The key to DeFi's mainstream adoption: Tokenization of physical assets

DeFi needs to make progress in areas such as asset custody, liquidity, and credit protocols to cross the moat of TradFi.

DeFi needs to make progress in areas such as asset custody, liquidity, and credit protocols to cross the moat of TradFi.Written by: Vaish Puri

Compiled by: aididiaojp.eth, Foresight News

The influence of DeFi is slowly penetrating into real-world assets, and the financial industry is on the brink of transformation. As more and more assets are tokenized, traditional capital markets are also merging into the crypto world.

Due to rising dollar interest rates, declining DeFi demand, and an unfavorable global macroeconomic environment, the opportunity cost of transferring funds on-chain is at its highest level in the history of cryptocurrencies. Real-world assets (RWA) provide a unique opportunity for yield-seeking DeFi investors to access off-chain debt markets while allowing TradFi institutions to tokenize assets and issue debt without geographical constraints.

What are RWAs?

RWAs are tokens representing physical assets (either fungible or non-fungible) that can be traded on-chain. The physical assets that RWAs can represent include real estate (homes and rentals), loans, contracts, and guarantees, as well as any high-value items used in transactions.

RWAs free themselves from many of the constraints of traditional finance. Imagine a medium-sized fintech company in Indonesia called Bali wanting to raise funds to drive their business growth and marketing efforts. By issuing tokenized bonds, the company can raise over $100,000 in just a few hours, rather than going through traditional banks and VC channels. These tokenized bonds can be bundled with many similar Indonesian fintech bonds and sold at different prices and interest rates.

Since everyone can view on-chain assets, Bali's financial status is transparent. As Bali's revenue and costs change, the token price will also fluctuate, and changes in credit risk will be automatically reflected in the loans.

Thanks to RWAs, Bali can borrow at a rate of 7%, while the typical borrowing rate for Indonesian fintech companies is above 14%. When DeFi yields are low, investors can obtain attractive real-world loan rates. Regardless of geographical location, RWAs can drive economic growth.

The Necessity of RWA Development

Using the success of securitization in the 1990s as an example, we can understand how improved system standards can change capital formation. Securitization is merely a system for creating, collecting, storing, and diversifying risk, significantly increasing liquidity and funding sources by proposing benchmarks that assets must meet (in terms of length, risk, etc.). Mortgages, corporate loans, and consumer loans have been institutionalized through securitization, providing consumers, companies, and homebuyers with lower-cost financing.

After nearly 30 years of development, the standards for securitization have changed little, and financial markets have not effectively adapted to the rise of the internet. This is because intermediaries, including investment banks, trustees, and rating services, have kept borrowing costs higher than they should be. Most assets cannot be securitized because they cannot be issued under the same rules during the initiation process. Most businesses still cannot access international financing markets, and basic resources like insurance remain difficult to obtain in Africa and Asia. This raises the question: what needs to be done for digital capital markets to cross the moat of TradFi?

Establishing a connection between cryptocurrencies and the real world is a primary goal of DeFi. Although the digital asset market is still small (around $1 trillion), the physical asset market is enormous (over $600 trillion). If DeFi is to integrate into the mainstream, cryptocurrencies must enter the physical asset market.

Asset Custody

Given the surge in digital assets and the influx of new institutions, the importance of a reliable digital asset custodian is self-evident. In recent years, licensed DeFi custody services (such as Anchorage Digital and Copper) have surged. Some credit protocols secure their assets by hosting tokenized assets on these licensed platforms.

Currently, the custody process is largely governed by the legal structures deployed in contracts and standard KYC/AML procedures. Taking Centrifuge as an example, when interacting with liquidity pools, investors sign agreements with liquidity pool issuers, setting the liquidity pool as a special purpose vehicle. The agreement requires the issuer to be responsible for any future repayments.

All financing transactions and payments are completed directly between the borrower, SPV, and investors, and are conducted on-chain. Future credit protocols hope to combine more with DIDs like Kilt to enable the verification of assets, and then establish on-chain underwriters to act as third-party risk assessors.

Liquidity

Specific tokenized assets (such as real estate contracts) may be very illiquid. The liquidity of funding pools depends on the asset's duration and the inflow and outflow of investors. Income-based incentive models are another profitable source of liquidity.

