In-depth Analysis of Opyn: The Inventor of DeFi Strategies

Although opyn has obvious advantages and disadvantages, it can still be expected as a pioneer of innovation.

Although opyn has obvious advantages and disadvantages, it can still be expected as a pioneer of innovation.Author: Yuky, W3.Hitchhiker

## Project Introduction

Introduction:

Opyn is a decentralized options protocol platform based on Ethereum, where users can earn profits through options trading or providing liquidity. Opyn allows users to buy, sell, and create options on ERC20 tokens. It is a non-custodial options protocol and also a permissionless insurance protocol.

Opyn has gone through iterations of V1 and V2, both of which have essentially been declared failures. Now, the Opyn team is shifting focus to a new direction, Squeeth.

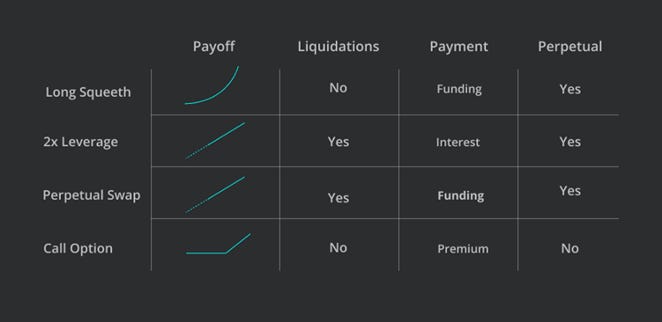

Squeeth is a derivative product introduced by the team that serves as a perpetual inheritance in DeFi, tracking the squared value of an underlying asset. The product is based on the "perpetual" contract concept proposed by the renowned research institution Parath on August 21.

Financing:

$2.16 million in 2020, led by Dragonfly

$6.7 million in 2021, led by Paradigm Series A

Team:

## Strategies

2.1 Long only

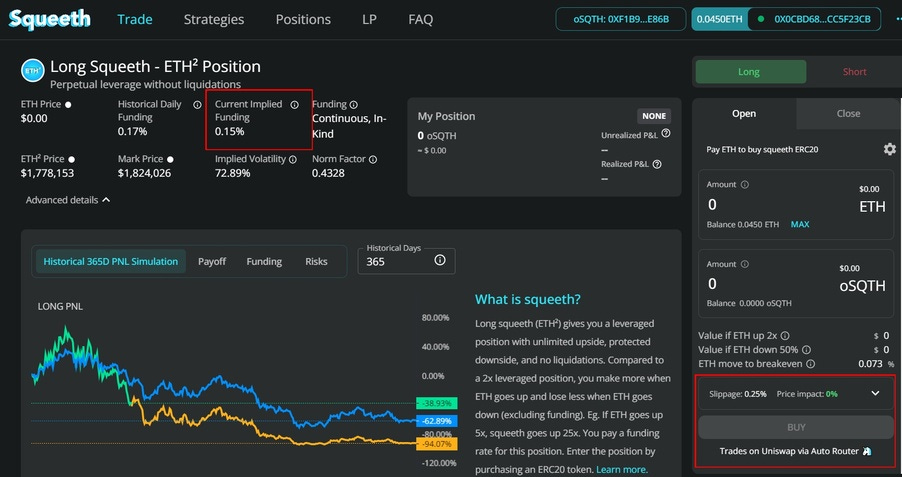

Buy oSQTH tokens on the Opyn platform, with the underlying asset being ETH^2 (an index, gamma > 0, delta > 0).

Opening position: ETH - oSQTH

Closing position: oSQTH - ETH (on Uniswap or Opyn platform)

