Messari: The Development History and Common Dilemmas of Social Tokens

Social tokens need to improve their shortcomings in discoverability, user experience, and overall utility to lead the next bull market and achieve success.

Social tokens need to improve their shortcomings in discoverability, user experience, and overall utility to lead the next bull market and achieve success.Written by: Kel Eleje,《The Social Token Thesis》

Compiled by: Babywhale, Foresight News

Key Points:

A new type of token distribution mechanism that attracts retail investors can catalyze a bull market, and social tokens are such a distribution mechanism.

Due to issues of discoverability, user experience, and application layers, social tokens like WHALE, ALEX, and FWB have failed to catalyze a sustained bull market in the past.

New platforms like Purple Trader and upcoming events like the World Cup may trigger a revival in demand for social tokens.

If social tokens make significant improvements to their utility, their ultimate state may resemble the "network state" described by Balaji Srinivasan. The TAM for such an outcome is substantial.

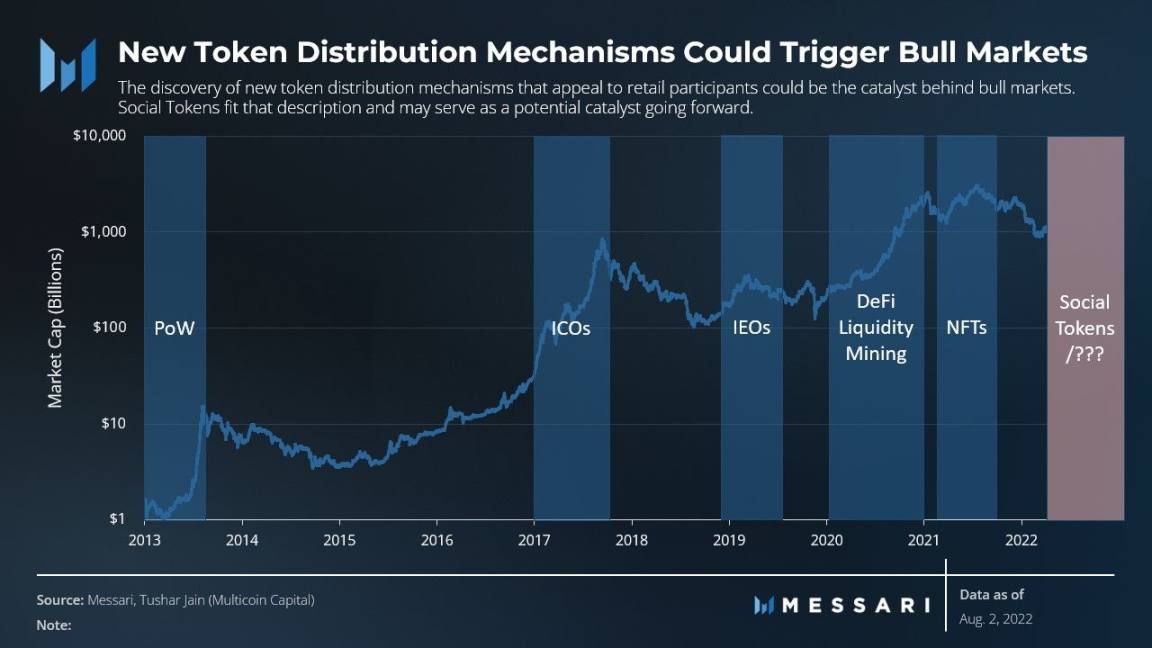

Currently, a question that often arises in the minds of cryptocurrency investors is: When will the next bull market arrive?

The collective consciousness known as the "market" has spawned countless papers on what will be the next catalyst for a bull market. A prominent argument is that novel token distribution mechanisms—such as ICOs, DeFi mining, and NFT minting—are catalysts for bull markets.

The focus of this theory is that new distribution mechanisms must be able to attract retail investors. The attraction to retail investors and the novelty of the distribution mechanism are precisely embodied in social tokens.

