The Battle for Web3 Traffic Entry: Wallets, CEX, and DApps - Who Will Win?

Thoughts on the current status and future trends of Web3 traffic entry points.

Thoughts on the current status and future trends of Web3 traffic entry points.Written by: OP Research

I. The Development History of Entry Points

The current Web3 industry is still in its early stages of development. Compared to the traditional Web2.0 industry, the acquisition of traffic is still in a relatively primitive phase, usually conducted in a rather crude manner. As the Web3 industry evolves, we categorize the methods of acquiring traffic into three major stages based on user needs.

Early Stage:

In the early stages of the crypto industry, the primary user demand was for cryptocurrency trading. Most users in the crypto industry typically accessed centralized exchanges (CEX) through web or mobile platforms to utilize various functions, such as the early Mt. Gox and Bittrex.

Therefore, during this stage, CEX became the main entry point for traffic, leading to the emergence of numerous CEX platforms, such as Binance, Huobi, OKEX, KuCoin, MEXC, and Gate. In addition to trading cryptocurrencies, since users also had needs for fiat currency deposits and withdrawals, CEX often integrated P2P deposit and withdrawal services to further control the traffic entry. However, because CEX held a significant market share, any issues with CEX could severely impact the entire market, as exemplified by the Mt. Gox incident.

Mid Stage:

As the crypto industry continued to develop, the functional demands of individual users gradually diversified, such as using blockchain wallets to store digital currencies or for transfers, on-chain interactions, etc. Particularly after the birth of Ethereum, the launch of smart contracts spurred the development of on-chain ecosystems. DApps sprang up like mushrooms, and with the popularization of basic knowledge about the crypto industry and the influx of numerous new users, the usage rate of wallets also increased, as wallets began to take on the role of entry points for various on-chain DApps.

In the subsequent development, the business scope of CEX and wallets further expanded. CEX gradually began to develop financial derivative services centered around trading, such as adding contracts and options, competing with wallets. However, due to the singularity of public chains and the lack of on-chain infrastructure, the number of chains supported by major wallets was limited, and the experience of transferring and cross-chain functionalities was not as good as that of exchanges. Especially after the emergence of TRON, its extremely low transfer fees provided a significant advantage over CEX. However, with the launch of EOS and USDT, the demand for on-chain interactions noticeably increased, further expanding the functionalities of wallets, and traffic began to shift from CEX to wallets, gradually forming the on-chain ecosystem of the crypto industry.

Present Day:

Today, user demands are even more diversified. Due to the wealth creation effect in the crypto industry, users crave more direct ways to profit, involving more complex business models. For traditional CEX, they have introduced features like IEO that have a strong wealth creation effect and are also striving to integrate various derivative services and DApps into their ecosystems, such as Binance's newly launched DeFi section and mini-program features, as well as Binance Pay. Meanwhile, CEX platforms like MEXC and Gate have chosen to list more "meme" projects to provide users with more options. Thus, CEX has become increasingly critical as an entry point for the entire Web3 ecosystem.

At the same time, wallets have begun to support multiple chains and started auditing aspects such as entry point security, incorporating features like DEX. With the further popularization of wallets and the demand for complex financial services, DeFi Summer emerged, with various DEXs, lending platforms, oracle services, and derivative trading markets springing up. The wealth creation effect from the wave of token issuance brought a large influx of new users to Web3. During this period, some outstanding leading Web3 applications began to independently use their own apps (or DApps) as their own independent traffic entry points, such as Opensea and StepN, as well as utilizing traditional Web2.0 applications as entry points to bring in traffic for Web3 applications, such as plugins for Twitter and some traffic spillover to social platforms like Telegram and Discord.

In summary, as the industry develops and traffic surges, the competition for traffic has intensified, and due to the differing demands for traffic, entry points have begun to form a diversified development model centered around exchanges and wallets, with other traffic entry points developing in parallel.

