Top 5 Predictions for the Ethereum Ecosystem in 2023

ZK-Rollups may not see significant traction in 2023. Layer 3 will become a true competitor to Cosmos.

ZK-Rollups may not see significant traction in 2023. Layer 3 will become a true competitor to Cosmos.Author: neworder

Compiled by: Overnight Porridge, The Way of DeFi

Our five predictions for the Ethereum ecosystem:

- The bear market is not over;

- EigenLayer will be the most important innovation for Ethereum;

- Blob transactions will not fix scalability issues;

- In 2023, ZK-Rollups will not see significant traction;

- Layer 3 will be the true competitor to Cosmos;

1. The bear market is not over

2022 was destined to be an important year for crypto. With institutional capital flowing into crypto-focused projects, exciting new financial primitives being developed, and its legitimacy as an asset class continuously strengthening globally, the industry seemed to undergo a massive transformation. Unfortunately, these narratives were overshadowed by a major story: a series of financial misconducts primarily occurring among bad actors in positions of power. The exposure of this widespread fraud, coupled with tightening global monetary policy, led the crypto market into a relentless bear market comparable to that of 2018.

For crypto, 2022 was a year dominated by profit-driven capital—entities as value extractors and participants shifting from one opportunity to another, seeking outsized short-term profits with no interest in engaging with the community or building future infrastructure. This was prevalent among most stakeholders in the crypto space, from end users to liquidity providers to crypto VCs—all of whom participated in various forms of rug pulls and dumping activities. However, these three implosions left the industry in a dire situation:

- Do Kwon's Terra-Luna adopted an inherently flawed algorithmic stablecoin model and bribed people to use it for artificially high yields. The decoupling of this algorithmic stablecoin wiped out $60 billion in market value and drained the savings of retail investors globally.

- Three Arrows Capital (3AC), founded by Su Zhu and Kyle Davies, was a forex arbitrage fund that funded its directional crypto bets through massive borrowing. When this severely over-leveraged firm collapsed under adverse market conditions, its billions in bad debts left a huge hole in the balance sheets of lenders across the crypto space.

- Finally, when SBF misappropriated customer deposits and lent them to his trading firm Alameda Research, the FTX exchange collapsed. The crash, triggered by the plummeting value of its FTT token, resulted in billions in losses and led to the bankruptcy of several lending institutions.

So, what does this mean for the crypto industry in 2023? First, we expect that FTX position liquidations and widespread bad debts will continue to negatively impact the crypto market throughout the coming year. As bankruptcies and criminal prosecutions progress, liquidity issues and bankruptcies may continue to be discovered in CeFi and DeFi services. Second, the misconduct involved in these bankruptcies will severely hinder regulatory processes, investor activity, and consumer confidence.

Looking Ahead

Despite the severe setbacks our industry has faced, we remain optimistic about the crypto outlook for 2023. While profit-driven capital has damaged our reputation, our industry is also filled with dedicated builders who are pouring immense sweat into this burgeoning Web3 world. These are what we refer to as "visionary capital," who continue to build even as most industry speculators have left. They are investing long-term efforts to irreversibly push Web3 into everyday life. We believe that 2023 will be a year for visionary capital and a year when cryptocurrency transitions from a speculative investment to a core component of society built around Web3.

To some extent, this transition is already underway. Among the emerging narratives today is the blurring of lines between decentralized solutions and the real world, as DeFi protocols integrate with traditional financial systems, DAO treasuries accumulate real-world assets, and traditional gaming companies venture into Web3. This process will only continue, and 2023 is likely to be the year when Web3 projects enter the mainstream.

To give a few examples. In an era where data breaches are ubiquitous, companies may begin adopting decentralized identity technologies that allow users to self-custody their data. Consumer-facing applications of blockchain technology will emerge in the media space, where marketing, storytelling, and gaming will converge to create immersive interactive worlds. By building blockchain networks on top of existing grids, utility companies will be able to integrate distributed energy into new decentralized energy networks.

While this may not be news to crypto natives, these examples represent the introduction of a large new user base and indicate that the closed world we have seen over the past decade is preparing to open up. Behind these fundamental changes to our daily lives will be a wave of technological advancements that will enhance crypto's capabilities and prepare it for a central role in the metaverse. These events are unfolding in real-time, and our expectations can be summarized as follows, with our predictions for how crypto and Web3 will leap forward in 2023.

