The 7 "Calabash Brothers" of DCG collectively face the volcano: Grayscale is losing competitiveness, and exchange Luno's trading volume is extremely low

How are the other subsidiaries under DCG developing, and can they help DCG get through the tough times?

How are the other subsidiaries under DCG developing, and can they help DCG get through the tough times?Written by: PANews, Jiang Haibo

Genesis has encountered multiple pitfalls in events involving Luna/UST, Three Arrows Capital, Babel, and FTX/Alameda, ultimately announcing a suspension of redemptions and new loan issuances on November 16. As it sought financing and was rejected by several institutions, the likelihood of Genesis securing investment has diminished over time, with bankruptcy becoming a potential final outcome. Given the debt relationship between Genesis and DCG, if Genesis goes bankrupt, DCG could be affected as well. How will the other subsidiaries under DCG fare, and can they help DCG weather the storm?

Genesis Faces a $1 Billion Shortfall; DCG May Be Insolvent

Genesis's troubles began with the LUNA incident. In May of this year, the Luna Foundation Guard (LFG) exchanged $1.5 billion worth of UST for an equivalent value of BTC from Genesis and 3AC. Genesis may have paid $1 billion in BTC in this transaction, and depending on Genesis's business model, it might have acted merely as a broker. The specifics of the transaction remain unclear, but if the former is true, Genesis has already lost $1 billion in this deal.

After the liquidation of 3AC, Genesis still had $1.2 billion in bad debts. Its parent company, DCG, stated it would inject capital to cover this loss, but the funds have not actually arrived.

Following FTX's bankruptcy, Genesis's derivatives department reported having $175 million in funds in FTX accounts. However, according to analysis from Arkham Intelligence, Genesis had previously received over $1 billion worth of FTT from FTX and Alameda Research, and may have additional loans from FTX/Alameda, leading to an overall loss of over $1 billion for Genesis in this incident.

Ultimately, Genesis faced a liquidity crisis. For more information about Genesis, you can read: "Genesis on the Brink of Bankruptcy: 500 Million Financing Puzzles DCG, Once Encouraged 3AC to Borrow"

As a subsidiary of DCG, if DCG and Genesis maintain an independent relationship, Genesis could file for bankruptcy without affecting DCG's other businesses. However, there are significant financial transactions between Genesis and DCG.

According to a letter from DCG CEO Barry to shareholders, DCG previously borrowed approximately $575 million from Genesis Global Capital, with the debt maturing in May 2023. After 3AC defaulted, DCG assumed 3AC's liabilities to Genesis, holding a promissory note worth $1.1 billion that matures in June 2032. Additionally, DCG has a $350 million debt owed to creditors such as Eldridge. The total debt amounts to approximately $2 billion.

DCG raised $700 million at a $100 billion valuation from institutions like SoftBank at the peak of the bull market in late 2021. Based on this, DCG may now be insolvent. Taking Grayscale, DCG's "cash cow," as an example, Grayscale charges a 2% management fee on its assets. Over the past year, the issuance of GBTC has not increased, while the price of BTC has dropped from $67,000 to $16,700, a decline of 75%. Grayscale's revenue has also seen a corresponding drop, and considering the different earnings expectations in bear and bull markets, Grayscale's valuation may have decreased even more significantly.

DCG and Genesis are now tied to the same chariot; it's no longer a question of whether to save Genesis, but whether it can be saved. This depends on the operational status of several other subsidiaries in DCG's portfolio.

Grayscale: Diminished Competitiveness, No New Subscriptions

Currently, the most valuable part of DCG's portfolio may be Grayscale, which manages billions of dollars in BTC and enjoys a 2% annual management fee.

Due to the failure of Grayscale's products to impact the BTC spot ETF, its trust products cannot be redeemed. With the approval of Bitcoin ETFs in Canada, Grayscale is losing its competitive edge.