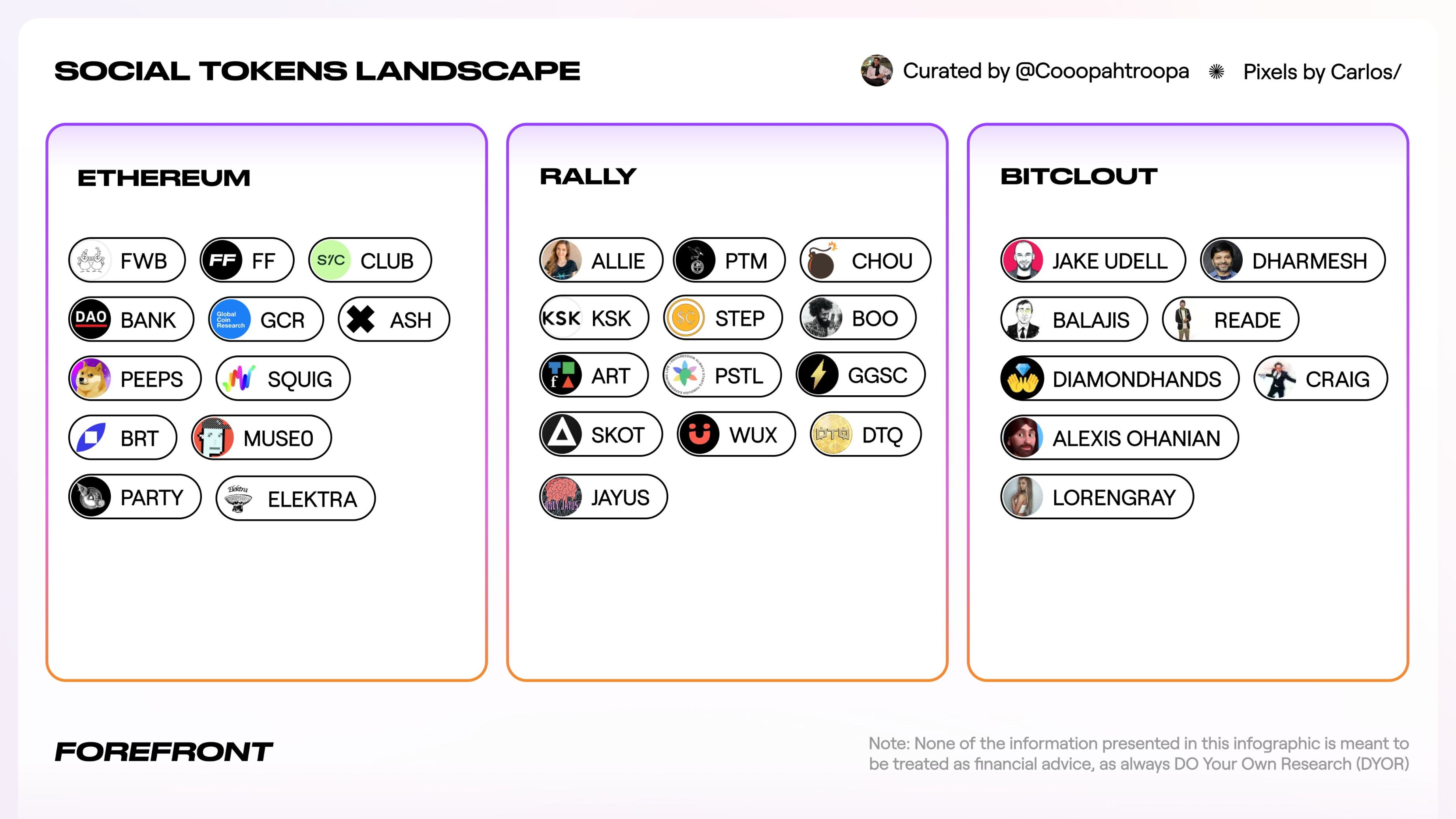

Social Tokens: Introduction, Development History, and Existing Issues

Social tokens represent user participation in some form of community. Communities can form around sports teams, individual creators, or any other shared interests. These communities use social tokens as coordination tools, which can be fungible tokens (FT) or non-fungible tokens (NFT). Homogeneous social tokens are most commonly used as "social currency" within the group, while NFTs are typically used as access to the community.