II. Current Status of Web3 Entry Points

However, according to data from NFTgo.io, on October 28, the total trading volume of NFTs on Ethereum was approximately $10.68 million, while the trading volume of Reddit Collectible Avatars was about $2.5 million. This means that Reddit NFTs accounted for roughly 25% of the entire Ethereum NFT market's trading volume. Opensea has approximately 2.3 million cumulative users, while among the 2.83 million holders of Reddit NFTs, the vast majority have registered for Reddit Vault. The number of Reddit wallet registrations is nearly on par with the number of wallets that have traded NFTs on Ethereum (approximately 3.43 million). A Web2.0 platform issuing an NFT can attract traffic comparable to the entire Web3 NFT industry, and in a short time, the user base surpasses that of Opensea, the largest NFT market in Web3. This indicates that despite many revolutionary innovations in Web3, there is still significant room for further development.

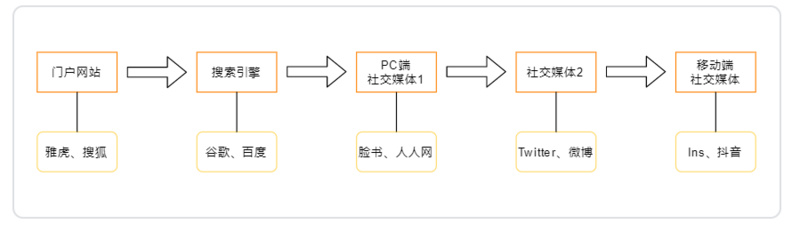

When we review the changes in Web2.0 entry points, we find that the development sequence is: portal websites - search engines - PC social platforms - mobile social platforms. From a curated collection of comprehensive information to a self-curated collection of information, then to users' own information output, and finally to fragmented views of information output by users. This bears some similarity to the current Web3, which has evolved from initially investing in BTC-based POW public chains, to a surge in investment targets during the ICO era, to the screening of tokens through IEOs and IDOs, and finally to users spontaneously or based on DAO organizations conducting research and analysis of quality projects and making recommendations. Information is transitioning from centralized, passive, and complex to decentralized, proactive, and simplified.

Based on this phenomenon, we reflect on the current status, distribution, and future development of Web3 entry points. Since there is currently no unified definition of Web3, this article defines Web3 as: a collection of decentralized applications running on blockchain. These applications (DApps) allow anyone to participate without sacrificing personal data. Therefore, when we talk about Web3 entry points, we do not limit it to "Crypto," but encompass all objects that can drive traffic, such as traditional Web2.0 platforms, centralized exchanges, and Web2.0 games.

We will categorize Web3 entry points based on different user behaviors, briefly describe their characteristics, and compare the main entry points within the same category. Finally, we will provide our views on the future development of various Web3 entry points based on their characteristics and comparative results.

III. Comparison of Web3 Entry Points

Before categorizing Web3 entry points, we need to determine the purpose of users entering Web3, or what Web3 can bring to users:

Changing the logic of existing applications: copyright confirmation, privacy ownership, asset ownership, behavioral incentives

Cryptocurrency investment

NFT investment

Based on the aforementioned functions of Web3, we have outlined the process of users entering Web3. Based on this process, we define two major categories of Web3 entry points:

Account Systems (Deposit and Withdrawal and Fund Management): Centralized exchanges, independent deposit and withdrawal projects, deposit and withdrawal aggregators, cryptocurrency ATMs, cryptocurrency debit cards, and over-the-counter (OTC) trading; EOA, CA, and MPC wallets, account abstraction (AA).

Web3 DApps (Tools, Social, and Entertainment): DEX, NFT Marketplace, copyright trading markets, domain names, DeSoc, GameFi, X to Earn.

Account Systems

1. Fund Management

Fund management involves the storage, sending, and receiving of crypto assets. Apart from the early exchanges, wallets are the primary entry point for users in the crypto industry, carrying user identity, assets, and even reputation. Security is the top priority for wallets, followed by convenience. The core of a wallet is essentially a public-private key manager, with its private keys generated based on asymmetric encryption and other technologies, granting users absolute control over their wallets, addresses (public keys), and assets. Therefore, how to manage private keys is a key technological aspect of different wallet products. Beyond that, how to expand functionalities based on wallets is another battleground for different wallet products.