Position: Long oSQTH

Squeeth price = 10,000 * (_oSQTH price in USD) / (normalization factor)*

Return: Long squeeth return ≈ 2r + (r)² - funding

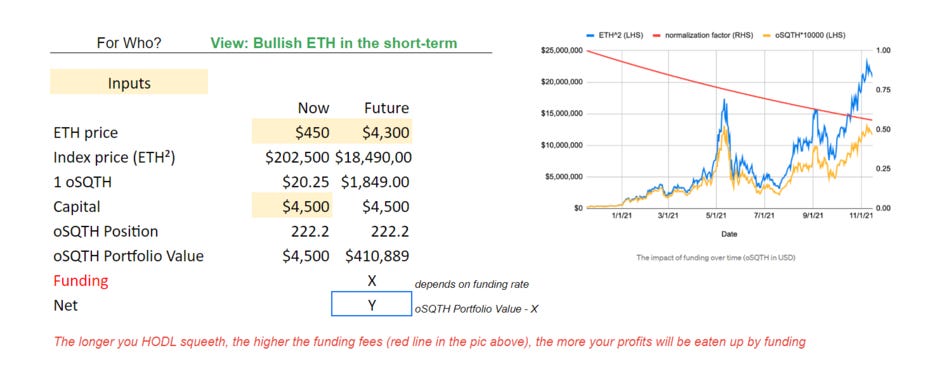

Example calculation:

- (Data read from Google Sheets link here) *

It is important to note that the funding rate is paid daily (from longs to shorts), equal to the funding on the platform, in-kind, thus it is not suitable for long-term investment (as the red line will reduce returns unless there is exponential market movement).

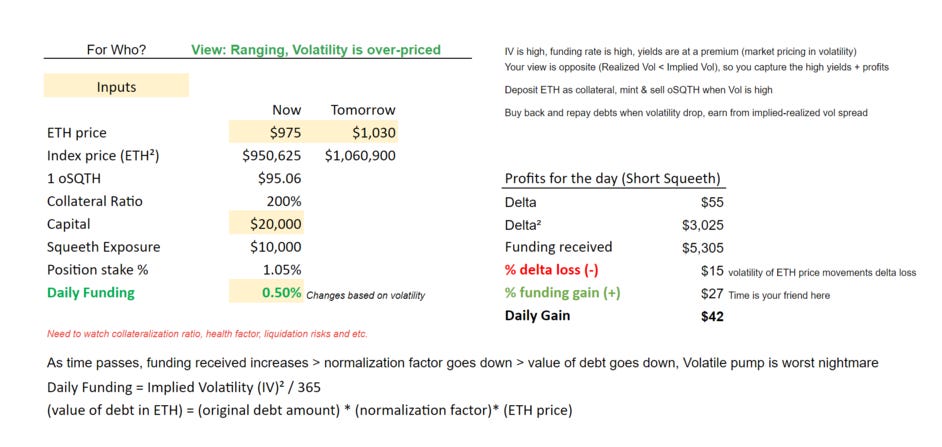

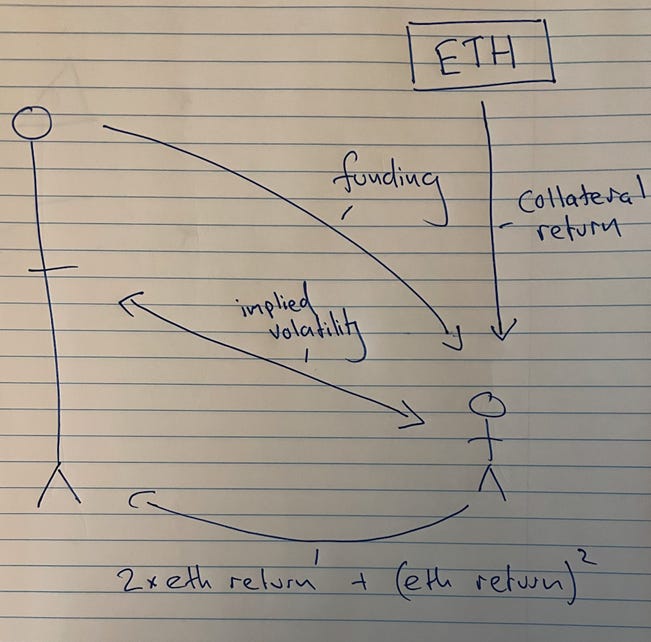

2.2 Short only

This situation is a bit more complex;

A short position requires at least 6.9 ETH as collateral, with a collateral ratio (CR) between 150% - 300% (below 150% triggers liquidation).

