SnapFingers Research: 2023 Cryptocurrency Sector Review and Outlook

In-depth analysis of the development and trends of public chains, Layer 2, NFTs, and the GameFi sector.

In-depth analysis of the development and trends of public chains, Layer 2, NFTs, and the GameFi sector.Author: SnapfingersLabs

01 Public Chain Landscape and Trends

As the core narrative of the industry, public chains have primarily evolved in three directions: consensus mechanisms, programmability, and scalability.

1.1 Changes in the New Public Chain Landscape

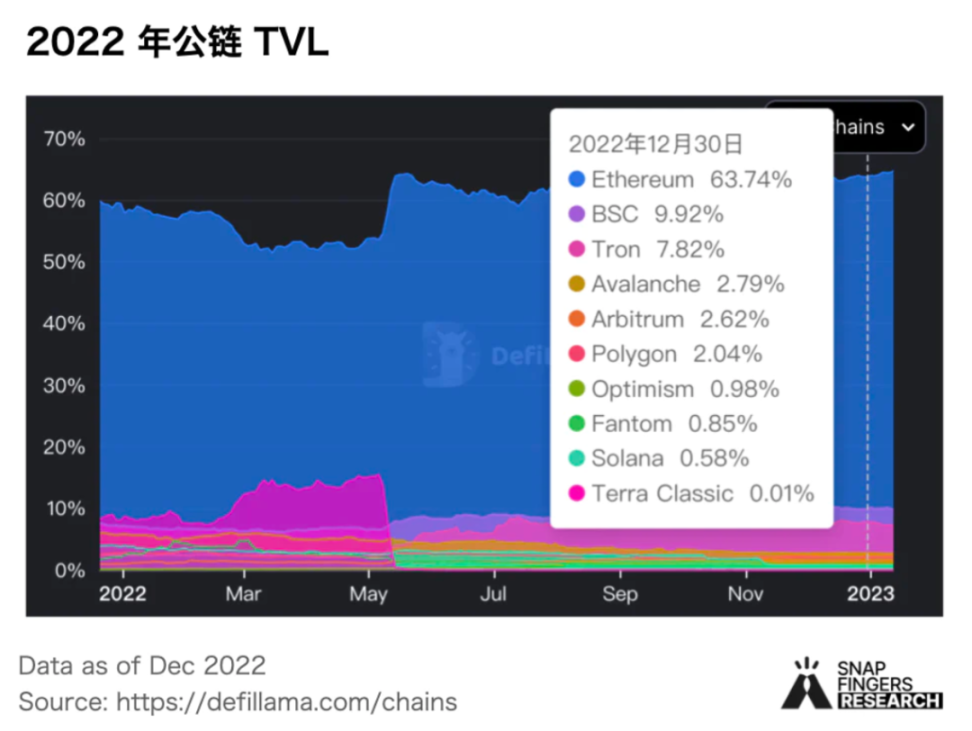

- After a series of new public chain competitions, Ethereum's TVL share steadily increased in 2022, reaching 65%.

- BSC's share also slightly increased, reaching 9.9%.

- With the backing capital and platforms declining, and the ecosystem migrating towards Move-based public chains, Solana is being abandoned by the market and capital, with its TVL dropping from 4% at the beginning of the year to 0.58%.

- Tron’s TVL has significantly increased, rising from 2.41% at the beginning of the year to 7.82%.

- Arbitrum and Optimism's TVL share reached 3.59% by the end of the year, tripling from the beginning of the year.

1.2 Move-based Public Chains

To address scalability issues, Ethereum has compromised on the sharding route in favor of the Layer 2 Rollup route, and there may be a Layer 3 scalability in the future. Move-based public chains choose to build a new L1 from scratch, addressing scalability and contract security issues at once. They enhance public chain performance through a parallel execution environment and provide higher contract security through the Move language and MoveVM.

Aptos and Sui are two blockchains based on the Move programming language, both focusing on enhancing scalability, with their TPS theoretically reaching 120,000 to 160,000. However, current Aptos browser data shows that the total transaction volume on the network is 67,128,283, with a current real-time TPS of 6. The total supply of the native token APT is 1,014,385,262, with 836,936,550 staked and 102 active nodes.

Compared to Aptos's focus on ecosystem promotion, Sui is more about sharing its technical documentation and evangelizing Sui Move. In terms of community airdrops, Sui appears more cautious. With significant funding, the development of the Sui ecosystem in 2023 is worth looking forward to.

1.3 Cosmos Ecosystem

The future of multi-chain allows for greater flexibility and customization. Building entirely new blockchains provides more freedom in underlying architecture decisions compared to modifying smart contracts to meet specific needs. Cosmos is a representative in this field. The Cosmos 2.0 white paper updates the utility of ATOM to address current issues of application chain security, lack of value capture for ATOM, and high inflation rates.

Highlights of the Cosmos application chain in 2023:

- The decentralized derivatives leader dYdX will migrate to Cosmos, with its V4 version reappearing as a high-performance application chain + order book. dYdX plans to eliminate gas fees on the application chain, with validators compensated by receiving a portion of transaction fees.

- Sei is the first parallelized Cosmos chain, focusing on creating a high-speed chain specifically for trading. Sei Network features multiple concepts such as parallel execution Layer 1, CLOB, and anti-MEV, making it easy to attract market attention. Additionally, its EVM compatibility facilitates the establishment of an application ecosystem.

1.4 Modular Blockchains

The core components of an L1 blockchain are the execution layer, consensus layer, and data availability layer. By modularizing the execution and data availability layers, performance improvements can be made for each layer, resulting in a more scalable, composable, and decentralized system. Furthermore, the modular architecture breaks the correlation between computation and verification costs, allowing blockchains to scale throughput while maintaining trustlessness and decentralization, thus solving the scalability trilemma. The uniqueness of modularization lies in its pluggability and composability.

- Celestia is a modular blockchain that provides data availability and consensus layers. Polygon Avail offers similar functionalities, including a data storage layer and a transaction ordering consensus layer within the consensus layer. Besides Celestia and Polygon Avail, StarkEx and zkPorter also provide data availability. The data availability layer is a Lego block that has been overlooked in the future of modularization.