Currently, the main types of wallets are divided into custodial wallets and non-custodial wallets, simply put, whether you control your wallet through private keys. The main custodial wallets today are exchange accounts, where exchanges take care of the assets in your wallet. Non-custodial wallets are more diverse, including hardware wallets, address wallets (EOA), and smart contract wallets (CA). EOA wallets are further divided into plugin wallets and mobile wallets based on usage. Additionally, EOA wallets have another extension called multi-party computation wallets (MPC). There is also a new wallet concept, account abstraction (AA), which upgrades EOA wallets to have smart contract functionalities.

Custodial Wallets

"Owning the private key means owning the wallet" sounds very secure, but in reality, the importance of private keys/mnemonic phrases has made their storage a barrier for users to use wallets. The user experience of most existing wallets falls far short of Web2.0 standards. This is why CEX has become the first choice for most users entering Web3, as CEX allows users to only remember their login passwords. However, the drawbacks are evident; once an exchange crashes, goes bankrupt, or is hacked, the assets on the CEX may also disappear. The Mt. Gox incident is a prime example, where in 2014, it claimed to have suspended user withdrawals due to hackers stealing 850,000 bitcoins, and subsequently declared bankruptcy. Moreover, since all funds within a CEX are controlled by the CEX, they can manipulate numbers to call funds (e.g., the notorious data dumping) or even directly misappropriate custodial funds for profit.

However, these drawbacks do not deter users from continuing to use CEX, as the credibility of the exchanges, combined with their ease of use, and the fact that most users only require secondary market trading, means that exchanges still hold the majority of traffic in the entire Web3 space. In December 2021, the number of users in the crypto industry reached 295 million, with the largest exchange, Binance, having 120 million users, while the largest DEX, Uniswap, only had about 3.9 million users. This illustrates the significant advantage of CEX as an entry point for Web3. In other words, most users choose to sacrifice security for convenience.

Non-Custodial Wallets

In contrast to CEX, most wallets sacrifice convenience for security, resulting in a high barrier for users to enter Web3. Specifically, hardware wallets are the most secure because assets can only be accessed if both the hardware wallet and the password are available; however, this also makes them more complex. Users need to spend a considerable amount of money to purchase a hardware wallet and must carry it with them every time they use it. If the hardware wallet is lost, the funds inside are also lost.

EOA wallets are relatively secure and convenient. They can be used via web plugins or mobile software, allowing users easier access, but users still need to remember and securely store their private keys. EOA wallets provide another type of private key—mnemonic phrases (12 English words derived from the private key). If the private key/mnemonic phrase is lost, the wallet becomes insecure, so while it is secure, it also carries risks. According to CertiK, losses due to private key leaks have amounted to at least $274 million from 2022 to date, including significant losses from industry professionals like Wintermute.

Although new technologies have emerged, such as MPC wallets developed from EOA wallets and more extensible CA wallets to achieve so-called keyless or low-barrier wallets, EOA wallets remain the mainstream. Among them, Metamask (the little fox) leads the way, boasting over 80 million users in December 2021, with monthly active users exceeding 30 million in March 2022. Although this pales in comparison to Binance, Metamask's position among software wallets is already unshakeable.

MPC wallets distribute parts of the private key among multiple parties rather than the entire key. This is similar to multi-signature wallets, where all parties must sign to initiate a transaction. MPC wallets decentralize the private key in an off-chain manner, enhancing the security of wallet accounts. Additionally, MPC wallets can refresh key fragments: replacing existing key fragments with new ones to solve the problem of lost keys. Users only need to match corresponding email or biometric verification information to recover their wallet assets. This latest solution undoubtedly increases user convenience compared to the cumbersome security operations of traditional wallets, lowering the entry barrier to Web3.

