Using History as a Mirror: Reviewing the Ten-Year Changes in the Blockchain Sector

The cryptocurrency industry has experienced ups and downs over the past decade, from the foundational ideas to the underlying technological basis, and then to the improvement and establishment of application foundations. We believe we are on the eve of a full-scale explosion of blockchain applications.

The cryptocurrency industry has experienced ups and downs over the past decade, from the foundational ideas to the underlying technological basis, and then to the improvement and establishment of application foundations. We believe we are on the eve of a full-scale explosion of blockchain applications.Original Title: “Using History as a Mirror to Understand Rise and Fall: A Review and Outlook on the Evolution of the Blockchain Landscape”

Author: Frank Fan @Arcane Labs, Don @Arcane Labs

Editor: Charles @Arcane Labs

Innovation and development of anything cannot be separated from iterations based on the foundations and problems left by predecessors.

Since the term "blockchain" was born with the Bitcoin white paper in 2009, it has gone through 13 years. From an obscure term to a well-known industry, it has spawned countless flourishing ecosystems and tracks. Through several cycles of bull and bear markets, the industry has evolved from nothing to something, allowing many early players focused on various tracks within the industry to rise and reap enormous wealth. Looking back at the changes in various tracks of the industry over the past few years, we can easily discover the hidden patterns within.

Firstly, it is well-known that the blockchain industry has always been characterized by particularly significant cyclical behavior. During bull market cycles, the industry thrives, continuously generating bubbles. In bear market cycles, the industry becomes very quiet and bleak, rapidly clearing out. The timeline has often been marked by Bitcoin halving events, accompanied by a frenzy of capital pouring in and out, forming an industry pattern of bull and bear cycles every four years.

In each cycle, aside from the unchanging narrative of Bitcoin halving, we can also observe unique industry changes that serve as the main line of industry development.

For example, we have previously experienced three cycles:

The first was the value discovery of decentralized commodity currency led by Bitcoin;

The second was the value discovery from purely decentralized currency to decentralized smart contract platforms;

The third was the value discovery as users began to shift towards on-chain behavior and decentralized foundational applications.

1. The First Three Cycles Experienced by the Blockchain Industry

1.1 Enlightenment Stage of Decentralized Commodity Currency (2010-2013)

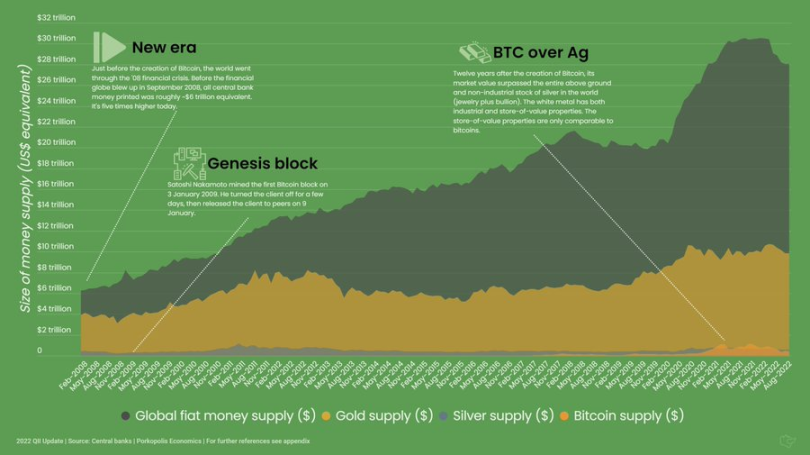

Looking back at history, in the first crypto cycle, Bitcoin, as the pioneer of the entire industry, gradually entered people's view due to its anonymity, decentralization, and the scarcity of its fixed total supply. Its narrative value as a means of cross-border transfer and digital gold also began to gain recognition from more and more people. "Bitcoin as gold, Litecoin as silver" was the best interpretation of the enlightenment phase of decentralized commodity currency at that time.

It was also due to the 2008 financial crisis that people's trust in traditional finance began to fracture. Early participants in the cryptocurrency market were more inclined towards hardcore geeks, and compared to the capital that has widely ventured into the cryptocurrency market today, early market participants had a very high demand and belief in decentralization.

This stage was more of an enlightenment phase of the decentralized ideology.