Source: Cooper Turley

Source: Cooper Turley

Development History and Existing Issues

The above image outlines a brief history of social tokens. Each token offers different value propositions for its community, but ultimately failed to attract users sufficiently for various reasons. These past examples help clarify why social tokens have so far failed to catalyze a bull market.

ALEX

The ALEX token is one of the earliest social tokens. It was issued by Alex Masmej, the current founder of Showtime, in April 2020. The "Initial Alex Offering" of the ALEX token raised $20,000 to fund his move from Paris to San Francisco and to launch his next startup project. In exchange, Masmej offered token holders three rights: a share of the money he earned over the next three years (up to $100,000), the power to vote on certain life decisions, and the right to request promotions using Masmej's social media.

Issues with the ALEX Token

This is likely your first time hearing about the ALEX token. As one of the earliest social tokens, the ALEX token could never catalyze a large-scale bull market, especially with a target fundraising size of only $20,000, which was not aimed at attracting the general public. Furthermore, there was no mass-market platform to facilitate fundraising, such as a "Uniswap for social tokens." Early platforms like Roll had yet to crack the "code" for mass adoption.

Social tokens need to provide stronger discoverability and optimized user experiences for future users to succeed.

ASH Token

ASH was launched by renowned crypto artist Murat Pak in June 2021 and is an early example of a multi-faceted tokenized community. The burn.art platform only mints ASH tokens when users destroy NFTs. Users can receive 1,000 ASH tokens for destroying 1 Pak NFT, while destroying other types of NFTs yields 2 ASH tokens. ASH can then be used as a form of currency to mint new NFTs issued on the burn.art platform.

As the project gained notoriety, several well-known partners participated in the second NFT issuance—ultimately creating a lineup of renowned crypto artists including FVCKRENDER, Coldie, and Mad Dog Jones, with even Paris Hilton joining in.

Issues with the ASH Token

Pak's burn.art platform attracted a group of artists to join its community, but it failed to develop a larger community, partly because Pak did not particularly commit to developing the project. After the second issuance, Pak stopped tweeting about the project, leading it to ultimately fade into obscurity. Future platforms based on social currency must continuously provide value; otherwise, they will be fleeting.