Opening position: collateralize ETH, receive funding rate (gamma < 0, delta < 0)

Closing position: eliminate the contract, redeem ETH

Position: Short oSQTH

Return: Short squeeth return ≈ -2r - (r)² + funding + CR * r

Example calculation:

- (Data read from Google Sheets link here) *

The short oSQTH has negative delta and gamma, thus exhibiting a characteristic of losing more on declines than gaining on rises, but the funding and staking ETH returns can offset some losses (in a rising market). However, due to the minimum collateral requirement of 6.9 ETH, it is not accessible for retail investors.

Summary: We use a simple image to describe the situation of both long and short sides.

Or in the form of counterparties:

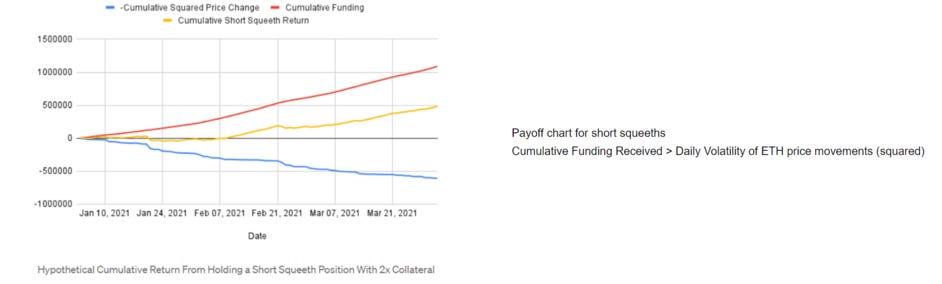

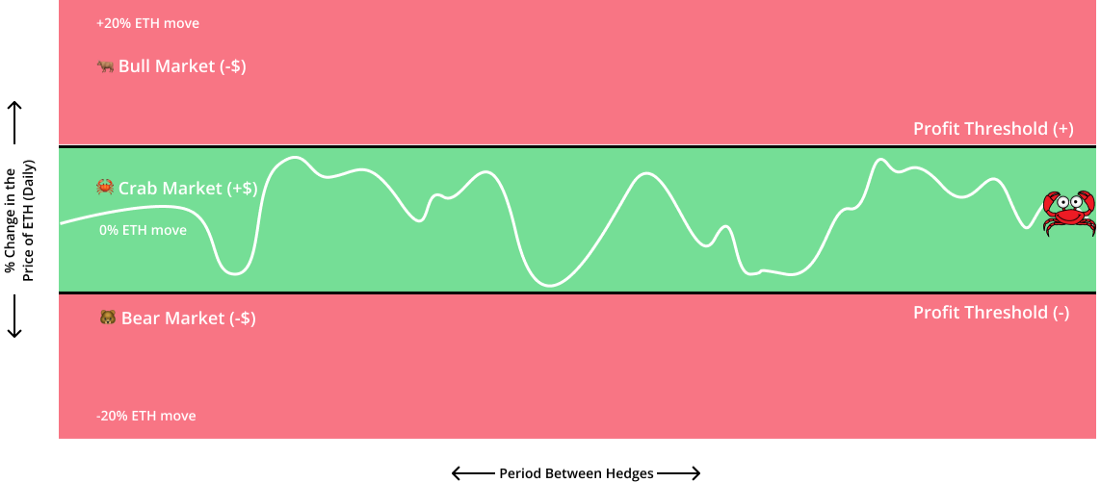

2.3 Crab Strategy

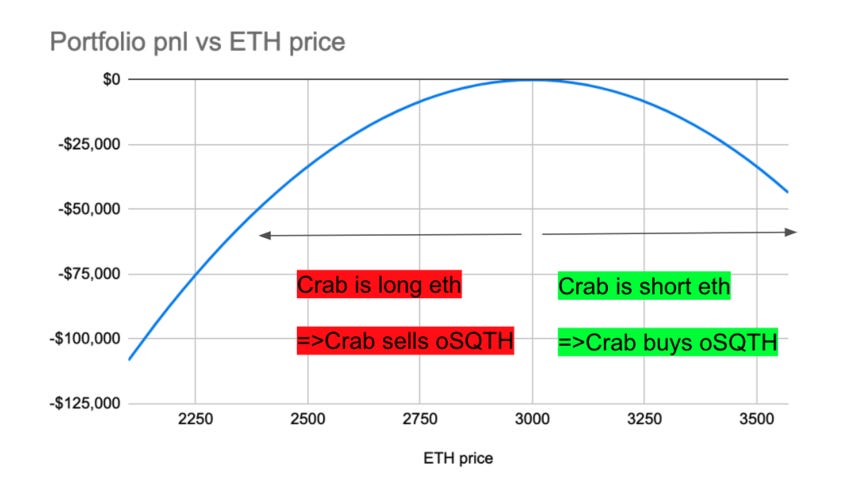

The Crab Strategy is a new strategy introduced on Opyn for sideways markets, with the position being: long ETH + short oSQTH (delta hedge, gamma < 0).

Dynamic Adjustment (Here is a derivation process)

It acts as a self-stabilizer or buffer zone,

Essentially, it is a strategy for shorting implied volatility;

Return (daily): Crab return = funding - (ETH return)²

Annualized return: *E(Crab apy) = 365 * funding - (variance of ETH)*

The graphs are as follows:

Arbitrage Form of Crab Strategy: Auction

The Crab Auction is divided into "buy" and "sell" types to balance the Crab Strategy.

Buy: This means using WETH to buy your oSQTH, which is selling from the user's perspective; you need to have oSQTH tokens to participate. (long ETH + short oSQTH)

