In-depth analysis of the differences in digital currency regulatory policies between Singapore and Hong Kong

Regulatory policies, current regulatory status, and possible future trends of the two major centers of digital currency.

Regulatory policies, current regulatory status, and possible future trends of the two major centers of digital currency.Author: Li Ke, PANews

The year 2022 was an extraordinary year in the history of digital currency development. In May, the largest algorithmic stablecoin, Luna, decoupled and collapsed, triggering a series of chain reactions, including the collapse of Three Arrows Capital and the liquidation of lending platforms Voyager and Celsius. Just as one wave subsided, another arose; in early November, the leading exchange FTX quickly collapsed under insolvency, with valuations of over a hundred billion dollars rapidly turning to dust. The FTX collapse caused hundreds of millions in investments from Temasek and Red Shirt Capital to become worthless, BlockFi announced bankruptcy, and Genesis was on the brink of bankruptcy. The FTX disaster further exacerbated the already weakened digital currency industry.

As the saying goes, "A loss may turn out to be a gain." A series of hacking incidents and collapses have spurred the arrival of strong regulation. For centralized institutions, the necessity of regulation has been further highlighted; only with appropriate regulatory policies can the industry develop healthily. To explore the current state of digital currency regulatory policies, PANews conducted an in-depth analysis of the regulatory policies in the two major centers of digital currency, Singapore and Hong Kong, attempting to understand their regulatory status and future directions regarding digital currency.

Hong Kong Digital Currency Regulation

Security Tokens

Security Token Offering (STO) refers to the issuance of tokens that possess traditional security attributes. The security attributes indicate that the tokens have certain asset or economic rights (such as equity and profit-sharing rights). In March 2019, the Hong Kong Securities and Futures Commission (SFC) issued a statement on the issuance of security tokens, stipulating that security tokens are considered "securities" under the Securities and Futures Ordinance and are thus regulated by Hong Kong securities laws. To promote and distribute security tokens (whether in Hong Kong or targeting Hong Kong investors), one must obtain a license or register under the Securities and Futures Ordinance for regulated activity (securities trading). Anyone engaging in the above activities without a license, unless exempted, will face penalties and fines.

Virtual Asset Tokens

On June 24, 2022, the Hong Kong government published the "2022 Amendment Bill on Anti-Money Laundering and Counter-Terrorist Financing" (hereinafter referred to as the Amendment Bill) in the Gazette, which has passed its second reading and is currently under review by the Hong Kong Legislative Council, expected to come into effect on March 1, 2023.

