Coin Meng Research - BendDAO (BEND)

With the development of the NFT market, using lending tools to unlock the liquidity of NFTs will become a necessity. As a leader in the field, BendDAO has a circulating market value in the tens of millions of dollars and enormous potential for growth.

With the development of the NFT market, using lending tools to unlock the liquidity of NFTs will become a necessity. As a leader in the field, BendDAO has a circulating market value in the tens of millions of dollars and enormous potential for growth.Source: 0xCike, TokenMore

01 Project Overview

BendDAO is an NFT collateral lending protocol that adopts a peer-to-pool model, allowing users to mortgage their blue-chip NFTs to obtain loans, thereby liberating the liquidity of NFTs. At the same time, BendDAO, with lending at its core, has also launched two additional features: collateral sale and down payment for purchasing NFTs.

02 Product Design

Lending Model

NFTs, like real estate, have relatively poor liquidity. To reasonably release the liquidity of existing NFTs, NFT lending applications have emerged. Similar to DeFi lending platforms like Aave, NFT lending also utilizes over-collateralization to withdraw part of the liquidity. Currently, mainstream NFT collateral lending protocols are mainly divided into two models: peer-to-peer and peer-to-pool.

The peer-to-peer model is led by NFTfi, and X2Y2's NFT lending is also peer-to-peer, meaning that lending occurs one-on-one between users, with the platform merely acting as an intermediary. This model has the following characteristics:

Low efficiency: Matching between lenders and borrowers may take a long time.

Accurate valuation: NFTs with different attributes in the same series have different values. The lending parties can negotiate and determine the valuation (and how much can be lent) based on the attributes of a single NFT, rather than using the floor price of the entire NFT series as the sole valuation standard.

High security: If an individual defaults, it only affects the two parties involved in that loan, without expanding the risk exposure to other users on the platform.

Summary: The peer-to-peer model is more suitable for liquidity-scarce bear markets, as it is not afraid of extreme market conditions affecting the platform's security.

The peer-to-pool model is led by BendDAO, where borrowers interact directly with the platform's loan pool, using NFTs as collateral to borrow ETH from the loan pool. When the price of the mortgaged NFT falls to a certain level, liquidation will be triggered. The ETH in the loan pool comes from deposits made by depositors, who, as liquidity providers for the platform, can earn interest income. This model has the following characteristics:

High efficiency: Direct interaction with the pool allows for borrowing at any time.

Inaccurate valuation: The platform cannot conduct detailed collateral valuations based on the attributes of each NFT, and can only determine the valuation based on the floor price of that series of NFTs. The loan amount available for mortgaging any NFT with the same attributes in the same series is the same.

Security risks: Each loan on the platform affects the interests of all depositors. In extreme cases, a large number of NFT liquidations may trigger systemic risks.

Few supported NFT series for collateral: For security reasons, only blue-chip NFTs with high trading volumes, good liquidity, and relatively stable prices are supported as collateral.

Summary: The peer-to-pool model is more suitable for liquidity-rich bull markets.

Borrowing Rules

The BendDAO platform supports the collateral lending of seven blue-chip NFTs: BAYC, MAYC, CryptoPunks, Azuki, Moonbirds, Doodles, and CloneX.

After borrowers mortgage their NFTs, the amount of ETH they can borrow is related to the floor price of that NFT series and the collateral ratio set by the platform. For example, if the current floor price of BAYC is 80 ETH and the collateral ratio is 60%, then mortgaging 1 BAYC NFT can yield a maximum loan of 48 ETH.

Currently, the collateral ratios for various NFT series are as follows:

CryptoPunks: 60%

BAYC: 60%

MAYC: 50%

Others: 30%

The floor price data for NFTs is obtained through the Bend oracle, which is developed in collaboration with Chainlink. The original data for the oracle comes from the floor prices of Opensea, X2Y2, and LooksRare, while filtering the original data to calculate low prices based on the trading volume of each platform, using TWAP (Time Weighted Average Price) to ensure that the data is not manipulated.