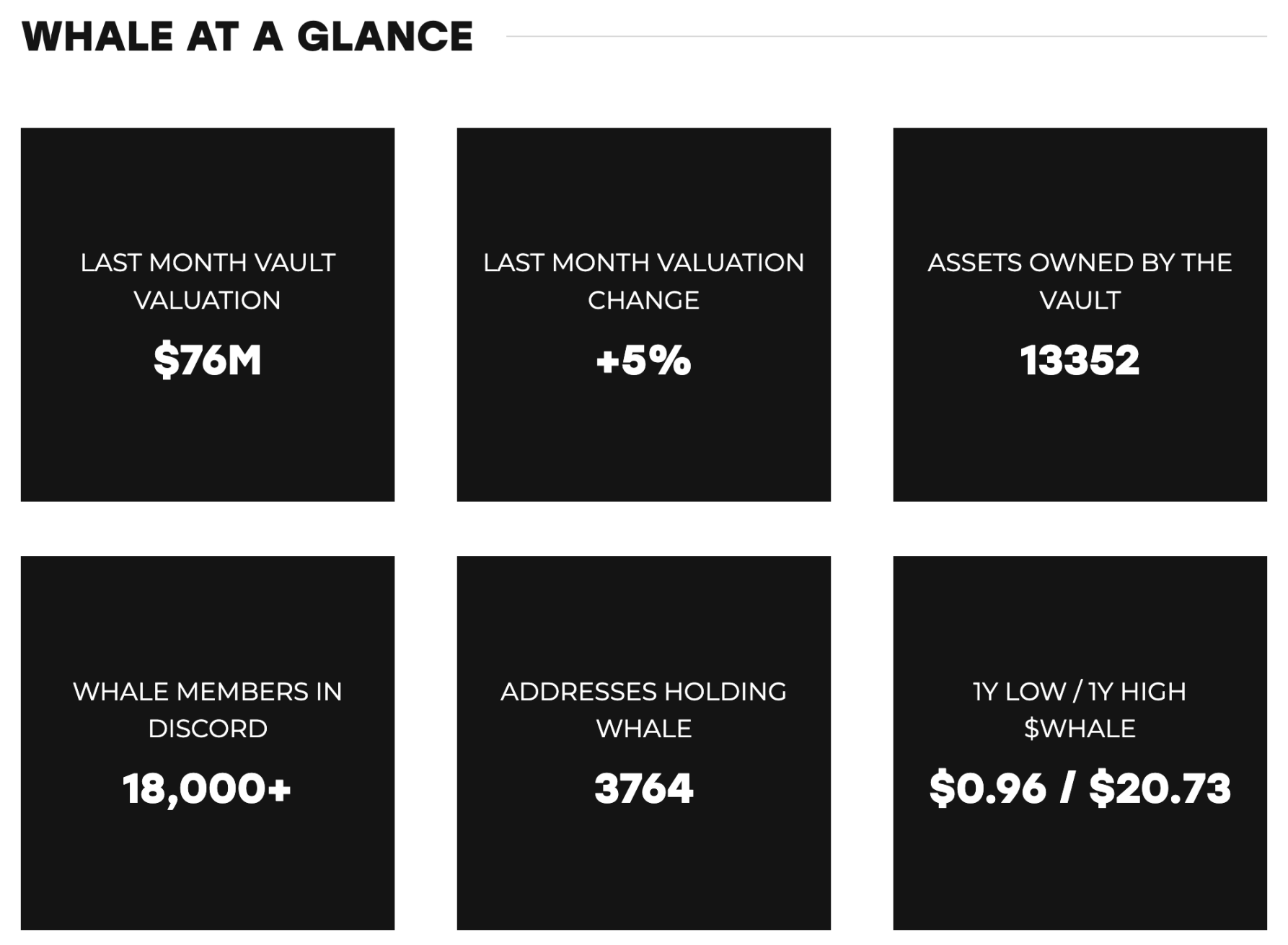

WHALE

WHALE is another art-themed token. WHALE was issued by NFT collector WhaleShark in the summer of 2020. The WHALE vault associated with the WHALE token has grown to a valuation of $76 million. Unlike the ASH token, the WHALE token has no special burn/mint features—users can purchase it on the secondary market or buy it from existing holders on Discord.

Source: Whale

Source: Whale

Issues with the WHALE Token

Despite the vault's valuation of $76 million, the trading volume of the WHALE token is only $11 million. The reason for this is that token holders do not own the vault—the vault belongs solely to WhaleShark. The lack of community ownership leads to a complete disconnect between the vault's valuation and the token. Shared ownership is a great idea—provided that the group sharing can share ownership of its assets.