2. EigenLayer will be the most important innovation for Ethereum

One of the most significant differences in blockchain development is the degree of permissionless activity that can occur between the infrastructure layer and the application layer. Infrastructure upgrades and changes lag behind the application layer because application deployments are permissionless, while core network upgrades require permission. Changes to consensus, core, sharding, p2p, and middleware layers are based on democratic voting by designated parties, while applications can freely deploy and experiment on top of the core consensus logic.

Established and well-capitalized network systems require prudent risk analysis before core upgrades or changes. This limits innovative solutions to consensus issues and core obstacles, or causes them to arrive late to the market. Once a sovereign trust network for the system is established, the protocol becomes very rigid, making it harder to innovate and upgrade. When innovative consensus mechanisms or middleware layers (such as Snowman, Chainlink, or Nomad) emerge, they cannot operate new networks in a permissionless manner using existing trust layers.

Moreover, new networks are often constrained by inevitable capital boundaries. For decentralized networks to ensure the security of core consensus logic, the cost for malicious actors to self-implement changes or control assets needs to be prohibitively high. Therefore, merely having groundbreaking technology is not enough; builders also need to seek a substantial capital base for network security, which often becomes the biggest obstacle to infrastructure innovation.

The reward distribution further highlights the capitalization issues in network bootstrapping. In the Ethereum validator stack, a total of 96% of rewards are allocated to capital providers, while only 4% are allocated to node operators. The reward distribution is far from arbitrary; it reflects the implicit capital costs in proof-of-stake (PoS) networks. The implicit risks of staking unstable assets for network security are fundamentally much more expensive than running reusable generic nodes.

It is worth mentioning that ensuring the security of core infrastructure guiding the network is a primary concern for decentralized networks. That said, applications built on top of it are always limited by the least secure denominator in their infrastructure stack. Applications that include middleware layers protected by their own sovereign trust networks (such as cross-chain bridges and oracles) are lowering the overall security of the system to the least secure dependencies.

To address the core divergence of innovation from infrastructure to application layers, EigenLayer introduces a simple yet extremely effective solution to tackle the high cost of capital: re-staking.

EigenLayer's Approach

EigenLayer is a smart contract layer on Ethereum that allows users to leverage existing trust networks to secure other core infrastructure and middleware layers through re-staking. The core of re-staking is to use the same staked ETH used for validating the Ethereum network to secure other networks. This gives ETH stakers greater flexibility in staking capital while extending the trust layer to peripheral infrastructures such as sidechains, middleware, and even other non-Ethereum networks.