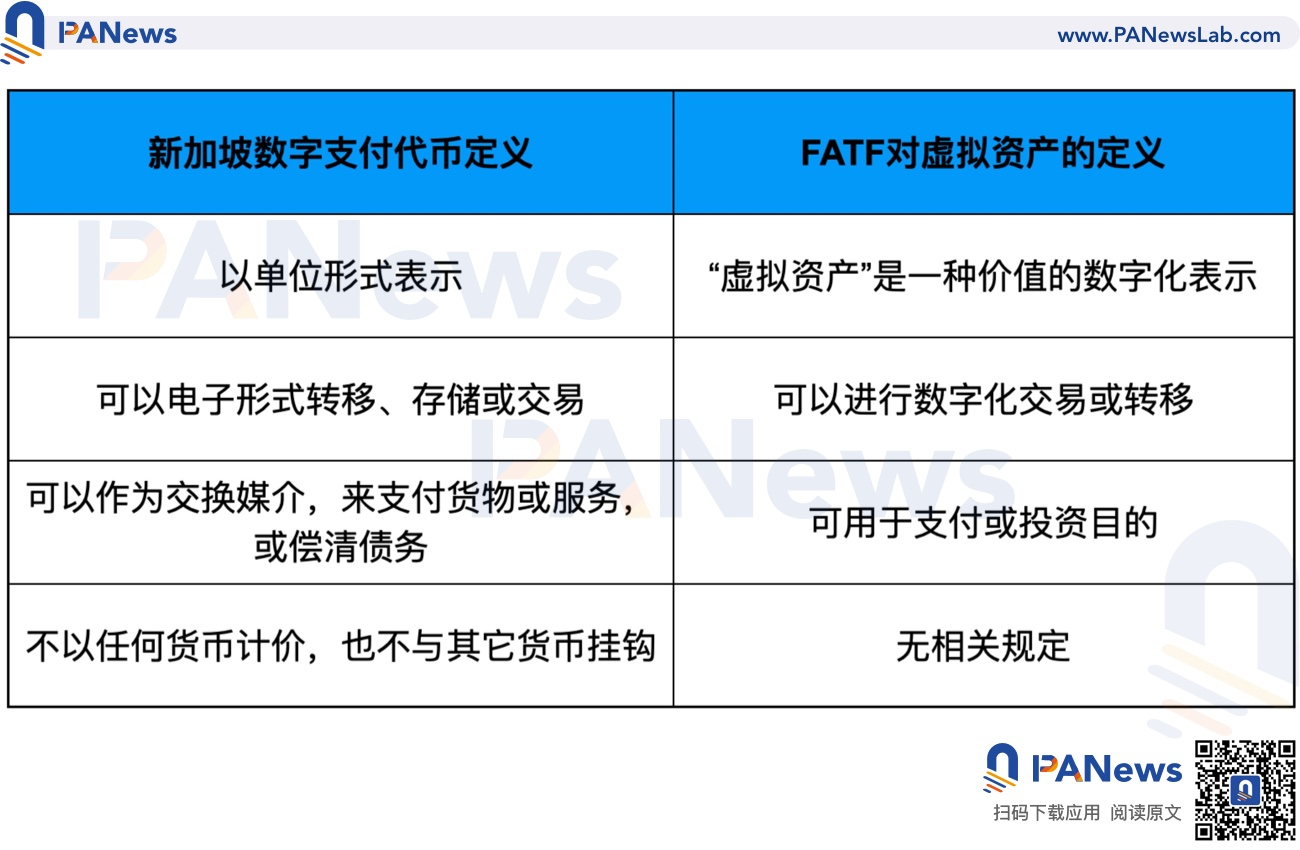

The Amendment Bill defines virtual assets, stipulating that (1) virtual assets are a form of encrypted digital value expressed through computational units or stored economic value; (2) they can be used as a medium of exchange for goods or services, to settle debts, for investment, or for voting on matters related to virtual assets; (3) they can be transferred, stored, or traded electronically; (4) the SFC or the Secretary for Financial Services and the Treasury can expand the definition of "virtual assets" through publication in the Gazette.

Hong Kong's definition of virtual assets is based on the standards set by the Financial Action Task Force (FATF). The FATF is one of the most influential and authoritative international organizations in the field of anti-money laundering and counter-terrorist financing, with member countries spanning major financial centers across continents. The FATF's "Forty Recommendations on Anti-Money Laundering" and "Nine Special Recommendations on Counter-Terrorist Financing" are the most authoritative documents in the world on these matters. The FATF's 2021 risk guidelines on virtual assets provide a clear definition: "virtual assets" are a digital representation of value that can be digitally traded or transferred and can be used for payment or investment purposes.

It is noteworthy that the Amendment Bill excludes security and futures tokens, as well as central bank digital currencies (CBDCs), from the definition of virtual assets. This aligns with the FATF's risk guidelines on virtual assets, as CBDCs and securities fall under other types of financial assets previously defined by the FATF, such as securities, commodities, futures, derivatives, and fiat currencies, while virtual assets represent an emerging asset class.

Exchanges

Prior to this, Hong Kong regulators applied the principle of "same business, same risk, same rules" to regulate digital currency exchanges under the existing Securities and Futures Ordinance. In November 2019, the SFC published a position paper on regulating virtual asset trading platforms, proposing a voluntary licensing application system, allowing virtual asset exchanges to apply for licenses "selectively."

