After the hellish 2022 for the crypto market, will it get better next year?

Outlook 2023

Outlook 2023Original: 《Looking Ahead to 2023: Will the Crypto Industry Get Better or Worse? (Part 1)》

Author: Master Wuhuo, Plain Blockchain

After a hellish year in 2022, will 2023 be any better?

I think it will probably be a bit better, after all, it's hard to imagine how 2023 could "explode" and "de-leverage" again, especially since even FTX has collapsed. How much worse can it get? The only thing I can think of that could make the environment worse is an "epic" event like a leading CEX shutting down.

Following the thought process of reviewing the past, let's look at several aspects such as macroeconomics, public chains, DeFi, and NFTs to see what we can expect in 2023.

First, let me clarify that these are just things to look forward to. If you take this as the main investment theme for next year, you might end up with a slap in the face. After all, if you review the expectations and forecasts from various institutions and KOLs over the years, the accuracy rate is quite low.

This is also what makes this market interesting; it always develops in unexpected directions. Just like at the end of 2020, when everyone was looking forward to further innovations in DeFi, Polkadot, and Layer 2, unexpectedly, the hottest topic in 2021 turned out to be Alt Layer 1 Solana, along with stable Luna, GameFi Axie, and Cryptopunks NFTs. By the end of 2021, no one could have predicted that Luna would collapse in 2022, 3AC would go bankrupt, and FTX would shut down…

But similarly, don’t be afraid of being wrong; we still need to make predictions and outlooks!

01. Macro

The super major theme of 2022 forced every participant to become an economist, casually tossing around terms like interest rate hikes, balance sheet reduction, dot plots, and CPI.

However, if you ask this group of people (including me) to predict what the macro environment will be like next year, most would be dumbfounded. This is also a problem for amateur economists; they can barely explain the past. Predicting the future? Forget it… After all, even professional economics professors often struggle to see the future direction. If they could, we wouldn't have had the 2008 economic crisis.

However, there are at least a few relatively certain things you can understand:

Interest Rate Hikes

Interest rates have now reached the range of 4.25-4.50%. According to the dot plot, we will continue to raise rates next year until we get close to 5%. This event will likely occur in Q1 or Q2 of next year, meaning interest rate hikes will continue, but the pace will slow down. Don’t fantasize about a flood of liquidity and a Bitcoin surge next year.

Recession and Rate Cuts

Many people now believe that next year will see an economic recession. Whether it will happen and how severe it will be is unknown. But if it does happen, the current prices of crypto assets may not yet be affected by this expectation. So is there a possibility that Bitcoin will continue to decline next year? Of course, there is.

As for rate cuts, we will likely have to wait until the Federal Reserve's inflation target of 2% is achieved or nearly achieved. The timing? Maybe Q4 next year? Or even the year after. At that time, it will naturally be good for price support in the market, but prices will likely reflect this in advance. This means that a few months before the rate cut, if signs of a rate cut emerge, prices will start to rise, rather than waiting until the actual rate cut day. In financial markets, it's all about "expectations."

02. Public Chains

In 2023, the two prominent themes in public chains will undoubtedly be the "disaster zones" for speculation and investment.

- The first prominent theme is ZK

If nothing unexpected happens, we will see the mainnet launches of the four major ZK Layer 2s: Starknet, Zk-sync, Scroll, and Polygon ZKEVM in the first half of the year.

The OP series only has two (Arb and OP; yes, I’m directly ignoring Metis, Boba, and other forks, as they are not worth mentioning), while the ZK series has four… Thus, we can happily see that the already fragmented liquidity in Layer 2 is now even more fragmented.

In addition to the liquidity fragmentation issue, there are also performance considerations. The overall overhead of ZK is actually higher than that of OP. Although theoretically, ZK can achieve higher TPS and lower costs than OP when the blocks are full (because ZK requires less transaction data to be uploaded than OP, which needs to upload some intermediate state information for easier verification),

Initially, the first block is unlikely to be at full capacity, and there is still considerable room for circuit optimization and hardware acceleration. Therefore, at this time next year, the performance and costs of the ZK series will actually be at a disadvantage compared to the OP series. Whether users will pay for the "mathematics > game" security remains to be seen based on market performance at that time.