Liquidation Rules

BendDAO introduces a health factor as an evaluation metric for account security, calculated as follows:

Health Factor = (Floor Price * Liquidation Threshold) / (Loan Principal + Interest)

The liquidation threshold is currently set at 70%. When the health factor falls below 1, meaning that the total debt principal and interest has reached 70% of the collateral's floor price, liquidation will be triggered. The liquidation process involves a 4-hour auction of the mortgaged NFT, where bidders (liquidators) must bid more than the total debt principal and interest.

If the borrower repays the loan during the auction, the liquidation will stop, but the borrower must pay a penalty to the liquidator, which is either 5% of the total debt or 0.2 ETH (whichever is higher).

Collateral Sale

In mainstream NFT markets, selling NFTs as a buyer is not instantaneous (unless accepting offers below the floor price) and requires waiting for a buyer to make a purchase. In BendDAO, users can deposit NFTs as collateral into BendDAO and then sell them, receiving up to 60% of the floor price in ETH immediately, which is essentially a prepayment from future buyers, still fundamentally a loan secured by the NFT.

Once the transaction is completed, the seller will receive: Total sale price of the NFT - Debt principal and interest (prepayment principal + interest).

Down Payment for Purchasing NFTs

When buyers want to purchase a certain NFT but lack sufficient funds, they can use BendDAO to make a minimum down payment of 40%, with the remaining amount covered by Aave's flash loan. The purchased NFT is mortgaged in BendDAO, and users can release the collateral after repaying the loan principal and interest or can sell it at any time.

boundNFT

boundNFT is the debt NFT of BendDAO. When users mortgage NFTs, they can receive boundNFT (for example, mortgaging BAYC to receive boundBAYC), which has the same metadata and ID as the original mortgaged NFT and carries the same rights. It can be used as a PFP on social media, for claiming airdrops (for example, previously holding BAYC to claim Otherside airdrops), or to earn rewards on other protocols. boundNFT is non-transferable, protecting users from hacking.

03 Bend Ape Staking

In December 2022, Yuga Labs launched the Ape ecosystem Staking incentives, allowing users to stake APE tokens, BAYC/MAYC/BAKC to earn APE rewards. APE can be staked independently, while BAYC or MAYC must be paired with APE tokens to stake, and BAKC must be paired with either BAYC or MAYC along with APE tokens to stake. In the same month, BendDAO launched the Ape Staking service to assist users in peer-to-peer pairing.

Holders of BAYC or MAYC can publish pairing requests on BendDAO to match with APE token and BAKC holders to jointly earn staking rewards. When publishing requests, they need to set the minimum staking amount for APE and the distribution ratio of staking rewards, while APE token holders can choose suitable pairing requests in the pairing market. Generally, they prioritize requests that allocate more staking rewards to themselves.

BAYC/MAYC that have already participated in BendDAO's collateral lending (i.e., boundBAYC/boundMAYC) can also participate in Ape Staking, and BAYC/MAYC that have participated in Ape Staking can also engage in collateral lending on BendDAO.

Currently, Bend Ape Staking has staked 5.97 million APE, 507 BAYC, 442 MAYC, and 135 BAKC.

04 Business Data

Basic Data

According to the official Dune data dashboard, as of now (2023/2/7), BendDAO's total TVL (ETH deposits + value of mortgaged NFTs) is approximately $203 million. Detailed data is as follows:

There are 75,873 ETH in the loan pool, approximately $124 million.

The total floor price of mortgaged NFTs is 48,970 ETH, approximately $79.81 million.

The current outstanding debt is 20,488 ETH, approximately $33.4 million.

The cumulative loan amount is 127,912 ETH.

Currently, the total number of blue-chip NFTs mortgaged in BendDAO is approaching 1500, with BAYC/MAYC being the most numerous. In terms of value, BAYC accounts for 65% of the total collateral value on the platform.

BendDAO has cumulatively lent out 127,810 ETH, with the amount of ETH lent using BAYC accounting for 76.32% of the total.