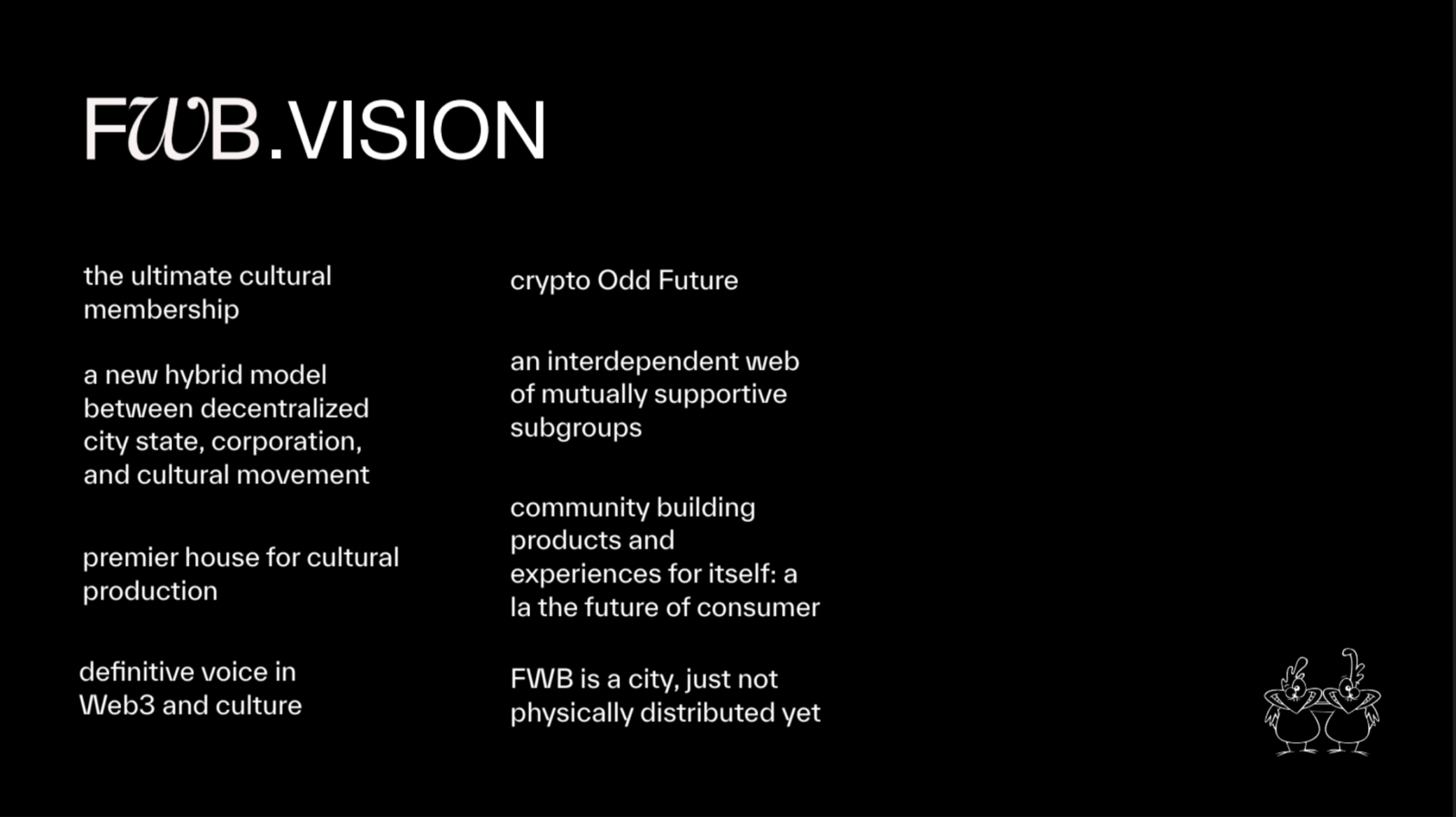

FWB

Friends With Benefits DAO describes itself as "a network of collaborators, a community of communities." It created the FWB token to "incentivize community participation and create collective value." In reality, the FWB token is used to access FWB-sponsored events and the entire FWB community. To become a community member, one must always hold 75 or more FWB tokens.

Source: FWB Roadmap

Source: FWB Roadmap

As more influential cryptocurrency-native users joined FWB, interest in it grew. So much so that a16z led a $10 million funding round for the platform at a $1 billion valuation in October 2021. It now seems that this was not a wise decision.

Issues with FWB

Why has FWB's momentum faded? Unlike ASH's lack of direction, FWB's issue lies in its overly grand vision. Its funding roadmap outlines several bold visions for the protocol's future, including becoming "a new hybrid model between decentralized city-states, companies, and cultural movements." However, the current product essentially consists of a paid-access Discord channel and rights to participate in some parties around the world. A grand roadmap can generate short-term momentum, but short-term momentum does not necessarily translate into long-term success; a more moderate approach should be taken to move forward and manage community expectations.

Improvement Journey: Adoption Cases of Social Tokens

In summary, the main issues that plagued early social tokens were a lack of attention, discoverability, and utility. To spark the next bull market, new social tokens should seek breakthroughs in these areas.