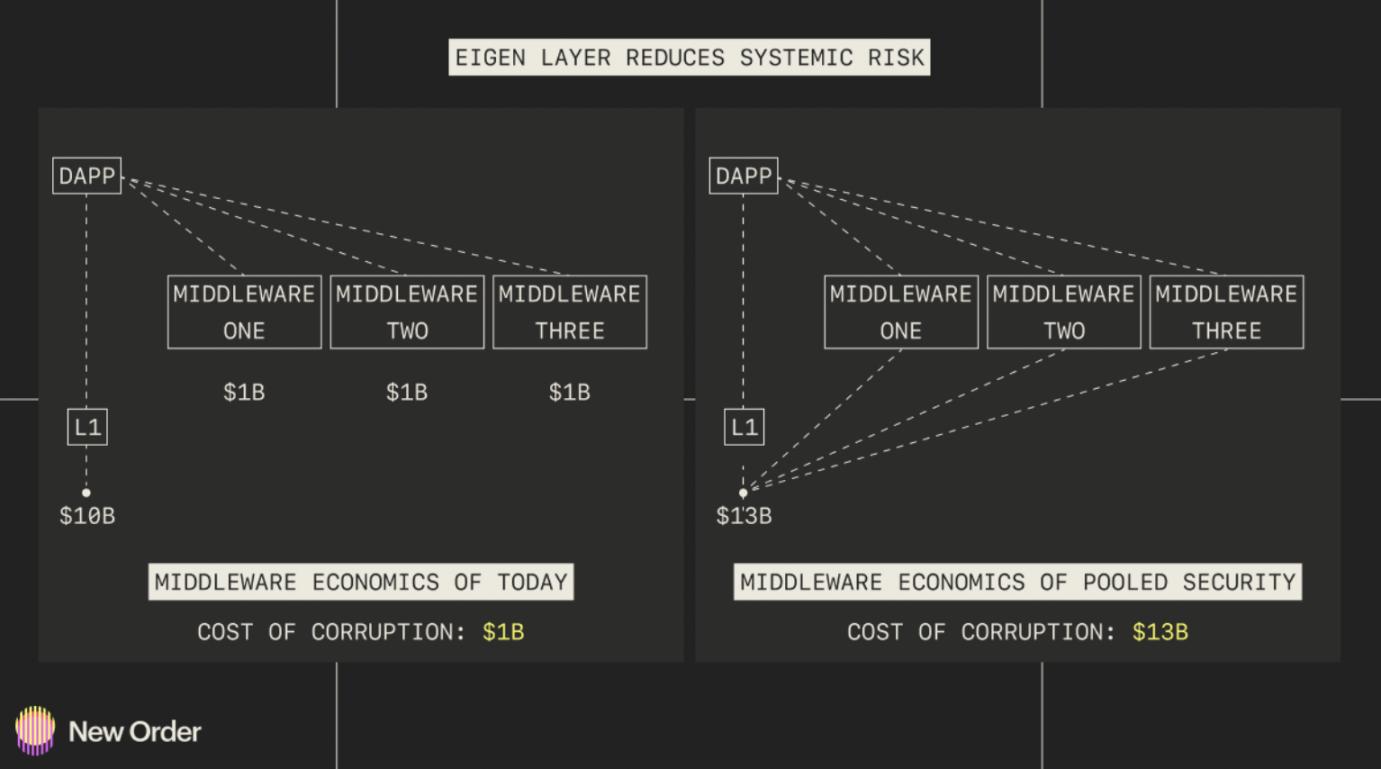

EigenLayer is introducing a two-sided market where ETH stakers can provide services to networks that require a trust layer. This allows new networks to lower their network security costs while accessing a massive pool of capital. In effect, this eliminates the least secure denominator problem in the application layer. Oracles and cross-chain bridge networks will gain security and trust from the same infrastructure layer that builds the applications themselves. EigenLayer allows for the consolidation of trust, ultimately enhancing the security of all networks interacting with that layer. For example, a new entrant into the asset cross-chain bridge space can interact with EigenLayer and immediately gain a security base of $18.7 billion.

Given that ETH stakers do not incur any marginal capital costs when validating other networks, re-staking significantly broadens the range of possibilities for stakers. Of course, EigenLayer does carry some risks of leverage and slashing, as the underlying staked assets may be slashed across multiple secure networks if malicious activity occurs. Whenever the same funds are used to validate multiple networks, the asset base is essentially leveraged, exposing the system to potential cascading failures.

The slashing risk is complex and may lead to slashing contagion. Losses due to malicious activity or downtime fundamentally reduce the security considerations of all validated networks. If left unchecked or unmitigated, this contagion could adversely affect the system architecture. At launch, EigenLayer will introduce prudent leverage guidelines and limits to ensure the stability of the trust system.

EigenLayer is also developing a data availability layer called EigenDA for Ethereum. This layer is similar to the current danksharding specification and includes features like data availability sampling (DAS) and custodial proofs. However, EigenDA is an optional middleware rather than a core component of the protocol. As a middleware layer, it can be stress-tested without requiring a hard fork, providing several advantages: permissionless experimentation of the DA layer and allowing validators to participate on an opt-in basis. If the implementation of pseudo-danksharding succeeds on EigenDA, it may become the de facto DA layer for all optimistic and zk-rollups built on the Ethereum ecosystem before the lengthy process of Ethereum-level protocol changes.

During the prolonged bear market of 2022-2023, liquidity is expected to continue seeking safety within Ethereum, further solidifying the network as a haven and central trust layer for crypto. The security competition will further expand Ethereum's capital base, widening the gap between alt-L1s and pushing the capital costs of new native validation networks to prohibitive levels.