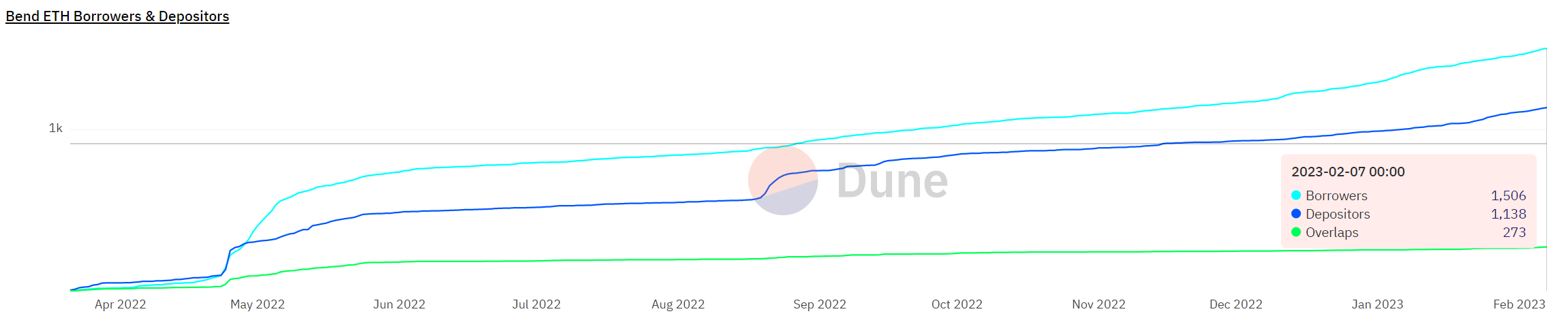

Currently, the number of depositors on the BendDAO platform is 1138, while the number of borrowers is 1506.