Attention and Discoverability

ALEX represents a newcomer hoping to provide economic benefits to early followers in their ongoing growth—but this is just one potential characteristic of individual social token issuers.

Overall, the cryptocurrency and internet space is filled with individuals who have already amassed a large following and wish to profit from those followers. The more influential individuals adopt the social token model, the more significantly attention can be increased.

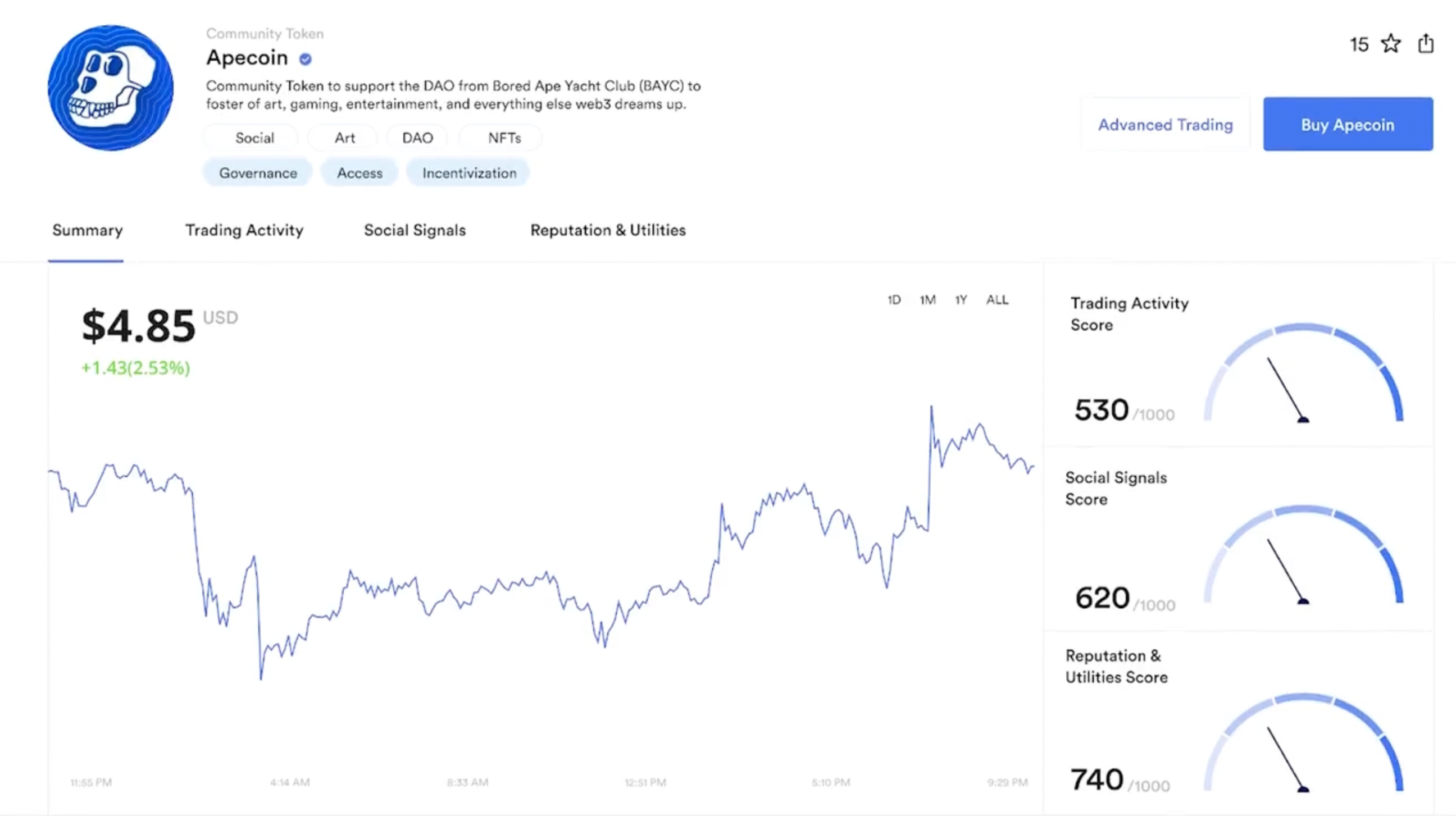

The same goes for the discoverability issue. Success in the crypto vertical is often driven by exchanges, as they simplify the user experience, making it easier for users to discover such assets, just like long-tail tokens on Uniswap or NFTs on OpenSea. Social token-specific exchanges like Rally and TryRoll have yet to fully realize the user experience needed for ordinary users to discover social tokens. One approach to solving discoverability comes from the upcoming social token exchange Purple Trader.

Screenshot of Purple Trader demonstration

Screenshot of Purple Trader demonstration

Purple Trader aims to address the discoverability issue by presenting users with easily understandable social token analytics on the platform. Theoretically, combining exchanges with analytics will catalyze greater demand, as users gain a clearer understanding of the assets they are purchasing.

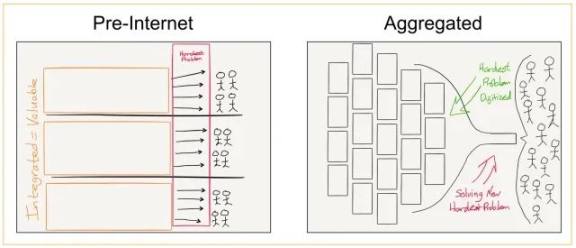

Purple Trader also has the advantage of being an aggregator. Due to timing issues, aggregators have failed in other chain markets—when aggregators like 1inch for ERC-20 tokens or Gem for NFTs entered the market, individual exchanges like Uniswap and OpenSea had already gained first-mover advantages for traders and liquidity providers. Social tokens currently lack such exchanges. In this case, aggregators should win based on the internet aggregation theory.

Source: On Aggregation Theory And Web3