Sell: This means exchanging "excess" oSQTH for WETH, which is buying from the user's perspective; you need to have WETH tokens to participate.

Both will have a minimum starting amount. From the perspective of participants in the auction, for example, you can buy at least 8 oSQTH tokens or sell at least 10 oSQTH tokens, which is the threshold.

The potential arbitrage opportunity is the classic "buy low, sell high." For instance, if you buy WETH to purchase oSQTH sold by the Crab Strategy, the purchase price is generally cheaper than the price on Uniswap at the same time, so you can sell it on Uniswap for a profit. If you buy oSQTH tokens on Uniswap to sell to the Crab Strategy, you need to ensure that your purchase cost of oSQTH is lower than the acquisition price of the Crab Strategy to make a profit. Of course, you also need to pay attention to authorization and transaction gas fees, as well as token price fluctuations during extreme market conditions to ensure you do not incur losses.

"Participating in the squeeth crab auction"

Crab proof calculation table

If ETH price rises → the strategy uses WETH to buy oSQTH

If ETH price falls → the strategy sells oSQTH for WETH

Summary: From a long-term holding perspective, the Crab Strategy is a negatively convex strategy with left-tail risk; however, it somewhat lowers the entry barrier for short sellers of oSQTH. In the short term, the Crab Auction provides opportunities for short-term arbitrage, and the continuous income from the funding rate will improve the return curve.