Gaining security from re-staked ETH will significantly reduce the scaling costs of middleware, sidechains, and general decentralized technology stacks. We believe that since Ethereum was first introduced in 2015, Eigen will bring the most significant change to how decentralized networks are built.

3. Blob transactions will not solve scalability issues

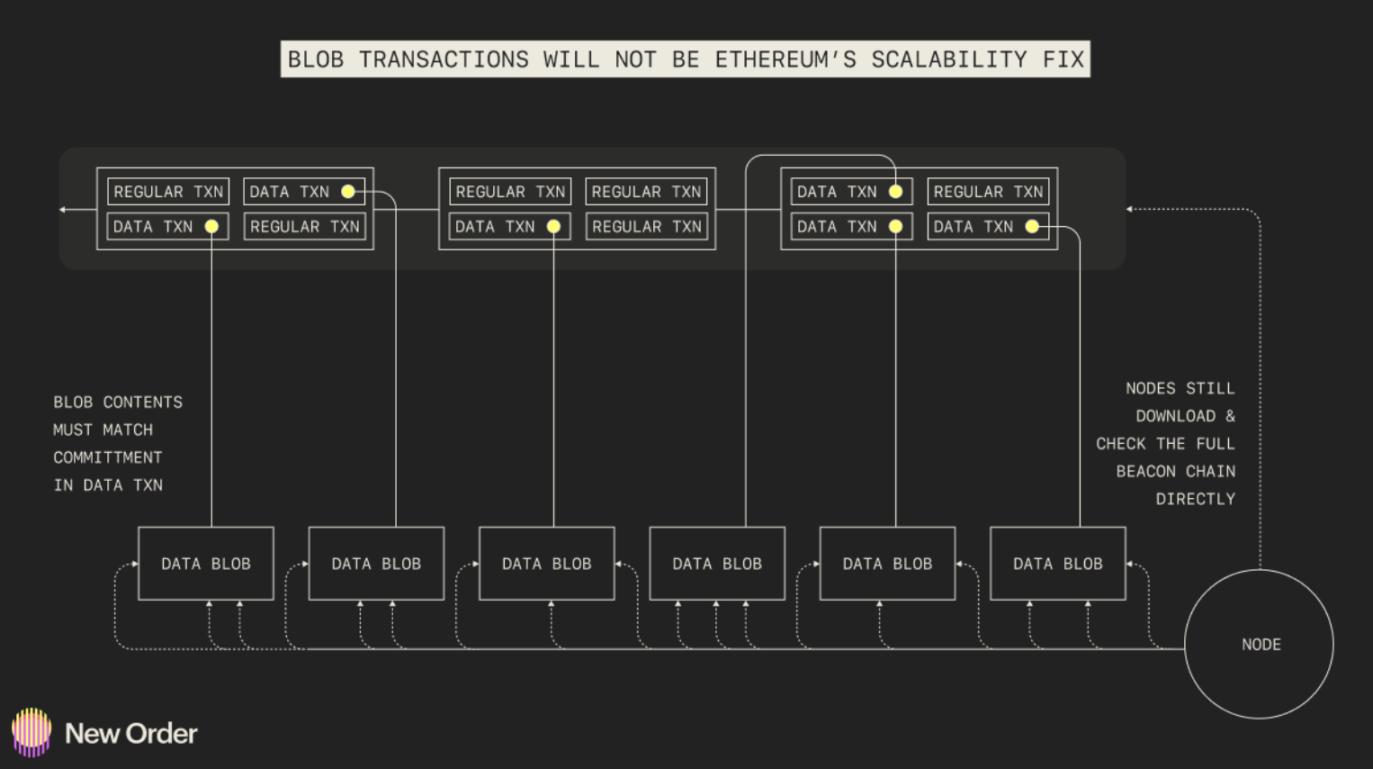

Blob transactions will not become the magical fix for Ethereum's scalability before the implementation of modularity. The implementation of modularity will face considerable technical hurdles and delays. The sharp increase in on-chain data will also drive the need for state expiry to alleviate state bloat, potentially even leading to changes in Ethereum's peer-to-peer structure. Blob transactions introduce a new data format for calldata (which rollups rely on), containing a large amount of additional data that is not accessed by EVM execution but can only be accessed for commitments. As the demand for rollup and modular execution grows, this new data market will become increasingly competitive. This means we may see price competitiveness, similar to the competitive gas prices we see on Ethereum, and we may see competitiveness around Data_gas, which is a new type of gas being implemented. There are still many questions to resolve, such as whether gas should be time-based or slot-based, as if it is slot-based, there is a possibility of missing a slot without blob transactions, which would make demand appear to increase, thus affecting gas prices.