- Fuel Labs is developing a parallelized virtual machine, positioning itself as a modular execution layer.

1.5 Polygon

Polygon's TVL has dropped from $5 billion at the beginning of 2022 to $1 billion currently, ranking fourth, with only a $40 million difference from the fifth-ranked Arbitrum. In 2022, Polygon made significant progress in various aspects.

- Polygon has been integrating with the real world, expanding its user base, and aligning with regulatory trends.

- In 2022, Polygon became a key choice for mainstream brands entering the blockchain world, including Starbucks, META, NIKE, Reddit, Disney, and Trump NFTs. For example, Reddit provided NFTs for active users as rewards, with over 4.3 million independent wallets minting more than 5 million avatars. Starbucks' NFT membership incentive program and META's NFT minting on Instagram will bring more crypto users.

- Mid-year, Polygon achieved carbon neutrality by purchasing carbon credits and plans to reduce carbon emissions in the future, providing emission reduction quotas for important projects and launching a carbon trading market (although the EU no longer emphasizes emission reductions);

- During the Luna collapse, Polygon actively provided funding and technical solutions to encourage outstanding projects to migrate to Polygon, with over 50 gaming projects migrating from Terra to Polygon;

- Polygon has a complete set of zero-knowledge proof (ZK) and data availability (Data Availability) solutions called Avail.

Three types of zero-knowledge proof solutions:

- Currently, Polygon's flagship ZK solution is Polygon zkEVM, which is fully compatible with the Ethereum Virtual Machine through an equivalent EVM. It is now in the final testing phase, having achieved 2000 TPS in previous tests.

- In December 2021, Polygon acquired Mir for $400 million, renaming the protocol to Polygon Zero, which has implemented the recursive zero-knowledge proof system Plonky2. Plonky2 not only proves faster but also has significant advantages in proof costs with the re-pricing of CALLDATA in EIP-4488.

- Polygon Miden is an Ethereum-compatible Rollup scaling solution based on STARK. It uses a relatively STARK proof system to build a virtual machine, aiming to solve the problem of rollups struggling to support arbitrary logic and transactions, enhancing the ability to validate all off-chain transactions.

1.6 Privacy Layer

Privacy and data sovereignty are among the core issues of Web3.0 research, and scalability continues to be a key challenge for blockchain performance. Zero-knowledge proofs can help enhance privacy protection and transaction throughput for blockchains:

- Enhanced Privacy: Zero-knowledge proofs can hide information while allowing blockchain miners to verify the correctness of transactions, achieving privacy protection.

- Increased Throughput: Aggregating nodes can send a large number of proofs corresponding to transactions to the mainnet through effective zero-knowledge proofs, allowing mainnet validators to verify the proofs without recalculating a large number of transactions, thus improving throughput and significantly reducing transaction costs.

Although the privacy sector is still in its early stages, it will become increasingly important as a necessity with the development of the blockchain industry. The Tornado Cash sanctions incident in August attracted significant attention and sparked industry discussions. Regulated privacy protocols are a consensus among new privacy protection protocol projects and will become a development direction.

The privacy sector has attracted the attention of top VCs in the industry:

- Aztec Network is a privacy Layer 2 that has launched ZK money and completed a $100 million financing round led by a16z in December.

- In May, Oasis Network received an additional investment of $35 million, bringing the total ecosystem development amount to $235 million.

- Aleo is a blockchain that protects privacy through zero-knowledge technology, completing a $200 million financing round in February.

- Secret Network, a privacy Layer 1 based on Cosmos, received a $400 million ecosystem development fund in January.

In the future, with the development of new application scenarios such as DID and social applications, as well as traditional institutions entering the blockchain space, the privacy sector is expected to experience explosive growth.

02 The Rise of Ethereum L2

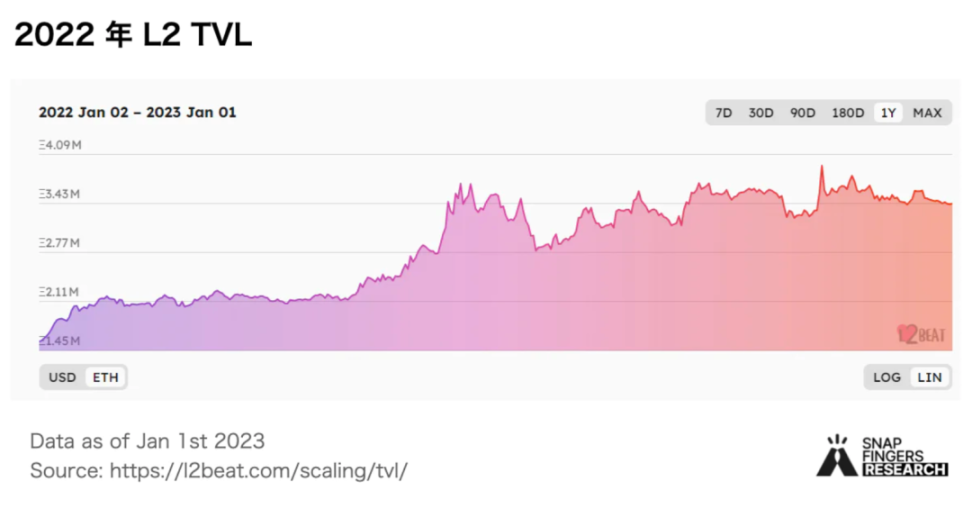

The dollar value of assets crossing to L2 has decreased from $5.7 billion to $4.1 billion, a decline of 28.6%. However, this may be due to the drop in cryptocurrency prices rather than user fund withdrawals. When measured in ETH, the TVL rose from 1.6 million to 3.4 million, an increase of 120.6%. This indicates a significant influx of liquidity into L2 in 2022.

2.1 OP Track

Currently, Optimistic Rollup occupies the main market of L2, with Arbitrum being the leader.