The Socios.com ecosystem adopts another method to enhance discoverability. Socios' Chiliz blockchain hosts fan tokens for popular football teams around the world, allowing fans to gain exclusive promotions and rewards related to the respective teams. While these benefits are not groundbreaking innovations, Socios.com’s partnerships with various football clubs and leagues may create wonders during this year's World Cup.

Entering the 2022 World Cup year, Socios has partnered with teams like Argentina and Portugal, which are the teams of Messi and Cristiano Ronaldo, respectively. These players are among the most famous athletes in the world, with billions watching their matches. In other words, the World Cup will be a massive marketing opportunity for Socios, the Chiliz blockchain, and the entire fan social token ecosystem.

Utility

To some extent, WHALE, ALEX, and FWB serve as early proof of concepts for future communities. Future communities have the opportunity to enhance project value by replicating these early cases while adding new utility to their tokens. In DeFi, token trading volumes rarely fall below 6-7 times their treasury value because governance enables the application and liquidation of treasury assets.

While tokens like WHALE do have some governance functions, financial management is not included in the governance content. It is easy to imagine that a future "decentralized art gallery" could provide some type of decentralized ownership for token holders. In WHALE, the token valuation is limited by the valuation of the assets acquired by the community.

The ALEX token is the first example of an on-chain income-sharing agreement (ISA). However, the design of the token sale minimizes buyer utility by limiting the duration and income applicable to the agreement. Imagine if the company founded by Masmej grew to a valuation of $1 billion, but early investors in Alex would hardly receive any benefits. As ISAs attract more investors, they may diversify their terms.