1.2 Emergence Stage of Smart Contract Platforms (2014-2017)

In the second crypto cycle, the main focus was on the value discovery of blockchain smart contract platforms represented by Ethereum during the initial coin offering (ICO) era. From its inception to the first discovery of its financing value, Ethereum was followed by a host of Ethereum killers, such as well-known projects like EOS, Tron, and ADA. This stage was dominated by the concept of "blockchain," a wild period where only a few blockchain smart contract platforms had consensus value for their native coins, and there were very few applications on the platforms, with the token values of these applications largely unrecognized. Users quickly exchanged the tokens they earned back into the platform's native coins. Activities across various chains were extremely tepid, with most users primarily engaged in "trading" on centralized exchanges. Finding killer DApps was a recurring theme mentioned by many blockchain practitioners at various industry conferences.

This stage was the true beginning of the blockchain concept stepping onto the historical stage.

1.3 Basic Stage of DApp Applications (2018-2021)

The third crypto cycle, which is the most recent one. The most noticeable change in this round was the evident prosperity of on-chain ecosystems and user activities on-chain. The most intuitive feeling was that many trading users, when mentioning a token they were unfamiliar with, no longer asked which centralized exchange it could be traded on, but rather inquired about the contract address on the token's chain. What sounds commonplace now was unimaginable in the previous cycle.

This was thanks to the improvement of some decentralized foundational applications on-chain during this cycle. Starting from the well-known DeFi Summer, the two major weapons of AMM automated market maker mechanisms and liquidity mining completely opened the era of on-chain DeFi prosperity. The subsequent stories are well-remembered; throughout 2021, on-chain applications like DeFi, NFTs, and GameFi took turns becoming the hot topics of the bull market. Additionally, the brief meme craze initiated by Doge and Shiba, along with the wealth effects brought by airdrops from projects like Dydx and ENS, were also significant drivers of the prosperity of on-chain activities in this cycle.

By this stage, the DeFi infrastructure on-chain had basically been established, with relevant leaders emerging in trading, lending, and other products. DAOs were still in the nascent stage of thought, with products yet to mature. NFTs were situated between DeFi and DAOs, having explored a relatively mature successful path with PFP avatars but needing to expand into more successful scenarios for further development. This is the current state of what was once referred to as the three pillars of blockchain applications.

Currently, on-chain applications in this cycle have reached a bottleneck, with most related applications being minor innovations and patches based on predecessors, resulting in significant homogenization. Moreover, in the later stages of this crypto cycle, the market's speculative hotspots began to lean towards more grand narratives, such as the metaverse and Web 3.0, which is a typical sign that innovation on the product side has begun to lose momentum. Of course, we are still in the early stages of the blockchain industry; if we were to compare it to a person's growth, it resembles a teenage phase. Everything is still foundational, just beginning to have various segmented paths.

This stage has laid a solid foundation for more diversified DApp applications in the future. It is also during this cycle that the term "track" began to have substantive meaning.

2. The Initial Stage of Comprehensive Blockchain Application Explosion

The next cycle will mark the preliminary value discovery of comprehensive blockchain application.

The comprehensive development of applications will make the blockchain industry more mainstream, and only by continuously mainstreaming can the industry bring exponential user growth. Against the backdrop of the current macroeconomic downturn and the disappearance of the internet industry's demographic dividend, with the popularity of Web 3.0 as a new synonym for the blockchain industry, the industry has also received unprecedented attention from both old and new capital. Additionally, some public chain platforms that have already settled down in this cycle, newly capital-intensive public chains, and narratives like Ethereum's Merge followed by Rollup and Danksharding, under the impetus of capital and the accumulation of technology, have shown us a glimpse of the dawn of large-scale blockchain applications in the future.

The industry's further move towards mainstreaming also requires strengthening in these three areas:

a. More scalable underlying blockchain technologies and platforms to handle and run more complex blockchain applications

b. Regulatory and compliance policies that are more compatible with the crypto industry to bring in more mainstream capital and funds

c. Further lowering the entry barriers for newcomers to the crypto industry and optimizing the experience of entry products to facilitate the influx of more mainstream users

Of course, Rome wasn't built in a day. Looking back at the explosive narratives of several cycles, it has also spiraled around several dimensions.

2.1 Products and Concepts

Excellent blockbuster products are the premise for the explosion of corresponding tracks, and the rapid growth data exhibited by products themselves is the best story. For example, Uniswap and Compound for DeFi rapidly increased on-chain TVL by an order of magnitude; Axie Infinity for GameFi saw its revenue surpass that of the top Web 2 mobile game "Honor of Kings" in a short time; Sandbox and Decentraland for the Metaverse; CryptoPunk and Bored Ape Yacht Club for NFTs, etc. In contrast, many tracks have yet to explode, primarily because there are no blockbuster or market-validated products in those tracks. Of course, in a bull market, liquidity is rampant, and many immature concepts will be repeatedly speculated upon, and the speculation of concepts can also help attract more people to participate in product development, ultimately sifting out better products.