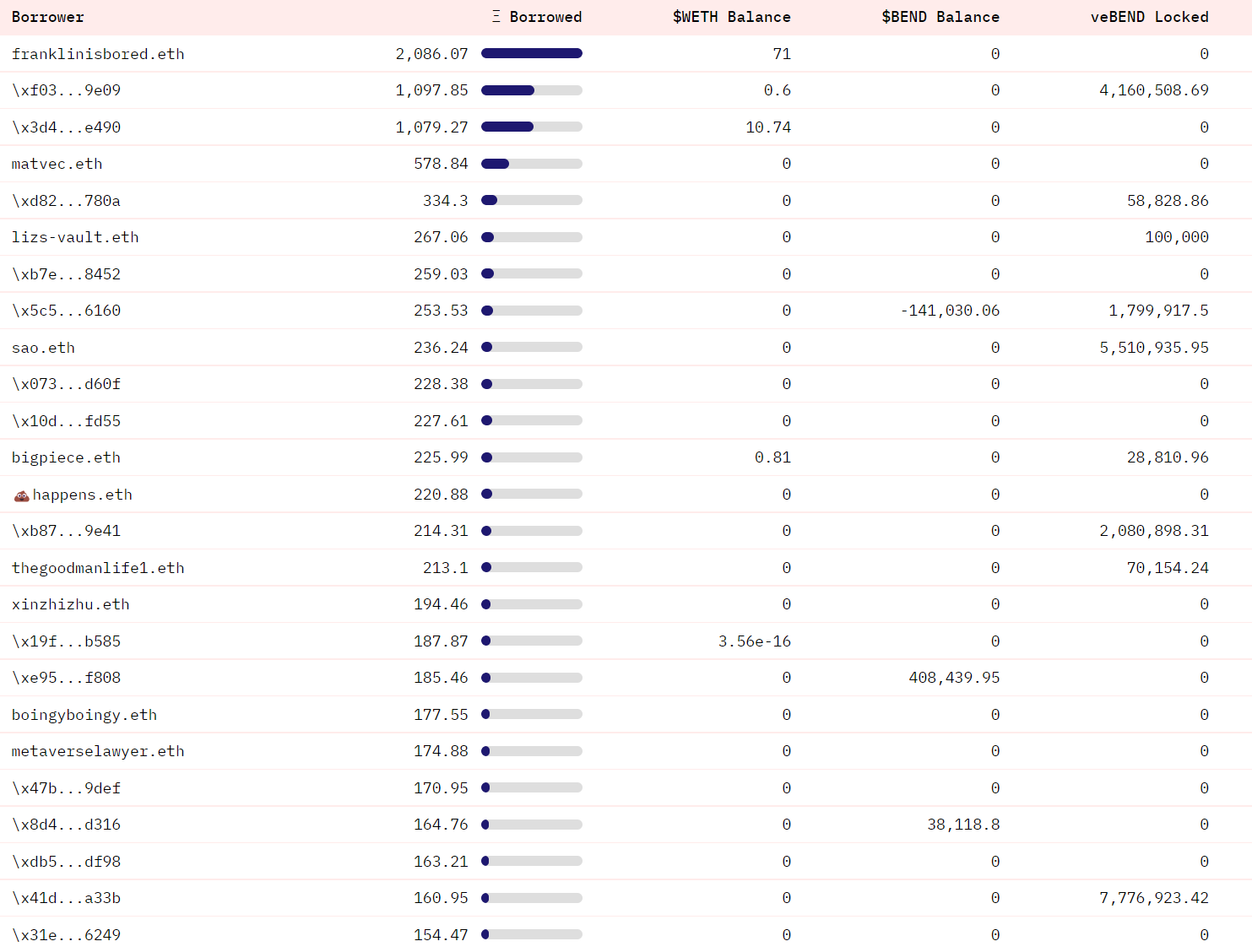

Major Borrowers

The following chart shows the top 25 borrowers on the BendDAO platform, with the top three borrowers each exceeding 1000 ETH in borrowing.

Market Share

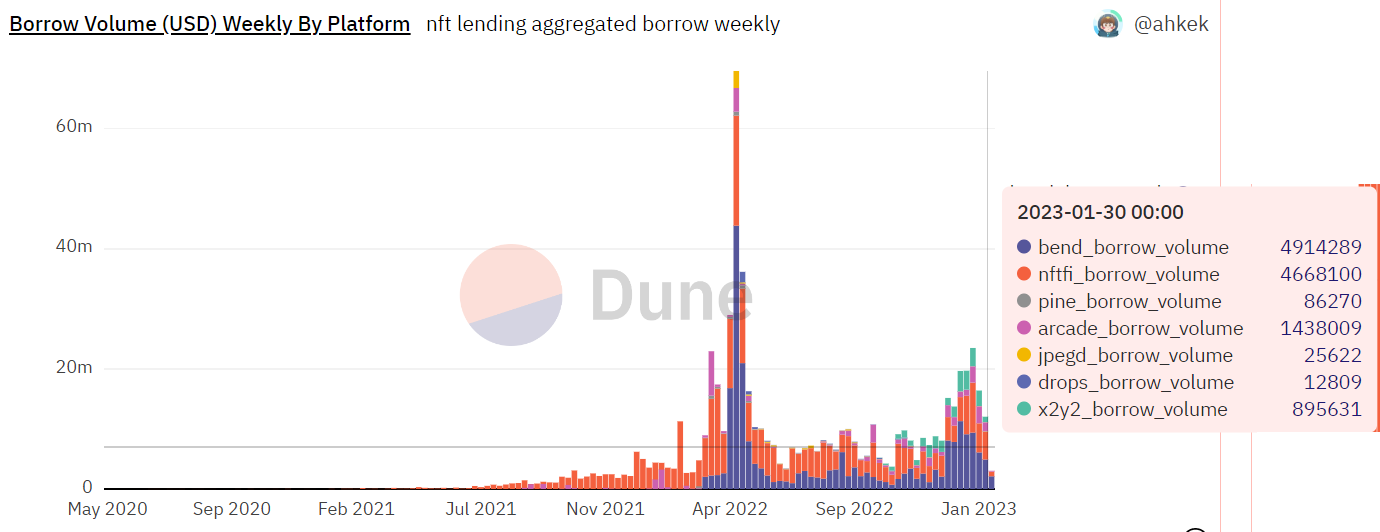

In terms of cumulative loan amounts, BendDAO ranks first among peer-to-pool NFT lending platforms; across the entire NFT lending market, BendDAO is second only to NFTfi, which adopts a peer-to-peer model.