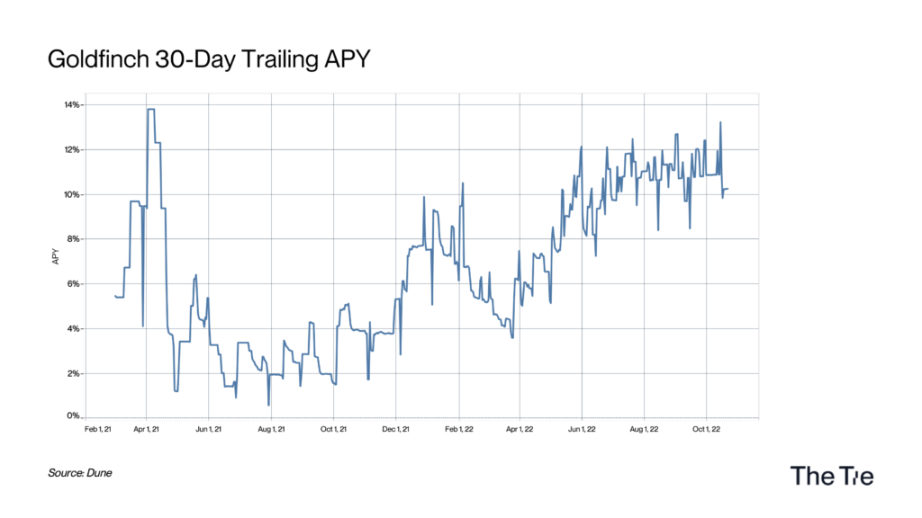

To create liquidity, protocols can collaborate with DEXs, AMMs, and other DeFi applications (such as Balancer and Curve). A typical example is Goldfinch. Goldfinch members created a liquidity pool on Curve using FIDU, a token representing deposits from liquidity providers to senior pools, allowing FIDU-USDC curve LP positions to be staked for GFI liquidity mining rewards.

Credit Protocols

One of the biggest reasons institutions feel uneasy about DeFi is the lack of a standardized reputation system, such as credit scoring. Because institutions cannot enforce future loan repayments in the event of default, DeFi protocols are forced to require liquid tokens as collateral. While this approach does exclude credit risk, it also limits the number of available financial products. Credit protocols are using supplementary strategies to provide reputation proof for loans. While some are striving to bring off-chain reputation into the on-chain world, a better approach is to create an on-chain reputation system.

Specific major credit protocol examples include Maple, TrueFi, Goldfinch, Centrifuge, and Clearpool, but their goals vary.

Goldfinch

Goldfinch is developing a decentralized loan underwriting protocol that allows anyone globally to issue loans on-chain as underwriters. Goldfinch uses a unique identity (UID) NFT representing KYC/KYB, with two fundamental principles:

Over the next decade, due to the overall transparency and efficiency of DeFi and the low-interest macro environment (which is currently changing), investors will need new opportunities for higher yields than traditional banks and institutions can provide.

Global economic activity will shift to an on-chain model, making every transaction transparent, thus creating a new public good. This new public good is immutable and has publicly available credit records, which can significantly reduce the transaction costs associated with banking.

Goldfinch aims to collect information generated in real life and online and use it to build user reputations that can be applied on-chain.

Like any credit institution, the system is not without risks. Goldfinch needs to prevent defaults as much as possible, or in the event of a default, to repay lenders as much as possible.

Goldfinch relies on its supporters (investors providing USDC to the borrower pool) to monitor the health of the liquidity pool and provide liquidity. Since their liquidity is the first to be lost in the event of a default, they are motivated to do this work. Similar to TrueFi, Goldfinch provides smart contract insurance through Nexus Mutual.

Centrifuge

Centrifuge is an on-chain network that provides fast, cheap funding for small businesses while also offering investors stable returns. Centrifuge connects real-world assets to DeFi to lower the capital costs for SMEs and provide DeFi investors with stable sources of returns unrelated to volatile crypto assets. Centrifuge relies on asset originators and issuers to provide reliable loans with low default rates. In the event of a default, investors in the Centrifuge junior tranche bear the first losses.

Tinlake is the first user-facing product, providing any company with a simple way to access DeFi liquidity. For investors, these assets will generate safe, consistent returns for their investments, unrelated to the volatile outcomes of the cryptocurrency market. The native Centrifuge token (CFG) uses proof of stake and sets incentives for validators. Through on-chain governance, CFG holders can actively influence the development of Centrifuge.

Tinlake's valuation method is based on a fair value discounted cash flow model, which can be summarized as follows:

Derive expected cash flows: For each outstanding financing of an asset, expected cash flows can be calculated based on expected repayment dates and amounts.

Risk-adjust expected cash flows: Adjust for credit risk based on expected losses. Expected loss = expected cash flow * PD * LGD, and subtract from expected repayment amounts to adjust for credit risk.

Discount risk-adjusted expected cash flows: Discount the risk-adjusted expected cash flows at an appropriate discount rate (depending on asset class and asset pool) to arrive at the present value of the financing.

Calculate net asset value: Sum the present values of the risk-adjusted expected cash flows of all financings in the liquidity pool to arrive at the net asset value.

TrueFi

TrueFi is a leading credit protocol that provides a wide range of applicable scenarios for both real-world and crypto-native capital markets. As of November 2022, TrueFi has issued over $1.7 billion in unsecured loans and paid over $35 million to lenders, with every dollar allocated on-chain. Through gradual decentralization, TrueFi is now owned and managed by TRU token holders, with underwriting rights held by the TrueFi DAO or independent portfolio managers.

TrueFi serves four main participants and coordinates their actions:

Lenders use TrueFi to access opportunities within a range of portfolios.

Borrowers, after review, rely on TrueFi to quickly obtain competitively priced capital without collateral, maximizing capital efficiency.

Portfolio managers use TrueFi to build on-chain portfolios, leveraging the advantages of blockchain technology for investment activities, such as 24/7 access to global lenders, higher transparency, and lower operational costs.