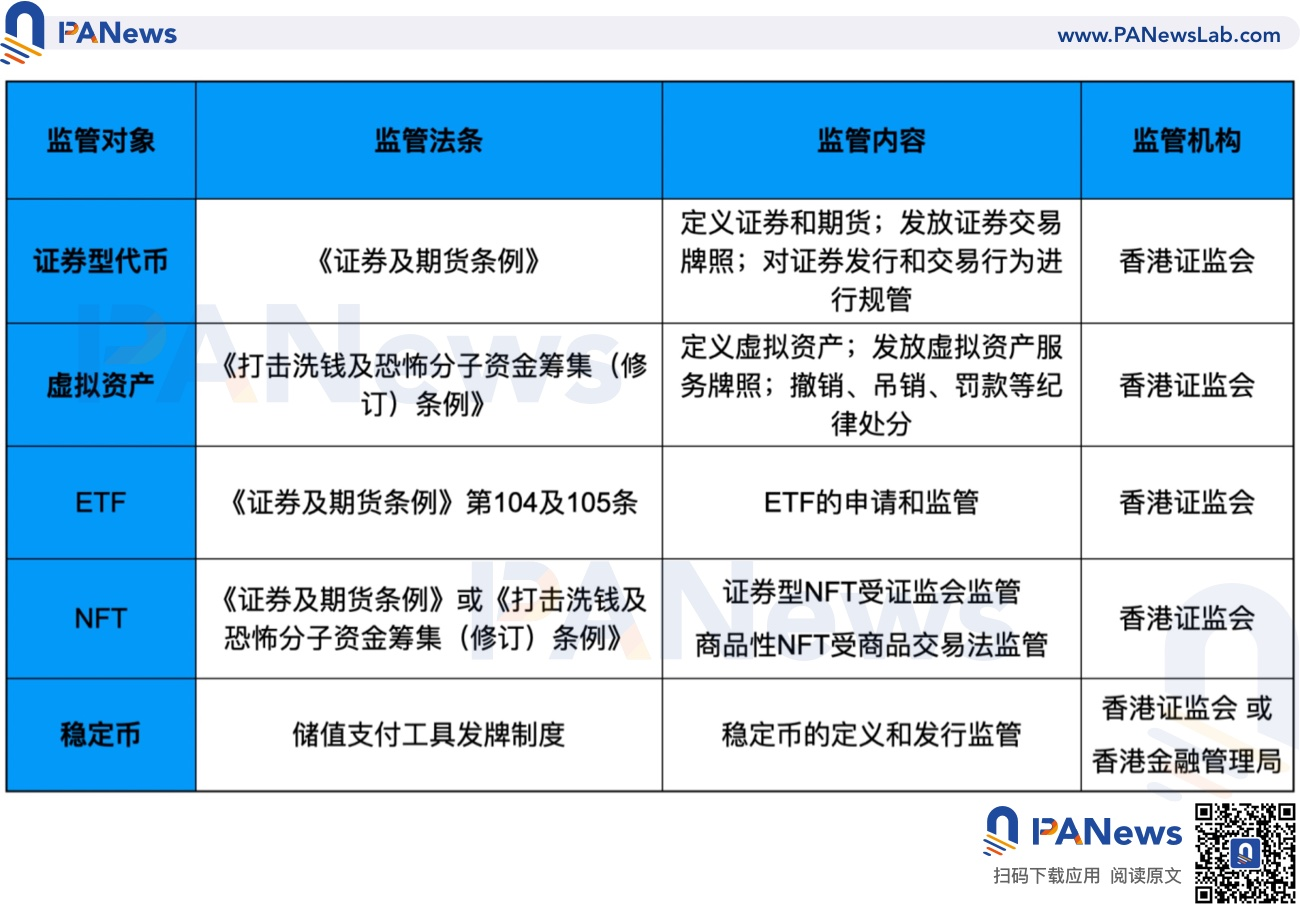

In Section 1, Part 4 of the position paper, the SFC stated that it does not have the authority to license or regulate platforms that only trade non-security virtual assets or tokens, as such virtual assets do not fall under the definition of "securities" or "futures contracts" in the Securities and Futures Ordinance. This indicates that under the current regulatory framework, only platforms providing trading services for security tokens fall within the SFC's regulatory scope. In this context, Hong Kong digital currency exchanges OLS and Hashkey obtained licenses under the Securities and Futures Ordinance for Type 1 (securities trading) and Type 7 (automated trading services), while Huobi Technology obtained Type 4 (advising on securities) and Type 9 (asset management) licenses.

Based on the definition of virtual asset tokens in the previous section, virtual assets do not belong to security tokens and are not subject to the Securities and Futures Ordinance. In this case, a new licensing system is needed to regulate virtual asset token exchanges. Therefore, the recently amended "Anti-Money Laundering and Counter-Terrorist Financing Ordinance" will introduce a new mandatory licensing system for virtual asset exchanges and define virtual asset services to primarily include operating exchanges for virtual assets (including decentralized exchanges). The bill also clearly states that the SFC will be the approving and regulatory authority for virtual asset exchanges, and operating virtual asset services in Hong Kong requires a regulatory license; otherwise, it constitutes an offense, punishable by a fine of 5 million HKD and up to seven years in prison.

Stablecoins

In May 2021, the Hong Kong Financial Services and the Treasury Bureau mentioned in the public consultation summary of the legislative proposal to strengthen anti-money laundering and counter-terrorist financing regulations that the FATF's definition standard for virtual assets—"can be traded or transferred; can be used for payment or investment"—applies to various forms of virtual assets, regardless of their stability. Therefore, stablecoins will also be regulated under this ordinance, as stablecoins can be traded or transferred and can be used for payment.

The Hong Kong Monetary Authority ("HKMA") released a discussion paper on "Crypto-assets and Stablecoins" in January 2022, and the consultation results will be published soon. It is believed that further regulatory policies regarding stablecoins will be introduced. The aforementioned discussion paper explored Hong Kong's current regulatory framework for stablecoins and sought public and industry opinions on whether stablecoins should be classified as stored-value payment instruments and how they should be regulated. The HKMA indicated that it may draw on the existing regulatory framework under the "Payment Systems and Stored Value Facilities Ordinance" to regulate the issuance of stablecoins and implement a licensing system for stored-value payment instruments.