The emergence of account abstraction (AA) could potentially change the current wallet landscape. Account abstraction combines EOA and smart contracts, upgrading EOA wallets to smart contract wallets (CA) without altering the underlying ETH architecture, significantly lowering the entry barrier for EOA while providing infinite extensibility, achieving most functionalities of current Web2.0 accounts. For example, paying gas fees on behalf of users, keyless access, and social recovery of accounts. Specifically, smart contract wallets mean that the wallets themselves can be programmable, customizable, and even modular, giving smart contract wallets endless possibilities. With smart contracts, wallets can customize different security thresholds for transfers of varying amounts, and establish permission levels for operations on different DApps, among other scenarios achievable through smart contracts, making them more user-friendly. Current examples of smart contract wallets include Argent (social recovery), Gnosis Safe (multi-signature), and A3S (wallet transferability).

2. Deposit and Withdrawal

Key factors for deposit and withdrawal projects include: identity verification, fiat to cryptocurrency deposits, and cryptocurrency to fiat withdrawals.

Typically, users trading over a few hundred dollars monthly need to undergo KYC. KYC requires identification documents (ID card, passport, or driver's license), proof of residence, and facial recognition. Most compliant exchanges require users to complete KYC to deposit and withdraw, but not all exchanges have this requirement. Independent deposit and withdrawal projects, deposit and withdrawal aggregators, and cryptocurrency ATMs tend to be more decentralized and free. However, centralized exchanges and large OTC platforms tend to support a wider variety of fiat currencies due to their greater legal and technical resources.

In terms of payment and receipt methods for deposits and withdrawals, they are limited to wire transfers, ACH transfers, debit/credit cards, and third-party payments (like Google or Apple). However, some exchanges, such as FTX, support internal cryptocurrency exchanges for fiat and transfer them to receiving accounts via wire transfer. This greatly facilitates users while avoiding the possibility of receiving dirty money on OTC or decentralized platforms.

However, there are frictions in the process of exchanging fiat and cryptocurrency, such as exchange rate fees, distributor markups, and blockchain network fees. Generally, the fewer the layers of distributors, the smaller the friction. Therefore, in terms of friction loss, CEX = OTC < independent projects < aggregators.

Centralized exchanges are the most commonly used platforms for fiat deposits and withdrawals, generally holding remittance licenses in most countries worldwide, supporting the most fiat and cryptocurrency types, and offering the lowest rates. However, CEX can also provide cryptocurrency payment services to realize another form of withdrawal, such as Binance's Binance Pay, which can be used for booking hotels, purchasing gift cards, etc. Since CEX already has a large number of secondary trading users, converting them into deposit and withdrawal customers is relatively easy.

Independent deposit and withdrawal projects (like Moonpay, Transak, Wyre) operate like small exchanges but mostly only provide fiat deposit and withdrawal services. Their interfaces are simple and user-friendly, resulting in low learning costs for users, but these projects often have distributor markups.

Deposit and withdrawal aggregators (like TransitSwap, KyberSwap, and MetaMask's fiat deposit service) aggregate various independent deposit and withdrawal projects and CEX to achieve optimal exchange rates while charging commissions. However, the key is that they can introduce features like DEX, liquidity staking, and NFT markets, providing one-stop deposit and withdrawal and Swap/Staking services.

OTC is most commonly conducted in a P2P model, where buyers and sellers directly engage in fiat deposit and withdrawal transactions. Some platforms (like Binance P2P) must rely on third parties to eliminate trust costs when facilitating transactions between buyers and sellers, charging very low fees. However, P2P means that payment methods can be relatively diverse; theoretically, as long as both parties agree, transactions can be conducted through any method. However, the risks are evident, such as potentially being passively involved in money laundering, leading to frozen accounts or even being forced to return withdrawn funds.