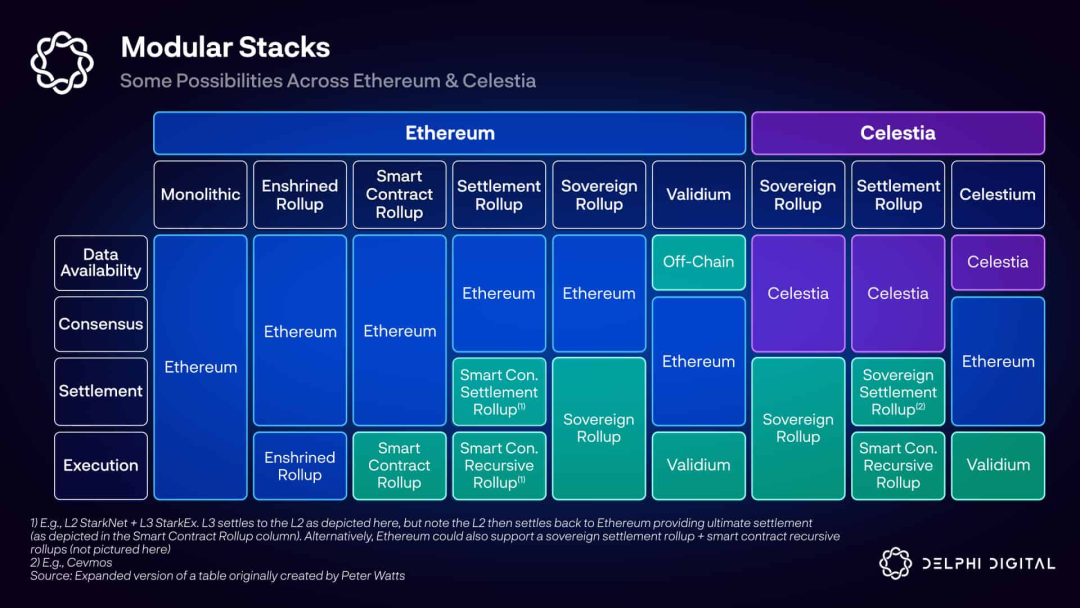

- The second prominent theme is the term modular blockchain

The term popularized by Celestia will also see its mainnet launch next year. The previous four-layer model has broken various Rollups into pieces, and the various combinations can leave those who don’t understand the technology feeling dizzy.

It’s time to see what’s real and what’s not.

However, I personally feel that this time next year is a bit uncertain for two reasons:

First, DA layers like Celestia rely heavily on a large number of Rollup-based Appchains. Major players like Arb, Op, and the ZK series are unlikely to use third-party DA layers; they will either use ETH or create their own solutions similar to Validium. Therefore, the true service targets of DA layers are Appchains. It feels like we are still 1-2 years away from a major explosion of Appchains;

Second, how much value DA layers can capture is actually unknown. After all, even ETH, which serves as both a settlement and DA layer, derives more value from the ecosystem and ideological aspects than from L2. If we really talk about how much Gas fees L2 contributes, it’s actually far less than the super DApps on L1, like Uniswap and Opensea. Once Proto-DankSharding is deployed and L2 fees drop another order of magnitude, it will be even less. At that point, if you extract DA again, Hmm… can capturing that little value justify the valuation of several billion?

Of course, our circle is not like Web2, where price-to-earnings ratios dominate. Just like back in the day when Solana nodes captured that little fee, can you say it justifies a market cap of tens of billions? Clearly not; narrative and sentiment often work much better than P/E ratios. Just look at Uni's token; it captures nothing, yet still has a market cap of tens of billions.