Through the May Luna stablecoin decoupling incident, we see that Hong Kong's regulatory considerations for stablecoins are relatively advanced, having released a discussion paper on stablecoins in January this year, mentioning seven related risks: financial stability risk, currency stability risk, computational risk, user protection risk, financial and cybercrime risk, international compliance, and regulatory arbitrage risk, along with a series of regulatory justifications and public consultations.

About ETFs

On the same day the Hong Kong government announced the "Policy Declaration on the Development of Virtual Assets," the SFC issued a circular stating that it would authorize the public offering of virtual asset futures exchange-traded funds (ETFs) in Hong Kong for the first time under Sections 104 and 105 of the Securities and Futures Ordinance. The SFC only allows index funds to be issued for virtual asset futures traded on traditional regulated futures exchanges, initially approving only Bitcoin futures and Ethereum futures index funds traded on the Chicago Mercantile Exchange, with further categories considered on a discretionary basis. The circular indicates that ETFs must meet trust and fund management requirements, and the ETF issuer must demonstrate at least three years of track record and compliance history. The issuer will need to prove that the ETF has sufficient liquidity, and the net derivative exposure cannot exceed 100% of the ETF's net asset value. The issuer must also conduct necessary investor education before launching the ETF.

About NFTs

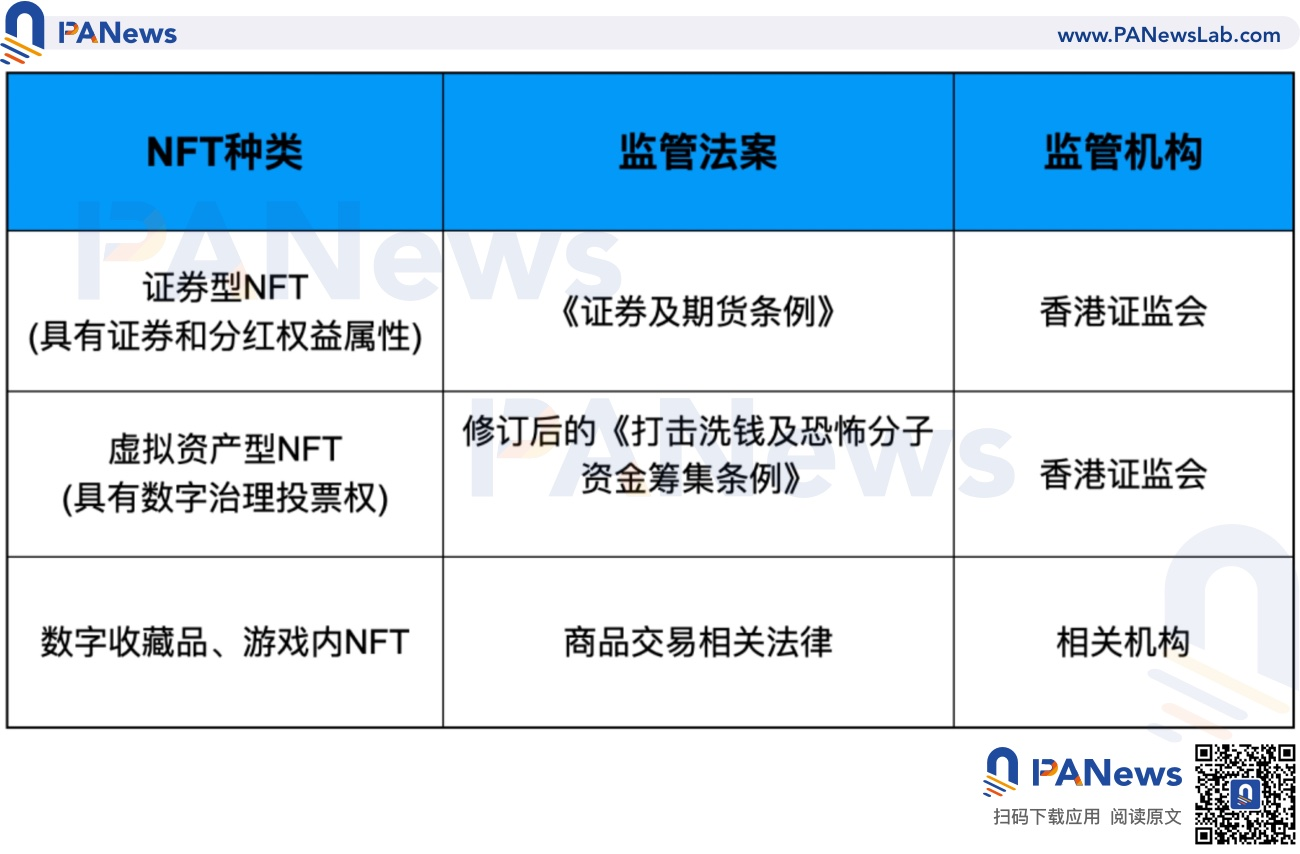

The "2022 Amendment Bill on Anti-Money Laundering and Counter-Terrorist Financing" in Hong Kong stipulates that NFTs used within games do not fall under the category of virtual assets. When the SFC issued a reminder on June 6, 2022, regarding the risks of non-fungible tokens (NFTs), it stated that if an NFT is a digitally existing collectible (such as an electronic image, artwork, music, or video), the related activities do not fall under the SFC's regulatory scope under the Securities and Futures Ordinance. However, some NFTs cross the boundary between collectibles and financial assets and may possess the securities attributes of "securities" or "interests under collective investment schemes" regulated by the Securities and Futures Ordinance, and thus will be subject to regulation.

It can be seen that the regulation of NFTs cannot be generalized. NFTs are essentially tokens, and depending on the asset attributes they represent, they will be handled in three different scenarios. NFTs with securities rights and profit-sharing attributes will be regulated as security tokens by the SFC; NFTs with governance voting rights will be regulated as virtual assets; while NFTs used in games or as electronic goods and collectibles will not be regulated under the Securities and Futures Ordinance or the Amendment Bill, and will be treated as ordinary virtual goods, subject to traditional commodity trading laws.

Overall, Hong Kong is establishing a comprehensive and targeted regulatory policy for digital currencies.

For security tokens, they are regulated under the Securities and Futures Ordinance based on the principle of "same business, same risk, same rules."

For virtual assets, the upcoming "Anti-Money Laundering and Counter-Terrorist Financing (Amendment) Ordinance" will classify virtual assets separately and introduce a new regulatory and licensing system.