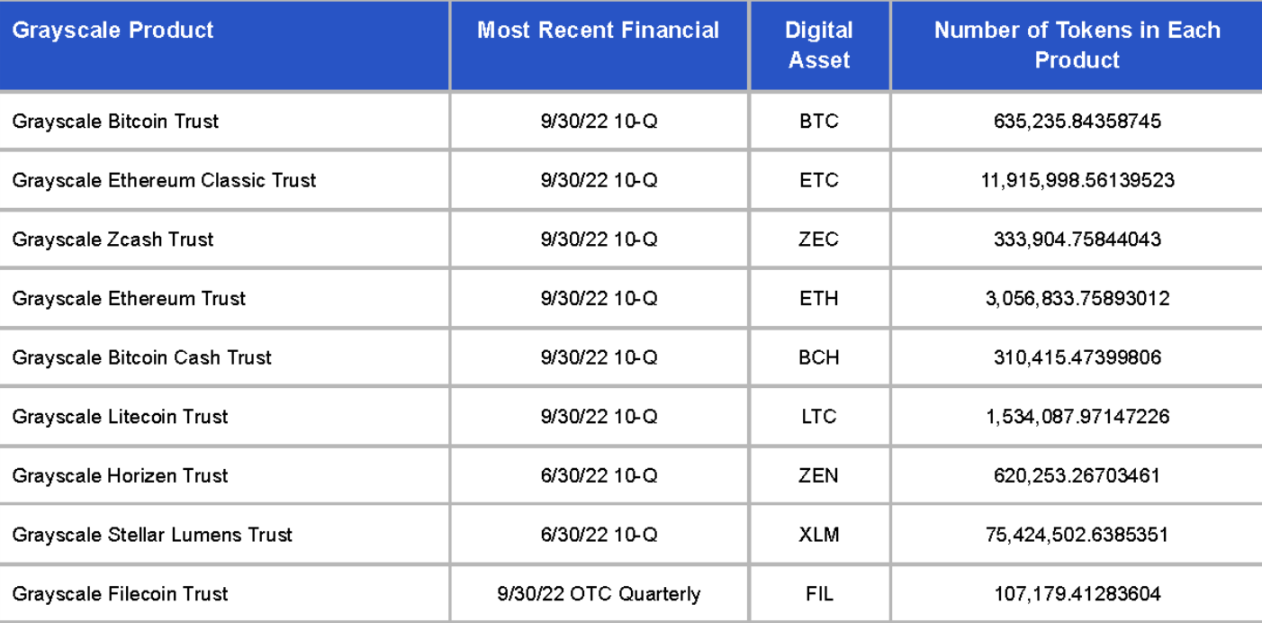

As of November 24, Grayscale holds BTC worth $10.466 billion, ETH worth $3.573 billion, ETC worth $1.668 billion, LTC worth $697 million, and BCH worth $102 million, along with other holdings like BCH, ZEC, MANA, and XLM valued under $100 million.