Moreover, truly paradigm-shifting products, at least in the current view, only appear once in each cycle. Bitcoin in the first cycle, Ethereum in the second cycle, and Uniswap in this cycle.

2.2 Applications and Infrastructure

The development of applications and the development of underlying infrastructure must be compatible and mutually beneficial. The development of applications relies on the continuous optimization of middleware built on underlying infrastructure technologies and providing certain service guarantees. The development of infrastructure, in turn, depends on the prosperity of applications built on top of it or served by it. For example, the rapid development of DeFi and the demand for DeFi fund security have not only solidified Ethereum's position as the No. 1 public chain but have also led to explosive growth for middleware and tools like ChainLink and The Graph. Applications like GameFi are more suited to be built on newer public chains like BSC, Avalanche, and Solana, which have lower transaction fees and faster processing speeds. Current applications are still mostly at a relatively simple logical level, and I believe that in the next cycle, more applications capable of handling more complex logic, along with matching infrastructure, will emerge.

2.3 Issuance and Circulation

The biggest difference between Web 3 and Web 2 is actually the Token (i.e., the essential difference between assets and information). The issuance and circulation of Tokens and their economic models are issues that every Web 3 entrepreneur cannot avoid. Over the years of industry development, the methods of Token issuance and circulation have also been changing. In terms of issuance, it has evolved from the earliest POW/POS consensus mechanism mining to later ICOs and IEOs for financing issuance, and now to the current DeFi liquidity mining and GameFi gold mining, as well as the popularity of various public offering platforms for IDOs and airdrop token issuance. The increasing entry of venture capital has made the issuance of Tokens for projects and multiple rounds of financing followed by IPO listings almost unquestionable, presenting a diversified state of Token issuance methods.

In terms of circulation, it has transitioned from the earliest decentralized OTC trading models to centralized exchanges facilitating trading, and now to decentralized exchanges, with mainstream trading models solidifying into centralized order book trading and decentralized AMM.

Whether the final form of the industry's Token issuance and circulation model will be like this remains to be seen. However, as the two most fundamental demand attributes of assets, every change in the Token issuance and circulation model can trigger significant changes in the industry, generating substantial wealth effects. We hope to continue seeing innovations in this dimension in the next cycle.

The preliminary value discovery of comprehensive blockchain applications also indicates some possible trends: in the next cycle, first, the degree and rules of industry changes will become more complex, and many things that were once regarded as rules in this industry may also be broken. I believe that many investors who have been "carving the boat to seek the sword" through on-chain data in the secondary market have already experienced this; secondly, the time required for product and technical innovation and maturity may be longer than before. Therefore, I also suggest that industry colleagues be fully prepared for long-term building and have sufficient capital reserves.

3. Predictions and Judgments on Hot Industry Tracks

3.1 Rollup and Other Scaling Solutions

In terms of blockchain scaling, there are many technical solutions and teams that have been building continuously. From earlier improvements to consensus algorithms to L1 sharding solutions, and now to the layered design of L1, L2, and L3, the most mainstream solution in the layered approach is Rollup. At the end of 2020, Vitalik Buterin published an article titled "Ethereum Roadmap Centered on Rollup," and in 2022, he reaffirmed the development status of the Rollup route at the ETH Shanghai Summit, with technologies like Danksharding specifically prepared for Rollup. Currently, Rollup is divided into Optimistic Rollup and ZK Rollup.

Optimistic Rollup is relatively easy to be compatible with EVM and supports general contracts, but the exit time from the network is relatively long. We can see that the representative projects of Optimistic Rollup, Arbitrum and Optimism, have already built a good ecosystem with many projects on them. At the same time, due to its exit characteristics, many third-party cross-chain bridges have found a good market.

On the other hand, Zero-Knowledge Proof technology is currently a track that capital is competing to invest in. From a technical perspective, ZK is a verification technology that allows the verifier to confirm that a proof is valid without the prover revealing any information about the proof itself. ZK technology was originally used for privacy and has recently begun to be applied for scaling.

ZK Rollup exits the network much faster than Optimistic Rollup, but it is relatively weaker in terms of EVM compatibility and support for general contracts, so current representative projects like ZkSync and StarkWare are still in the preparation stage.