- Throughout 2022, Arbitrum's transaction volume saw significant growth, driven by increased traction from native dapps like GMX and the Nitro upgrade, which greatly reduced transaction fees. The network's transaction volume grew from 5 million in Q1 to 34.9 million in Q4, an increase of 590%. On the user side, Arbitrum experienced strong growth in active users during 2022. The monthly average active user count for L2 surged from 91,800 in Q1 to 6.05 million in Q4, an increase of 559.1%.

- GMX, as a breakthrough L2 application in 2022, saw its usage soar when on-chain activity dwindled and prices fell. This decentralized perpetual exchange based on Arbitrum facilitated $81.4 billion in trading volume and generated $33 million in revenue, effectively utilizing the increased throughput of L2. GMX has become a core foundation of Arbitrum, accounting for 39.5% of the network's TVL, with many projects like Dopex, Vesta Finance, Rage Trade, and Umami Finance built on GMX and integrating the platform's liquidity token GLP. This growth, along with a strong token model that includes revenue sharing, has made GMX one of the best-performing assets in all cryptocurrencies, rising 87.4% against the dollar and 487.2% against ETH in 2022.

- Optimism also experienced significant growth in transaction volume, likely due to increased activity following the launch of OP and subsequent incentive programs. As the only Rollup solution that has achieved "EVM equivalence," Optimism has unique advantages in being friendly to Ethereum ecosystem developers and facilitating migrations. Optimism processed 3.2 million transactions in Q1 and 30.3 million transactions in Q4, with an increase of up to 846.7% between these two periods. The upcoming mainnet Bedrock upgrade will enhance EVM equivalence to Ethereum equivalence. After Ethereum deploys EIP-4844, Optimism will be able to offer optimal transaction fees. The number of monthly active addresses on Optimism surged from an average of 33.1K in Q1 to 403.4K in Q4, an increase of 1118.7%.

2.2 ZK Track

ZK-Rollup offers higher on-chain security and lower gas fees, but most ZK-Rollups currently only support specific applications and do not support general smart contracts. zkEVM can execute smart contracts in a way compatible with zero-knowledge proof computation, making the realization of zkEVM key for ZK-Rollups to capture the market.

zkSync and Starkware

zkSync and Starkware achieve EVM compatibility through high-level languages, with their zkEVMs structurally quite different from Ethereum, providing the highest performance at the cost of compatibility.

zkSync 2.0 is still under construction but has already launched its mainnet. zkSync has raised $458 million and has not yet issued a token.

Starkware has formed two development branches:

- StarkNet (general Layer 2 scaling network), with the StarkNet token economic model already released. StarkNet has a large number of native projects under development, with NFT and GameFi potentially becoming breakthrough areas. In Q1 2023, StarkNet will update to support Cairo 1.0, aiming to migrate to a fully Cairo 1.0-based network by the end of Q1, officially realizing its ZK-EVM.

- StarkEx (scaling engine technology) consists of two modules that serve blockchain applications with specific needs. It leans towards providing To B services for project parties rather than being a Layer 2 network. From a data perspective, StarkEx has already succeeded. There are a total of four projects in the StarkEx ecosystem—Immutable X, dYdX, DeversiFi, and Sorare—each with significant locking amounts and trading data that can stand alone in Layer 2.

Scroll and Polygon ZK EVM

Scroll and Polygon Hermez not only support Solidity language but also most development tools, protocol standards, and bytecode on Ethereum, realizing zkEVM as ZKRollup.

Scroll is a fully EVM-compatible zkRollup, aiming to have a scalable network that achieves native compatibility with the Ethereum protocol. Scroll completed a $30 million Series A financing round in April but has not yet issued a token.

03 DeFi Track Analysis

The DeFi market suffered a heavy blow in 2022, with total market capitalization and TVL both dropping by about 80%. However, it is undeniable that this industry has significantly shaken the TradFi market. Especially after the institutional blowups following the Terra collapse and the rapid downfall of FTX, DeFi has increased people's trust due to its resilience amid market volatility.

3.1 DEX

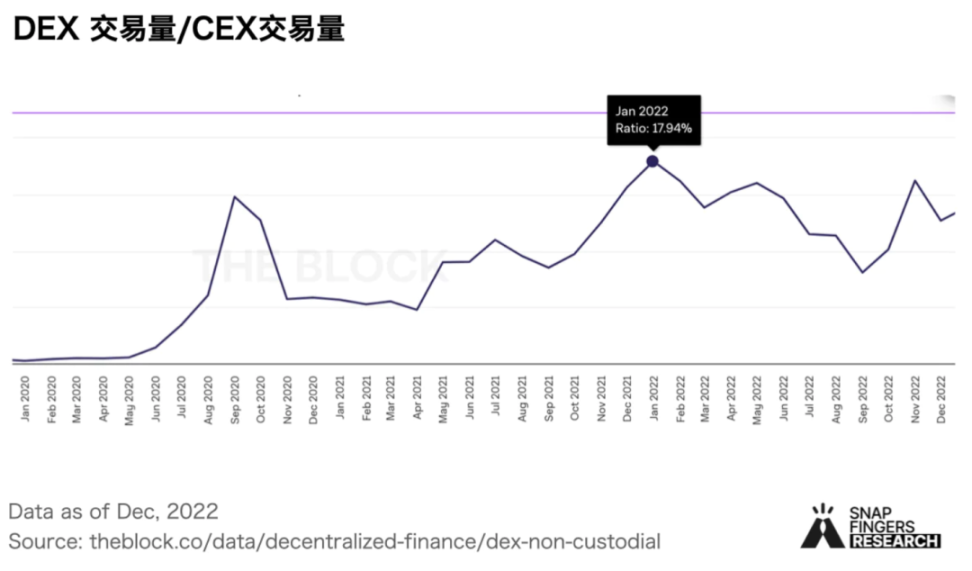

- On-chain trading has experienced explosive growth over the past two years. For spot trading, DEX trading volume was only 0.12% of CEX at the beginning of 2019, peaking at 18% in January 2022.