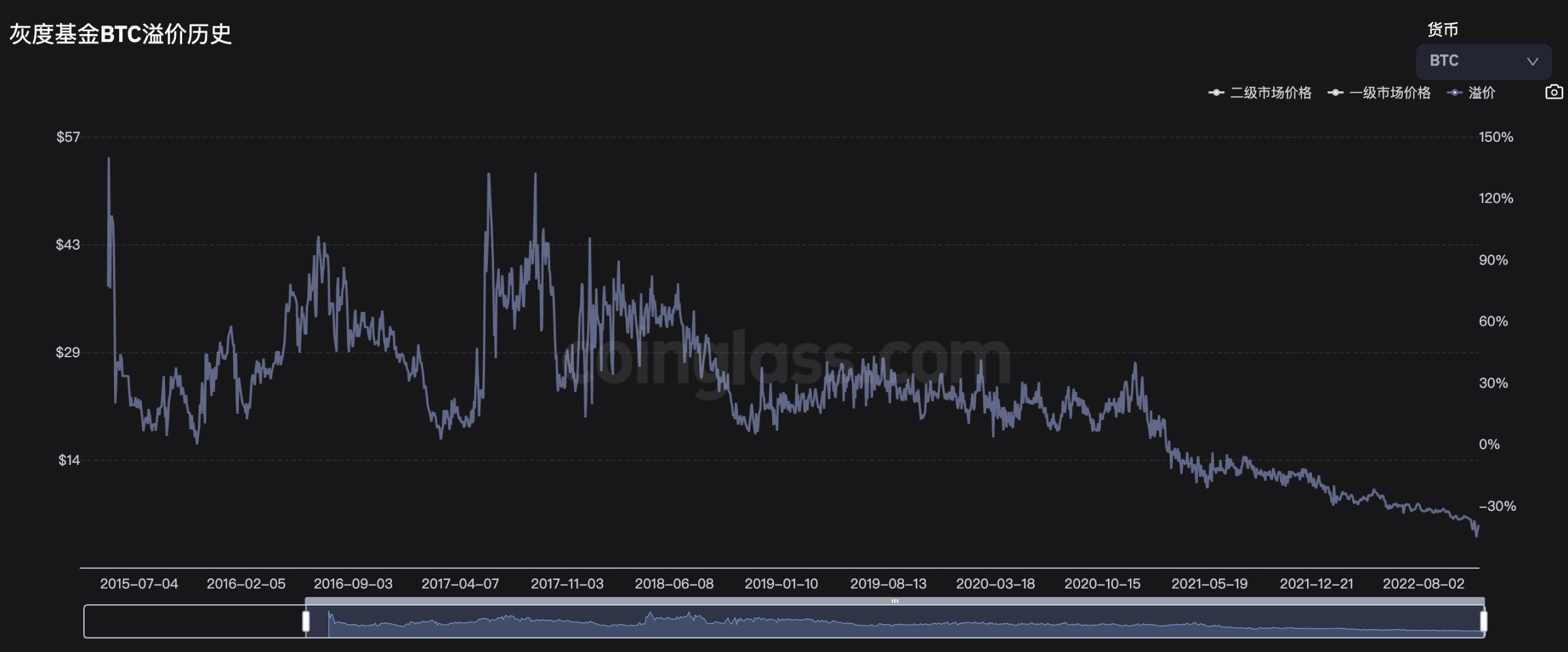

Grayscale's website publishes the assets contained in each share of its trust products. For example, to assess the premium of GBTC, one can multiply the amount of BTC each GBTC share contains by the real-time BTC price and compare it with the price of GBTC in the OTC market.

According to data from Coinglass, GBTC maintained a positive premium for several years before March 2021. Qualified investors could purchase GBTC through Grayscale with cash or BTC and sell it in the OTC market six months later to complete arbitrage. From May to October 2017, GBTC's premium was consistently above 50%, even reaching as high as 130% during certain periods.

However, starting in March 2021, the premium for GBTC disappeared, making it less advantageous to purchase GBTC than to buy directly in the OTC market, leading to a complete halt in new subscriptions. As of November 24, GBTC's premium had dropped to -39.2%.