In terms of performance, ZK Rollup is slightly higher than Optimistic Rollup, while the difficulty of ecosystem migration is easier for Optimistic Rollup than for ZK Rollup. This has led Vitalik to publicly express a short-term preference for Optimistic Rollup while focusing more on the long-term performance of ZK Rollup.

In fact, regardless of the type of scaling platform, the ultimate goal is to provide users and developers with a better experience, thereby building a prosperous ecosystem on top of that. The scaling competition is far from over, which is why I define the next cycle only as the initial stage of the comprehensive explosion of blockchain applications. We believe that the next generation of scaling solutions led by Rollup will continue to present a diversified pattern, and diversified infrastructure will be more conducive to the flourishing of applications and ecosystems.

It is worth noting what kind of different native applications will emerge based on new scaling solutions or architectures, especially in the derivatives and gaming fields, such as dedicated chains like Arbitrum Nova.

3.2 DID

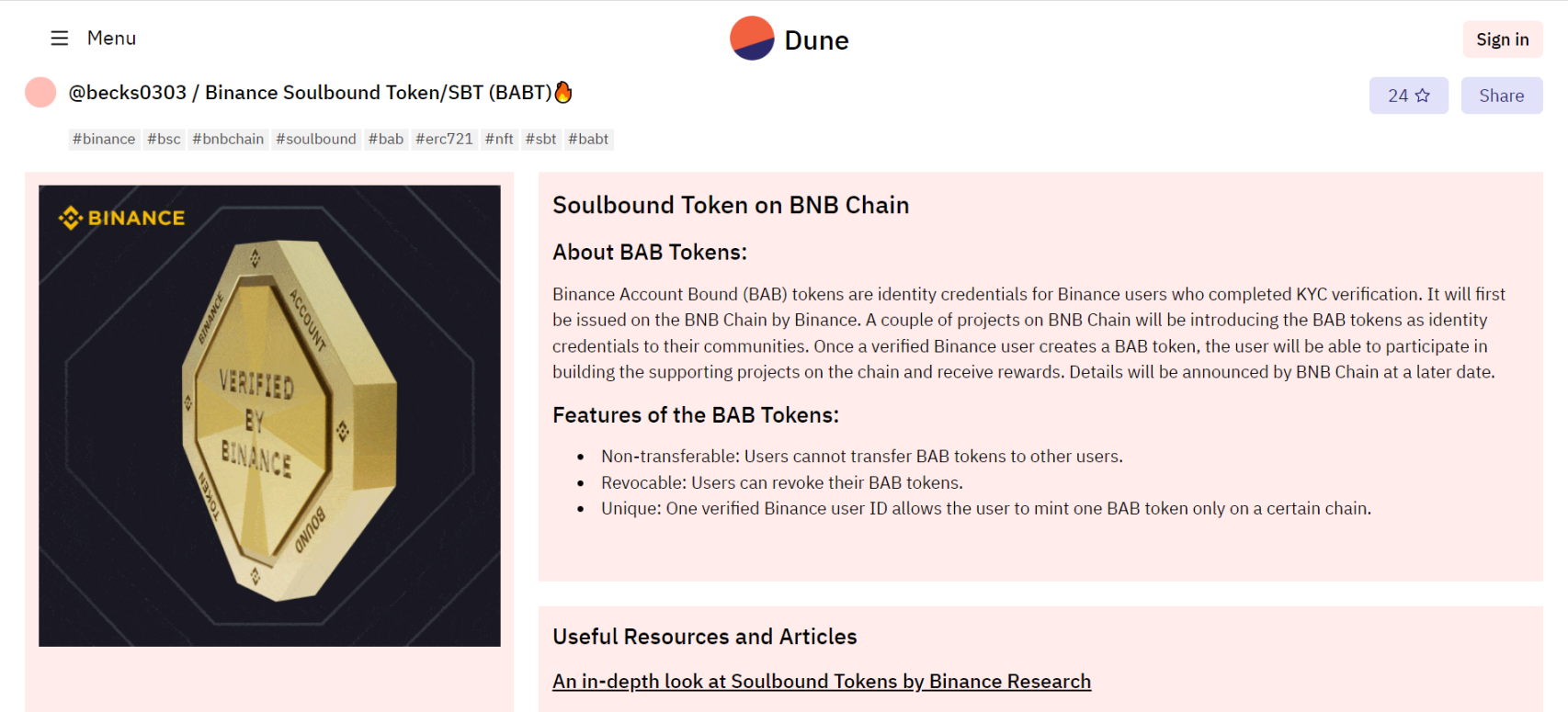

DID, or Decentralized Digital Identity. This concept has been proposed for quite some time, and this year, Vitalik introduced the concept of SBT (Soulbound Token), with Binance subsequently launching the "Soulbound Token" BAB. These two events have once again brought the DID concept to the forefront of market attention.