Web3 DApps

1. Tools

Tool applications are likely the most promising entry point for Web3 traffic among the three categories. Tool applications not only improve upon Web2.0 but also introduce cross-era innovations. Applications like DeBox (social payment platform), Monaco (instant social media), and Skiff (collaborative work platform) essentially build on Web2.0 applications by adding token economies and achieving privacy, transparency, and trustlessness through blockchain, thus earning the title of "Web3xx"—Web3 WeChat, Web3 Weibo, Web3 Google Docs. In other words, they do not provide users with a compelling reason to abandon Web2.0 entirely for Web3 but instead incentivize users to use them temporarily through tokens. Therefore, we will focus on discussing DEX, NFTs, and copyright trading platforms as entry points for Web3.

DEX

DEX DApps play a crucial role in users entering Web3. Previously, users needed to go to CEX to convert between different assets because the on-chain order book exchanges lacked the depth of CEX. With the emergence of AMM DEX, the role of market makers was eliminated, significantly enhancing on-chain trading depth, and the advent of liquidity mining further optimized the trading experience on AMM DEX. The existence of DEX allows users brought in by other DApps to directly convert earned tokens into stablecoins like USDT or USDC on-chain to lock in profits.

However, the problem with AMM DEX is the absence of market makers; when the depth of an LP pool is insufficient or when users conduct large transactions, it can result in significant slippage. For example, in the cUSDC incident on September 28, a user sold cUSDC worth $1.5 million on UniswapV2, but due to the lack of liquidity for cUSDC, they only managed to sell for about $520.

NFT Marketplace

NFTs (Non-fungible Tokens), as a new form of asset born from blockchain, serve as an excellent entry point for Web3 traffic. The record-breaking sale of Beeple's "Everydays: The First 5000 Days" for $69 million made people aware of the value of digital assets and spurred the birth of numerous NFT-related projects, such as the metaverse segments represented by Sandbox and Decentraland, the PFP segments represented by BAYC and CryptoPunks, and NBA Top Shot. Subsequently, various copyright-related NFTs emerged, including IP copyrights, patent copyrights, and music copyrights, helping creators confirm their rights.

NFTs are one of the easiest forms of crypto assets for the public to understand. The value of a painting lies not only on the canvas but in the art itself, so digital artworks also hold value. Compared to traditional artworks, NFTs are more shareable and satisfy users' desire for showcasing. Thus, PFP NFTs emerged, with CryptoPunks representing Crypto OGs, granting ownership of them the title of Crypto Native. BAYC aims to create a club that bridges the gap between mainstream culture and Web3, and it has become a symbol of reputation and identity due to the involvement of celebrities like Stephen Curry, Jay Chou, Lin Junjie, and even Chinese Li Ning. In contrast to PFPs, Sandbox and Decentraland have gained recognition as major international companies purchase land to enter the metaverse, using their land as a platform for brand display to attract customers, while their existing customers learn about Web3 and the metaverse.

Similarly, NBA Top Shot has introduced existing NBA audiences to Web3 through NFTs, leveraging the wealth creation effect to attract more people, further enhancing its price and fame. Likewise, copyright NFTs bring audiences from the creator's domain into Web3, providing creators with more income sources while facilitating investors or fans in investing in or collecting works' copyrights.

As the core venue for NFT appreciation, NFT marketplaces like Opensea, Rarible, and SuperRare, much like DEX for most DApps, provide users with the potential to profit from NFTs and guide users to engage in more interactions within Web3. Based on this, derivative platforms for NFT lending, NFT fragmentation, and NFT trading aggregators serve as tools to assist users in entering Web3.

2. Social

The domain names and DeSoc under the DID concept are typical entry points in Web3 applications. Similar to traditional DNS domain names and social media, they can directly carry user traffic and convert it, using "vanity numbers" and "information" as tools to acquire users. In 2020, the global domain registration market reached 374 million, and according to Messari's research report, the registration volume of ENS (Ethereum Name Service) reached a historical high of 1.12 million in the third quarter. When comparing the user numbers of Medium and Mirror, we find that Medium has a monthly visit count of 25 million, while Mirror only has 2.1 million. This indicates that as a Web3 entry point, domain names and DeSoc have over ten times the potential.