For stablecoins, they will be regulated as virtual assets and may be combined with the existing regulatory framework for stored-value payment instruments, while also being subject to the "Payment Systems and Stored Value Facilities Ordinance."

For NFTs, there is currently no one-size-fits-all regulatory policy; some NFTs with securities rights are classified as security tokens for regulation, some NFTs with governance voting rights are regulated as virtual assets, while NFTs used as points or for gaming purposes will not be subject to the above regulations.

Singapore Digital Currency Regulation

Security Tokens

As a supplement to the Securities and Futures Act, the Monetary Authority of Singapore (MAS) released the "Guidelines on Digital Token Offerings" on November 14, 2017, which was revised on May 26, 2020. The guidelines stipulate that if a digital token falls under the definition of capital market products (CMP) as defined by the Securities and Futures Act (SFA), it will be regulated by the MAS. Capital market products include securities, bonds, derivative contracts, collective investment schemes, etc. The "Guidelines on Digital Token Offerings" also include intermediaries providing security token issuance services under regulation, requiring these intermediaries to hold capital markets services licenses, financial advisory licenses, or to be approved exchanges by the MAS.

Digital Payment Tokens

On January 14, 2019, Singapore passed the "Payment Services Act" (PSA), which includes seven types of payment services under the licensing regime: (1) account issuance, (2) domestic remittance, (3) cross-border remittance, (4) merchant payments, (5) electronic money issuance, (6) digital payment token (DPT) services, and (7) currency exchange. The PSA defines digital payment tokens (DPT) as cryptocurrencies used for payment purposes (such as Bitcoin BTC and Ethereum ETH).

Similar to Hong Kong's definition of "virtual assets," Singapore's definition of "digital payment tokens" also draws on the standards set by the FATF. A comparison shows that Singapore's digital payment tokens, Hong Kong's virtual assets, and the FATF's definition of virtual assets refer to the same type of asset.

Additionally, the PSA stipulates that providing DPT services in Singapore, including buying, selling, or trading DPTs, requires a license issued by the MAS and compliance with the PSA's anti-money laundering and counter-terrorist financing regulations.

On January 4, 2021, the Singapore Parliament passed the "Payment Services (Amendment) Act" to align with the FATF's regulatory requirements on anti-money laundering and counter-terrorist financing. The amendment expanded the scope of DPT service providers to include those offering DPT transfers, DPT wallet custody, and decentralized DPT trading services, further regulating digital payment services and enhancing anti-money laundering and counter-terrorist financing oversight.

On January 17, 2022, the MAS released "Guidelines on Providing DPT Services to the Public," indicating that digital payment tokens (DPT) are highly risky and unsuitable for public participation. DPT service providers are required to avoid promoting DPT services in public places or on social media, and can only promote their DPT services on company websites and applications.