In terms of weekly loan amounts, BendDAO has seen significant growth in recent weeks, surpassing NFTfi to become the largest NFT lending platform by loan volume.

05 Economic Model

Token Distribution

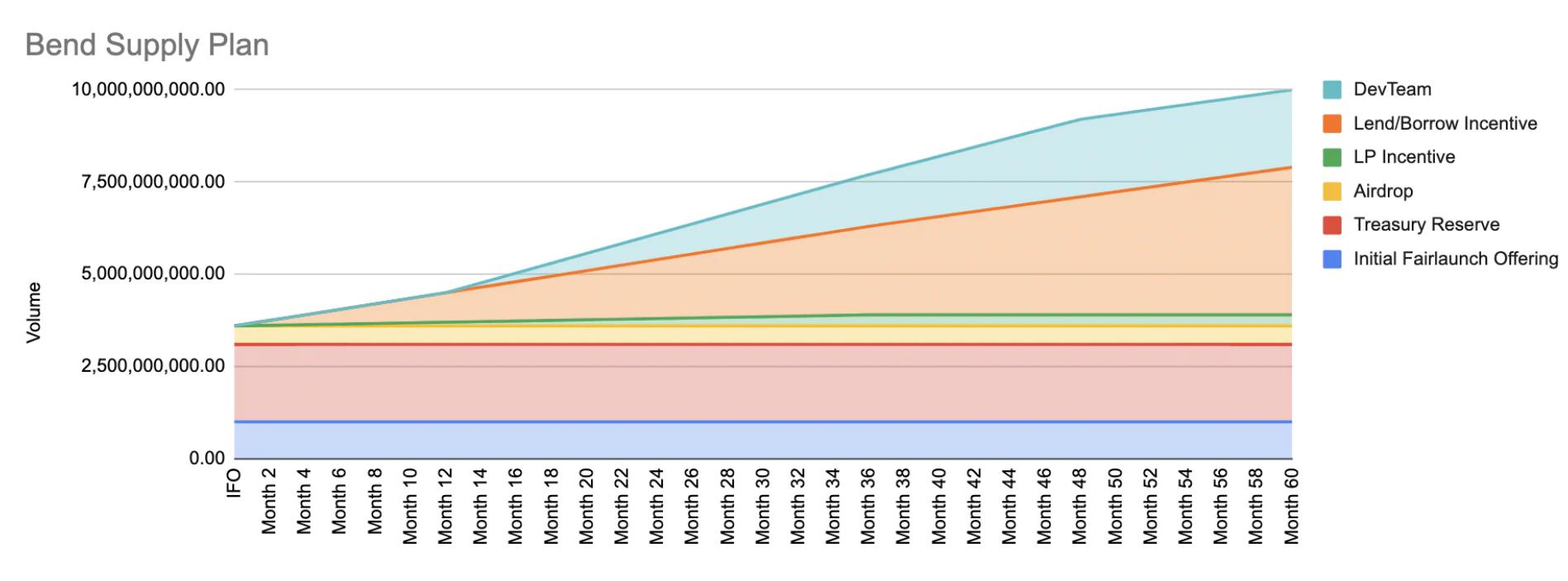

BendDAO's native token is BEND, with a total issuance of 10 billion BEND, and the TGE date is March 20, 2022. The distribution is as follows:

The official token release trend chart is as follows. Based on the TGE date, it is currently in the 11th month. However, the treasury reserves/airdrop/IFO portions in the chart are assumed to be fully released.