Source: https://www.eip4844.com/

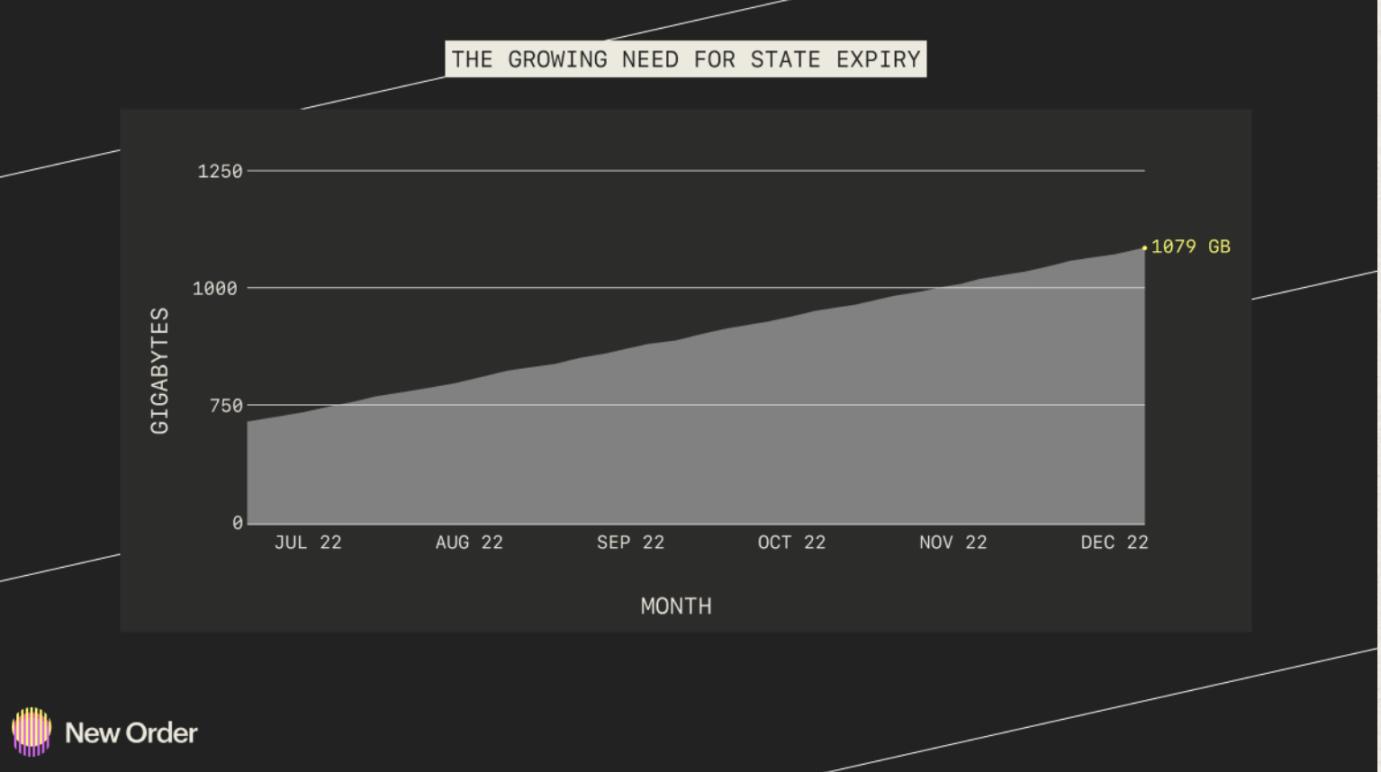

There are also practical gossiping issues with blob transactions on peer-to-peer (P2P) networks, as these blobs are significantly larger than anything currently being gossiped. This requires further research, and Paradigm is currently exploring it. It will be interesting to see what happens and whether the Ethereum network can handle this further state bloat and data. In any case, state expiry will likely be needed to limit the growth of Ethereum's state—currently, the growth of Ethereum's state has reached a staggering 1079 GB for full blockchain synchronization and is growing daily. State expiry will be achieved through state rent, allowing states to be rented to off-chain storage, or by periodically deleting states and storing them on archive nodes (which, unfortunately, are currently very centralized).

https://ycharts.com/indicators/ethereumchainfullsyncdata_size

As Ethereum and many L1s clarify their positioning in the coming years, it is evident that to maintain decentralization and "keep up with the times," they must turn to modularity.