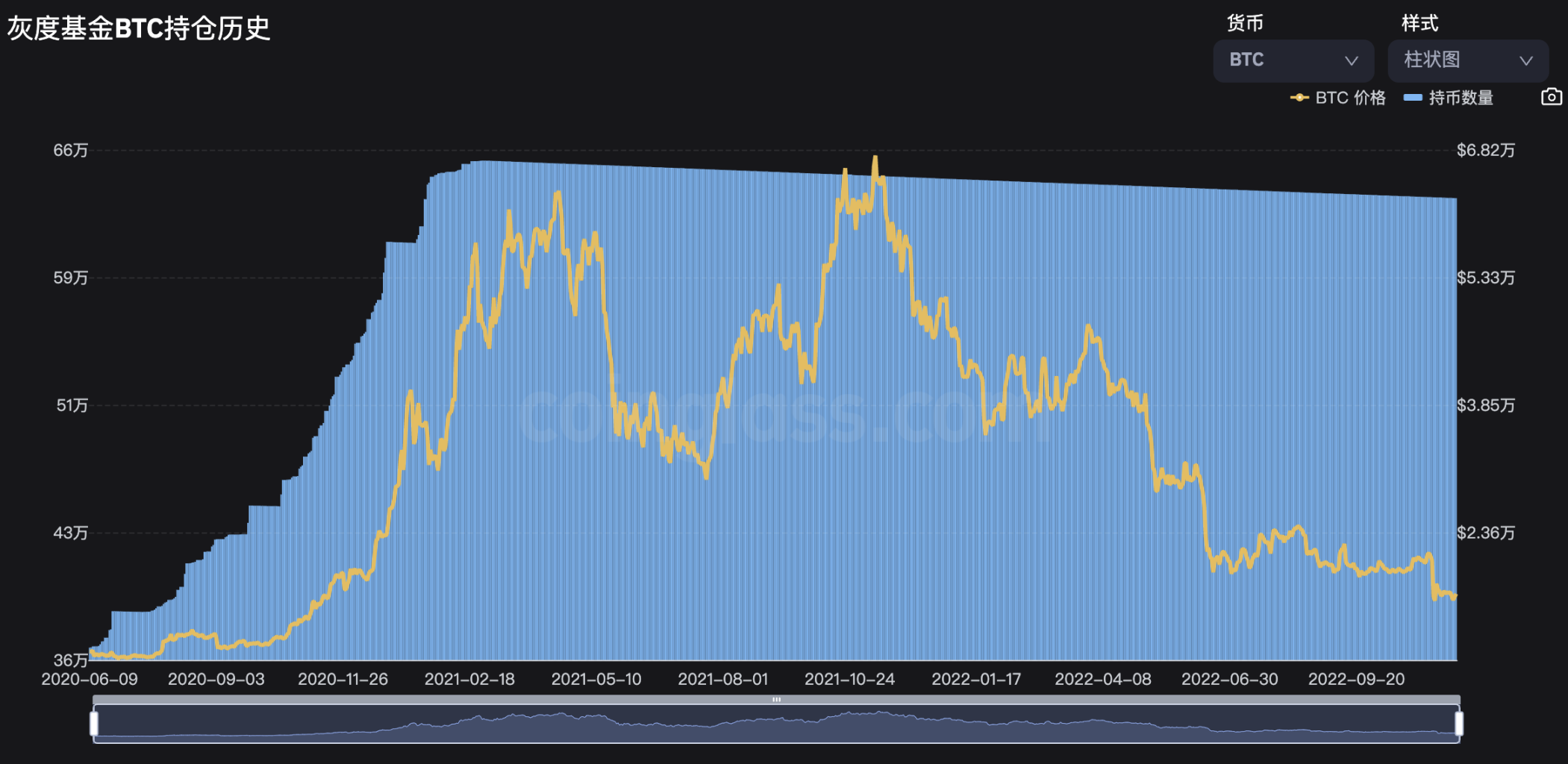

As shown in the chart below, the amount of BTC held by the Grayscale Bitcoin Trust has gradually decreased due to management fee deductions. Currently, the number of BTC held in GBTC is 633,400, valued at $10.466 billion.

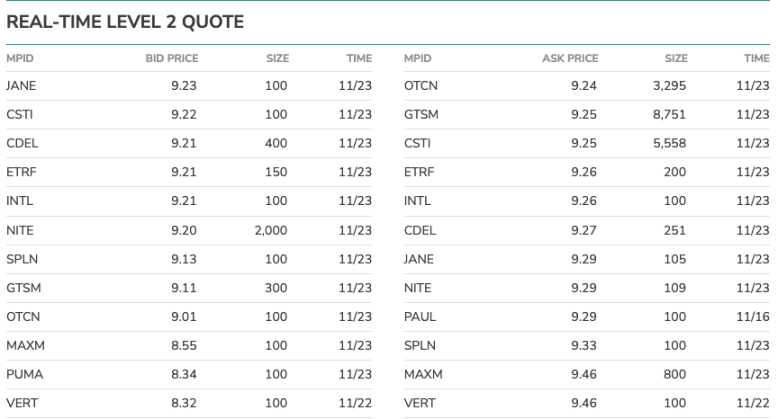

The trading volume of GBTC in the OTC Markets is also concerning. As of November 24, the average daily trading volume over the past 30 days was about 6.44 million shares, with a current price of $9.23, resulting in a daily trading amount of approximately $59.44 million. Compared to GBTC's market capitalization of about $6.39 billion, the daily turnover rate is about 0.93%.

In terms of liquidity, within a 2% price range, there are only buy orders worth about $30,000 and sell orders worth $170,000.

As one of the largest market makers, Genesis may have provided some liquidity in the trading of Grayscale products. If Genesis were to dissolve, the liquidity of GBTC could further decline.

Regarding security, even though Grayscale has refused to disclose the on-chain reserves of its trust products for safety reasons, it is highly likely that these assets are safe. Grayscale's assets are held by Coinbase Custody, an independent entity regulated by the New York Department of Financial Services (NYDFS), with the assets stored in offline cold wallets, meeting regulatory standards and ensuring the highest level of security.

Although Coinbase has not provided on-chain proof, it has issued a document co-signed by Coinbase Global's CFO Alesia Haas and Coinbase Custody's CEO Aaron Schnarch, confirming that as of September 30, 2022, the Grayscale Bitcoin Trust held 635,235 BTC, consistent with the data publicly disclosed by Grayscale.

While Grayscale is striving to obtain ETF approval, the Bitcoin ETF itself may have become a false proposition. For example, the first approved Bitcoin ETF in North America, the Purpose Bitcoin ETF, currently has a market capitalization of only $113 million, with a daily trading volume of about $300,000.