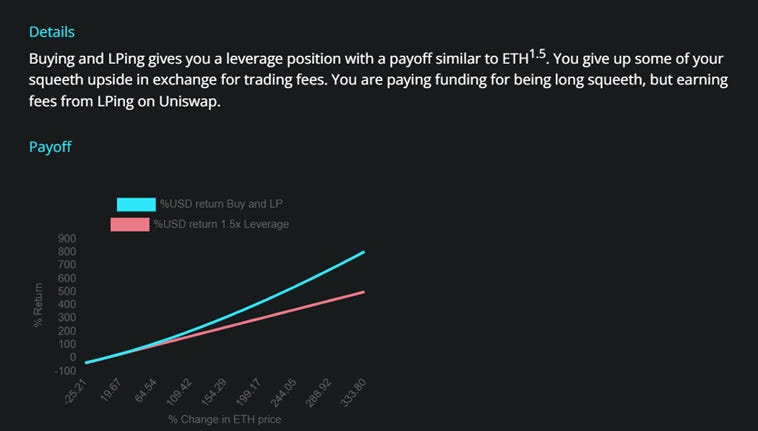

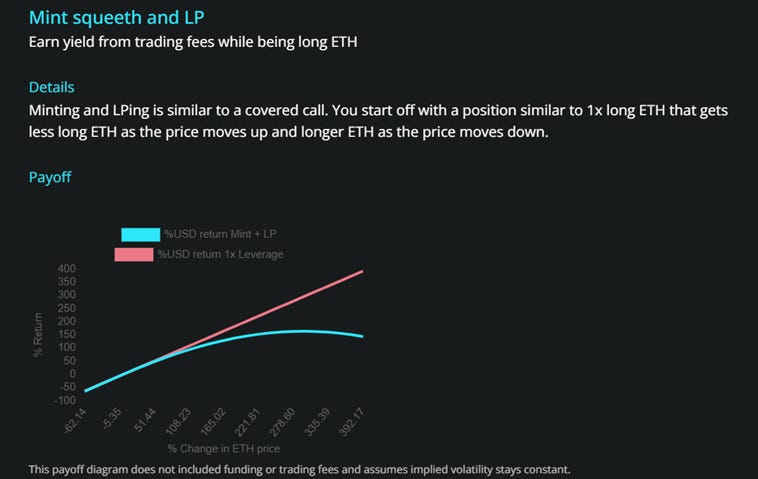

2.4 LP Business

You can choose to inject liquidity into the ETH/oSQTH pair in the Uniswap pool.

There are two methods: Buy and LP and Mint and LP.

If you are optimistic about oSQTH, you can choose the Buy and LP method. Due to the nature of LP on Uniswap, the ETH position is not fully allocated to oSQTH, so the return curve resembles tracking an index of ETH^1.5 (essentially a partial long position in oSQTH). The return graph is as follows:

If you are not optimistic about oSQTH, you can choose the Mint and LP method, which involves collateralizing ETH to obtain oSQTH, and then doing LP on Uniswap.

Covered call (writing a covered call): Position is long ETH + short oSQTH.

Similarly, LP will reduce the Long ETH position, and the short oSQTH has negative convexity, and since oSQTH tracks the ETH^2 curve, the negative convexity effect will become more pronounced over time. The return graph is as follows:

## Highlights and Drawbacks

3.1 Highlights and Outlook

Highlights: Opyn's Squeeth solves two problems: roll down and convexity.

As shown in the figure:

It uses perpetual theory to solve the roll down problem by continuously paying funding from the long side to the short side.

Regarding the derivation of perpetual theory: "Everlasting Options"

Using the square of the ETH price as a tracking index creates convexity (gamma), giving it properties similar to options.

Simple operations also have greater universality.

Outlook: More strategy combinations to attract more professionals to participate; for example, demand for gamma hedging; or the possibility of more derivative combinations emerging after the Opyn platform opens bear and bull strategies (large market), as well as imagination (cooperation with other derivative platforms as a derivative combination).

3.2 Drawbacks

From the perspective of the options platform, profitability is unknown (or limited), and the products created resemble options but are not options (essentially, Squeeth is just a futures index with convexity, different from straddle and strangle options strategies). The product elimination rate is concerning (the options products from V1 and V2 are no longer in demand).

From a strategic perspective: derivatives have a high threshold, making them unsuitable for ordinary investors (few participants); the current strategy content is still too singular, resembling a prototype; insufficient liquidity (liquidity on Uniswap is around $2 million), trading fees (gas), price impact, and slippage are relatively high (around 1.5%); all strategies point to short-term and arbitrage, which is not friendly for investors looking to implement long-term strategies.

## Conclusion

The advantages and disadvantages of the Opyn platform are quite evident.

Advantages:

It has created the index ETH^2 and introduced Gamma, which brings two changes from the market perspective:

One is to attract more professional investors to participate (more professional derivatives traders can have a wider selection).

One is that more derivative combinations can emerge (these combinations could be products of their own platform or cross-platform products). Although this is a small change, it indeed broadens the types and combinations of derivatives in the market.

The project has good professionalism and innovation capability, and we look forward to their Bull strategy and Bear strategy.

Disadvantages:

The platform products have a high threshold for retail investors (economically and cognitively), and increasing user numbers and popularity (promotional efforts, educational efforts) is an important issue for the project team;

The liquidity and depth of the UNI pool are also insufficient;

Issues with trading fees and price impact?

The term structure of strategies is still relatively singular, all pointing to short-term;

The format is also quite singular: currently, it is still primarily focused on arbitrage.

In summary, although the advantages and disadvantages are clear, as an innovative pioneer, there is still some expectation for the project.

References