4. ZK-Rollups will not see significant traction in 2023

ZK-Rollups will not gain significant traction in 2023 due to their lack of production readiness and inability to achieve sufficient decentralization. By production readiness, we specifically refer to their VM and proof verification times.

Conversely, ZKP is expected to see widespread use, particularly in non-interactive state proofs. Projects like Herodotus, Axiom, ETHStorage, and Lagrange will utilize them for various data-sharing purposes that require on-chain or cross-chain storage proofs.

Many cross-chain bridges are expected to start using ZKP for interoperability purposes, some of which are already moving in this direction, including Wormhole, Polymer, and the ZKBridge collective.

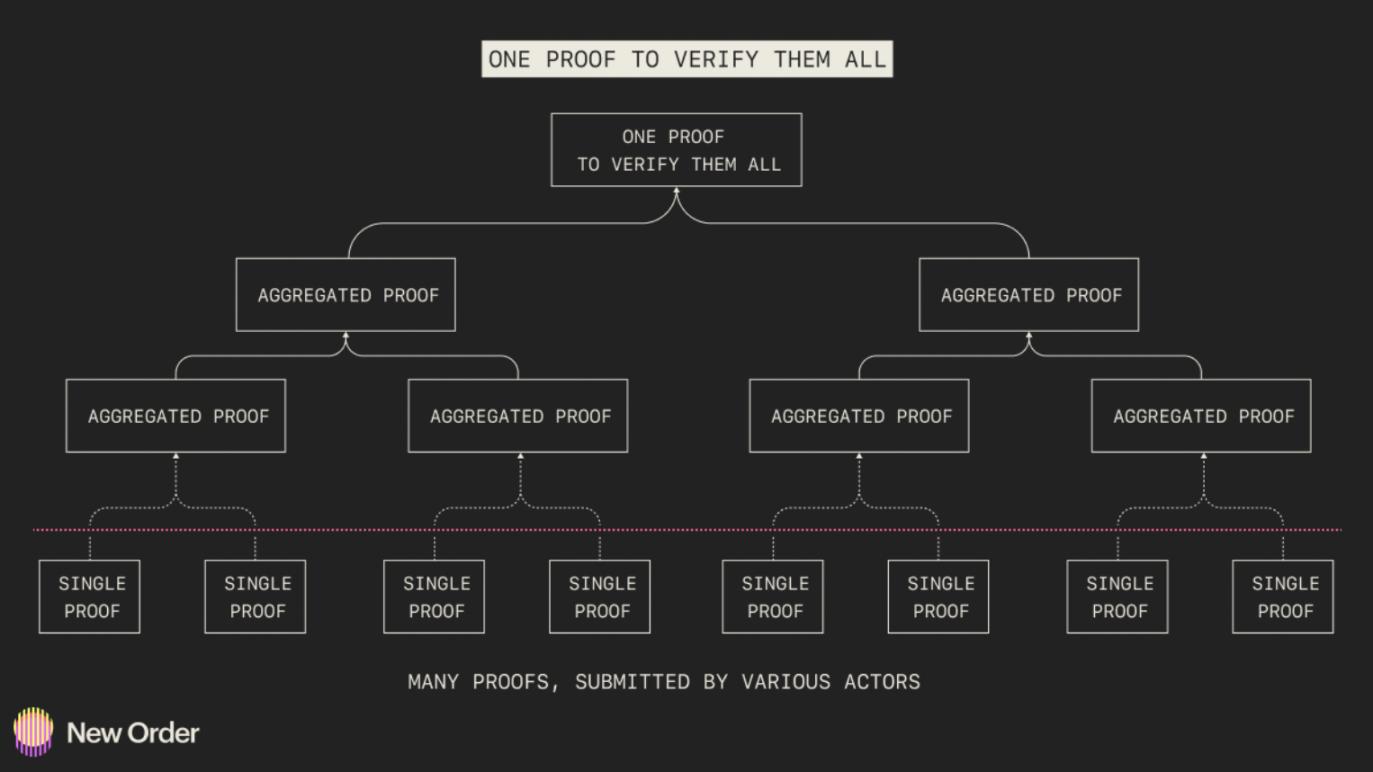

The applications of these ZKPs are nearly ready and are expected to enable on-chain verification at reasonable costs. The use of ZKPs improves efficiency through recursion, which involves aggregating multiple proofs into a smaller proof. Most protocols have recognized the need for recursive ZKPs to reduce costs and improve efficiency, although some proof schemes are more effective than others. However, it also comes with some caveats, as some proof schemes are more efficient than others.

https://ethresear.ch/t/reducing-the-verification-cost-of-a-snark-through-hierarchical-aggregation/5128

Many existing ZK schemes and algorithms with succinct proof sizes incur high overhead during proof generation time (also known as proof), which limits their efficiency and scalability. To address this issue, projects like Supranational, Ingonyama, and DZK are working to improve the efficiency of proof generation. However, it is important to recognize that this hardware acceleration is only part of the reason for efficient proofs. Optimizations are needed at the algorithmic level, software level, and beyond. Equally important is that the systems maintain sufficient decentralization, which is practically challenging to achieve.

https://eprint.iacr.org/2022/1010.pdf

Finally, proof times will also increase with the complexity of the relevant ZKP. Considering all the factors mentioned, it is undoubtedly challenging to establish a sufficient ZKRollup to gain significant traction in 2023. Currently, the most effective use of ZKP is in smaller-scale operations, such as the aforementioned non-interactive state proofs and interoperability.

