogeneous than ever.Written by: Celia Wan, Researcher at Dragonfly Capital

Compiled by: The Way of DeFi

For almost any non-fungible asset class, sellers are the price makers.

Take houses as an example: home buyers typically can only decide whether to reject an offer. Sellers decide what to sell (provide liquidity), at what price to sell (pricing), and what discounts they can offer.

A typical seller-dominated market is non-fungible assets, which at first glance seem no different. In the NFT market, sellers provide liquidity to the market by listing and determine market prices by setting a floor price.

However, despite the similarities, NFT sellers are on a different liquidity path. They increasingly rely on buyer interest to gain immediate liquidity, and their asking prices (floor prices) are no longer the sole indicator of collectible value. Even if NFTs themselves are non-fungible assets, NFT trading is becoming more homogeneous than ever.

A Liquid Market (Around the Floor Price)

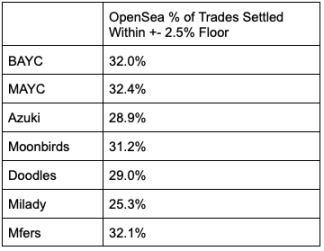

The most direct evidence of the homogenization of NFT trading is the growing demand for floor price NFTs. Some even argue that NFTs are merely "sham coins in the form of images." In fact, when we compare settlement prices on OpenSea with floor prices, we find that a significant portion of trades occur around the floor price.

Source: Reservoir data, April 30, 2022 - January 15, 2023

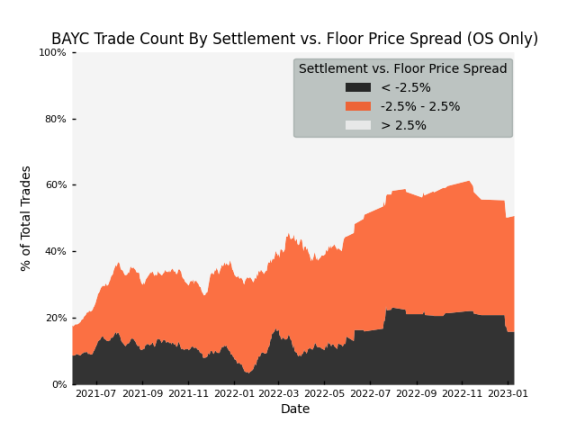

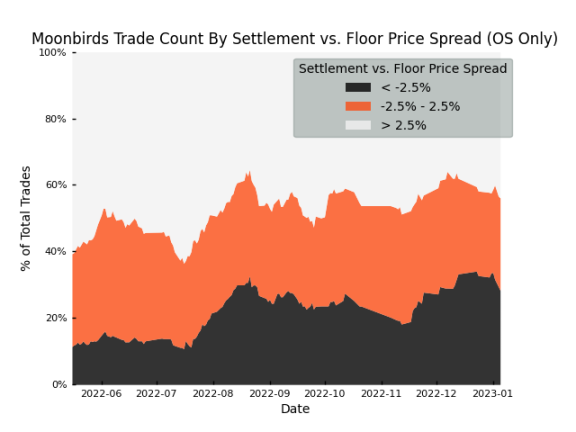

This indicates that it is a fairly liquid market, with trades of floor price NFTs occurring as if they were fungible. Popular collections, including BAYC, Moonbirds, and Doodles, will see more trades occurring around the floor price as the collections mature. In some cases, such as BAYC, daily sales at or below the floor price may account for over 50% of the series' trades.

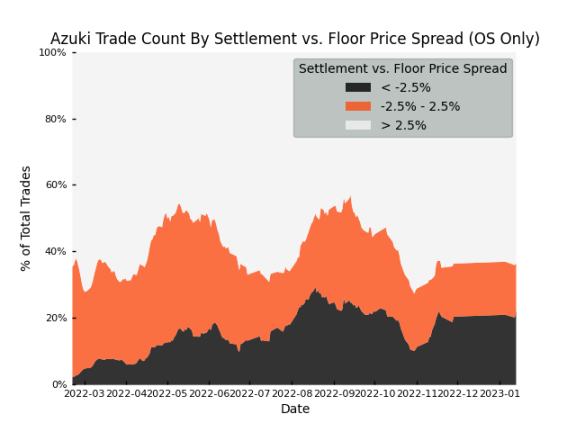

Of course, not every collection follows the same trend. Some collections, like Azuki, have relatively stable historical floor price sales, as shown in the chart below. However, even with fewer trades near the floor price, the number of trades settling below that price is still increasing.