Domain Names

Web3 domain names convert complex addresses (like Vitalik Buterin's address: 0xAb5801a7D398351b8bE11C439e05C5B3259aeC9B) into readable characters (Vitalik.eth), significantly lowering the operational threshold for addresses as interaction objects during identification and input, while readable characters can endow addresses with additional value (such as birth years, names, brand names, etc.). Current domain names are still in the early stages of their ecosystem, merely replacing addresses with short characters, but we can still see that when users change their Twitter names to xx.eth, they break the identity barrier between Web2.0 and Web3. "xx.eth" signifies all on-chain data associated with that address within the ETH ecosystem, in other words, it records the "life" of that address, and when applied to the Web2.0 world, it brings all its interactions in Web3 along, allowing Web2.0 users to locate the same "person" based on this name.

As domain names develop, in addition to .eth, we have seen .ether and domain names based on other public chains, such as BSC's .bnb, Aptos's .apt, Evmos's .evmos, and domain names issued by companies focusing on multi-chain domains, such as DAS's .bit, Unstoppable Domains' .nft, .crypto, .dao, etc. TwitterScan is also expanding the correlation between domain names and Twitter. However, in terms of practicality and recognition, .eth remains unmatched, as ETH's user base and capital still dominate. Other domain names often attract users temporarily through airdrop expectations but fail to retain them long-term.

DeSoc

In May 2022, Ethereum founder Vitalik Buterin, economist Glen Weyl, and Flashbots researcher Puja Ohlhaver jointly published an article titled "Decentralized Society: Finding the Soul of Web3." This led to the term DeSoc gaining immense popularity. The DeSoc mentioned in the article is built on Soulbound Tokens (SBT), aiming to construct a credible decentralized society through the non-tradability of SBT and DID. Currently, mainstream applications in Web3 are still concentrated in the financial sector, such as increasing capital utilization, faster and safer transactions, and more complex derivatives. DeSoc could change the current overly financialized state of Web3, leading us toward a "more transformative, diverse, socially bridging, and income-increasing future."

Taking current popular DApps as an example, task platform applications like Galxe and Quest3 convert project demands into a series of tasks and distribute corresponding SBTs as proof, allowing users to earn SBTs by completing tasks and await airdrops from project parties. These tasks often require users to interact on Web2.0 platforms like Twitter, Discord, and Telegram, which can attract a large number of Web2.0 users into Web3 through the profit incentive.

Another intuitive case is Binance's SBT—BAB, which uses BAB to channel KYC-compliant user traffic into BSC, retaining users through targeted airdrops for BAB while developing projects based on BAB, such as Lifeform.cc, which requires users to hold BAB to claim its game character token LBT.

3. Entertainment

Entertainment-related Web3 applications are an important part of the industry, with GameFi being the most significant category. GameFi has a natural advantage over other Web3 entry points, as it possesses a massive appeal to a large number of users, including many traditional Web2.0 users. In today's mainstream GameFi games, many have undergone Web3 adaptations of classic games from the Web2.0 era, meaning GameFi inherently possesses excellent cross-over capabilities.

Last year's attention on Axie Infinity made GameFi one of the most important tracks in the Web3 space, with the number of active players on-chain consistently around one million, primarily concentrated on the BSC, ETH, and POLYGON public chains. The "X to earn" concept, exemplified by this year's popular Binance-invested creative outdoor Web3 game StepN, represents the latest entertainment trend in the Web3 field. Additionally, entertainment apps or DApps still exist in various forms, such as imitation short video apps and social networking software. All these emerging Web3 applications are primarily user profit-oriented, enhanced by gamification, possessing strong cross-over capabilities. This type of application indicates that GameFi in the Web3 era has more mature gameplay and traffic attraction compared to other entry points.