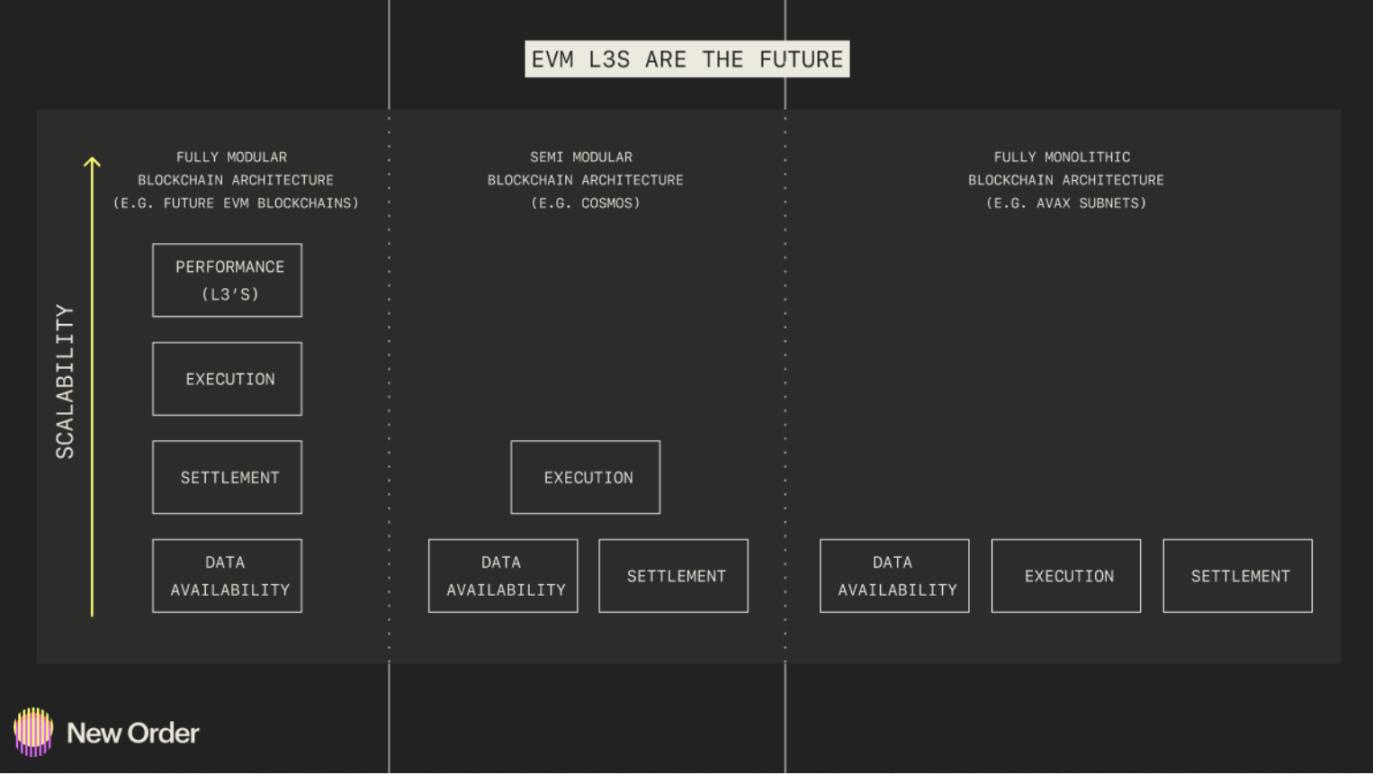

5. Layer 3 will be the true competitor to Cosmos

Layer 2 (L2) enhances Ethereum's scalability by reducing gas fees and increasing throughput. Due to these scalability factors and the trade-offs involved, L2 must optimize for specific projects. Layer 3 (L3) is an application-specific blockchain built on L2, designed to alleviate these trade-offs and make further improvements. They are similar to application chain environments like Cosmos, Avalanche, and Polkadot, but benefit from being built on a modular blockchain protocol stack rather than a monolithic chain protocol stack. Therefore, deploying a fully modular blockchain infrastructure stack, including a generic L2 and customizable L3, will mark the end of the era of monolithic application chain ecosystems and the beginning of a new era of decentralized application development.

https://medium.com/1kxnetwork/application-specific-blockchains-9a36511c832

Currently, monolithic application chains are the preferred choice for many applications, as this allows them to freely create custom logic and smart contracts while achieving better execution. Additionally, application chains have their own block space, so they do not have to compete with other chains for execution. However, this has not reached the efficiency it could achieve. Using a monolithic blockchain architecture, such as application chains built on modular software (like Cosmos) or as fully monolithic application chains (like Avax subnets), limits their ability to reduce transaction costs and increase computational throughput.

In contrast, application chains built on fully modular blockchain protocols reduce unnecessary friction, as they can leverage optimized blockchain layers built for specific functionalities. Suppose you build an L3 on top of zkSync (L2) that utilizes Celestia for data availability, leveraging Ethereum for settlement proofs and consensus, compared to a monolithic application chain that combines all or part of the layers. In this case, the only way forward is modular construction to achieve better scalability while retaining decentralization.