veBEND

Holders of BEND tokens can lock them (stake) to obtain veBEND, with lock-up periods ranging from 1 month to 4 years. The more BEND locked and the longer the lock-up time, the more veBEND can be obtained. veBEND can be used for governance participation, voting on which NFTs BendDAO supports as collateral/loan ratios, etc., and can also earn dividends from platform income (all in ETH), including:

100% of the platform's loan fees (30% of loan interest)

50% of the fees collected from NFT transactions by the platform (2% of the transaction price)

50% of the fees collected from the down payment purchase NFT feature by the platform (1% of the transaction price)

Here is an explanation of IFO: Users can freely choose the lock-up period when participating in IFO, similar to locking with other token holders.

Lock-up trend: The following chart shows the lock-up data for BEND tokens. It can be seen that the lock-up amount is steadily increasing, currently around 1.25 billion BEND.

Earnings data: As shown in the chart below, the total daily lock-up dividends in the past month have been around 5 ETH, with a cumulative dividend of 993.3 ETH, and the current lock-up APY is 8.9%.

Token Distribution

The top 16 holders of BEND tokens on-chain are shown in the chart below:

Holder 1: Mining reward pool, initially 43% (40% deposit/loan rewards + 3% LP rewards), currently 36.26%

Holder 2: Treasury, initially 21%, currently 23.72%, with unclaimed airdrops (4.4%) placed in the treasury

Holder 3: Team, 21%, locked

Holder 4: Lock-up address

Holder 5: BUG rewards, allocated from the treasury

Holder 6: Exchange

Holder 7: Uniswap LP

Holder 8: Secondary large holders, cost about $0.015

Holder 9: IFO large holders, cost about $0.01

Holder 10: Secondary large holders, cost about $0.0089

Holder 11: Exchange

Holder 12: Large holders, all obtained from rewards

Holder 13: IFO large holders, cost about $0.012

Holder 14: Secondary large holders, cost about $0.0074

Holder 15: After participating in IFO, purchased $200,000 worth of BEND at approximately $0.067 per unit in April 2022, subsequently sold at a loss in the range of $0.06-$0.03, and continued to purchase from June 2022, with a cost of about $0.08

Holder 16: Secondary large holders, cost about $0.007

Mining Release

A total of 4.3 billion BEND tokens have been allocated for mining rewards. Over the past 10 months (from 2022/3/20 to 2023/1/21, 305 days), approximately 624 million BEND have been released, averaging about 64 million BEND in rewards per month, and approximately 2.046 million BEND released daily.

Treasury Expenditures

The treasury wallet has had four outflows:

Transferred to the BUG reward wallet 166 million BEND, with 162 million remaining, sending small rewards regularly each month.

Three transfers to personal wallets totaling approximately 4.86 million.

Totaling over 8 million BEND.

Circulation and Market Value

The current price of BEND tokens is approximately $0.0266, with an FDV of about $266 million.

Based on the data above, the current non-circulating portion of BEND tokens includes the remaining amounts in the mining rewards wallet, treasury wallet, team wallet, and BUG reward wallet, with the circulating portion being approximately 1.74 billion BEND, giving a circulating market value of about $46.28 million; if we exclude the locked-up 1.25 billion BEND, the actual circulating portion is about 490 million BEND, with an actual circulating market value of about $13.03 million.

06 Project Summary

With the development of the NFT market, using lending tools to release the liquidity of NFTs will become a necessity. As a leading player in the field, BendDAO has a market value in the tens of millions of dollars and immense potential for growth.

Since its launch in the bear market, the locked amount of BEND tokens has continued to grow steadily, indicating high user loyalty. The loan volume is also continuously increasing, especially after entering the recent small bull market, with a significant increase in loan volume in early January, although there has been a recent decline.

Since this wave of market activity, the price of BEND has surged nearly 7 times from the bottom, with FOMO factors present, necessitating caution regarding short-term risks, but it is worth long-term attention.