Source: SPICYEST, Reservoir

This is an interesting phenomenon worth noting. By definition, the floor price is the best offer in the market. It is an indicator of what sellers believe to be the lowest equilibrium point in the market. Whenever a new NFT is listed at a lower price, the floor price changes, and the only way to trade below the floor price is for sellers to actively accept existing bids below the floor price.

For example, if 10% of trades settle below the floor price, it means that 10% of all trades are sellers actively accepting trades lower than the market's best offer. This often occurs when sellers want to quickly liquidate their positions, thus paying a premium for the time saved by accepting offers below the floor price.

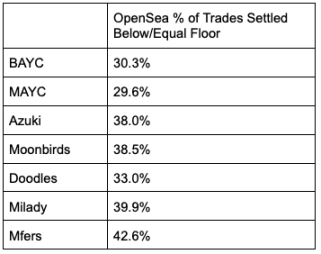

Source: Reservoir data, April 30, 2022 - January 15, 2023

From April 30, 2022, to January 15, 2023, approximately 30% to 45% of OpenSea sales in the seven collections we tracked settled below the floor price. In other words, at least 30% to 45% of trades are being market-made by buyers for sellers, rather than the other way around. This does not include sales of non-floor price NFTs, where sellers can accept offers above the floor price.

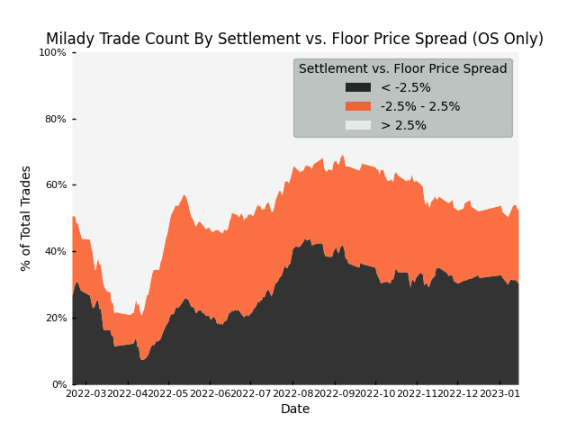

Moreover, the trend of trading below the floor price is also on the rise. For instance, since April 30, 2021, 21.1% of BAYC trades settled below the floor price, while this figure surged to 30.3% for all trades since April 30, 2022. As shown in the chart above, other collections like MAYC, Doodles, and Moonbirds also exhibit the same trend.

So, why are more sellers becoming market acceptors over time? Part of the reason may be the deterioration of market conditions since early 2022. When the market is down, NFT holders tend to quickly liquidate their positions, thus accepting higher discounts below the floor price.

This may also indicate that the pricing dynamics between buyers and sellers have changed over the lifecycle of the collection. As mentioned earlier, sellers of non-fungible assets are typically price makers because they have more insight into the market. This is especially true in markets like housing or art, where there is a wide range of assets and structural opacity creates significant information asymmetry between buyers and sellers, allowing sellers to continuously dictate pricing.

However, in NFT trading, this information gap is virtually non-existent. All transaction and order data is either on-chain or can be obtained through open market platforms. Even if NFT holders, as the initial liquidity providers, do have more say in pricing at the launch of a collection, the liquidity advantage quickly diminishes as other parts of the market catch up. The existence of public markets also ensures that new buyers can enter the market without barriers, providing sustainable buyer interest for the market. Therefore, NFT collections, especially blue chips, can have a relatively balanced two-sided market, with liquidity flowing from both ends. This distinguishes NFTs from other non-fungible assets—they are non-fungible assets with homogeneous trading characteristics.

The Long Road to Efficiency

Although the NFT market is becoming more balanced, there are still many challenges before it truly becomes efficient.

As market equilibrium no longer leans towards sellers, the signals contained in the floor price have also diminished, and it is no longer a good indicator of market sentiment. However, until recently, the floor price has been the only price-related indicator displayed in the market, making it difficult for traders to accurately understand the market.