Although entertainment applications currently face a series of issues, such as high performance requirements for public chains due to excessive on-chain interactions, the overall merits outweigh the flaws, with phenomenal entertainment applications emerging, such as Axie Infinity, RACA, and StepN. They utilize traditional EOA wallets for some external traffic, while others, like StepN, adopt a centralized app approach to guide users to register wallets with built-in entry points, significantly aiding these GameFi projects in attracting and converting traffic into new comprehensive Web3 users.

Thoughts on Web3 Applications:

As mentioned at the beginning of this article, we currently categorize Web3 application entry points into two major categories: account systems and DApps. Each of these entry types has its own advantages and disadvantages: for account systems, this entry method resembles a process from broad to specific, where users first enter funds through centralized account systems, creating their own account systems, and then radiate from that account system (such as exchanges, wallets, etc.) to specific points (DApps and other Web3 applications). This is a relatively traditional method of traffic entry.

Due to the maturity of this type of entry, the deposit system is relatively complete and convenient, and users have ample choice and freedom. The downside is that it is somewhat singular and one-dimensional in attracting traffic, lacking targeted strategies for different demographics. In contrast, Web3 DApp entry points resemble a radiation process from specific points to broader areas, where traffic often enters through specific DApps and then expands into the larger Web3 ecosystem. This method can fully leverage the subjective advantages of different types of DApps to attract their target traffic, such as specific NFT marketplaces and the once-popular Axie Infinity, both of which attracted a large amount of external traffic through the influence of the DApps themselves.

Currently, account system entry points have a long history and are more mature, with exchange users still dominating the overall Web3 user base, while wallets are essential for entering Web3. However, an increasing number of situations indicate that leading DApps or Web3 applications with independent large traffic advantages have already gained the ability and foundation to bypass exchanges and wallet entry points, starting to establish independent apps or application endpoints as entry points. This type of Web3 DApp represents a more emerging trend that deserves our attention.

Nonetheless, both types still face some similar challenges, such as the entry barrier to the Web3 world being significantly higher than that of the Web2.0 world. They are constantly striving to eliminate such obstacles while leveraging their advantages.

IV. Outlook on Future Web3 Entry Points

Although StepN, as a representative project of this year's traffic explosion, has temporarily shelved a series of plans due to operational and environmental factors, the current stage of development in the Web3 industry, given the eye-catching ability and traffic aggregation capacity of explosive applications born from the industry, has already created conditions for them to establish their own massive independent traffic entry points in a short time. After achieving phased success, they are not satisfied with merely opening up the gaming market but aim to leverage their traffic entry to develop a series of projects around the StepN ecosystem, including Launchpad, DEX, and even more DApps. This is undoubtedly a highly imaginative initiative, and I believe it is also the path for many entrepreneurs dissatisfied with Web3 apps or DApps to rise.

StepN's imitation of the wallet development path at least opens up a line of thought, hoping to utilize its peak traffic to develop its ecosystem and retain traffic. Such initiatives have made Web3 entrepreneurs realize that this path is not exclusive to wallets; APPs, DApps, and even various developers capturing traffic in the future can attempt this as well.

Recently, the new NFT trading platform MOOAR, under StepN's parent company Find Satoshi Lab, is also set to launch. Although the project has not fully realized its initial vision, StepN has at least set an example.

We believe that the emergence of such short-term explosive applications capable of escaping the gravitational pull of exchanges and wallets to independently capture traffic is merely a phase. In other words, the industry's dividend period is limited, both for users and entrepreneurs. We think this is due to the current immaturity or imbalance in the development of the Web3 ecosystem. As the industry matures, this phenomenon will gradually disappear, and precious traffic resources will concentrate on a few leading applications.

This is akin to the rapid development of the internet, where both application endpoints and traffic entry points could flourish, but now, in the mature phase of the industry, most services and even functionalities have converged into a few leading apps, with small to medium-sized applications either dying or being integrated. This is not merely a result of capital operations; we believe the fundamental reason lies in the nature of human behavior. As users, we cannot long endure entering through complex and cumbersome entry points; traffic will always tend toward convenience and one-stop integration. This may be an inevitable result of product demand; while applications in the Web3 era may decentralize the backend, the frontend still struggles against the gravitational pull of user habits, which are inherently difficult to decentralize.