From a project perspective, the situation is as follows:

ETH

The Shanghai upgrade in the first half of the year canceled EIP4844 (Proto Danksharding) and focused solely on POS withdrawals, still maintaining ETH's usual sluggish style… Did you think EIP4844 would be smoothly deployed in the second half of the year? Hehe, to be honest, if this "super important upgrade for L2" is delayed until 2024, I won’t be surprised at all. ETH is great in many ways, as long as you are mentally prepared for delays, it is definitely the "Blizzard" of public chains - the leader in quality, but also the leader in procrastination.

Cosmos

The proposal for Atom 2.0 was ultimately rejected due to the inflation model, and the community is now embroiled in heated debates over new proposals. However, regardless, several technical solutions in Atom 2.0, such as shared security, are likely to be seen next year. The years 2023-2024 may be the most crucial two years for Cosmos. Whether the Appchain narrative can take off and whether the 2.0 shared security model can provide sufficient value capture for Atom will depend on these two years.

Solana

The deep entanglement with FTX and SBF caused Solana to suffer heavy losses during the FTX collapse, with a massive outflow of TVL and the entire DeFi ecosystem gradually withering. Many developers have also turned their attention to new chains like Aptos and Sui, with projects flocking to these new chains to "open branches." However, from a positive perspective, "unbinding" from SBF gives Solana the opportunity to transition from a "heavy capital chain" to a community chain. Projects like Serum, which have ultra-low circulation and ultra-high FDV, may fork out some community projects and perhaps have a different future. After all, in recent years, Solana has made significant contributions to technological innovation at the base layer of public chains.

Alt Layer 1

It can be said that the vast majority of Alt Layer 1s may have a tough time next year. With Arbitrum currently thriving and innovative projects emerging one after another, the launch of the four major ZK series next year means that Alt Layer 1's competitors are no longer ETH, but a host of Layer 2s. The experience is similar, security is inferior to Layer 2, and the developer ecosystem cannot compete. I really can’t think of a way out for most Alt Layer 1s; gradual decline may be the fate of most Alt Layer 1s, just like EOS and NEO. The only ones with a chance to break through may be the Move-based Aptos and Sui, which have both underlying innovation narratives and capital support.

03. DeFi - Spot Market

DeFi's innovation in the spot market has entered a relatively bottleneck period. In 2022, there were basically no standout projects; the only one that might be worth mentioning is Euler as a lending project. Isolated pools and permissionless systems can't really be called "innovation"; they are merely carving out a niche in a relatively mature market, aided by capital.

In the spot market, there are three directions worth looking forward to in 2023:

One is Dex and lending projects that differ from the current style. As on-chain infrastructure continues to improve, the spot market cannot always be dominated by AMM; Order Book will eventually reclaim half of the market. Order Book has already made some attempts on Solana, and high-speed DeFi chains like Sei, which have built-in Clob, as well as Dex based on Aptos and Sui, will definitely see one or two Order Book types competing for the AMM market. On the lending side, Mars, which is based on multi-chain deployment in Cosmos, is another lending product that differs from AAVE and Compound. This type of lending project, which uses IBC to span multiple chains and can be centrally managed, may see good development after the concept of application chains rises.

Another direction is auxiliary projects based on existing infrastructure, such as Arrakis Finance, which manages Uniswap V3 LP tokens to optimize LP returns. Or Morpho, which is a lending pool optimizer built on lending protocols like Compound/AAVE, shifting loans from a pooled mechanism to a peer-to-peer mechanism to provide better rates for both lending parties (with pool rates as a baseline). Curve has already seen a large number of ecological auxiliary projects represented by CVX, so it wouldn’t be surprising to see a few new ones emerge in 2023.

The last direction is naturally in the stablecoin sector. After the collapse of Luna, the market has developed a stronger demand for native stablecoins while simultaneously reaching a peak of distrust towards such "algorithmically stable" styles. The AAVE GHO and Curve crvUSD, which are set to debut in 2023, are both over-collateralized types, with the leading lending platform and stablecoin Dex producing stablecoins, which is quite fitting and justified. I hope they can create a "better DAI," because frankly speaking, the circle has long suffered from MakerDAO…

In the next part, we will discuss the outlook for DeFi derivatives, NFTs, GameFi, and other directions.