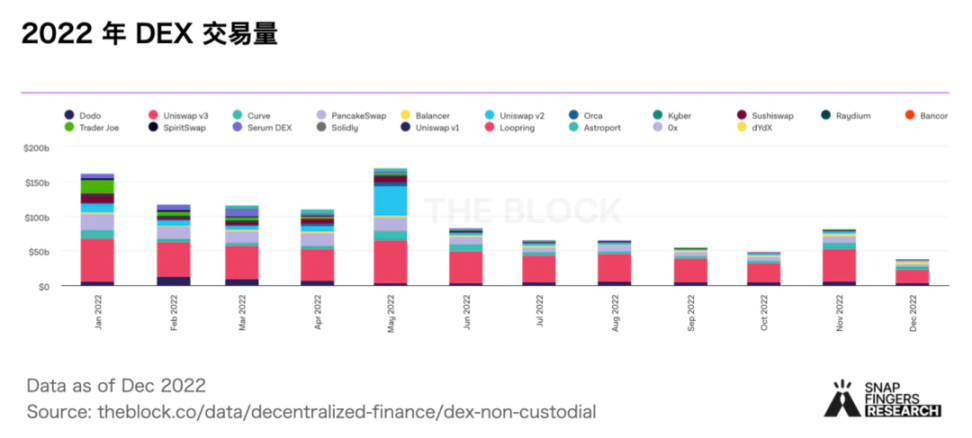

- Uniswap holds the highest market share, with the second tier including Pancakeswap, Curve, DODO, Balancer, and Sushiswap.

- Leading DEXs like Uniswap and Curve still occupy the majority of on-chain trading.

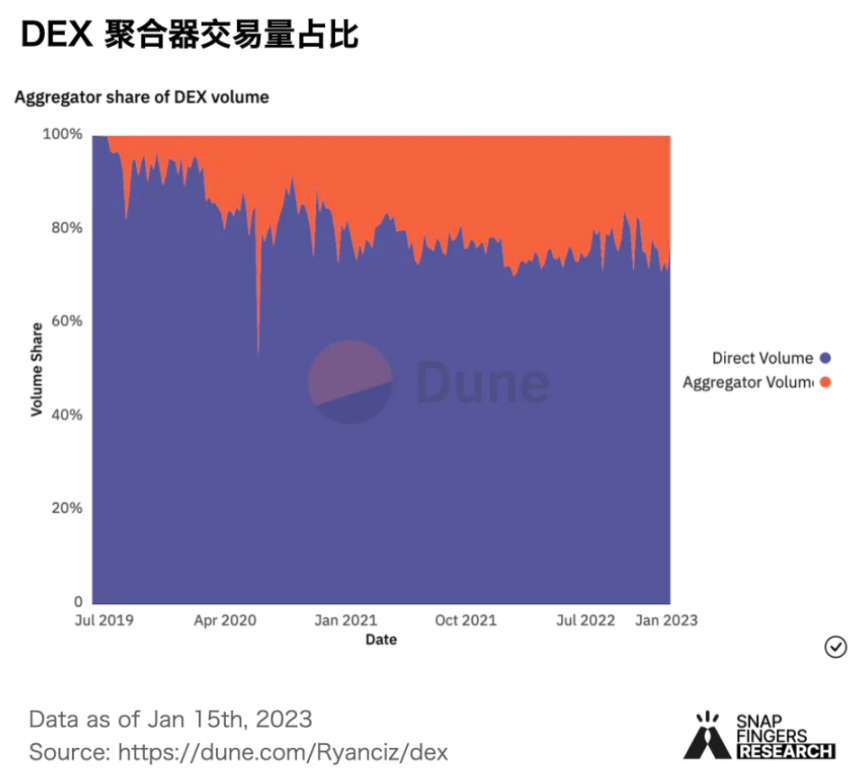

- Aggregators are trading platforms that prioritize user experience, representing non-bot trading volume (over 70% of aggregator trading volume is generated by non-bot traders). Notable projects include 1inch, DODO, Matcha, Paraswap, KyberSwap, and CowSwap. In 2022, DEX aggregator trading volume accounted for 15%-30%, still leaving significant market space.

- In 2022, DEX primarily focused on solving issues of capital efficiency, reducing slippage, impermanent loss, and fees. As platform token prices fell, impermanent loss in the AMM model became a prominent issue. If this issue cannot be resolved, order books may dominate.

- In 2022, DEX continued to expand to other chains and NFTs.

- Curve released a white paper for its crvUSD stablecoin, which adopts a lending-liquidation AMM algorithm. When collateral prices fall, LPs can gradually sell collateral for crvUSD, and when prices rebound, they can repurchase the collateral. More details and the issuance timeline for Curve's stablecoin are still to be determined.

3.2 Lending

In the crypto world, lending protocols serve as crypto banks, playing an irreplaceable role as credit intermediaries and liquidity engines.

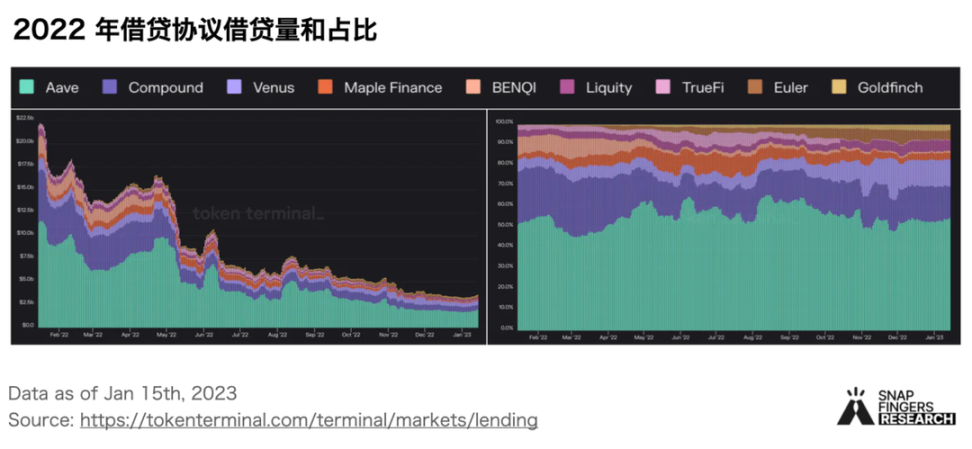

- In 2022, the total lending volume of lending protocols decreased by 83%, with the most significant drop occurring during the UST collapse. Aave maintained its market share, accounting for about 54% of total lending volume, while Compound's share fell from 25% to 15%.