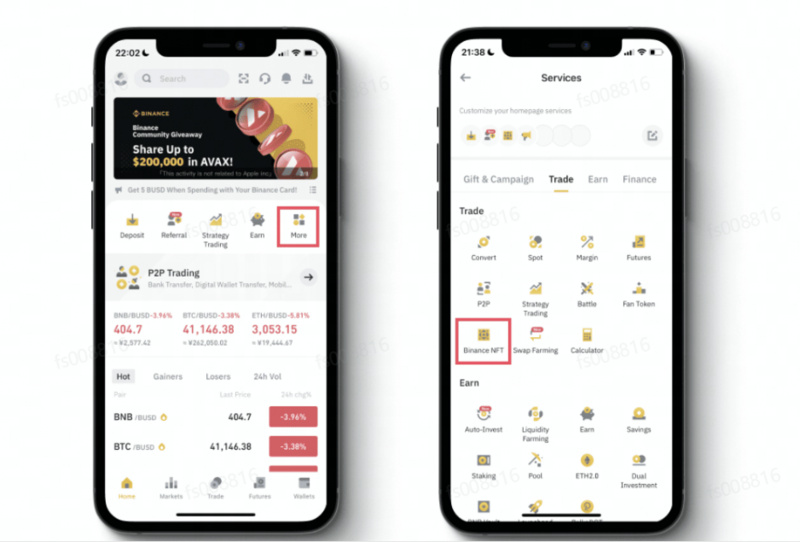

Thus, we believe that in this scenario, future Web3 traffic entry points, whether choosing account systems or Web3 DApp methods, will likely concentrate on a few, and should conform to a model radiating from broad to specific. Specifically, given the current situation, exchanges and wallets are the most powerful and likely candidates to achieve this outcome. If CEX and wallets can seize the current golden period of traffic and develop entry points that align with user habits and usage environments, they should significantly enhance their dominance in traffic. For instance, the dropdown mini-program interface in the main interface of the Binance exchange, which integrates various APP and DApp entry points, is a very commendable attempt in my view.

We believe that the concentration of traffic entry points in a few leading applications is the most likely industry model in the future maturity phase (currently, the entry points of exchanges and wallets are closest to this). Moreover, this method of traffic capture does not violate the spirit of decentralization and respect for individual users in Web3, as their backends are still built on a decentralized basis. Based on the spirit of decentralization, it is worth contemplating whether there will be better solutions for traffic entry in the future that can further optimize this centralized traffic entry method.

Additionally, Elon Musk has recently completed his acquisition of Twitter, the largest social network in Web2.0 and a massive entry point for internet traffic. Reforming Twitter in a Web3 manner is highly anticipated. Musk may implement significant changes to Twitter, and whether such a colossal Web2.0 and traditional internet giant will undergo Web3 reforms, what specific methods will be used, and to what extent these reforms will take place, all of these will have profound implications for traffic entry distribution. If Twitter can implement decentralized reforms or accommodate a large number of Web3 applications, it may disrupt the current distribution pattern of Web3 traffic. We believe this would be a groundbreaking event, and we look forward to seeing how it unfolds.

Reference:

Reddit NFT: Analyzing the Curve of Public Adoption from Web2 to Web3

Total OpenSea traders over time (Ethereum)

The First Stop for Web3: A Review of the Cryptocurrency Fiat Deposit and Withdrawal Business Model

Keyless Wallets Based on MPC: The "Breakthrough" of Web3 Entry Points

Low-Barrier Wallets: A Necessary Tool for Mass Adoption of Web3 Applications

Overview of Ethereum Blockchain Account Abstraction and Its Potential Use Cases

From DNS to ENS: The Era of Domain Names in Web3

Understanding Decentralized Society (DeSoc)

A Brief History of NFTs: A Shining Moment Across Sixty Years