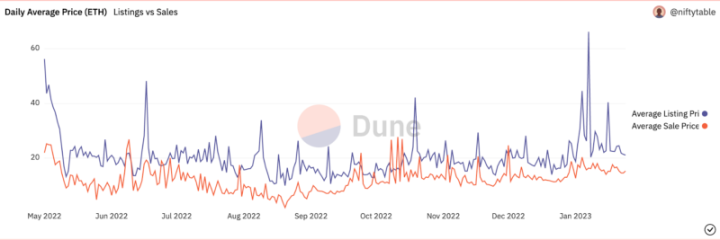

By comparing settlement prices and floor prices, we can see that there is a persistent price gap between the two. Here, "average sale price" is defined as the average settlement price of the bottom 5% of all trades, while "listing price" refers to the floor price. In the chart, Azuki's realized floor price is consistently much lower than the listed floor price. It is clear that the floor price alone does not reflect the true market value of the collection.

Source: Dune

However, the problem does not end there. The price gap between bids and asks can be further widened by various fees that sellers must pay. In recent months, the NFT fee war has been a widely discussed topic, and it does not seem to be calming down anytime soon. On one hand, some collections and markets blacklist those that do not honor royalties. On the other hand, market platforms like Sudoswap and Blur are racing towards zero fees.

This situation makes trading particularly confusing for sellers. When setting a floor price, sellers often have to consider fees to make their trades worthwhile. For example, market platforms like OpenSea charge sellers a 2.5% platform fee on all trades, in addition to which collections typically charge additional royalties ranging from 2.5% to 10%. This creates significant market friction for participants, especially for frequent traders who are sensitive to fees. For less mature sellers, high fees can sometimes lead them to completely abandon providing liquidity to the market.

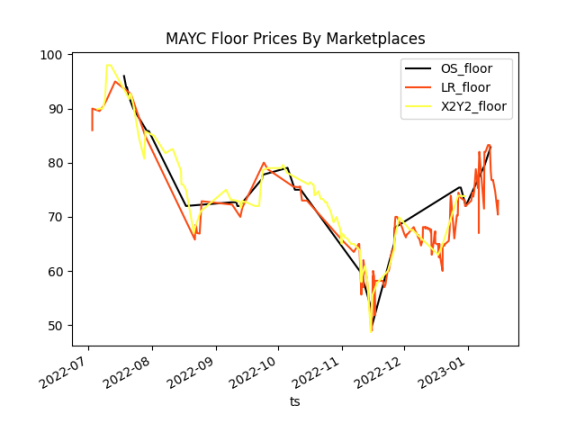

The impact of fees is also reflected in the different floor prices displayed for the same collection across markets. Exchanges for fungible tokens typically provide very tight quotes, differing by just a few cents. This is true for both centralized and decentralized exchanges. However, in NFTs, this price gap is much larger. Because different markets have different fee structures, their floor prices also differ, making price discovery challenging. High fees also deter market makers from arbitraging, leaving price gaps.

Source: SPICYEST, Reservoir

Aggregators partially solve this problem by providing users with a panoramic view of the market, but even this solution faces resistance. Some new collections, like Sewer Pass, prohibit markets that do not respect royalties, while OpenSea operates a blacklist to help creators prevent certain markets from trading their collections.

At its core, the fee war is a struggle between a nascent market hoping to become more efficient and new enterprises (collections) seeking viable monetization pathways. Zero fees encourage market participation and lead to competitive pricing and better price discovery. Meanwhile, charging royalties can incentivize creators to continuously contribute to the NFT market, ensuring its long-term prosperity.

Predicting the outcome of this war is difficult. However, one thing is certain—NFTs are on an irreversible path, trading more like fungible tokens. Although the road ahead is bumpy, the market will ultimately trend towards efficiency.

Acknowledgments: @karimhelmy, @hildobby_, @tomschmidt, @0xkofi, @0xDiplomat, @kadin256

Special thanks to SPICYEST for their help and insights into understanding the NFT market and data.

Note:

Floor price data does not include Blur, but trade data does.

The comparison of floor price and settlement price is only for OpenSea. The results may vary when comparing prices across the full range.

Reservoir does not have complete historical floor price data, so some data comes from SPICYEST's API.