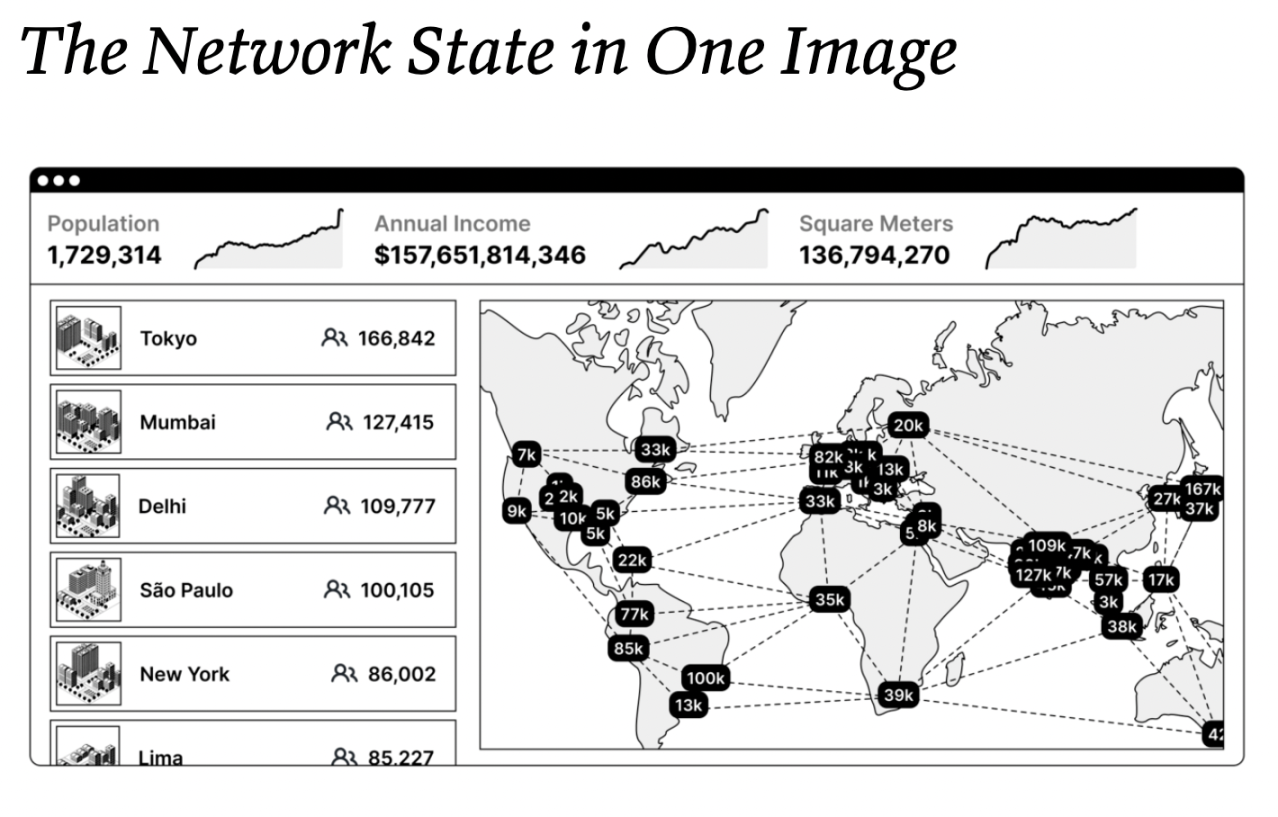

Among the projects mentioned, the most ambitious vision belongs to Friends With Benefits. FWB is one of the earliest attempts to build what Balaji Srinivasan calls a network state, which is "a highly cohesive online community with the capacity for collective action to crowdfund globally and ultimately gain diplomatic recognition from current nation-states."

Now, acknowledging that online communities have the potential to gain diplomatic recognition from existing nations seems absurd, but there are indeed tools to facilitate this outcome—social tokens. Imagine if FWB actually achieved its goal of becoming a hybrid of decentralized city-states, companies, and cultural movements. Imagine if the network state envisioned by Balaji (with 1.7 million members and $157 billion in annual revenue) were all associated with on-chain social tokens; what would the value of those tokens be?

Source: The Network State in One Image

Source: The Network State in One Image

Conclusion

Social tokens are just one of many token distribution mechanisms. At present, few projects are able to attract the attention of the mainstream crowd effectively. Tokens like FWB, WHALE, and ALEX have paved the way for this new vertical, but they have also learned some painful lessons along the way. If social tokens are to lead another bull market, the next generation of projects will need to improve upon the shortcomings of these pioneers in discoverability, user experience, and overall utility to succeed.