In April 2022, the Singapore Parliament reviewed and passed the "Financial Services and Markets Bill" (FSM), requiring digital token issuers and service providers to obtain valid financial licenses and imposing higher anti-money laundering and counter-terrorism financing requirements. The FSM bill, referencing FATF standards, expanded DPT services to include direct or indirect trading, exchange, transfer, custody of cryptocurrencies, or providing related investment advice, and broadened the regulatory scope to cover cryptocurrency service providers established in Singapore but serving outside Singapore.

On October 26, 2022, Singapore released a public consultation document on regulatory measures for digital payment token services, planning to further refine the regulatory policies for DPT services to mitigate risks in DPT transactions and protect investors.

Stablecoins

On October 26, 2022, the MAS issued a proposed regulatory policy consultation document regarding stablecoins, stating that if well-regulated, stablecoins have the potential to serve as reliable digital exchange mediums.

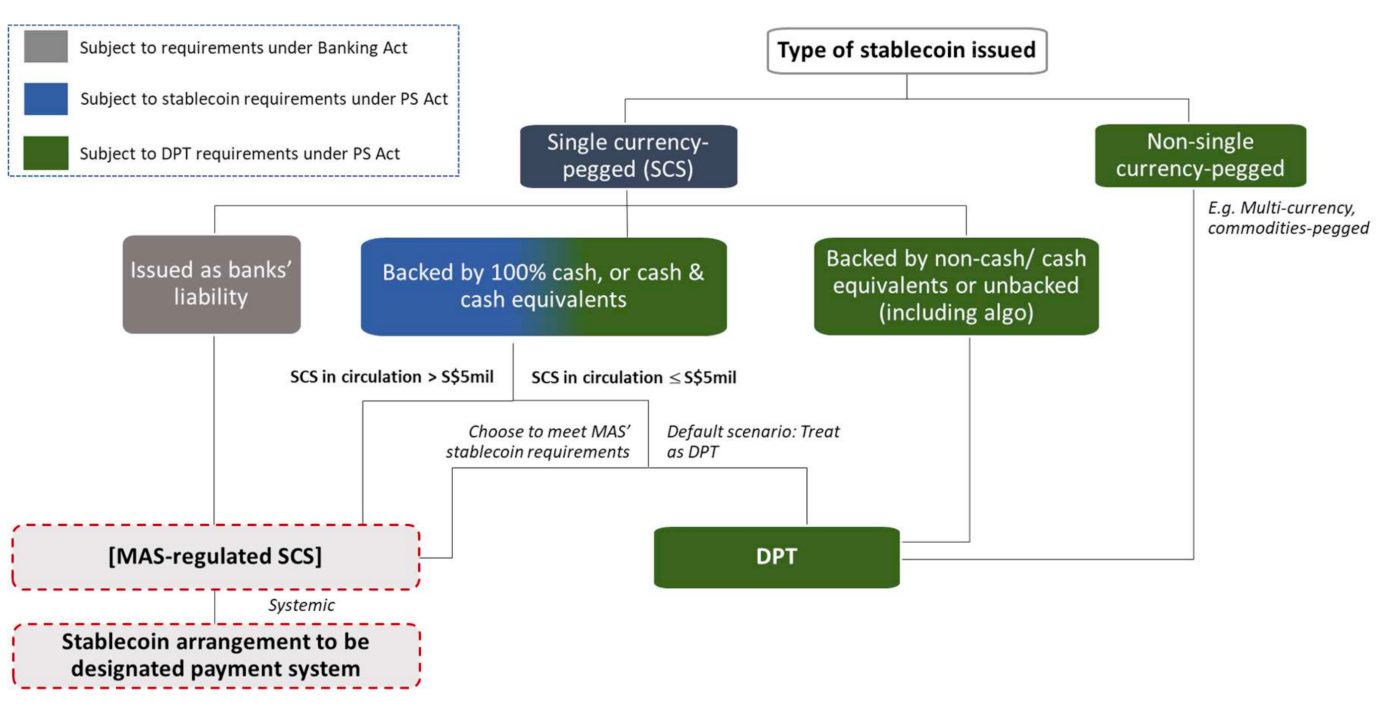

Under the current PSA, stablecoins are regarded as digital payment tokens (DPT) and are subject to corresponding regulation. The MAS believes that as Singapore seeks to develop a digital asset ecosystem, it is necessary to establish a new regulatory framework for stablecoins. The current regulatory framework under the PSA is insufficient to achieve this goal, as it lacks mechanisms to ensure stablecoins maintain value stability.

Currently, there are various stablecoins based on different pegged assets and stability mechanisms. The MAS intends to focus its regulatory efforts on single-currency pegged stablecoins (CSC) and stablecoins issued in Singapore. The MAS plans to introduce a new provision in the Payment Services Act (PSA) to regulate "stablecoin issuance services," aiming to maintain high value stability for SCS.