- Interest rates reflect the supply and demand relationship of assets. In 2022, the borrowing rate for USDC fell from around 4% at its peak to about 2%.

- Aave plans to launch an over-collateralized stablecoin called GHO. The Aave protocol will retain 100% of GHO interest income, which will become a significant driver of Aave's revenue growth.

3.3 Derivatives

In 2022, derivatives trading volume fell by 40% compared to the same period last year, a smaller decline than DEX.

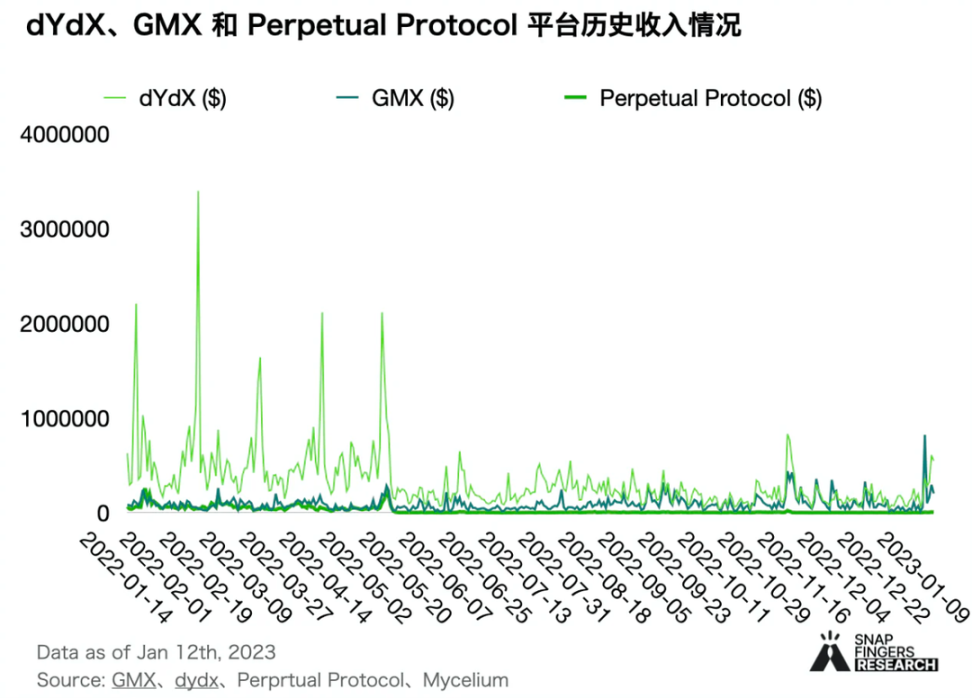

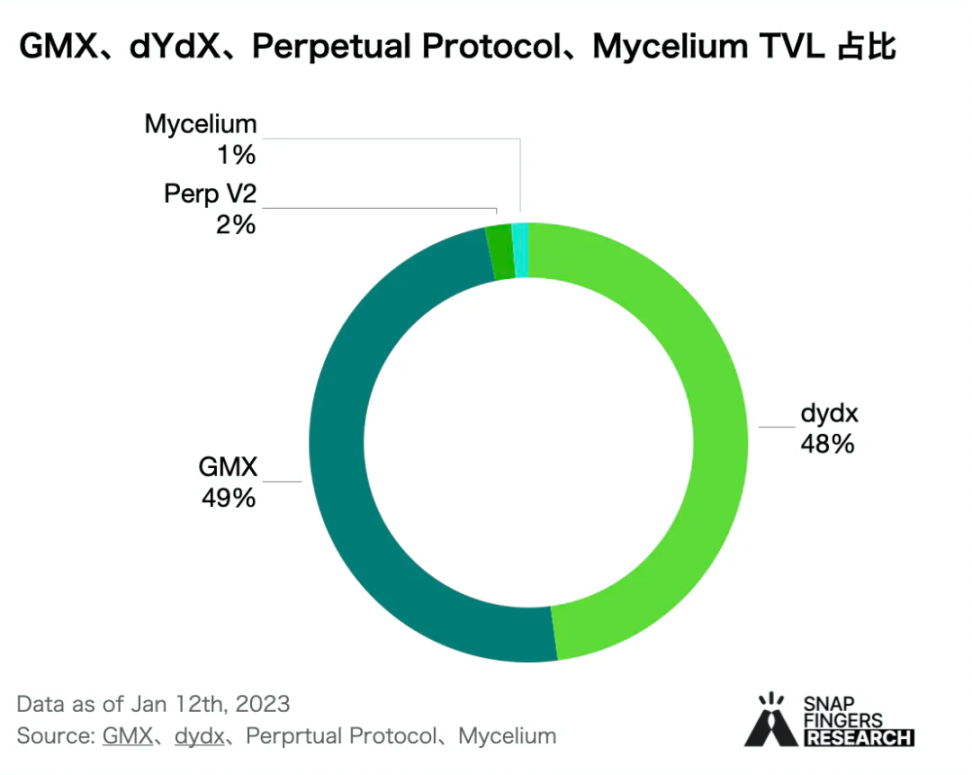

As the FTX incident continued to unfold, more users began to reassess security issues and turned to DeFi, laying the groundwork for GMX's explosion. dYdX remains the leading derivatives protocol, with the highest cumulative user base and revenue, but GMX is rapidly catching up.

GMX allows players to become counterparties through the GLP index token, eliminating the need for any market maker intervention. Based on this model, a series of derivative projects like Umami and Rage Trade have emerged, attempting to earn part of the GLP yield without holding risky positions like BTC or ETH.

04 NFT Track

Since 2021, NFTs have been the fastest-growing area in the crypto space. In the context of external financial panic and a chain of collapses in the crypto industry, NFTs have not been immune. In 2022, the largest NFT trading market, Opensea, reached a historical peak of $4.85 billion in trading volume in January, but by December, trading volume had dropped to $280 million, a decline of 94%. Both the prices of blue-chip NFTs and NFT trading volume and total market capitalization have decreased, leading the entire NFT market into a deep bear market.