It is noteworthy that the metrics of these benefits exceed the theoretical goals that monolithic application chains can achieve. For instance, L2 reduces costs by 100 times compared to L1, while L3 reduces costs by 10,000 times compared to L1. The zkPorter L3 being built by zkSync improves scalability by reducing fees by about 100 times and achieving over 20,000 TPS. L3 not only provides improved performance but also allows for customization for specific purposes. This includes adding privacy features when using ZKP, designing custom DA models, and enabling efficient interoperability solutions.

Almost every relevant EVM L2 plans to develop customizable L3s on top of their L2. Additionally, opportunities will arise to build more modular blockchains using Celestia's shared data availability foundation. However, an important point to note for this prediction is that the future development of application chains will occur as L3s on modular blockchain stacks, rather than monolithic chains. Combining the decentralization and security of EVM with scalable L3s makes the modular environment far superior to the monolithic application chain ecosystem. Significant interoperability issues still need to be addressed, especially for cross-rollup transactions. However, we are making progress, and L3 is expected to launch by the end of 2023.

Therefore, if L3 can solve interoperability issues, deploying application chains built on modular blockchain technology stacks will be the death knell for the theory of monolithic application chains. L3 will retain a degree of Ethereum security, enhance speed and scalability, and allow dapps to be customized for specific use cases. Application chain ecosystems like Cosmos will continue to gain traction in 2023. However, as L3 is ultimately deployed in 2023, we will see the narrative of application chains shift from a monolithic chain ecosystem to a modular ecosystem.