About NFTs

NFTs are essentially tokens, so some NFTs may be classified as security tokens, some may belong to digital payment tokens, while others may not fall into either category. Therefore, it is necessary to individually assess the underlying value attributes represented by NFTs to determine how they should be regulated.

The MAS states that the emerging NFT market is still in its infancy, and there are no targeted regulatory plans for NFTs. However, it may assess whether NFTs fall under the MAS's regulatory scope based on specific circumstances. If the underlying asset represented by an NFT has securities characteristics, such as representing shares or profit rights, it will need to meet the MAS's regulatory requirements. If an NFT possesses characteristics defined as digital payment tokens under the Payment Services Act (PSA), the supplier of that NFT may face certain restrictions and requirements.

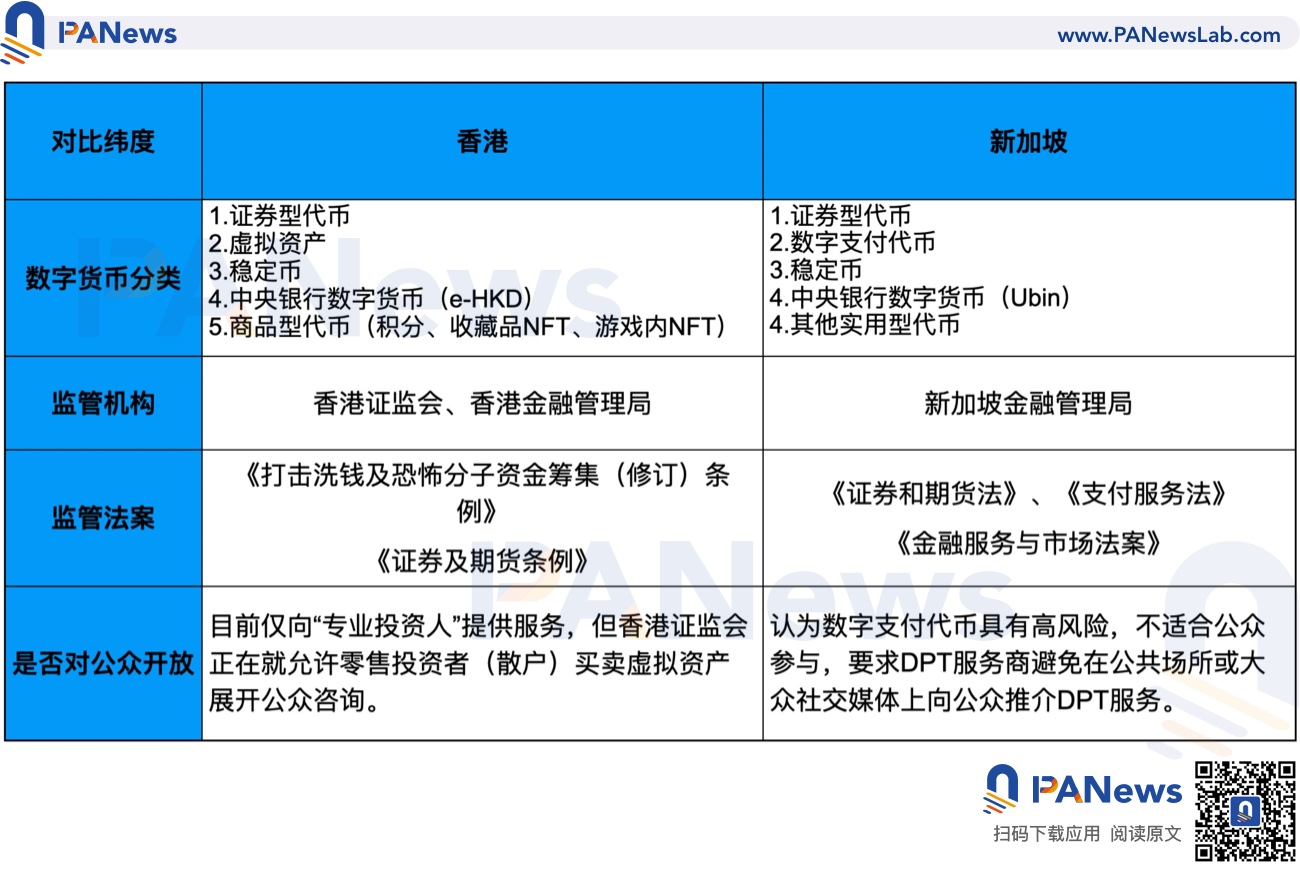

Overall, the MAS is Singapore's central bank and comprehensive financial regulatory authority, dividing the financial industry into four categories: banking, securities, insurance, and payment services, and establishing targeted licensing and regulatory policies. The HKMA follows the previous regulatory logic for the securities and payment industries, classifying digital currencies into security tokens and digital payment tokens for regulation, forming a matching relationship in business logic.