Despite the NFT market's slump, with current daily trading volumes only 15% or even lower than during the bull market, there are still noteworthy aspects:

- An increasing number of traditional brands are actively adopting NFT technology to connect with their customers and build more engaging communities.

- After cooling down in 2022, the NFT market has focused on solving liquidity issues and has experimented with AMM, collateral lending, and royalties.

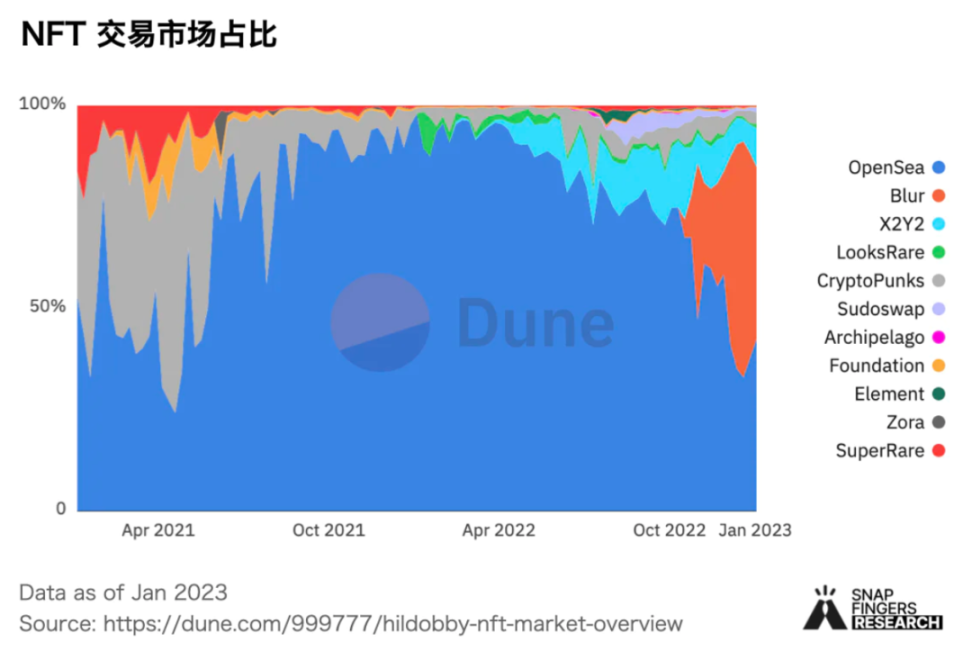

4.1 NFT Trading Market

In 2022, Opensea reached $30 billion in trading volume, maintaining its leading position. From a market share perspective, after achieving 98% absolute dominance at the beginning of 2022, its market share has steadily declined, dropping to below 90% by December. At the beginning of the year, LooksRare and X2Y2 attempted to compete with Opensea through liquidity mining, initially showing significant effects, but as incentives decreased, their market share declined noticeably. By the end of last year, Opensea's market share had significantly decreased, primarily due to the rapid rise of Blur.

Opensea and Its Challengers

- LooksRare: The first trading mining incentive market.

- In January 2022, LooksRare launched a vampire attack on Opensea, airdropping tokens to its users. Subsequently, through token staking incentives and trading mining incentives, zero royalties, and a 2% fee (Opensea charges 2.5%, with 25% going to the project party), it attracted users to the platform. On the day the trading mining incentive program was launched, the platform's trading volume reached $320 million, about twice that of Opensea. However, with the halving of trading incentives and the decline in token prices, the platform's trading volume also rapidly fell. Since the income from staking tokens comes from token rewards and fee dividends, the decline in platform trading volume and token prices leads to a spiral drop in token prices.

- X2Y2: The first listing mining incentive market.

- X2Y2 officially launched in February 2022, airdropping 12% of its total token supply to Opensea users. X2Y2's initial incentive mechanism differs from LooksRare's trading mining, opting to incentivize users who list NFTs. This approach is more user-friendly for ordinary users. The NFT listing mining model and ultra-low fees (only 0.5%) attracted many sellers to list on the platform, and its trading volume briefly surpassed Opensea to take the top spot. Subsequently, the platform shifted its incentives to gas consumption rebates and trading rewards, allocating most of the incentives to sellers in the design of trading rewards. Although X2Y2 still cannot escape user withdrawal, its trading volume ranks among the top three, excluding Magiceden, and it has introduced NFT lending features, with a professional trading version application portal visible on its official website.

In response to vampire attacks from other platforms, OpenSea has taken countermeasures:

- In April, OpenSea officially announced the acquisition of the NFT trading aggregator Gem. As the most successful NFT aggregator application, OpenSea previously derived about 1/10 of its trading volume from Gem, and the acquisition solidified its dominant position in NFT liquidity.

- In May, OpenSea launched a new market protocol called Seaport, reducing gas fees by 35% and allowing for diversified transactions, upgrading from only supporting ETH or WETH to supporting fungible tokens and bundling different assets for NFT exchanges.

NFT Aggregators and NFT AMM Protocols

Since October 2022, the aggregator platform Blur, aimed at professional traders, has captured a significant portion of the Opensea market with its effective airdrop strategy. Blur's airdrop strategy is considered a textbook case, combining strategies from Looksrare and X2Y2 while tailoring unique trading features. It balances randomness with timely feedback. From the data, Blur's growth strategy has been highly successful, currently ranking as the second-largest NFT market after OpenSea, with rapid growth trends in trading volume, unique user count, and transaction numbers. Blur has quickly become the strongest competitor to Opensea, establishing market dominance in a short period. However, as the airdrop ends or incentives decrease, maintaining momentum and aligning long-term with user interests may pose a greater challenge.

SudoSwap provides instant liquidity for NFT trading through the AMM model, representing another highlight in the NFT trading market, although its market share has rapidly diminished after the initial hype.

4.2 NFT-Fi

NFTFi primarily addresses the issue of insufficient liquidity, expanding the financial attributes of NFTs to make their liquidity forms more diverse and efficient, providing more combinable gameplay.