Its characteristics need not be elaborated upon; purely from the narrative and practicality perspective, a mature and widely used DID product in the future may be a necessary infrastructure for the entire industry to move towards greater mainstream acceptance.

For building decentralized social networks, on-chain KYC, on-chain credit systems, unsecured lending, and compliance with regulatory requirements, there may be some wonderful sparks with DID.

When it comes to DID products, directly transferring the KYC solutions and experiences from Web 2 to Web 3 is absolutely unfeasible. Project teams need to pay more attention to the organic integration of user interaction behaviors and data on-chain. Capturing users through a specific demand is essential.

3.3 GameFi

GameFi was an exceptionally hot track in the second half of last year. However, the good times did not last long, as retail investors' frenzy turned chain games into the last leg of this bull market. Now, investment in the gaming track has become one of the most controversial areas among institutional investors. Looking back at chain games, it is now well understood that GameFi 1.0 was essentially DeFi mining disguised as a game, or even a Ponzi scheme. Due to the gaming facade of GameFi, many participants engaged in it in the form of guilds (which can be understood as mining pools), leading to a lower participation threshold for many who are not well-versed in Web 3 compared to DeFi, as they only needed to entrust their funds to the guild. However, the conflict of interest between custodians and investors has harmed many GameFi users.

For the gaming industry, the essence of a game must be fun. This fun, beyond beautiful graphics, is more importantly about designing complex gameplay, interesting game modes, or engaging background stories that gradually immerse players, involving many methods from game theory or psychology.

All chain games last year were certainly not fun; they purely attracted players with high rewards for gold mining, especially in the later stages of the chain game craze, where participants were merely competing on who could achieve returns in a shorter cycle. When the price of tokens began to falter and returns started to decline, until the income became meager, chain game participants could no longer "immerse" themselves in it.

This is not just an issue with certain projects, but rather an overall problem of the current disconnection between the needs and experiences of Web 2 users and Web 3 users. Web 3 users pursue high financial returns, while Web 2 users seek entertainment needs. These two groups are not entirely without overlap; there are many game enthusiasts in Web 3, and Web 2 users also have a demand for making money. These needs cannot be satisfied merely by creating a beautifully designed game and slapping a token on it. Essentially, different strategies need to be formulated for users of different natures, breaking through from a specific point and achieving organic integration.

Returning to the original intention, our recognition of the value of blockchain games is that they can solve the problem of ownership of game assets, allowing users to control their assets. Secondly, they can participate in governance through tokens, ensuring that the game developers do not have absolute authority. These are the values that blockchain can provide once a game has already been recognized by players. Given the current level of Web 2 users' engagement with blockchain, this kind of chain transformation is still somewhat premature. Therefore, creating native Web 3 games makes incentives particularly important. Thus, last year's situation was also an inevitable phase of early incentives moving towards their first extremity.

The next stage may be one of shaping game assets, namely NFTs. Because NFTs themselves are the most aligned with gaming attributes and have the most consumer characteristics, rather than merely treating NFTs as "mining machines" for entry barriers as in GameFi 1.0. With the improvement of the gaming experience in blockchain games and the development of many NFT protocols, the liquidity of NFTs has been enhanced. Games oriented towards NFT value may be the direction for the next round of chain games.

Of course, token incentives will still exist; however, the economic models and values will tend to be more stable and not serve as the primary means.

Conclusion

The crypto industry has experienced a decade of ups and downs, from foundational thoughts to underlying technological foundations, and now to the improvement and construction of application foundations. I believe we are on the eve of a comprehensive explosion of blockchain applications. In addition to the hot tracks recently discussed, such as Rollup, DID, and GameFi, areas like DeFi derivatives, NFT liquidity, decentralized middleware, cross-chain foundational protocols, blockchain security, mobile blockchain application products, and DAOs will also see some excellent projects emerge. As a unique incentive mechanism of the industry, Tokens themselves also represent a special business model. Regardless of how the economic model is designed, it has its own cyclical financial attributes. When the resonance of Token business model innovation and product maturation, along with narrative innovation in applications, arrives, we will once again welcome the next major cyclical opportunity.