Luno: Low Exchange Trading Volume

In September 2020, DCG announced the acquisition of the crypto exchange and wallet Luno, without disclosing the purchase price. Founded in 2013, Luno had over 5 million customers in more than 40 countries and regions at the time of its acquisition by DCG.

However, as of November 24, Luno's official website shows that in the past 24 hours, the trading volume for the BTC/USDC trading pair was 2.4 BTC, the trading volume for ETH/USDC was 25 ETH, and the trading volume for ETH/BTC was 170 ETH. This trading volume is negligible compared to other exchanges.

Taking the longer-traded ETH/BTC pair as an example, the trading volume has shown a declining trend. At the beginning of 2021, the weekly trading volume for this pair was about 30,000 ETH, but now it is less than 1,000 ETH.

Blockchain Media CoinDesk: Low Ceiling

DCG acquired CoinDesk for $500,000 in 2016, and it remains one of the most influential blockchain media outlets today.

The initial risk disclosure regarding FTX/Alameda Research was triggered by an article on CoinDesk, which ultimately led to FTX's bankruptcy, implicating CoinDesk's parent company, DCG.

CoinDesk reliably generates revenue from ticket sales for its annual Consensus conference. This year's Consensus 2022 conference was held from June 9 to 12 in Austin, Texas, with tickets priced at $1,999. In DCG's portfolio, the media business serves primarily as a promotional platform, but its revenue and profitability are not high.

Bitcoin Mining Company Foundry

Foundry was established by DCG in August 2020, focusing on digital asset mining, staking financing, and consulting services.

Foundry currently encompasses multiple businesses, including: the U.S. mining machine secondary market Foundry X, Foundry U.S. mining pool, Foundry logistics, Foundry Academy, Foundry staking, equipment financing and procurement, mining consulting services, Foundry Labs supporting mining and staking, and Foundry Deploy providing mining equipment installation programs.

Foundry does not seem to be affected by the potential bankruptcy of Genesis. According to a report from The Block on November 22, Foundry is purchasing cryptocurrency mining facilities and other assets from Compute North. Compute North filed for bankruptcy last September, and Foundry CEO Mike Colyer stated that Compute North is a long-term partner of Foundry, and he is pleased to have the opportunity to build and develop the North American mining ecosystem on the foundation they established over the years.

According to PANews from North American mining practitioners, Foundry has been in a rapid market expansion phase. The initial investment in mining is high, and the payback period in a bear market is extended, so even if there are immediate profits now, they are likely not substantial.

TradeBlock

In January 2021, CoinDesk announced the acquisition of data provider TradeBlock. DCG had previously invested in TradeBlock, and the largest user of the TradeBlock XBX index is the Grayscale Bitcoin Trust.

Therefore, TradeBlock may primarily focus on maintaining data security internally.

HQ

In June 2022, DCG announced the establishment of a wealth management subsidiary, HQ Digital, to provide services such as private investment, estate planning, risk mitigation, and insurance, complementing DCG's existing Grayscale, Genesis, and CoinDesk.

The HQ website indicates that the project is still in stealth mode, with more information focused on job postings for finance, product, and investment positions.

What is the Way Forward for DCG and Grayscale?

DCG's situation does not seem optimistic. Among its seven subsidiaries, Genesis is on the brink of bankruptcy, Luno's trading volume is negligible, Foundry's mining sector is currently yielding low profits, TradeBlock provides data support, and HQ is in a recruitment phase. The potentially profitable media outlet CoinDesk has a low ceiling, and Grayscale has lost its competitive edge.

DCG is now tied to Genesis; if Genesis heads towards bankruptcy, DCG may also face bankruptcy as a result. Before that, DCG still has various possibilities, such as completing financing, raising funds by selling subsidiaries like CoinDesk, or reaching a settlement with creditors. In the worst-case scenario, Grayscale, as part of DCG, may also be forced to dissolve.

However, there is little concern about the safety of the assets in Grayscale's trust products; the likelihood of assets like BTC being misappropriated is very low. Even if DCG chooses to dissolve Grayscale to repay debts, it would require SEC approval and would not happen in the short term.

The negative premium of GBTC may serve as an indicator for observing the possibility of Grayscale's dissolution. If Grayscale is about to dissolve, informed investors will inevitably buy GBTC in the OTC market in anticipation of redemption.

Dissolving Grayscale may be the last resort; if the worst-case scenario occurs and the BTC locked in Grayscale is redeemed, the market may decline further.