Currently, the absolute mainstream in NFTFi is NFT lending, with the main models being peer-to-pool and peer-to-peer, led by BendDAO and NFTfi.

- BendDAO has captured a significant portion of the NFT lending market since its launch. In addition to using a peer-to-pool model, BendDAO also implements an NFT admission system, currently only supporting 8 top blue-chip projects.

- NFTfi allows users to list their NFTs after submitting for review and meeting certain conditions, supporting a wide range of assets.

The main players in the NFTfi track are a few top blue-chip users, while BendDAO's peer-to-pool model design provides core users with a more convenient lending experience and arbitrage tools. The NFT lending track is still relatively niche, with the number of independent users across several major contracts only around 4,000, and the highest number of active users in a single day in 2022 was only 268.

NFTfi derivatives mainly consist of options, and the scale of the track is relatively small. Current NFT leasing solutions mainly revolve around Double Protocol's ERC-4907 standard, which is still in early stages. The market demand and development potential for NFTfi have been validated through BendDAO and NFTfi, but numerous technical challenges and business logic designs currently hinder its growth.

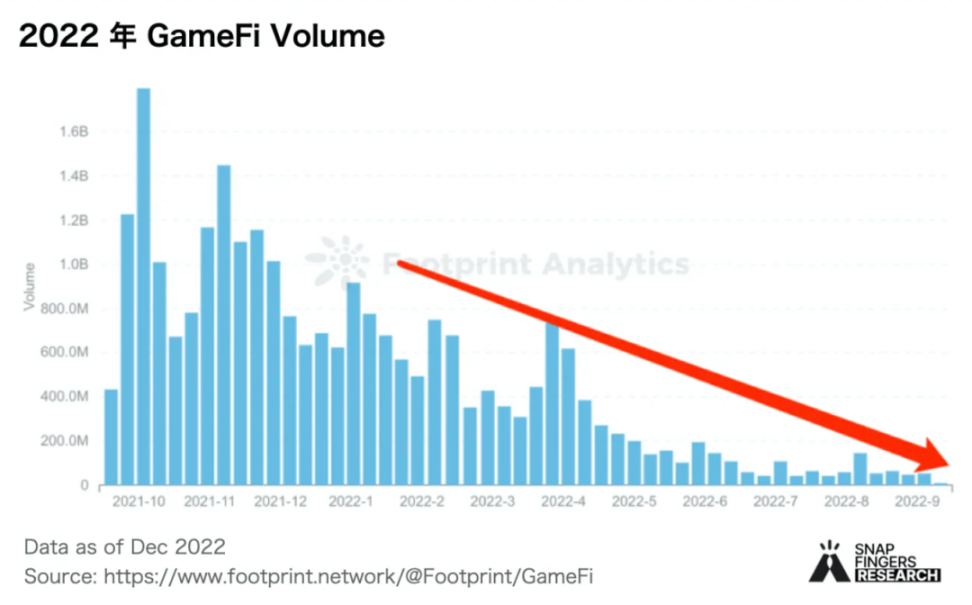

05 GameFi Track

The blockchain gaming market experienced a highlight period from 2021 to 2022. We saw Axie Infinity's daily revenue surpassing that of Honor of Kings, StepN achieving 300,000 daily active users within just four months, becoming the hottest crypto application in Q1 2022, and users scrambling for Otherside land sales, leading to sky-high gas fees.

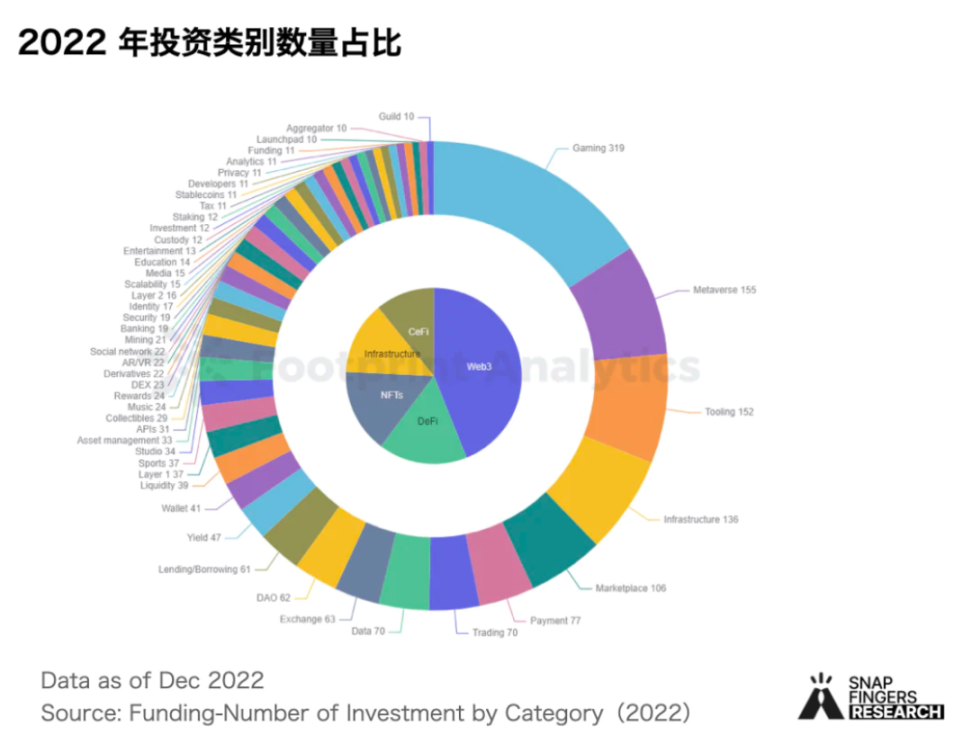

Financing was equally hot. Throughout 2022, total investment in blockchain games increased by 84%. Game projects accounted for 16% of the total investment in the blockchain industry, surpassing any other type of investment. Metaverse projects followed closely behind, ranking second and accounting for 7.79% of total blockchain financing.