TRU holders effectively own and manage the TrueFi protocol, making key decisions and contributions necessary for TrueFi's development through public discussions and on-chain voting.

TrueFi's core contributor Archblock (formerly TrustToken) initially launched the TUSD stablecoin in 2018 based on real-world assets. Since early 2022, TrueFi has further delved into RWAs, allowing traditional funds to transfer their loan portfolios on-chain. Today, TrueFi has a portfolio facilitating loans to fintech companies in Latin America, emerging markets, and even crypto mortgages.

Becoming a borrower or portfolio manager on TrueFi follows a process similar to most other credit protocols: each new applicant must submit a public proposal describing their business and intended use of funds, which must be approved by the community while also meeting underwriting requirements (such as management capital, maximum leverage, and asset exposure set by the TrueFi credit committee). Successful applicants are whitelisted and can borrow from TrueFi's permissionless DAO pool or design and launch their portfolios.

TrueFi has taken a series of measures to protect lenders. In addition to managing a strict underwriting process led by the DAO credit committee and committing to regular code audits during major protocol upgrades, TrueFi also has a three-tier recourse system. Up to 10% of staked TRU will be used to cover lender losses; TrueFi's user security asset fund may draw on its reserves to cover any further losses; finally, any successful collection actions against defaulting borrowers will be appropriately compensated through the DAO. Additionally, TrueFi offers a smart contract assurance program that can be purchased through Nexus Mutual, providing insurance in the event of exploitation of the smart contract.

After gradual decentralization, TrueFi is now owned and managed by TRU token holders. The TrueFi DAO now owns and manages TrueFi's permissionless pool, treasury, and roadmap. The DAO is looking towards deeper institutional adoption and DeFi integration, launching features such as tiered levels and improved portfolio composability.

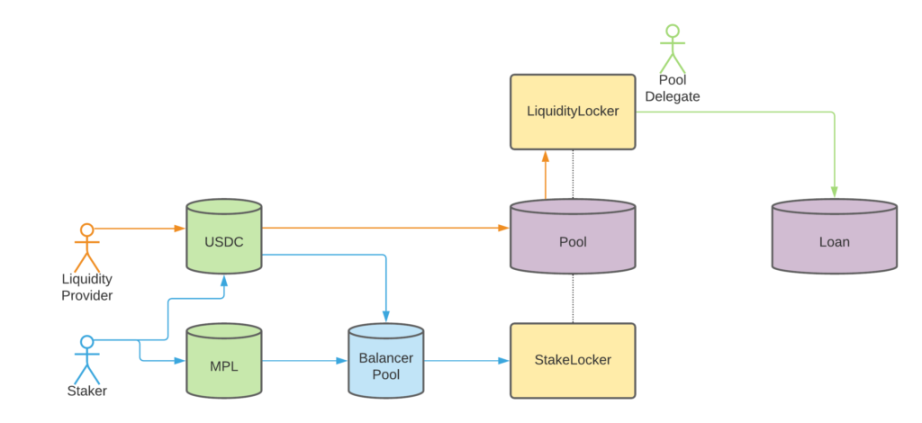

Maple

In 2021, Maple launched a non-collateralized loan program for licensed KYC loans.

Maple does not use the standard DeFi model that relies on collateral that can be reduced in the event of insufficient payment; instead, it enables users to provide under-collateralized loans to well-known companies based on reputation. Alameda Research, Framework Labs, and Wintermute Trading are some current borrowers from other funding pools.

The protocol is governed by two tokens (MPL and xMPL), allowing token holders to participate in governance, share fee revenue, and provide liquidity to lending pools.

Maple Token (MPL) holders participate in the following ways:

Passive MPL holders earn incentive fees.

Savvy MPL holders can earn additional returns by selecting liquidity pools.

Staking MPL-USDC 50-50 BPT provides a reserve to cover loan defaults in exchange for a portion of ongoing fees.

As Maple moves towards full decentralization, MPL holders will be able to submit proposals and vote on changes, such as adding mining pool representatives, adjusting fees, and staking parameters. For Pool Delegates, Maple is a tool for attracting funds and earning performance.

In Maple, mining pool representatives are crucial. Because they are responsible for maintaining the stability of Maple's lending pools, they undergo a rigorous approval process. The approval process involves authorizing loan requests, screening borrowers, and initially establishing loan pools. Finally, Maple requires each mining pool representative to hold tokens and submit MPL tokens as initial loss capital. If a borrower defaults, the mining pool representative will also be affected. However, in the event of a default, Maple can use Pool Cover funded by Pool Delegates and MPL holders for priority compensation.

Conclusion

As the industry evolves, the efficiency of capital flows will increase by an order of magnitude. In a fully efficient market, a pre-approved borrower could obtain a $5 million loan and repay it within 30 minutes, then watch another borrower quickly take out the same amount. This liquidity will be driven by a credit model that continuously assesses each borrower's default risk and prices any new available information. In this future, every dollar of capital will be immediately allocated to where it provides the highest risk-adjusted return. Credit protocols like TrueFi, Centrifuge, and Goldfinch will play a significant role in guiding finance in this direction.