Similarities and Differences in Regulatory Policies between Hong Kong and Singapore

By comparing the digital currency regulatory policies of Singapore and Hong Kong, we find that the regulatory policies of a country (or region) are closely related to the business scope of its regulatory agencies and the existing legal framework of that country (or region). For example, the main business scope of Singapore's regulatory authority, the MAS, is to regulate banking, securities, insurance, and payment services. Therefore, Singapore classifies digital currencies into security tokens and payment tokens for separate regulation. The SFC in Hong Kong is responsible for regulating traditional securities, so it has primarily regulated security tokens until now. However, some tokens do not fall under the category of security tokens, leaving the regulation of non-security tokens in a long-standing vacuum. The United States has independent regulatory bodies such as the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC), along with different Securities Exchange Acts and Commodity Futures Trading Acts, leading to differing opinions on whether to classify digital currencies as security tokens or commodity tokens and who should regulate them.

Singapore and Hong Kong have both similarities and differences in their regulation of digital currencies.

In the regulation of security tokens, there is already a relatively mature regulatory system for securities. Therefore, both Singapore and Hong Kong apply existing securities regulatory policies to regulate through the Securities and Futures Ordinance or the Securities and Futures Act.

In the regulation of non-security tokens, Singapore tends to establish entirely new regulatory laws, having enacted the Payment Services Act (PSA) and the Financial Services and Markets Bill (FSM) to classify most non-security tokens as digital payment tokens (DPT) for regulation. Hong Kong is more inclined to amend existing laws to cover digital currency regulation, such as revising the original Anti-Money Laundering and Counter-Terrorist Financing Ordinance to classify non-security tokens as virtual assets for regulation.

In the regulation of stablecoins, Singapore and Hong Kong share many commonalities. On one hand, they both regulate stablecoins as digital payment tokens or virtual assets, and the virtual assets defined by Hong Kong and the digital payment tokens defined by Singapore are essentially very similar. On the other hand, both Singapore and Hong Kong have taken further measures to regulate stablecoins. Hong Kong may combine the Payment Systems and Stored Value Facilities Ordinance for regulation, while Singapore intends to add regulatory provisions for stablecoins under the Payment Services Act (PSA).

Both Singapore and Hong Kong place significant emphasis on the regulation of stablecoins. On one hand, they recognize the important role stablecoins play in building a global digital currency center; on the other hand, they have taken targeted measures in response to the collapse of the Luna stablecoin this year.

Additionally, regarding central bank digital currencies (CBDCs), Singapore launched the Ubin project for central digital currency in 2016 for cross-border real-time settlement, which is currently in its fifth phase. The Hong Kong government began exploring the central bank digital currency e-HKD in 2017, aiming to implement the digital Hong Kong dollar through three phases.

As competitors vying for the digital currency center in Southeast Asia, both Singapore and Hong Kong adopt an inclusive and open attitude in regulating digital currencies. They embrace and encourage technological innovation while implementing supporting regulatory policies to properly manage risks and protect investors. From the similar regulatory strategies adopted by Singapore and Hong Kong across different dimensions, we can roughly understand the development direction of digital currency regulation. Good industry regulation is a prerequisite for the orderly and vigorous development of the market, and the responsible regulatory attitudes of Singapore and Hong Kong give us hope for the development of the digital currency industry.

References:

Public Consultation on Legislative Proposals to Strengthen Anti-Money Laundering and Counter-Terrorist Financing Regulations in Hong Kong

Summary of Public Consultation on Legislative Proposals to Strengthen Anti-Money Laundering and Counter-Terrorist Financing Regulations in Hong Kong

"2022 Amendment Bill on Anti-Money Laundering and Counter-Terrorist Financing"

Position Paper: Regulating Virtual Asset Trading Platforms

Statement on the Issuance of Security Tokens

SFC Reminder on the Risks of Non-Fungible Tokens

Consultation Paper on Proposed Regulatory Measures for Digital Payment Token Services

Discussion Paper on Crypto-assets and Stablecoins

Guidelines on Provision of Digital Payment Token Services to the Public PS-G 02

Guidelines to Notice PSN 02 on Prevention of ML and Countering the Financing of Terrorism

Guidelines on Provision of Digital Payment Token Services to the Public PS-G 02

Proposed Regulatory Approach for Stablecoin Related Activities

Singapore Payment Services Act 2019

Singapore Payment Services (Amendment) Act 2021

Virtual Assets and Virtual Asset Service Providers by FATF

Risk warning

Risk warning Risk warning

Risk warning