Beyond the highlights, this track reveals the harsh realities of survival. The daily active wallet count for Axie has dropped from a peak of 1 million to just 9.5K now, with the vast majority of games failing to last even a month before entering a death spiral. In the metaverse sector, ROBLOX has 202 million monthly active users, Minecraft has 141 million, while Sandbox has only 200K and Decentraland has just 56K.

Summarizing the overall performance of GameFi in 2022, we find:

- The infrastructure for blockchain games is inadequate, facing high storage costs, high computation costs, and long response times.

- There is a lack of effective product logic. The development processes of Axie and StepN demonstrate that relying solely on existing token economic models cannot avoid a Ponzi-like outcome. While positive spiral effects can lead to explosive growth, they cannot prevent negative spiral effects. New economic models and narrative methods still need to be explored.

Conclusion

Gaming is a comprehensive track, and the development and operation of games test the overall strength of project parties. Blockchain games involve not only blockchain technology innovation but also gameplay, economic models, modeling, and other dimensions. In fact, the gaming track has attracted a large influx of funds since 2021. The total investment in blockchain games reached 135 deals in 2021, a year-on-year increase of 1130%. The market's enthusiasm and the comprehensive capabilities required by products indicate that blockchain games possess strong potential to break into mainstream markets. Therefore, we believe that GameFi projects are among the areas with the greatest growth potential in crypto's future.

- Emphasize Gameplay. Fun and profit are not mutually exclusive; the challenge lies in integration. Rich gameplay should be prioritized to provide a reliable guarantee for the lifecycle of blockchain games. Purely mining-based games will find it increasingly difficult to survive in the face of high-quality games, but it cannot be ruled out that during market downturns, mining games may attract a large number of speculators.

- Both AAA titles and lightweight games are paths worth exploring. Looking back at the traditional gaming industry's development history, almost every industry breakout point has been accompanied by technological innovation. Currently, the vast majority of blockchain game products lack a background from WEB2 gaming companies, resulting in almost no authentic AAA titles on the market. However, both AAA titles and lightweight games are paths worth exploring. The project experience, financial strength, and rich IP that traditional gaming giants possess are also needed in blockchain games, which is a guarantee of gameplay.

- The design of economic models needs to serve the long-term stable development of games. Providing more rewards for skilled players and those willing to contribute is essential for promoting the long-term development of games. At the same time, adjusting token inflation levels according to player growth rates and maintaining players' perception of the game economy are crucial for continuously incentivizing UGC output. The success and revenue that games can achieve should be predicated on the value players gain from their gaming experience and economic returns.

Finally, Outlook for the Crypto Track in 2023

Public chain infrastructure is maturing. Public chains will continue to develop along the directions of scalability and cost reduction, as well as privacy. Based on the explosive paths of new public chains in the previous cycle, the explosion of public chains is closely related to ecological prosperity, requiring higher demands from capital and developer communities. In the future, the competition dimensions for public chains will become more complex.

With the maturity of zkEVM solutions, general-purpose scaling platforms based on zero-knowledge proofs will have significant advantages. In the future, we will see projects that have adopted Optimistic Rollup begin to seek transitions to zk proofs or hybrid solutions, leveraging their existing user base advantages to consolidate their market dominance. Ultimately, numerous Rollup solutions (and the increasingly fierce competition among them) will continue to improve the user experience in the Web3 world and attract more users as application platforms.

DeFi derivatives platforms and on-chain strategies are poised for explosive opportunities. Trading and lending in the DeFi track have matured, operating in an orderly manner even during multiple market crashes. The scale of DeFi derivatives is also gradually increasing, and with GMX's popularity, 2023 may see attempts and explorations of composability in on-chain derivatives. Additionally, on-chain options and the off-chain but fully decentralized order book that dYdX V4 will create will be noteworthy in the realm of decentralized derivatives.

Currently, the overall crypto options market has immense growth potential. Compared to centralized options platforms like Deribit, on-chain options protocols lag in terms of liquidity scale and market share. However, as developers create more effective and sustainable liquidity models, and with the market recovery, on-chain derivatives and trading strategies are expected to experience rapid growth.

The NFT ecosystem is blossoming in multiple ways, with application value emerging. Despite the significant contraction of the NFT market due to market conditions, an increasing number of fashion and luxury brands are recognizing the value of NFTs and entering the NFT ecosystem. Based on the non-fungible characteristics of NFTs, there are inherent advantages for authentication and certification. Whether this advantage can find more intrinsic value in areas such as intellectual property, digital identity, ticketing, membership/subscription, or RWA tokenization remains to be seen. The emergence of projects like BendDAO reflects the exploration of NFTs in the DeFi space. Continuous innovation in the NFT field and participation from Web2 will be the foundation for strong growth in the future. After all, whether in a bull or bear market, there are always demands for gaming, social interaction, or consumption.

The breakout effect and explosive potential of GameFi are worth looking forward to. Blockchain games received substantial financing in the last cycle, and some growth models have already been validated as effective. With financial support, more innovative models can be validated, making it easier to produce successful products. Additionally, with improved infrastructure, there is an opportunity to achieve truly decentralized blockchain games.

Identity and contracts are the pillars of Web3 application development, and Web3 social potential is immense. The success of Galaxy provides insight into the tremendous growth potential of precise incentives. DID can be used for credit lending, governance, and targeted airdrops. In 2022, there were increasingly more applications built on identity foundations:

- At the beginning of 2022, the Galaxy Project gained significant traffic, and the application of OAT demonstrated the value of Web3 identity in marketing, becoming a standard for blockchain online activities and significantly increasing participation.

- By the end of 2022, the number of ENS domain names created had surpassed 2.75 million, with 75% of its main income coming from 2022, making it one of the few projects that rose against the trend in a bear market and currently the most widely used identity project.

- Lens Protocol is a social protocol based on universal social identity, now accumulating dozens of ecological projects. Although its overall scale is not large, it is growing rapidly. Since its launch in May 2022, it has attracted nearly 100,000 users and published over 780,000 posts.

- Vitalik's proposed SBT concept has drawn further attention to the Web3 identity track. SBT builds native digital identities in a bottom-up manner, with data accumulation giving each account a "soul." In 2022, projects related to certificates, identities, and semi-credit lending SBTs grew rapidly.